Summary of key points: -

- Three prime prerequisites for the Kiwi dollar to move back above 0.6000

- NZ economy outperforms all forecasters

Three prime prerequisites for the Kiwi dollar to move back above 0.6000

The buying and selling forces on any currency does “wax and wane” over any given period, as economic trends and data changes opinions and market positioning.

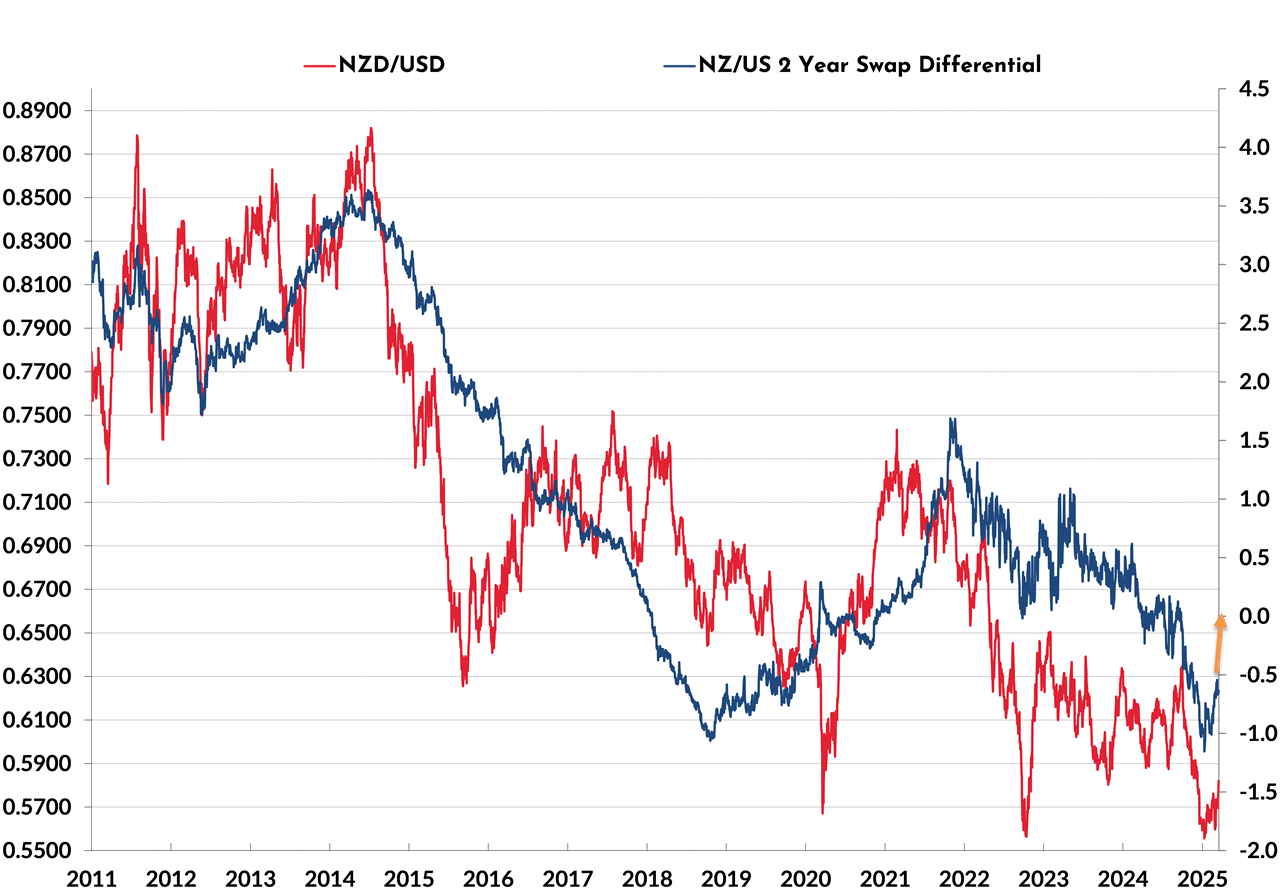

The New Zealand dollar has been under downward pressure for some time now, due to a stronger US dollar against all currencies, questions over China’s demand/growth and a domestic economic recession orchestrated by the Reserve Bank of New Zealand (“RBNZ”) to bring down inflation. Over recent months, all three of these negative variables have started to change, allowing the Kiwi dollar to locate some stability in the 0.5600/0.5700 region against the USD. We are now well past the period in late 2024 when the RBNZ moved at a faster pace in cutting interest rates (following a mid-year U-turn) than the US Federal Reserve. The US experienced a period of stronger economic data in the final quarter of 2024 which slowed the Fed down, whereas New Zealand’s economy slumped in the June and September quarters, resulting in early and more aggressive reductions in our interest rates. The timing and extent of monetary policy adjustments left the NZ two-year interest rate (which prices-in all the market expectations about future OCR movements) a full 1.00% below the US two-year interest rate. The interest rate differential favouring the US over New Zealand was a major incentive for the FX traders and speculators to sell the Kiwi dollar and buy the US dollar. On the other side, the 1.00% interest rate gap was a significant disincentive for anyone wanting to buy the Kiwi dollar (having to pay away the forward points).

The aforementioned prevailing market conditions are now changing again; therefore, it is timely to look forward into the remainder of 2025 to project what the likely forces will be on the Kiwi dollar.

In our view, three prerequisites are required to be in place before the NZD/USD rate can have an opportunity to return to trading levels above 0.6000: -

First Prerequisite - US to NZ interest rate differential closing further up

The two-year interest rate differential was 1.15% just over two months ago on 10 January 2025 (US at 4.48% and NZ at 3.32%). The NZD/USD exchange rate dropped to 0.5550 in mid-January as a result. Today, the interest rate gap has closed up to 0.65% (US at 4.10% and NZ at 3.45%). The expectation is that the gap will continue to close over coming months to be very close to zero, as NZ interest rates remain stable or inch a little higher, whereas US two-year interest rates have the potential to fall a lot further to around 3.50%. The impact of Trump’s tariffs on US inflation is delaying the further reduction in US short-term interest rates, based on a slowing economy. The Federal Reserve need a little more time and evidence to give them the confidence to “look through” the tariff-induced increases in US inflation as a temporary/one-off event and re-commence their interest rate cuts. Weaker US economic data through March and April is set to provide that economic evidence to the Fed.

As the first chart below confirms, the NZD/USD exchange rate does closely follow the interest rate differential. Both lines are now heading north. The last time the interest rate differential was zero, the Kiwi dollar was trading between 0.6000 and 0.6300.

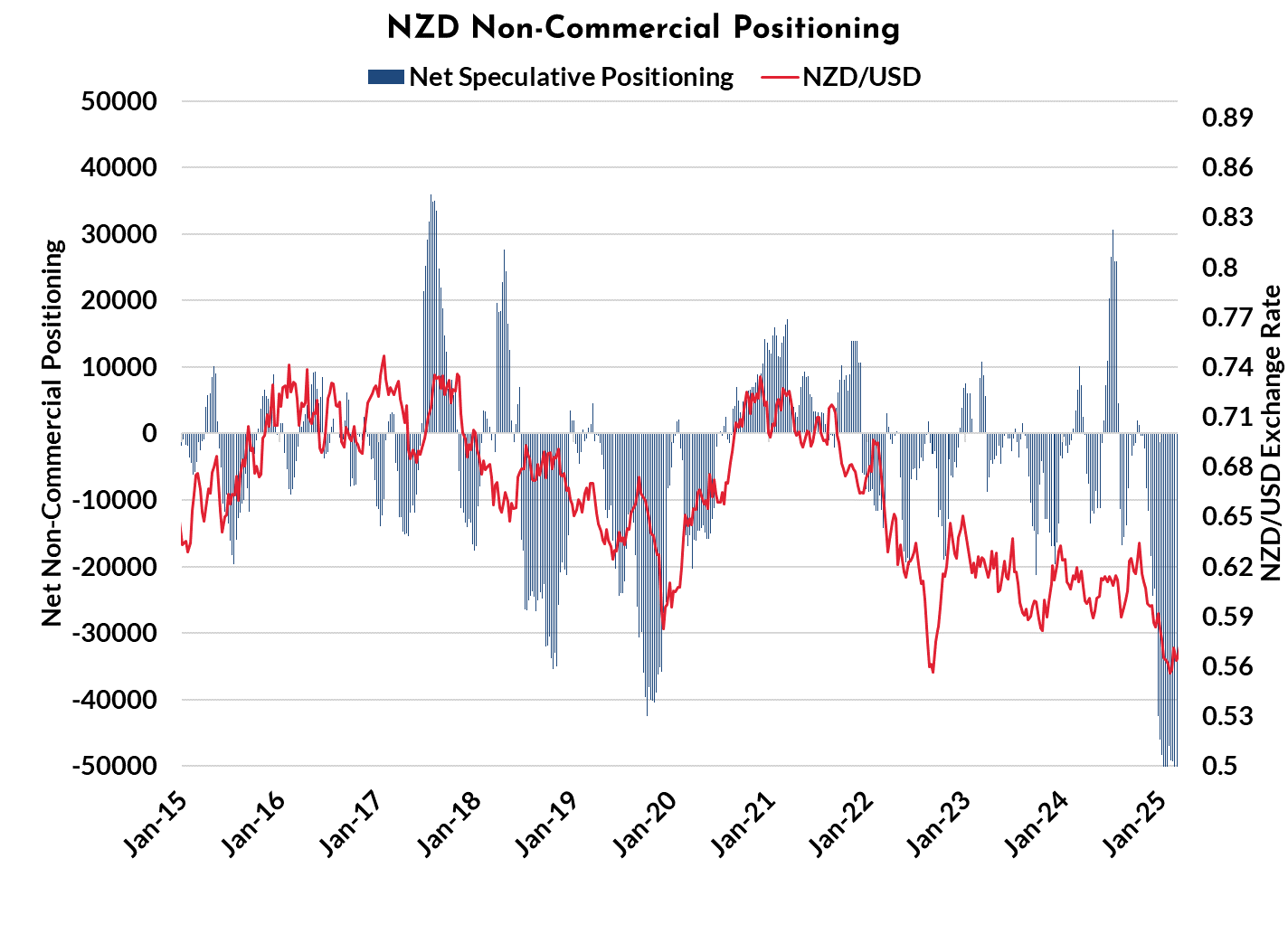

The second chart below highlights the current large “short-sold NZD” speculative positioning in US futures markets. As the interest rate differentials closes-up over coming months, the incentive to sell the Kiwi dollar dissipates and history tells us that the punters will quickly buy the Kiwi to unwind their short-sold positions. In 2021, the interest rate differential increased, resulting in the speculative positioning abruptly changing from short-NZD to long-NZD.

The first prerequisite is on track to be fulfilled.

Second Prerequisite - Continuation of US dollar depreciation

As discussed last week, the US dollar has depreciated 6% from its high of 110.00 on the USD Dixy Index in January to the current 103.70 level. The Trump regime wants lower US interest rates and a weaker US dollar to help the US economy transition from the Bidonomics-era of Government spending fueling all the growth, to the private sector investing and expanding. What Trump’s team underestimated was the high degree of uncertainty being displayed by US consumers and business firms to the tariffs and the blowing-up of Federal Government departments by Musk’s DOGE attack dogs. The dramatic slowdown in demand in the US economy over the last two months has caught the Trump regime by surprise and it has also forced a hasty reassessment by the Fed compared to their stance in December. At last week’s Fed FOMC meeting, Chair Powell was walking the tightrope between lowering their GDP growth forecasts for 2025 and lifting their inflation forecasts a tad due to tariffs.

Weaker US economic data over coming weeks should tip the balance for the Fed to recommence their interest rate cuts at their next meeting on 7th May. PCE inflation data for the month of February due for release this Friday 28th March has a better than even probability of being lower than the +0.30%/+0.40% consensus forecasts, due to lower oil prices and US retailers losing their pricing power on the lower demand levels. The following week, ISM manufacturing and Non-Farm Payrolls jobs data are also likely to record sharply softer conditions. The March jobs increase could be as low as 80,000, confirming the damage Trump is doing to the US economy with his chaotic policy swings. Further USD selling on lower US interest rates is anticipated from this weaker economic data.

Trump’s retribution tariffs being introduced on the 1st of April are turning out to be far more targeted on specific products and countries than what was threatened in his election campaign last year. The risk of an all-out trade war with the rest of the world similar to 2018/2019 appears to be diminishing. For this reason, the US dollar is not appreciating, however its depreciation was paused over this last week as the markets awaited the Fed’s new position and await the trade/tariff policy detail next week. Global geo-political risk stopped decreasing last week and increased a touch as Israel recommenced missiles into Gaza and the Ukraine/Russian ceasefire talks stalled (as they were always going to do) on Russian demands. Further progress to a ceasefire and conditions for peace talks can still be expected and this will be negative for the US dollar. It was never going to happen as fast as Trump originally boasted he would achieve; however, a “deal” is still very likely.

The impressive straight-line run-up in value of the Euro against the US dollar from $1.0300 in January to a high of $1.0940 a week ago, was always going to have a correction back on profit-taking. We saw the EUR/USD exchange rate peg back to $1.0815 last week as the inevitable profit-taking required EUR selling. The EUR/USD FX market has now been cleaned out somewhat, clearing the way for further USD selling against the Euro as the markets react to the expected weaker US economic data.

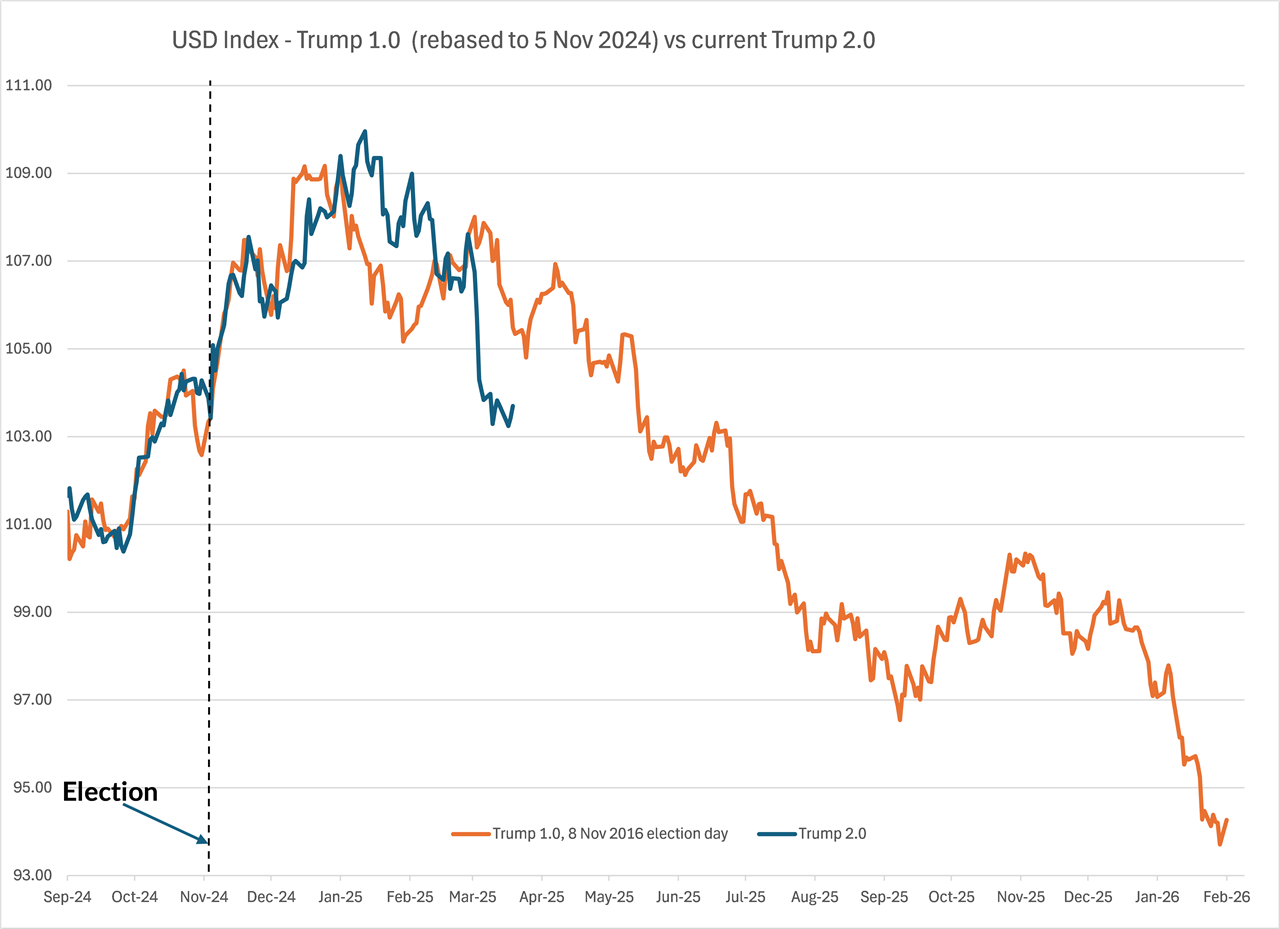

The Trump 2.0 USD response plotted against the Trump 1.0 (2017 to 2020) USD movements in the chart below has been extended out to 12 months beyond the Presidential election data. As history repeats, there is still a considerable amount of US dollar depreciation to take place over the next 12 months. The outperformance of the US economy over all others over recent years is rapidly being replaced with an underperformance situation, which is very negative for the US dollar value.

The second prerequisite is also appearing very likely to be fulfilled.

Third Prerequisite - Further improvement in NZ and Chinese economic data

As last week’s NZ GDP growth data for the December 2024 quarter indicated, the NZ economy is recovering earlier and stronger than what most have been forecasting. Lower interest rates and higher export commodity prices since that time is driving a continuation of positive growth in 2025.

Chinese economic data is also on the improve in 2025 since the stalling and fluctuating trends of 2024. Last week, both Chinese industrial production and retail sales numbers printed above forecast. The latest economic stimulus package from the Chinese authorities is tilted towards household consumption. The package amount has doubled to US$41 billion, expanding the consumer product subsidy scheme for electric vehicles, appliances and other goods. The services sector is China also needs a boosting to counter the negative impact of Trump’s tariffs on their manufacturing export industry. Stronger Chinese economic data looks assured over coming months.

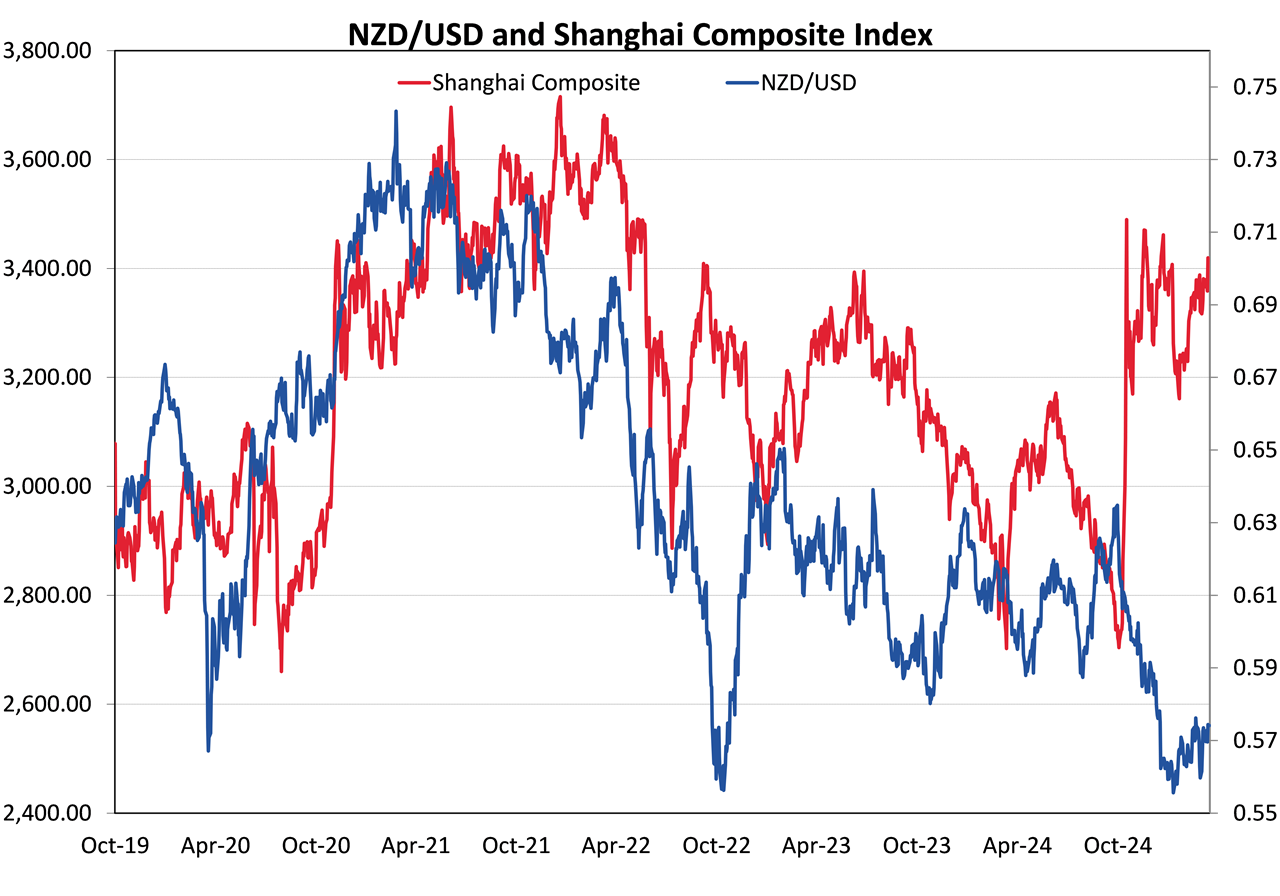

As the chart above displays, the Chinese equity market is already on the rise in anticipation of stronger economic data coming through this year. Foreign investors are returning to Chinese equity markets after several years of remaining on the sidelines. The NZD/USD exchange rate was closely correlated to the fortunes of the Chinese economy as represented by the Shanghai Composite equity market index. The correlation broke down in mid-2024 as lower NZ interest rates hurt the Kiwi dollar independent of Chinese influences. On the basis that the Aussie dollar and Kiwi dollars are proxies for all things China, the Kiwi dollar has some considerable catching up to do to the current increases in China’s share market.

The third prerequisite has not yet lifted the Kiwi dollar; however, the right ingredients are present for it to play a positive role over coming months.

To maintain some balance to the economic and FX market arguments in support of a higher Kiwi dollar, it is important to consider the inhibiters, limitations or risks to the view. The current risks are listed as follows

- The Reserve Bank of Australia reverse their current monetary policy stance of not reducing their interest rates by much at all this year. Weaker than expected inflation and employment data in Australia could lead to earlier interest rate cuts and hold back the AUD from its recovery from the low 0.6000’s. The timing of their general election in May will likely mean no more interest rate cuts over the next two months.

- Geo-political risks re-escalate in the Middle East and the Ukraine/Russian war ceasefire talks breakdown. Such a development would be USD positive and halt the current USD depreciation.

- There is a much more negative FX market reaction to the details of Trump’s tariffs next week. An increase in the risk of a more damaging global trade war is USD positive.

On balance, the three prerequisites discussed above seem more likely to play out as described and outweigh the listed risks.

NZ economy outperforms all forecasters

The amusing part of the media reporting of New Zealand’s stronger than expected GDP growth result for the December 2024 quarter, was all the excuses rolled out by the economists as to why the quarterly growth of 0.70% was well above their prior forecasts and why you cannot trust the accuracy of the GDP data! As this column has repeatedly stated over recent months, the NZ economy was already recovering from the doom and gloom of mid-2024 much earlier and stronger than generally being recognised by the fraternity of local economists. We have been discussing a strong export-led recovery in the NZ economy in 2025 since late last year. The stronger than expected GDP numbers confirmed the accuracy of our analysis. Consensus forecasts for the December quarter ranged from +0.20% to +0.40%, therefore the +0.70% actual outcome was a real surprise to most. Eleven of the 16 industry categories in the GDP measure recorded increased activity levels. Construction remains in contractionary mode; however, it generally lags other parts of the economy in an upturn. Agriculture and services lead the way in the economic recovery stakes.

Looking ahead, the lower Kiwi dollar value and lower interest rates will turbo-charge the rapid improvement in all activity levels across the economy over the remainder of 2025. Low base-effects in mid-2024 will propel the annual GDP growth rate to at least +3.00% by the end of the year.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.