Summary of key points: -

- Trust and confidence in the US erode away

- US “Liberation Day” and “Retribution Day” through tariffs this week

- Political risk for the Aussie dollar?

Trust and confidence in the US erode away

Can you trust the Americans anymore?

Like any investment asset class, the US dollar currency requires continuing trust and confidence from buyers to maintain its value. Any loss of that confidence from existing holders and buyers, then the value starts to slide as safer options are sought out.

As the Trump regime upends the world economic and security orders, the emerging evidence is that their policies are starting to erode the US dollar’s status as the dominant reserve and trade currency in the world. The erratic, inconsistent and chaotic announcements on introducing tariffs on imported goods into the US is bamboozling not only households and business firms within the US with elevated uncertainties, but it is also unsettling international investors into the US. The depreciation of the US dollar witnessed since mid-January is a clear sign that foreign investors into the US are voting with their feet by reducing planned capital inflows into the US and exiting capital out of the US.

Superior economic performance and higher interest rates than counterparts have kept the US dollar at a strong level against all currencies over recent years. Those two positive variables are now diminishing, with clear evidence of the US economy abruptly slowing in early 2025 and the interest rate advantage is disappearing, as we highlighted in last week’s FX report on the closing bond yield differentials with Germany and Japan.

What has been really surprising to see over recent months since Trump came to power is the incredibly poor management of their economic policy changes. Tariffs and all the disruption they are causing has dominated the media headlines and caused negative reactions by the financial and investment markets. The other Trump policies of lower taxation rates and cutting excessive regulation, that stifles business investment, have hardly been mentioned. Investors and financial markets may have taken a more balanced view of the impact on the US economy if the positive policies were implemented alongside the tariffs, which are negative for US GDP growth. It does seem that Trump is obsessed with the concept of returning the US economy to the 1950’s and 1960’s period when they manufactured everything, they needed within the US for themselves. The intended reversal of all the evils of globalisation is based on a misguided Trump view that the rest of the world has somehow “ripped off” the US and now it is time to get that money back through tariffs. The reality is that other economies have grown faster under globalisation of goods and services, they have innovated and overtaken the US. The US may have just become fat and lazy. It is difficult for most of us to understand that the free-market capitalism and entrepreneurship that the US economic exceptionalism has been based on, is now being replaced by protectionism and isolationist policies. That a Republican President and Congress is promoting such socialist policies is equally baffling. The reality is that Trump only promoted these polices to get elected, the damage he is now doing to the US economy will ultimately force him to unwind the extreme elements of the tariff policies.

Evidence that foreign investors are pulling capital out of the US because they just do not trust the US anymore, is seen through the following developments: -

- The depreciation of the US dollar from 110.00 on the Dixy Index in mid-January to 103.70 today. Global investment banks who were forecasting a stronger US dollar in 2025 based on Trump’s pro-business policies are all now hastily revising those forecasts lower as the probability of economic recession looms later in the year.

- US share markets have tumbled in recent weeks as investors become nervous about the US economy. Foreign investors into US equity markets are clearly taking their equity and currency profits and returning funds to home-base.

- European share markets have risen over recent months as fund managers switch out of the US to European listed stocks that are expected to benefit from the increased defence spending by Germany and France.

- The gold price has skyrocketed as investors hedge against inflation but also hedge against a weakening US dollar value.

- Global fixed interest fund managers are now preferring the higher bond yields available in Germany and Japan.

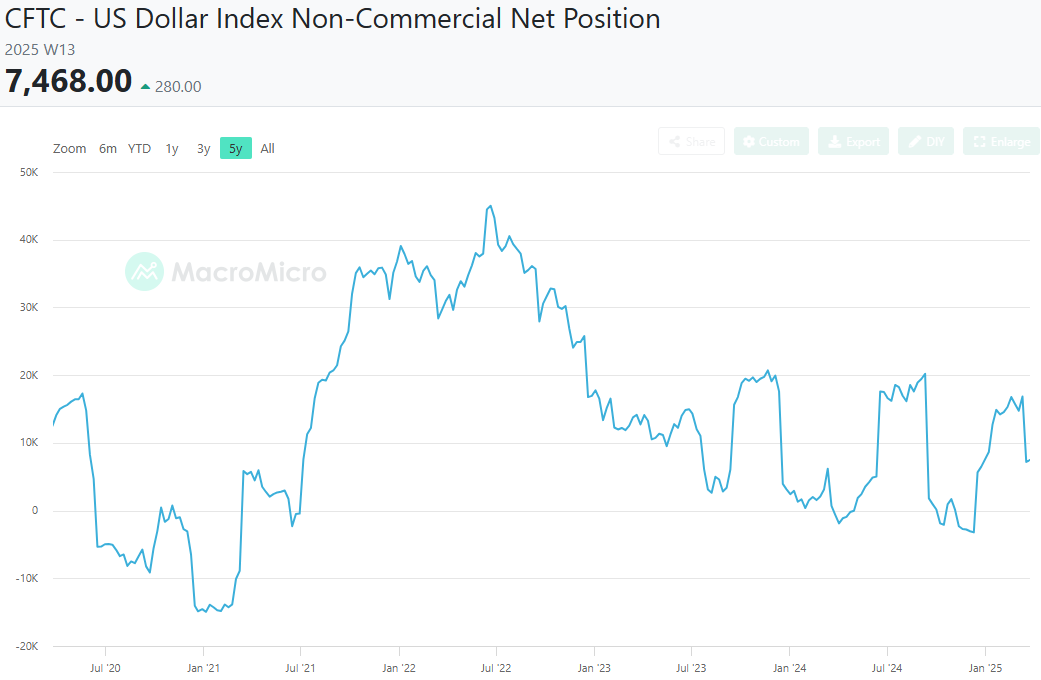

- Speculative currency market positioning on the US dollar is changing, as the previous US dollar bulls substantially reduce their long-USD positions. It cannot be too far away before we see net “short-sold USD” positioning by the currency punters (i.e. below zero on the chart below).

A continuation of investors around the world reducing their weightings to US dollar denominated investment assets for all the reasons cited above has to be expected. Therefore, the US dollar is expected to continue its slide over coming months as further evidence emerges that the probability of the US economy plummeting into recession later this year increases. The US dollar is also depreciating because global geo-political risks are reducing with the prospect of ending the Ukraine/Russian war. Although, unsurprisingly, the Russians are currently delaying progress. You can never trust the Russians either!

Former Goldman Sachs currency strategist, Jim O’Neil was regarded as the leading FX analyst and forecaster 20-odd years ago. Jim had a massive following around the world. In a recently published opinion piece, Jim highlighted three reasons why the US dollar is now depreciating, when most expected further USD gains in 2025: -

- Cyclical factors – Economic activity levels in the US are softening as the declining consumer confidence surveys tell us. The Atlanta Fed GDPNow forecasting model is signalling negative GDP in the March 2025 quarter.

- Structural factors – If Trump persists with tariffs, or goes further with doubling down on them, the knock-on negative impacts on the US economy would decrease the equilibrium value of the US dollar.

- Systemic factors – The argument goes that the US dollar has been in demand for a long time as the “reserve” currency of the world because the US Government acts as a security guarantor for the rest of the world. The US has also dominated global institutions. “If the US is now abandoning these roles, others will be forced to stand up for themselves, and the dollar’s unquestioned dominance could finally come to an end”.

Adding to the negative factors accumulating onto the US dollar is the risk of a sovereign US Government credit rating downgrade. Moody’s ratings noted last week that increasing interest payments on the US Government debt and widening budget deficits are eroding the US’s debt affordability. Moody’s warned that US fiscal strength has “deteriorated further” since the sovereign outlook was cut to negative in late 2023. US Government debt servicing costs have increased from 9.00% of Federal revenue in 2021 to a projected 30.00% by 2035. The increase in interest cost is the most critical threat to fiscal flexibility. Trump would blame sleepy Joe Biden for the debt hole, however that makes no difference to the credit rating agencies.

US “Liberation Day” and “Retribution Day” through tariffs this week

The NZD/USD exchange rate has held above the 0.5700 support level through this last week as foreign exchange markets mark-time ahead of the US announcements on April 2nd on the detail of their trade and tariff policies. Trump is labelling the announcement as “Liberation Day” for the US economy, many others would see it as “Retribution Day” as he attempts to rectify the score from other countries taking advantage of the US. The NZD and AUD currencies have again been held back from lifting against the weaker USD as “risk-off” investor sentiment in US equity markets effects the sentiment towards the antipodean pair.

It would be fair to state that the FX markets have most likely already priced-in the worst-case scenario in respect to the details of the US tariff policies. It is unlikely that the level of tariffs will suddenly be higher again to what has already been announced. The question is whether they will be more lenient with more exceptions?

It is doubtful that the big reveal on the detail of the tariffs will change the current softening direction of the US economy. Consumer confidence continues to plummet in the US with both the Conference Board and University of Michigan sentiment indices sharply lower last week. The PCE inflation result for February was in line with prior forecasts. The decrease in the oil/gasoline prices being offset by increases in new and used car prices. With the threat of tariffs increasing motor vehicle prices in the future, US consumers have been “doom” buying their vehicles in advance and this has caused some supply pressures and price increases now. With a slowing economy, more job insecurity and higher prices from tariffs looming ahead, it seems inevitable that US retail sales will follow the consumer confidence surveys sharply lower. The next retail sales figures for March are due on 17th April.

Upcoming US economic data which will potentially move the dial on the US dollar value, over and above the details on tariffs, includes: -

- March Non-Fram Payrolls employment data on Friday 4th April. Forecasts range from +80,000 to +130,000 which are significantly weaker than previous months – USD negative.

- March CPI inflation figures on Thursday 10th April. Another 0.20% monthly increase will lower than annual headline inflation rate from 2.80% to 2.40% - USD negative.

The evolving economic data is coming out generally weaker than forecast, which should provide more evidence and confidence to the Federal Reserve to recommence cutting the Fed Funds interest rate again in May. The detail on the tariffs is unlikely to force the Fed to increase their current inflation forecasts for 2025.

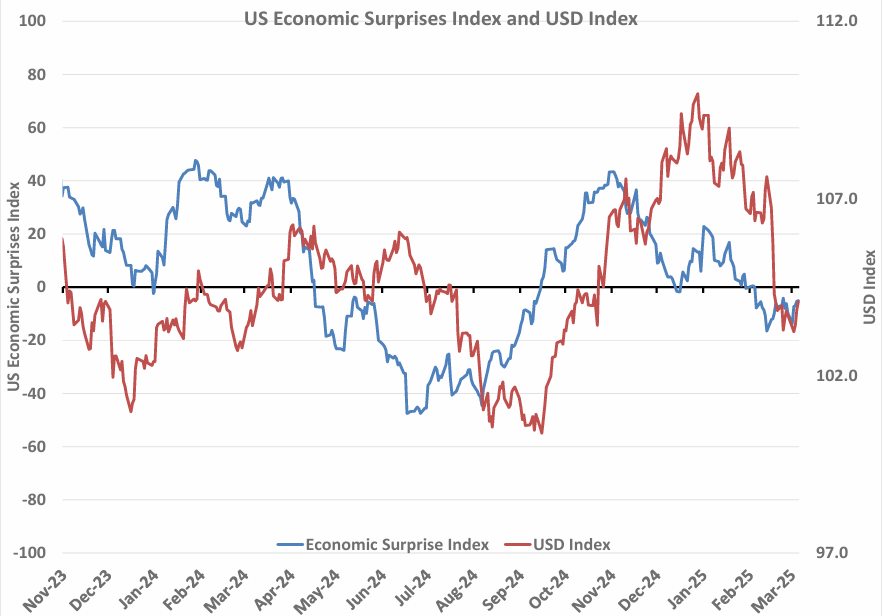

The USD Index (red line in the chart below) has followed the US Economic Surprises Index (blue line) lower over recent months (as expected). When the Economic Surprises Index is below zero, all the US economic data released is on average printing weaker than prior economist forecasts. We would expect the Economic Surprises Index to continue to move lower over coming months as the sharp slowdown in US economic activity surprises the pundits on the downside. The US dollar therefore has further to fall towards 100.00 on the Index and potentially as lot lower than that.

Political risk for the Aussie dollar?

The Australia Government has announced that their Federal general elections will take place on the 3rd of May. The current political opinion polls have closed right up between the ruling Labour Party and the Coalition Liberal/National opposition. The election campaign will largely be fought over domestic issues such as housing, cost of living, immigration, superannuation and healthcare.

The general expectation as to the likely impact on the Aussie Dollar’s value is that a change of Government to the Coalition would be a positive. Currency speculators are currently “short-sold” the AUD against the USD only because Australian interest rates are below those of the US and therefore the punters are paid the difference. As US short-term interest rates fall over coming weeks on weaker US economic data, the currency speculators are likely to be enticed to close-down their positions. The upcoming election would also be a secondary reason to close down the “short-sold” positions by buying the AUD.

It would be a blow to the Albanese Government if the US made no exceptions for Australia in the upcoming tariff policy release. The Australian Federal Budget last week offered tax cuts as an election bribe; the Coalition countered with a planned cut to the excise tax on fuel which would provide more immediate financial relief to households.

The Reserve Bank of Australia (“RBA”) is unlikely to make any changes to monetary policy during the election campaign. At their last meeting in February, they indicated that they would be in no hurry to make further cuts from the current 4.10% OCR. The next RBA meeting is this Tuesday 1st April, wherein a similar statement/position to the last meeting is expected.

FX risk for the Aussie dollar could intensify with increased volatility if the election result is not clear-cut on the day. Overall, the political risk factor appears muted with US dollar movements dominating

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.