Summary of key points: -

- Trump draws closer to walking back on tariffs and the war

- Trump and Powell on a collision course

- Kiwi dollar threatens 0.6000 as local economists turn gloomy

- The depreciating US dollar is rapidly approaching a long-term support area

Daily utterings and disparaging remarks from the US President on just about every financial/economic matter you can think of continues to dominate the short-term movements in global financial and investment markets. The markets are still reacting, however ones gets a sense that the markets are rapidly becoming bored with his non-sensical “hoodoo economics” which ignores every economic, technological, business and investment advancement around the world over the last thirty years.

The only succinct way anyone outside the US can describe the narcissistic idealogue now leading the US Government, is that he has “no understanding” and “no respect”. Like most commentators, we have run out of adjectives in an to attempt to describe his dictatorial disregard for the rule of law and unsubstantiated criticism of all and sundry. His chaotic approach to go to the extreme ends of any negotiation or position, unfortunately for Mr Trump, is now starting to bite him in the rear end. A continuation of his ridiculous tariff policies will drive the US economy into recession within a few months unless he quickly agrees some trade deals with the US’s major trading nations. Despite Trump writing a book many years ago on the art of “negotiation”, as a so-called property tycoon his business deals were in fact years apart on property transactions. Therefore, he has no idea of how to leave something on the table to oil ongoing, continuous and harmonious business relationships where both parties come away with what they want. His idea of business between companies and business between countries is “I win; therefore, you must lose!”.

Latest indications are that President Trump is prepared to compromise to settle a new set of trading relationships with the UK and Europe. The US versus China trade war stand-off continues, however there are indications from Trump’s cryptic mutterings last week that at least the Chinese and US officials are getting closer to agreement on how they might start to conduct a trade negotiation.

Trump’s “bully-boy” threatening tactics is to force other countries, who are dependent on trade with the US, to reduce their import tariffs and non-tariff barriers to allow increased US exports to those counties. Anyone sitting in New Zealand, as one of the pioneers of free-trade agreements, would have to agree that Trump is doing a good thing as the dropping of import tariffs allows greater access for New Zealand’s export product. We have long pushed for greater non-tariff access to foreign markets like India, Canada and Japan. There is a lot more water to go under the bridge on the US’s demands to restructure global trading relationships. We would have to agree with our Deputy Prime Minister, Winston Peters, that New Zealand should just be patient and this point and keep its head down. The revised new world order on trade may be to our net advantage as a trading nation.

What happens next on Trump’s trade negotiations with Europe and China is important for the future direction of the Australian dollar, and therefore the dutifully following Kiwi dollar. A compromise solution on the current 145% plays 125% stand-off between the US and China would be seen as positive for the Chinese economy as their manufacturing exporters can stay in business.

Any good news for the Chinese economy is always a positive for the AUD exchange rate.

The Aussie dollar has been left behind by other major currencies (EUR, JPY and GBP) in the heavy US dollar sell-down over the last three months because of its close alignment with all things China. A massive AUD catch up (maybe after their general election on 3rd May) is shaping up to be a standout feature of currency movements over the weeks ahead. What Trump and the western media continue to inexplicably underestimate is the sheer size and power of the Chinese economy. Exports to the US are only 15% of their total exports and they can easily replace that loss of business with monetary and fiscal stimulation to domestic spending. There is a school of thought within China that the introduction of tariffs on their US exports might be a positive development as it will force a move away from low margin/low value toys, clothes and furniture into Walmart. China wants to replace those exports with more value-added product. The Chinese, off course, have extreme patience and fortitude, something that the Trump regime is already displaying that they are seriously short of.

Remember the claim made by Trump in his election campaign that he would end the Ukrainian/Russian war within 24 hours. His latest statement on the war is “If for some reason one of the two parties makes it very difficult, we’re just going to say, ‘you’re foolish, you’re fools, you’re horrible people,’ and we’re going to take a pass,”. He will walk away unless he gets immediate results that fill up his ego. The same impatience is likely play out in the trade arena as well, as more evidence comes in front of Trump and US voters that the US economy is being damaged by his policies and is nose-diving towards recession.

Trump and Powell on a collision course

Jerome Powell and the US Federal Reserve find themselves in a right pickle with inflation increasing (due to Trumps’ consumer tax/tariffs) at the same time economic growth is softening, and employment is weakening. The Fed over recent years have been adjusting monetary policy settings solely based off historical economic data. What is challenging for their current stance is that historical actual inflation is falling back to their 2.00% target more rapidly than what they were expecting. Therefore, monetary policy no longer needs to be restrictive. In a speech last week, Powell indicated that the tariffs are much larger than they expected, and likely future employment and inflation trends will be pulling in opposite directions.

“What to do, what to do?” – Faced with the dilemma in front of them, the Fed are most likely to do what most would do i.e. nothing. Two consecutive months of weak employment data (which seems likely with the number of US companies now indicating worker lay-offs) should be sufficient evidence for the Fed to “look through” the inflation increase from tariffs and re-commence cutting interest rates. The financial markets are already pricing-in this scenario with lower short-term market interest rates and the much lower US dollar value.

Doing nothing is not an option for President Trump and he is demanding immediate cuts to interest rates, otherwise Governor Powell’s days are numbered. The US law is very clear that the Federal Reserve is independent, and the President cannot prematurely remove the Governor, even if he wanted to. Powell’s term ends in early 2026. However, if Trump did manage to find a loophole or he convinced his appointed Supreme Court judges to find a precedence, a sacking of Jerome Powell would send a cataclysmic shock to equity, bond and currency markets. An egregious dismantling of the Federal Reserve’s protected independence would only add to the already massive loss of confidence in the US Government and the US dollar.

The US Dollar has already depreciated 9.70% from 110.00 in mid-January to 99.13 today. A risk event like the unconstitutional dismissal of Jerome Powell would likely send the US dollar down another 10.00% as investors around the world vote with their feet and exit USD assets.

Kiwi dollar threatens 0.6000 as local economists turn gloomy

The NZD/USD exchange rate climbed to a high of 0.5976 last Friday, just failing to reach the big 0.6000 psychological level, closing at 0.5940. The Kiwi dollar finally attracted some bids after lagging the strong gains of the major currencies against the faltering US dollar. Softer US economic data over coming weeks should see a continuation of the USD depreciation, therefore allowing further NZD gains to well above 0.6000. In particular, the US GDP growth numbers for the March quarter on Wednesday 30th April will confirm a significant slowdown in activity levels to an annual growth rate close to 0.00%, following the 2.40% annual increase in the December 2025 quarter.

Here in New Zealand, the economic forecasting fraternity has all suddenly turned vey gloomy on the outlook for 2025. All the bank economists are now confidently forecasting that the Reserve Bank of New Zealand (“RBNZ”) will need to slash the OCR interest rate to a terminal rate of 2.50%, based on the global economy turning to mush from Trump’s tariffs. Weaker than expected local retail sales over the last two months has contributed to the new pessimistic forward view. These forecasters seem to be totally discounting any likelihood of the Americans ending the global trade war by agreeing deals with the Europeans and Chinese. They are also stating that the RBNZ will need to cut interest rates to support the economy through an expected difficult patch.

The foreign exchange markets are not pricing-in such a negative NZ economic outlook as the NZ dollar has continued to make gains against the USD and AUD over the last week. The FX markets are reflecting a more considered view that there is a reasonable probability that the global economy will not decline into recession from the bombshell Trump has unleashed with his tariffs. The OCR being reduced to 2.50% is one of a number of possible scenarios that could unfold over coming months, depending on what trade deals countries can agree with the Americans. However, to have it as your central forecast is a very “big call” indeed.

As is usually the case, the local bank economists are pushing for much lower interest rates so that the residential property market lifts and they can lend more mortgage money to maintain their profitability. Currently, bank profitability is going south as new lending volumes are well below loan repayment amounts. The local media never seems to question the vested interests at play here; they merrily report the bank interest rate forecasts as gospel. The analysis behind the latest gloomy economic forecasts is also heavily lop-sided towards the retail and housing sectors, almost completely ignoring the boom taking place in nearly all of our export industries. Off course, the export sector will be adversely impacted if the global trade wars continue for a protracted period. However, there is currently no sign of our major primary exporters reducing volumes or suffering from lower demand/prices.

The negative outlook from the economists does appear to be a kneejerk and premature response to only one of many alternative international economic/trade scenarios over coming months. Nearer to the coalface of the NZ economy, Fonterra’s Chief Executive, Miles Hurrell delivered a much more upbeat assessment last week of how the dairy industry is placed in the face of the current global turmoil. Dairy commodity prices continued their climb to higher levels at last week’s GDT auction, despite futures market pricing beforehand indicating a 5.00% pullback. Miles Hurrell also expected the Chinese to quickly resolve any port/shipping bottlenecks as a result of cancelled and diverted orders from the US tariffs. The dairy, beef, sheep meat and horticulture export industries are currently enjoying strong demand, higher prices and increased output. That very positive picture is a long way from the doomsday projections currently being bandied about!

The view from the International Monetary Fund (“IMF”) last week was “Trade tariff uncertainty is "literally off the charts" but there will not be a global recession”. They talk about of an erosion of trust between trading nations; however, they stopped short of predicting a worldwide recession. It all comes down to how quickly Europe and China can agree new trade arrangements with the devil that is the Donald. Global trade volumes will fall with all the current uncertainty, however once that uncertainty reduces with trade deals being struck, the economic downturn may be very short-lived.

When the local interest rate market realises that the NZ economy is not going to hell in a handcart, the forward pricing will reverse back upwards from 2.50% to somewhere above 3.00%. Such an adjustment, if it happens, would be positive for the Kiwi dollar in its own right.

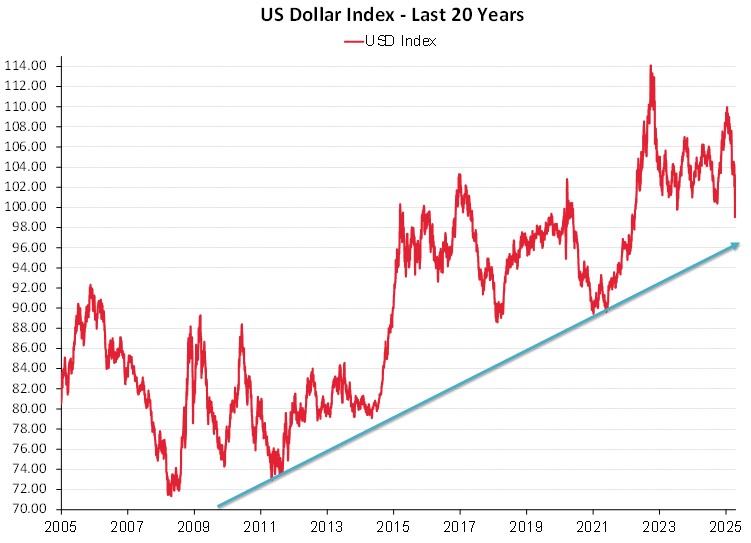

The depreciating US dollar is rapidly approaching a long-term support area

Twenty years of US economic exceptionalism is coming to an end. The dramatic drop in the US dollar value over the last three months represents a significant re-rating of the US economy and its current political leadership. The USD Dixy Index, currently at 99.13, is set to break below the 96.00 support level on the long-term upward sloping trend line for the USD (refer to the chart below). Over coming weeks, the currency markets will certainly test the level of support for the US dollar at that critical chart point. A return to the previous 2015 to 2020 trading range of 90.00 to 100.00 for the USD would send the NZD/USD exchange rate into the mid-0.6000’s.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

8 Comments

"As is usually the case, the local bank economists are pushing for much lower interest rates so that the residential property market lifts and they can lend more mortgage money to maintain their profitability."

Exactly.

"His idea of business between companies and business between countries is “I win; therefore, you must lose!”."

Very well said Roger. Unfortunately there are some commenters on this site who cannot contemplate a win-win scenario, and think likewise.

The rise of the NZD to USD is temporary and news driven.

The global credit event is around the corner. Tight liquidity and counterparty risk.

As per historical credit/market events there will be a rush to save haven USD.

Is that not old thinking though ? Is the USD still considered a "safe haven" currency under Trump's lunacy ?

Depends if the US is the worst off due to Trump's decisions. It should be bad for them, but potentially much worse for others.

Might depend how much you believe Peter Zeihan.

As per historical credit/market events there will be a rush to save haven USD.

At the moment, gold and JPY are operating like safe havens. But System 1 thinking would suggest you are correct. Of course that's assuming something isn't broken.

BTW, just noticed XAUUSD hit 3,383 while all the Westerners gorge themselves on chocolate. Must be those pesky Chinese again.

The USD Dixy Index, currently at 99.13, is set to break below the 96.00 support level on the long-term upward sloping trend line for the USD (refer to the chart below).

Dropping like a stone at the moment. DXY at 98.3.

To me a key sentence in Rogers report is 'The analysis behind the latest gloomy economic forecasts is also heavily lop-sided towards the retail and housing sectors, almost completely ignoring the boom taking place in nearly all of our export industries.'

Things may be looking somewhat rosy in the short term for the agricultural sector but increasing world greenhouse gas emissions plus enormous releases of methane and carbon dioxide from melting permafrost see https://cpo.noaa.gov/emissions-from-thawing-permafrost-add-trillions-in… are really going to screw the scrum in NZ. Yet the current NZ Government is looking the other way... no problems here.. I guess there is no problem until beyond the next election so why even think about it, and don't say anything, shhhh.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.