Summary of key points: -

- Trump-induced carnage in equities, bond, oil and FX markets

- Trump’s trade bomb: What happens next?

- Where to from here for the Kiwi dollar?

Trump-induced carnage in equities, bond, oil and FX markets

President Trump’s tariff and trade policy announcement last Thursday morning has proven to be far more severe than widely expected beforehand.

The smart money was on reciprocal tariffs specific to products and countries, rather than a blanket 20% or 25% tariff on all imports into the US. As it transpired, the percentage tariff on each country was calculated higher by dividing the US trade deficit figure for each country by the number of exports into the US of A. Incredibly, the sale and purchase of services between the US and all other countries was completely ignored in the calculation. As a so-called property tycoon, Trump seemingly only understands physical assets and physical goods! Initially, there was considerable head scratching in Wellington as to just how New Zealand scored 20% for tariffs on US goods imported into our market. We abolished import tariffs decades ago; however, such inconvenient facts are not considered as relevant by the wrecking ball now occupying the White House.

The best media headlines observed in response to Trump’s “Liberation Day” for the US economy have been “Obliteration”, “Mindless Vandalism” and “America’s trade policies back to the 19th century”. Assessing the new economic and financial/investment market landscape has become nigh impossible and wild volatility ensues, due to the extreme uncertainty as to how world trade plays out from here. Planned corporate mergers, acquisitions and public market IPO’s have been canned as businesses’ competitive positions, strategies and investment plans are also totally up ended. The value destruction is incalculable against the very debatable benefits for the US economy. Several market commentators are now considering whether the US share market is investible as their new Government changes the rules at will. As stated in last week’s commentary, global investment funds can no longer trust the Americans and are rapidly reducing their weightings to the US market and therefore the US dollar.

Around the global the reaction by investors, companies and Governments has been one of total disbelief that the Americans would deliberately up-end established trade relationships and economic order. In true Trump style, he has thrown yet another grenade and now waits to negotiate a supposed better deal for the people of America after the dust settles. The Trump regime appear disturbingly unaware of the damage they have created in attempting to reverse globalisation and build a protective wall around the US economy. The tariff policies have not worked in the past and will not work now to achieve the economic changes Trump and his cronies desire.

Financial and investment market reaction to the larger than expected US tariff levels has been swift and severe over the two trading days since the President’s release of the detailed trade policies: -

- The NZD/USD exchange rate has been tossed around on a three-cent roller-coaster. From 0.5740 on Thursday morning, the Kiwi climbed to a high of 0.5850 overnight as the US dollar tumbled on global FX markets. However, the gains were short-lived as both the NZD and AUD were thumped down very hard after China announced their 34% retaliatory tariff on US imports on Friday. The Kiwi dollar was sold down to a low of 0.5550 and closed Friday night battered and bruised at 0.5600.

- As forecasts on the probability of a US economic recession later this year increased, the US dollar was initially smashed lower in the FX markets. The USD Dixy Index plummeted from 104.00 on Thursday morning to a low of 101.20 early Friday. Following the Chinese retaliation tariff, the USD recovered to close at 102.77.

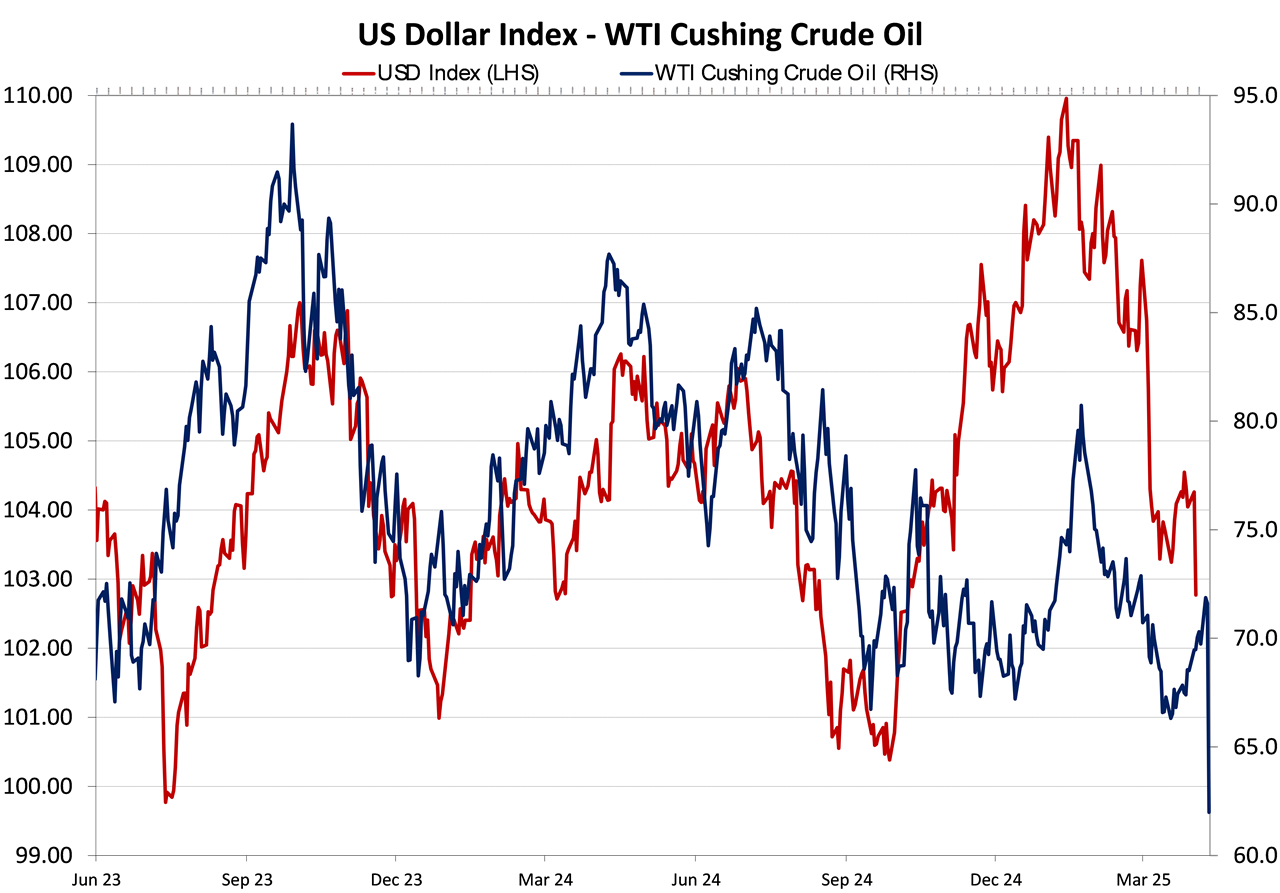

- The US 10-year Treasury Bond market delivered their verdict on Trump’s tariff policies by pricing-in a much weaker US economic performance (despite tariffs pushing up inflation in the short-term). Bond yields sliding from 4.25% on Thursday to a low of 3.86% Friday and closed at 4.00%. Further reductions in bond yields is a firm reason for continuing depreciation of the US dollar (see chart below)

- US equity markets capitulated in right royal fashion as investors ran for the hills. The Dow Jones Index crashing 9.20% from 42,200 on Thursday to 38,315 at the market close on Friday.

- Oil prices have also tumbled over the last two days. West Texas crude prices spiraling 13.60% lower from US$71.80 on Thursday to US$61.99 by Friday, reflecting the market pricing lower global growth and lower oil demand. Falling oil prices is yet another contributing factor to a lower US dollar value (see second chart below).

Aiding the US dollar recovery back up from 101.20 was the statement from US Federal Chair, Jerome Powell that the tariffs were “larger than expected” and the Fed would be in no hurry to adjust monetary policy. Unbelievably, Trump then accused Mr Powell of playing politics by not slashing interest rates immediately! The rest of the world and most of the US is struggling to understand from where this Trump hoodoo economics is coming from. Nothing adds up!

The decision by the Chinese authorities to immediately retaliate with counter tariffs on the US was a real surprise to market participants. The feared global trade war has started and that is a big reason why the Kiwi dollar is trading at 0.5600 and not 0.5800.

Trump’s trade bomb: What happens next?

There are very sound business and economic reasons for the US having large trade deficits with many countries. The fundamental reason is that US consumers want the cheaper and smarter foreign product and consumers in the rest of the world have no appetite for the more expensive and inferior US product. Trump is attempting to reverse that situation by forcing consumers around the world to buy US product. One way of doing that is to force countries to reduce their own import tariffs on US goods and buy more US product. At the same time, the import tariffs into the US are designed to force US companies to bring back manufacturing to the US, reducing imported product.

US manufactured products are not competitive on price or quality in the rest of the world for the following reasons: -

- US unionised labour costs are too high (an I-Phone would cost four times the current price if manufactured in the US).

- US companies design and produce product for the massive US domestic market first and generally only export when that market is softer. They are poor exporters, always have been. Unlike other exporters all around the world, US exporters do not make product specifically designed for export markets. The arrogant American way is take my product as it is or leave it. Most leave it, hence the large US trade deficits.

- The value of the US dollar is too high – US exporting firms cannot sell in foreign markets at a competitive price.

It is hard to see these required adjustments to reduce the US trade deficits happening anytime soon. Apart from the US dollar which is now depreciating for all the reasons we have highlighted over recent months.

Our summation of what happens next following the anti-free trade bomb lobbed into the world economy by Trump is as follows: -

- Many Asian countries with high import tariffs will cut those tariff rates in response to the US tariffs on their exports into the US. That is what Trump wants to see.

- Counties all around the world (especially Europe) will impose special taxes on the US companies who export services into their markets i.e. Microsoft, Apple, Alphabet and Meta. Yet another unintended consequence that hurts US economic growth.

- As many have adroitly pointed out (i.e. Warren Buffet), US import tariffs are essentially a tax on US consumers as the end-consumer ends up paying it, not the foreign exporter. An increase in tax in the US is a tightening of fiscal policy, therefore the Federal Reserve will be forced to loosen monetary policy to compensate. The interest rate markets are now pricing four x 0.25% cuts by the Fed from June.

- It is in China’s best interests to negotiate a more harmonious relationship with the US on trade. Their immediate retaliatory response is an attempt to get the high ground, however it will not work for them. China will stimulate domestic spending even further to compensate for some reduction in manufactured export activity. Good news for NZ food exporters.

- Trump’s strategy and tactics for negotiating deals is to smack you in the nose first, then start talking. Generally, such bully-boy tactics might work for a short period, however eventually the playground unites and over-powers the playground bully.

- The real possibility of the US economy sliding into recession over coming months will force Trump’s finance team to backtrack on these extreme policies.

Where to from here for the Kiwi dollar?

The NZ dollar was making solid progress over recent weeks on recovering from the 0.5550 low of mid-January caused by the initial Trump-trade election euphoria. After climbing to 0.5850 last Thursday, the Kiwi dollar was badly caught in the downdraft of the Australian dollar being smashed in global FX markets following China’s 34% tariff retaliation to the US. The prospect and risk of a tit-for-tat trade war between the US and China was actually happening and the Aussie dollar suffers the most when there is bad news for China. The AUD selling (which the NZD follows) is arguably well over-cooked and the three-cent depreciation from 0.6350 to 0.6050 is likely to reverse when the traders realise that it is not the end of the world for the Australian or Chinese economies.

The NZD/USD rate did not plunge as far as the AUD/USD rate, resulting in the NZD/AUD cross-rate jumping up to 0.9250 from below 0.9100. Local exporters selling in AUD’s have had ample opportunity to enter hedging at levels around 0.9000 against such a risk. Local USD importers with orders placed with banks to buy USD’s around the 0.5800 level have also bought some time with their forward hedging.

Exchange rates are relative prices and therefore on a relative basis New Zealand exporters into the US are better off with a 10% tariff than many others who are paying much higher tariffs into the US. Our export volumes of lamb, beef, wine and sawn lumber into the US are unlikely to suffer too much because of the tariffs.

The Reserve Bank of New Zealand have an OCR review this Wednesday 9th April wherein they will make another 0.25% cut to 3.50% and express concern as to global uncertainties. The cut is widely expected and priced-in therefore it will not be negative for the Kiwi dollar. What we do know is that the RBNZ is nearing the end of their monetary easing cycle, whereas many others (Australia and the USD) have much further to go.

A critical determinant of the NZD/USD direction is the interest rate differential to the US. The NZ two-year swap rate interest rate has been well below the US two-year rate since last August when the RBNZ started cutting. The gap was over 1.00%, today that gap has closed up to 0.50% (US at 3.70%, NZ at 3.20%). The NZ two-year interest rate is unlikely to go much lower than 3.20%, whereas the US is on track to decrease significantly as the US economy weakens and the markets price-in the possibility of economic recession.

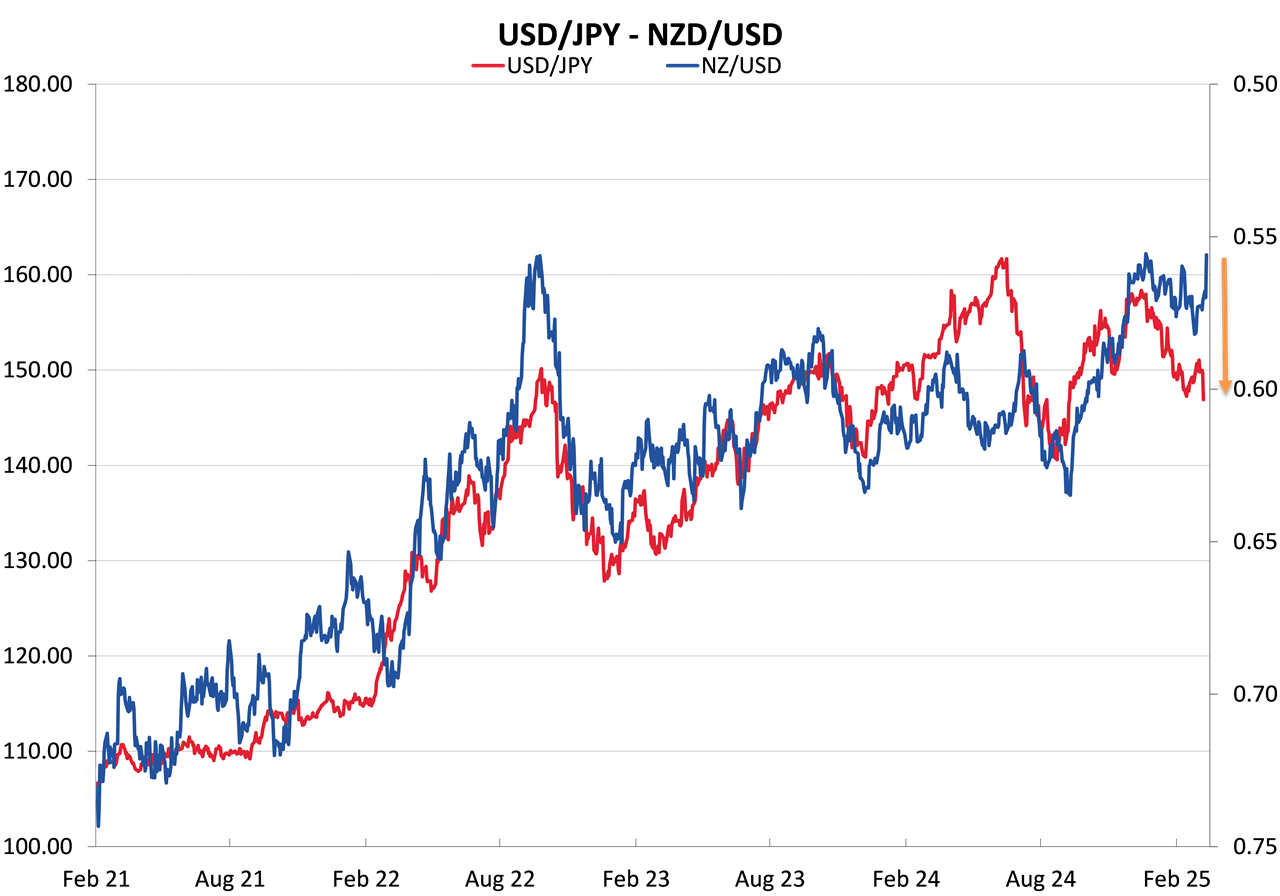

Another key driver of the NZD/USD exchange rate direction is the USD/JPY movements. The Japanese Yen is appreciating against the USD on safe haven inflows and the bond yield differential closing up. Over recent years the NZD/USD rate has closely followed USD/JPY direction. The latest fall to 0.5600 for the Kiwi is out of step with the close Yen correlation. History would tell us that the current Kiwi dollar divergence will not last and a catch up should occur (refer chart below).

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

1 Comments

In September the $ was $63.48 by Christmas it had fallen to $56.42 its now what ...$55.54 but yet its all Trumps fault !

by all means comment on the influence of things but this constant inference that everything bad is Trumps fault negates the fact that the $ was in freefalll over 10% down in the 3 months before Christmas and its now bumping around in a new window - 55-58 ish

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.