Summary of key points: -

- US Dollar: Crisis of confidence

- What is de-dollarisation?

- NZ Dollar: Left behind, but likely to catch up

US Dollar: Crisis of confidence

The US dollar continues to plummet in value on global foreign exchange markets.

President Trump’s erratic trade policies, made mostly on the hoof, are convincing the currency markets that the policies will send the US economy into recession and are pricing that underperformance vis-à-vis others accordingly. Investors around the word are pulling their funds out of the US as they no longer trust the Americans to be fair and active participants in the long-established rules on international trade arrangements. Trump has upended the world order with his attempted policy to return manufacturing to the US, and there are serious consequences not only for the US economy, however also for many other economies who are now dealing with disruption, cancelled orders and pressured cash flows. When international confidence in an economy and currency is lost, its value can only go one way

The overall US dollar as measured by the Dixy Index has now depreciated 9.20% to 99.89 since the high of 110.00 it reached just three months ago in mid-January when Trump was inaugurated. Over the last month, since the tit-for-tat tariff brinkmanship started between the US and China, the US dollar has depreciated 4.40% from 104.50 to the current level of 99.89. The Euro has soared in value from $1.0200 against the USD in mid-January to new highs of $1.1360 (up 11.40%) at the market close last Friday. The financial and economic advantage the US dollar has had over other currencies over the last three years is rapidly dissipating as market forward pricing of US short-term interest rates expands out to five x 0.25% cuts by the Federal Reserve this year. US interest rates are being priced lower as investors and borrowers see the prospect of an US economic recession forcing the Fed’s hand to cut rates, despite import tariffs increasing inflation later this year. The interest rate advantage that has kept the US dollar strong against all currencies until recently has changed dramatically.

Evidence of the foreign disinvestment from the US is seen with the plunging share market and over this last week US Treasury Bonds being heavily sold down as well. Foreign investors from Europe, Japan, China and the rest of Asia are quite rightly reducing their exposure and fund weightings to the US and US dollar as they cannot trust what the clown in the White House will do next. It is always the large cross-border capital flows that shift currency values and there is a wholesale exit from the US happening before our eyes.

The reality of life that Donald Trump fails to understand is that the US economy does not generate sufficient private savings of its own to fund its own annual Government budget deficits and the debt that is issued to meet that financial shortfall. Therefore, for many years the US has relied on foreign investors into its Treasury Bond market to fund the deficits. The risk of this situation is that if you, as the borrower, annoy the lender too much with wild shifts in financial policies and performance, the lender will call-in the loan i.e. sell-out of US Treasury Bonds. In the deteriorating relationship between the US and China with Trump ramping up tariffs to 145% on Chinese imports last week, Trump appeared oblivious of the fact that China has US$760 billion of their foreign reserves invested in US Treasury Bonds. It does appear that the Chinese played one of their strong cards to retaliate against Trump by dumping a small part of their bond holdings last week. The speculated selling by the Chinese (not confirmed) sending the 10-year bond yield up from 3.90% to 4.50% over the seven days. These are unprecedented large moves in the value of bonds, and it was clear that the financial power than China holds finally dawned on Mr Trump.

The US did blink first in this tariff stand-off with China, as Trump announced a 90-day pause for non-China tariffs and all countries’ tariffs reducing to the 10% baseline tariff. Not that there was any great policy design behind the decision to pause. Trump does not read anything; he just watches Fox News on TV and cheats when playing golf! The story goes that last week he watched Ray Dalio, billionaire and hedge fund manager at Bridgewater Associates, suggest in an interview on Fox News that a 90-day pause on the import tariffs would be smart move by the US. The next day, Trump announced exactly that as the carnage in the bond market forced his hand. Trump and Treasury Secretary, Scott Bessent had earlier stated that they were not at all worried about US equities being sold off and claimed that the decreasing bond yields was evidence that investors were backing their policies. The spectacular reversal in the 10-year bond yields to 4.50% has smashed that claim of success.

It is now clear that the US tech billionaires and the titans on Wall Street who backed (and financed) Trump to be elected to power as President (as they liked the concept of lower tax rates and deregulation) are now regretting their decision, as Trump’s policies potentially sends the US economy into recession. The announcement late on Friday from the Trump administration that I-phones, memory chips, electronics and computers would have a temporary exemption from tariffs on imports from China, is evidence that big businesses in the US such as Apple and Nvidia have forced Trump to bow. Otherwise, a company like Apple paying 145% tariffs on the import of Chinese made I-phones into the US were facing bankruptcy, as US consumers can afford a US$1,000 I-phone, but not a US$3,500 American made I-phone. Apple does have factory in India, however that is only a fraction of the manufacturing capacity in China.

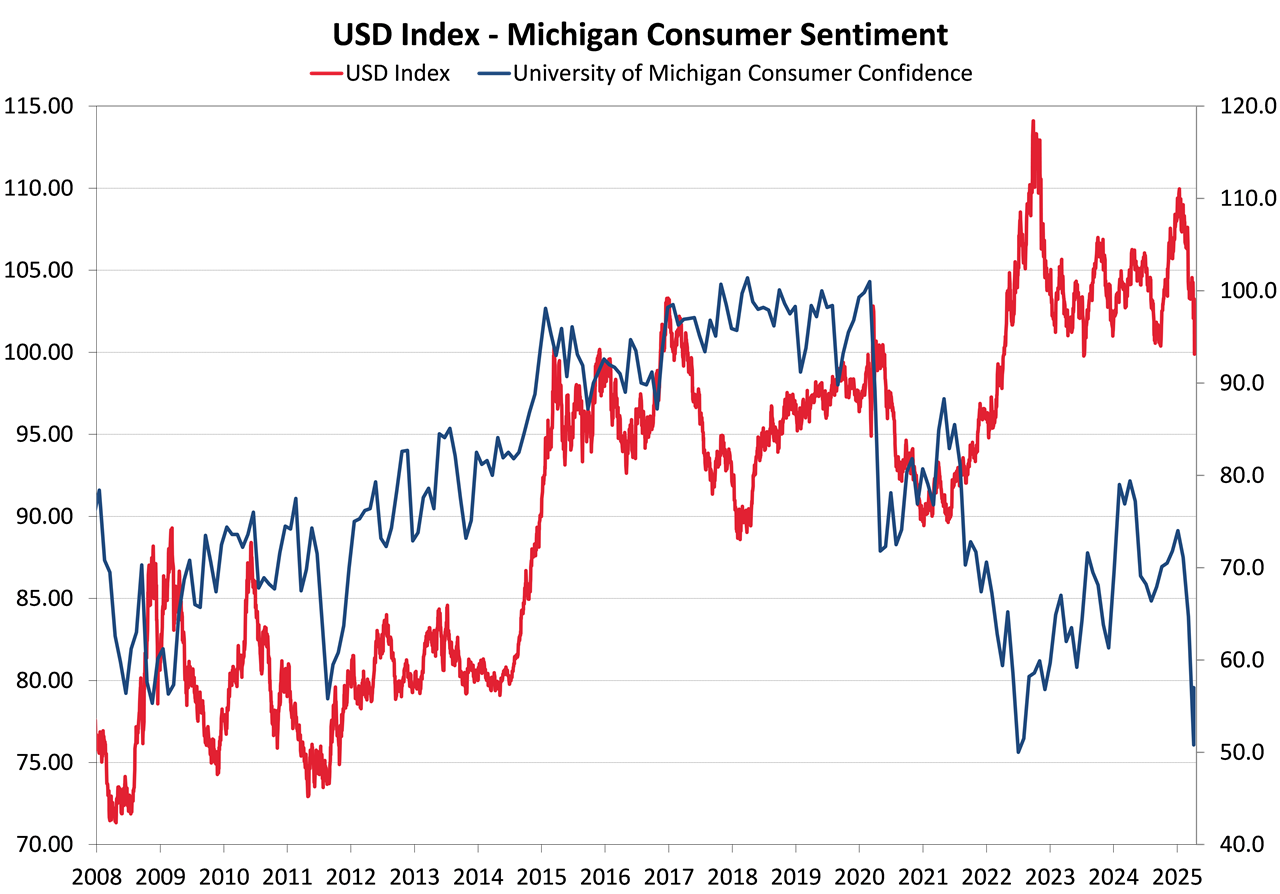

Evidence of the slumping US economy and what it means for the US dollar value is shown in the chart below. Last Friday, the University of Michigan Consumer Sentiment survey index plunged to 50.8 from 57.0 last month as households worry about rising prices from tariffs and job security. Strongly positive consumer sentiment in the US transfers through into a strong US economy and strengthening US dollar value (refer to 2010 to 2020 period on the chart). We are now seeing the opposite, which suggests the US dollar still has much further to fall.

What is de-dollarisation?

The massive debt and capital markets in the US have dominated international trade and finance for a long time now, leading to the justified status of the US dollar as the world’s preeminent “reserve” currency. That privileged position for the US dollar is only maintained whilst there is trust and confidence in the US markets, economy and currency. Right now that trust and confidence in the US is under serious scrutiny.

New Zealand imports consumer goods from China in US dollars and many emerging market economies (Argentina, Brazil, Indonesia, South Africa) export their hard and soft commodities in US dollars because they have borrowed US dollars to finance the trade and mine extraction.

A New Zealand importer of retail product from China, denominated in USD’s, effectively shares the FX risk with the Chinese manufacturer. The NZ importer has the volatile NZD/USD exchange rate to manage in making the USD payments and the Chinese manufacturer has to sell the USD received to buy Yuan (CNY). As Chinese interest rates are well below those in the US, the Chinese manufacturer “pays away” the forward points when hedging the USD/CNY FX risk. A lower risk position for both importer and manufacturer is to price the business in CNY. The NZD/CNY cross-rate is a lot less volatile (less risk) for the NZ importer. The Chinese manufacturer receive their own currency, and it eliminates the FX risk. Many Chinese manufacturers prefer to invoice in USD’s as they pay for their raw material imports in USD (to achieve a natural hedge). However, if CNY labour costs and internal infrastructure/overhead costs are a majority part of the cost of goods sold, they will switch to CNY invoicing. In this manner the US dollar is removed from the import/export trade i.e. de-dollarisation.

Argentinian exporters of beef and soya beans to China may switch to Yaun as the trade currency, instead of US dollars, as has been the practice in the past. The Argentinian exporters will only sell in CNY if they can finance the export trade in CNY. Therefore, continuing de-dollarisation can only really occur if the Chinese banks become more internationalised and offer CNY trade financing to exporters of commodities like Argentina.

Trump may want to build a protectionist wall around the US economy; however, US banking, debt and capital markets may lose their dominant role in international trade finance and investment. Not sure that the titans on Wall Street had this in mind when backing Trump into power again!

NZ Dollar: Left behind, but likely to catch up

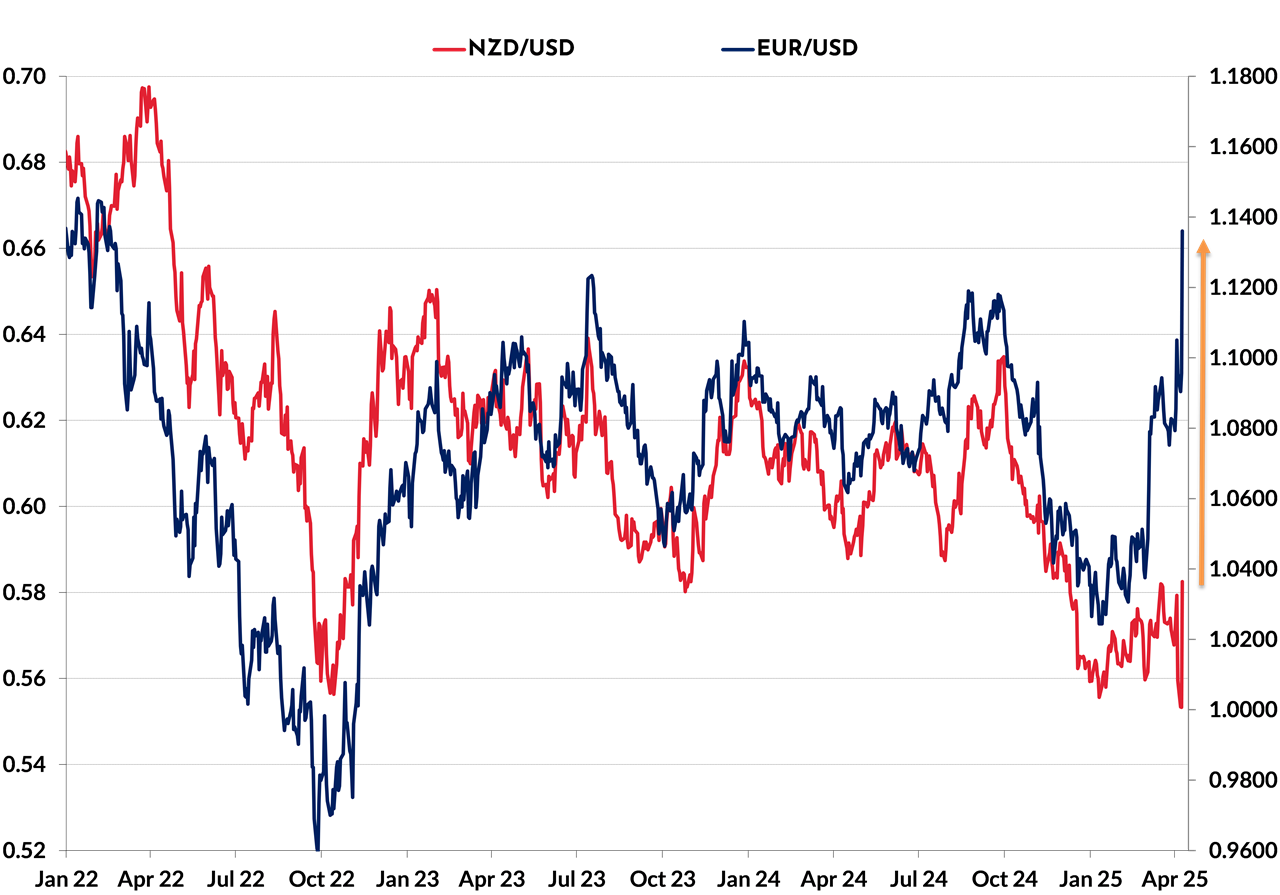

The Kiwi dollar has traded in another three-cent range over this last week. The NZD/USD exchange rate lifted off the 0.5500 lows of a week earlier when Trump upped the ante on Chinese tariffs and the Aussie dollar was pummeled lower in the FX markets. A weaker USD on the global stage last week has allowed the Kiwi to recover to 0.5825. However, the NZD/USD exchange rate seriously lags the gains other major currencies have made against the USD over the last three months (refer to the NZD/USD versus the EUR/USD chart below).

If the NZD/USD movements continued the close correlation to EUR/USD changes (as they normally do), the Kiwi dollar would be closer to 0.6600 right now! The Kiwi dollar is not at 0.6600 today due to two significant negative forces that have singled it out (along with the AUD) as different to the Euro, Pound, Yen and Swiss Franc.

- As a “risk” currency the NZ dollar has always been influenced by the investor “risk-on” and “risk-off” sentiment on US equity markets. US equities have been sold down the toilet over recent weeks and this has prevented any NZ dollar gains. If the Kiwi dollar is to have any chance of catching up to the gains of the major currencies, it will be dependent on US equity markets stabilising. They will stabilise, they always do after major fear-induced selloffs.

- New Zealand, like Australia is heavily dependent on trade with China. Any weakness in the Chinese economy due to Trump’s tariffs is never good news for the NZD and AUD. We have seen the sharp sell-offs in both currencies over recent time due to the China linkage. It would be in both the interests of the Americans and the Chinese that Trump and Premier Xi Jinping reach a compromise deal on tariffs. The Chinese well know how to play to Trump’s ego from the previous trade wars in 2017/2018. Give him the “win” media headline he craves for, however protect China’s long term position as a world economic power. Any resolution or “deal” between Trump and Xi Jinping will be viewed by the markets as very positive for the NZD and AUD. If this occurs, the Kiwi dollar will catch up to rates well above 0.6000 over coming months.

The Reserve Bank of New Zealand, in cutting the OCR by another 0.25% to 3.50% last week, played a very sensible straight bat to the highly uncertain and volatile situation we currently find ourselves in. Most local bank economists have immediately moved to a terminal OCR rate of 2.50%, as they place a 100% bet on their expectation that the global economy is going into a deep and dark recession. We would not be as pessimistic as that, as the alternative scenario is that a damaging trade war is averted, and the NZ economy expands with our booming exports to +3.00% growth rate later this year. Forward market pricing of shorter-term interest rates can change quickly the other way when the reality does not match the narrative.

The NZ March quarter CPI Inflation figures this Thursday 17th will not be a negative for the Kiwi dollar. The quarterly increase in inflation is forecast to be +0.80% compared to 0.50% in the December quarter. The annual rate of inflation will therefore move higher to 2.40% from the previous 2.20%.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.