Affordability may have improved for first home buyers over the last year or so, but the latest Reserve Bank figures suggest they remain cautious in their approach to the market.

Interest.co.nz’s latest Home Loan Affordability Report showed overall affordability improved significantly for first home buyers last year due to falling mortgage interest rates, rising after-tax incomes and flat prices at the bottom end of the market.

And Reserve Bank data suggests while more first home buyers have been getting into a home of their own, they remain cautious on price.

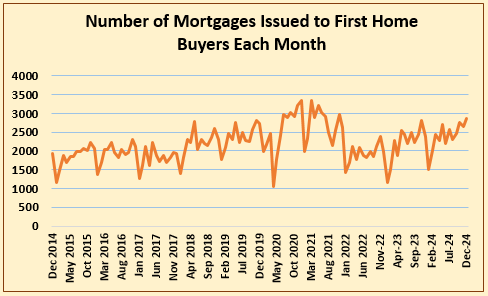

Reserve Bank lending figures show t28,781 first home buyers took out mortgages last year, up 9% compared to 2023.

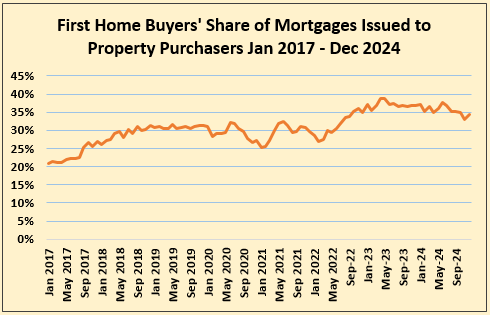

However, their share of all new mortgages issued that involved the sale of a property, ie, excluding new mortgages issued as top ups for existing loans or where a borrower changed banks etc, declined from 37% in 2023 to 35% in 2024.

So although first home buying activity improved in 2024, it did so at a slightly slower rate than the market as a whole, suggesting first home buyers aren’t getting carried away.

This has probably been helped by the high levels of supply of homes for sale, creating a buyer's market and allowing all types of buyers to take their time when choosing a property.

The prices first home buyers are paying also suggests a degree of caution in their approach to the market.

Interest.co.nz estimates the average prices paid by first home buyers last year remained within a fairly narrow range, barely moving from $673,341 in December 2023 to $672,081 in December 2024.

December 2024’s estimated average price was also barely changed from the December 2022 average of $670,135, suggesting the prices first home buyers have been paying have been largely flat for the last two years, although they are down by more than $45,000 (-6.3%) compared to December 2021.

These trends are clearly visible in the three graphs below, which suggest that while first home buyers are becoming steadily more active in the market, with more of them getting into a home of their own, they are showing no signs of a return to the irrational exuberance that drove market activity in 2020 and 2021.

The comment stream on this story is now closed.

74 Comments

I love the stock art photo. They look like they've just realized what the weekly payments on their lousy townhouse in Ranui will be.

Hats off to the younger folk who get into their own homes. 🏠

It’s never been easy but the long-term rewards make it worthwhile.

And let’s not forget to acknowledge the “bank of mum and dad” which, in many cases, will have made it possible.

Onward and upward …. especially with the slashing of mortgage interest rates. 💸

TTP

To the bitter end...

And let’s not forget to acknowledge the “bank of mum and dad”

I guess you are thanking them for pushing up your investments and making houses unaffordable for those without generational wealth?

The Bank of Mum and Dad will be closing if it hasn’t already. Once Auckland's RVs come out and values drop by 17-19%, and the last boomer born in 1964 hits 65 in 2030, Mum and Dad won’t be lending anymore. The Ponzi scheme will have run out of greater fools.

Gen X is still paying off their mortgage, while Gen Z is broke.

Hi rastarse,

You have no idea what investments I may, or may not, hold.

Further, parental support for the long-term welfare of one’s offspring is neither new nor inappropriate. Note that family involvement applies to health, education, sport and many other worthy areas - not just housing.

TTP

P.S. Kraken - your comment above would be one of the most naive comments I’ve ever read here.

The wealth effect is reversing as Auckland RVs come out, and Gen Z, like everyone else, isn't saving during the recession. The youth are better off in stronger economies like Australia or the US.

First it was wellington, next hamilton in April, with expectations of steep falls.

Followed by the big reveal, Auckland in may..

Hi TTP

On the other hand, we do know for certain the laws that you broke. Commerce Commission - Property Brokers Manawatu and director fined $1.5m in price fixing case

Well.... the laws that you got caught breaking. Where there is smoke there is fire, so no doubt this wasn't the only malfeasance you have been involved in over the years.

Get a life, Starrider.

You know nothing “for certain”.

TTP

Based on your response he knows more than you are comfortable with

Fantastic work.

I would like this case to be forced on to every post that TTP makes, because it's critical that readers know that this individual who constantly pushes FOMO and the narrative that housing is the best place to put their money, is a convicted individual for dishonesty.

I like the idea but do not want TTP to be considered in the same high standing as Trump.

Lets not try and build his credibility.

tpp I can only assume you have investments as there is no other sane reason to celebrate parents going into late life financial stress.

Every parent who does this is making it harder for every non asset owner.

It's called bidding up a ponzi. Same applies to KS and kick start loans. They all funnel cash up to the few.

But it appears you do not have the mental fortitude to comprehend this.

edit- my eldest took my advice to start his own business 3 years ago and not use his cash (or mine to enter the ponzi). He's recently purchased at $1.2 mill and steaming ahead in life.

Here, I fixed up the opening sentence for you.

"Hats off to the younger folk who get into their own homes in Australia"

You're welcome!

All those snakes 🐍 and crocodiles. 🐊

TTP

There is one in nz called TTP

😂🤣

Well played, you won!

The crocodiles are north of Gladstone. Australians don't live there either.

Why hats off to Ozzie first home buyers?

Yes it is dearer to buy in the Australian cities than NZ, and cost of living is now every bit as expensive as NZ.

Currently in Oz so I am qualified to comment.

- Better Superannuation outcomes

- Salary Sacrifice

- Aussie Labour party is more National then NZ Labour

- Better Infrastructure

- More job and better opportunity as for example you working for head office of a Bank, not an NZ backwater..

- Better weather

- Better airline connections and lower holiday fares.

- Cheaper 91 fuel...

- WAY Better public transport options

like for like prices, less shit boxes in Aussie.

IT GUY, if you think it is better, then away you go?

Depends what you do and whether you want to get ahead in whatever you are good at!

I have lived in both countries and Oz is great to holiday in, but I now prefer NZ for lifestyle and income.

As for weather being better, I would dispute that.

Earning an Aussie income too? Or scraping by on NZ dross?

(Just a reminder, 50% of Australians earn more that 75% of Kiwis).

I am in Brisbane and 50c Public Transport to all destinations is a bloody winner.

Classic build it and they will come, price it like Auckland and they will drive.

Our NACT politicians seem to be inspired by Manila's transport and planning rather than Singapore's.

According to CoreLogic the median dwelling price in the Australian cities (Feb 25) is (in AUD):

Sydney - $1,193,228

Melbourne - $772,317

Brisbane - $893,592

Adelaide - $819,363

Perth - $809,870

Hobart - $658,180

Darwin - $502,632

Canberra - $850,534

Combined capitals - $897,632

Combined regional - $656,445

And in New Zealand (REINZ) (Dec 24) (NZD)...

Auckland - $1,000,000

Wellington - $765,000

Canterbury - $707,000

All New Zealand - $775,000

Auckland is somewhere between the size of Adelaide and Perth, while Wellington and Christchurch can questionably even be considered cities.

Those Australian prices aren't all that bad in comparison. Especially when you get to live in a functioning first world country.

In AKL FHBers often Ranui Flatbush etc etc , Mangere, but in Perth etc you get a decent home in a suburb you would want to live in.

Perth. Really? People here are way too negative about NZ. I’ve had family visit from Europe over the summer, and they were blown away by how beautiful our country is. Comparing it to a remote, culturally isolated city like Perth is just craaazy.

Perth, remote? Lol

much closer to Europe and Asia than NZ

Auckland is closer to most Australian cities than Perth is.

By definition,

(of a place) situated far from the main centres of population; distant.

And?

Perth is much closer to most of civilisation

HM is just arguing for the sake of it. Don’t bite.

Perth, in Western Australia, is often considered to be the most isolated major urban area when it comes to distance. To put this into context, the nearest destination with over 10,000 inhabitants, Adelaide, is a staggering 2,100km (1,305 miles) away; that's roughly the distance from London to Casablanca, Morocco

@Bigben,

How to tell people I haven't been to Perth, without telling people I haven't been to Perth!

I’ve been there a few times.

Enjoyed the wineries in Margaret River, beaches are great.. But I wouldn’t want to live there.

Thanks for that, some here are completely deluded on the cost of living and housing comparison

Good luck getting property in Sydney Melbourne for those prices anywhere close in.

There are a lot of crap areas further out that brings prices down on average.

At the end of the day if many on here think that OZ is better than NZ then away you go.

Some Things are every but as expensive in Oz including food prices from where we are shopping.

Yes some things are better but plenty of extra taxes and most people complaining about cost of living.

Not too sure why it is known as the Lucky Country?

Congratulations on your understanding of medians. I have it on good authority that medians work the same ways in both countries.

It's known as the lucky country because the ground doesn't start shaking and level your entire village.

Out of the ruins

Out from the wreckage

Can't make the same mistake this time

We are the children

The last generation (the last generation, generation)

We are the ones they left behind

And, I wonder when we are ever gonna change, change

Living under the fear, 'til nothing else remains

We don't need another PONZI

We don't need to know the way home

All we want is life beyond an OVERPRICED HOME !!! ..... ('We dont need another hero' Tina Turner)....lol

FHBers can only afford whar they can afford.

Rich Mum and Dad might get poorer soon, perhaps they are passing their super to kids?

An economist says New Zealand needs to have a tough conversation about superannuation.

Finance Minister Nicola Willis yesterday told Newstalk ZB the scheme needs to become sustainable and a debate about age eligibility will be needed eventually.

Bagrie Economics says raising the age makes sense, with the average life expectancy up a lot.

Cameron Bagrie says we can't keep kicking the can down the road.

"More than 50 percent of all welfare spending is going towards New Zealand's Superannuation - and some people need that money, but there's a chunk of society that I don't think need that money and they're double dipping."

While I agree it needs addressing and pronto, as long as we have a population bulge of an older generation still living and very engaged at the voting booth, I cannot see it happening unless the voted in parliament makes it happen and does a 180 on an election promise

More from Cameron Bagrie

THREE KEY FACTS:

- More than 200,000 people were on a Jobseeker benefit in September this year

- New Zealand’s gross domestic product (GDP) fell 0.2% in June 2024

- Monthly food prices fell 0.9% in October compared with September, according to figures released by Stats NZ

The days of selling more expensive houses to each other are done. Tourism, China and migration – previous fire-powers of growth – are not there.

The economy is getting back on track.

Sort of.

We can celebrate that interest rates are coming down. With almost 50% of borrowers to refix mortgages in the coming six months, monetary policy will be providing an economic injection.

The Government is claiming credit but the seeds sown in 2023 and 2024 were the delivery in crushing inflation, though non-tradable (domestic) inflation is still too high and needs watching.

Now the debate needs to start on the quality and durability of that economic improvement we are starting to see. Will it be of quality?

There are numerous issues we need to own up to as well as opportunities.

My biggest concern is division.

This growing divide we have across New Zealand, as illustrated by the recent hīkoi to Wellington, or farmers taking their tractors to Parliament in opposition to the previous Government has been socially and economically corrosive. The political centre (National and Labour) got 65% of the vote at the last election. The periphery got 35%. Extremism is becoming more common.

Consensus policy-making has become more difficult as the periphery grows in influence.

Uncertainty rises with that. Uncertainty carries a risk premium. That makes businesses nervous. They do not invest, or any investment requires a higher risk premium.

Division is a global theme. Populism and short-termism are driving politics more and more.

It is not good for New Zealand or the global economy.

The head of the International Monetary Fund recently noted dissatisfied populations as global growth moderates.

The Government and Prime Minister need to lead. They are not.

They need to find more common ground. Work better to get consensus in areas such as education and infrastructure.

There must surely be common growth when it comes to kids and infrastructure. Education and infrastructure are essential economic enablers.

We urgently need to have a national discussion and hui on productivity.

Without productivity, or doing things better, living standards stagnate. It’s a recipe for an exodus out of the country which we are seeing through the departure of New Zealand citizens.

Productivity drives living standards. It provides the coin that underpins many aspects of wellbeing. It drives the tax coming into the Government’s coffers.

The Treasury’s chief economist has been direct in the past week. There is “accumulating evidence of a sustained productivity slowdown”.

The Reserve Bank also acknowledged in their October Official Cash Rate (OCR) decision that “low productivity growth is also constraining activity”.

Back in May, the Treasury noted that “productivity for the whole economy averaged 1.4% a year between 1993 and 2013 but averaged only 0.2% a year over the last 10 years”.

That is an economy in serious structural trouble.

The finger is consistently being pointed at the Government and what it can do.

Or at a trend decline in global productivity growth – which has not matched New Zealand’s decline.

People need to understand that New Zealand’s economic model is morphing. The days of selling more expensive houses to each other are done. Tourism, China, and migration – previous firepowers of growth – are not there.

Welcome in the new economic drivers. Productivity. Business investment. Natural resources.

Better policy. And businesses lifting their game.

These economic drivers require new discussions and a different policy prescription and acceptance.

The Reserve Bank’s decision, for example, to get banks to hold more capital has been a huge own-goal in encouraging home lending at the expense of real productive lending.

Why are more questions not being asked as to why exports have dropped from 29% to 25% of gross domestic product?

We are starting to see better nuances from Government, though far from complete, in areas such as education. The Government’s aspiration of doubling exports is too much demand (market access) focused and needs more supply focus (how we produce the stuff).

The recent announcement of the fast-tracking of initiatives will help.

New Zealand has a huge natural endowment that needs unlocking to drive growth, but also managing the risks around growth. An example is water and irrigation which could be a huge enabler. Horticulture has huge upside. Security is now a key theme in trade. New Zealand is yet to define its strategy and the opportunity.

The business sector needs to lift its game too if we are going to get out of this hole.

The OECD’s economic assessment for New Zealand in 2022 had some pretty pointed comments to make about management and governance.

“Managerial practices in New Zealand lag behind other advanced OECD economies, holding back the adoption and effective uses of digital technologies.

“Management boards in New Zealand’s firms are often more focused on preserving existing value and regulatory compliance than on growth strategies that involve productivity-enhancing investments and international expansion.”

The NZX 50 Index has not performed well in recent years compared to global peers. Companies were slow to respond to the economic signals in 2023 and cut costs.

New Zealand is at an inflection point. A sugar rush is coming from lower interest rates. We are seeing it initially within housing market activity levels though not in prices so far.

A sugar rush upturn is not what we need though.

We need better foundations. Tough times often deliver better foundations because they make people focus.

I’d favour a bit more economic hurt as the building blocks on a more sustainable economic gain.

The bottom line

New Zealand is at an inflection point. A sugar rush is coming from lower interest rates. We are seeing it initially within housing market activity levels though not in prices so far.

A sugar-rush upturn is not what we need, though.

We need better foundations. Tough times often deliver better foundations because they make people focus.

I’d favour a bit more economic hurt as the building blocks on a more sustainable economic gain.

IT GUY

You must have put in a lot of time and effort listing all the good and the bad benefitting and afflicting NZs economy respectively: well done!

However, as usual with mere written or spoken expressions of opinion, they are rarely carried through in practice. Have you ever thought of starting your own political party, and if not why not? Inotherwords 'walking the talk'. There are no bars in NZ to starting your own party....look at all those that have had a go in the last 50 years or so. And some do succeed: e.g.NZ First and Act. In NZ with MMP even small parties can have an outsized influence. Further, now is probably as good a time as any that I can remember to start a new party; the general population is currently as confused about who to vote for as they've ever been. You could call your party the "Common Sense Party".

Alternatively, you could join any existing party as a keen volunteer and demonstrate your determination to become an MP. That's how most of the current crop made it. But it would require commitment which is a rare quality.

I've asked this before but never got an answer.

Are immigrants classed as first time buyers even if they have owned property abroad previously.

E.g would a 50 year old lawyer from the UK who has previously owned several properties in London be classed as a FHB?

I believe so... if your name has never been on the Toitū Te Whenua database as the authoritative source of NZ land title,

then its your first time. But if you transfer kiwisaver type monies it can be tagged as already used for FHBer... so you cannot double dip super funds...

Generally yes but if they're taking out a mortgage with someone who has borrowed for a owner occupied house in NZ previously then no. From the RBNZ:

A first home buyer is a borrower entering the home ownership market in New Zealand for the first time. In the case of more than one borrowing party to a loan, borrowers are classified as first home buyers only if none of the borrowing parties have previously drawn down on housing finance for owner occupation.

Under Background Notes here:

Right, so these 'FHB'ers aren't necessarily actual first home buyers, they could be mid-career immigrants with savings earnt in other countries, or off-shore rich pricks buying up our real estate from under us.

Is there any indication what percentage of these first home buyers are home grown New Zealanders who have managed to save and buy in NZ after growing up and working in NZ?

What I'm getting at is that the term FHB evokes a young NZ couple buying their first property when it appears this may not be the case at all.

Conspiracy theory at its finest.

Is there any indication what percentage of these first home buyers are home grown New Zealanders who have managed to save and buy in NZ after growing up and working in NZ?

I'm assuming you have no answer to this and are just trolling again 🥱

If we have had record numbers of young New Zealander's leaving and record numbers of immigrants arriving, it would help explain a spike in FHB numbers and is important information to help understand where the opportunities are in the housing market as these two demographics have different tastes. You'll learn these things eventually Rookie, if you don't lose your shirt first.

do you have ANY stats to show immigrants who owned houses are buying our as FHB? at all?

If not, it's a theory.

You will use anything you can to make the situation sound worse than what it really is.

If not, it's a theory

Correct, just like the idea that the first home buyers reported here are actually first home buyers. It's just a theory, in the absence of any evidence to prove otherwise.

Your theory is more far fetched.

On 5 May 2023 this site published an article "Immigrants purchased 12.5% of homes sold in NZ" so the information about home grown NZers as FHBs is likely available, just not chosen to be publicised.

All the doomers sinking their teeth in to mediocre news.

Only a couple of weeks left on here for me Rookie, are you going to be the only left flying the flag for home owners ?

Pretty sad that all , your lot, can put forward is someone who doesn't even have an investment portfolio....

maybe he can start a new userid as Wantobeinvester, even sadder if its because he cannot afford to be an investor.

meanwhile successful investors are sitting on the sidelines, cashed out.... watching and pointing

we all start somewhere right?

the question is from march, when there are no pro housing commenters, what will form the new divide?

Loads of pro-housing commentators will still be on here. They will be cheering further house prices falls making housing more affordable for younger workers, cheering less money being sent overseas via mortgage payments to Aussie banks and more parasitic speculators hitting the wall.

Do you mean no more housing spruikers left? Fingers crossed.

Lol the irony, or is it hypocrisy, given the big info dump you posted upstream.

At this stage i can't justify $0.01/ hour to reply to trash, i'll still be reading for the education/ humor.

Maybe in the future.

Bon Voyage! °🥂⋆.ೃ🍾࿔*:・

As much fun as it was playing with that chew Toye

What an absolute delusional boomer comment to believe are you going to be the only left flying the flag for home owners ?

He likes to troll.

Kinky!

.... Just to address the 'all to frequent snobbery' about terraced houses ...

This :https://widget.auctionslive.com/widget/auctions/view/215598/19Y?src=

Gross annual return per annum: ~ 7.9%

That’s cheap.

A leaker or ‘remediated leaker’?

Attn: RBNZ.

Drop the OCR.

Tighten LVRs and DTIs for 'investors'

NZ Inc. will thank you.

This is probably the kind thing to do.

However, does some blood have to be spilled to keep us from repeating our past mistakes?

Do we cast aside the debtors or the savers?

The young. Don't care what their financial state is. All must be sacrificed so the Boomers can have the retirement they are entitled to.

And if they don't like it? Well, then we'll just import some new ones.

I checked out some open homes in Hobsonville point in the weekend. Asking price for a low quality 3 bed townhouse is $1.15m. Vendors are still completely delusional. Didn’t see a single person other than the agent in 4/4 places. There’s still a way to go yet.

Its just down down down in NZ Housing Ponzitown.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.