Summary of key points: -

- Major currencies realigning to rapidly changing bond yield differentials

- USD has further to fall under Trump’s chaos

- Should the Fed “look through” one-off impact of tariffs on US inflation?

Major currencies realigning to rapidly changing bond yield differentials

The mighty US dollar has ruled the roost over the major currencies of the world in recent years. A major reason being that US long-term interest rates have been substantially above those of other competing currencies. The USD yield advantage has occurred when the US economy has out-performed most others, leading to the widely used description of “US exceptionalism”. So, on both counts, why wouldn’t you hold US dollars in preference to other currencies? Global fund managers have stacked their portfolios with the higher yielding US bonds and, until recently, they were picking up currency gains as well on the USD appreciation. As they say in the financial market’s parlance “that trade has just become too crowded”.

The reign of the US dollar is now teetering, as it loses its preeminent position in respect to the two advantages outlined above: -

- US bond yields have decreased 0.50% since mid-January, down from 4.80% to 4.30%.

- US economic performance is wilting in early 2025 as US business firms and households hold back on investment and spending due to the considerable uncertainties the new Trump regime has created.

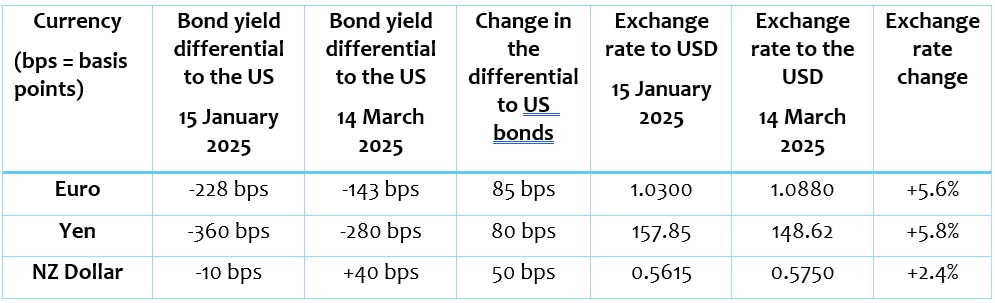

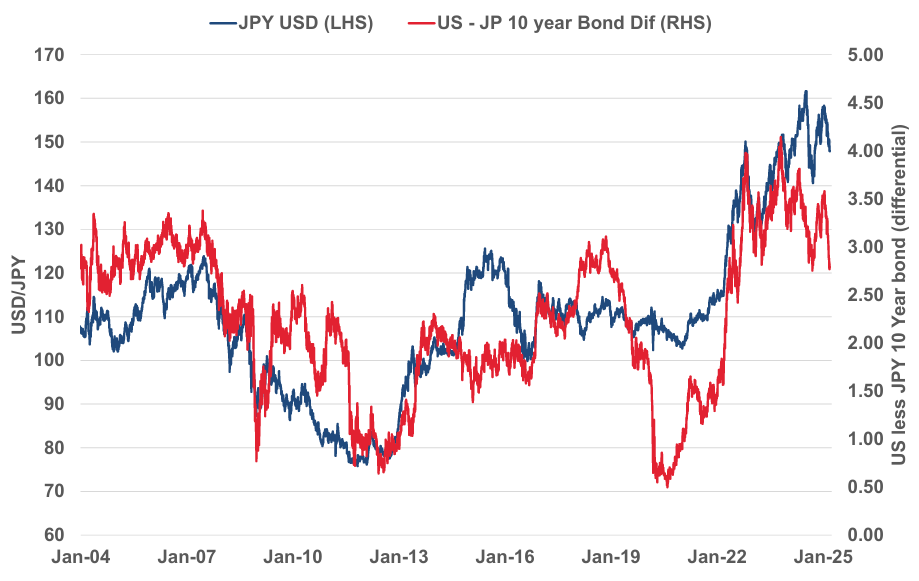

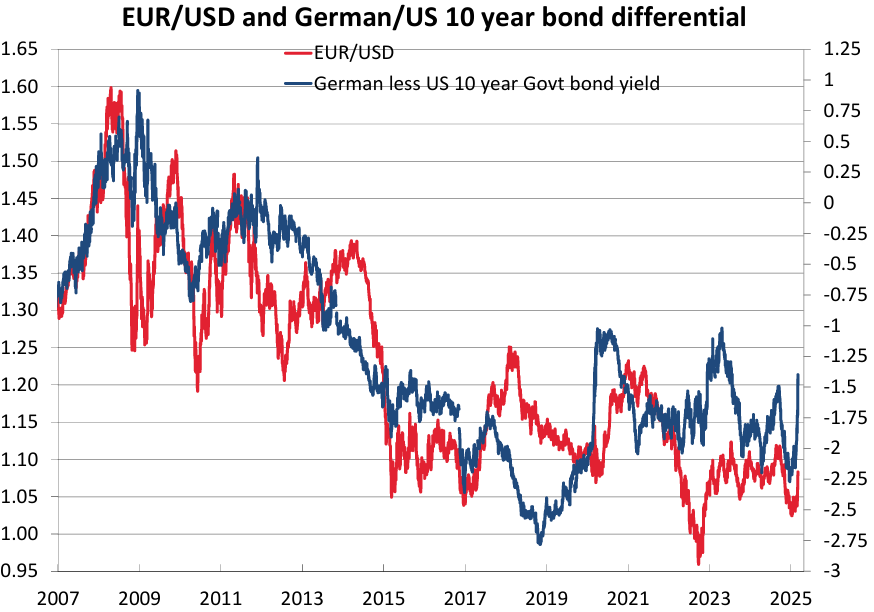

For their own independent reasons, both German and Japanese long-term bond yields have increased over recent months. The new German government is spending more on defence and other areas, sending their bond yields up from 2.40% two weeks ago to 2.87% today. Japanese 10-year bond yields are also rising as they tighten monetary policy to control their 3.00% inflation rate. The Japanese bond yield has lifted from 1.20% in mid-January to 1.50% today.

New Zealand 10-year Government bond yields were trading 10 points below US 10-yields in mid- January. NZ yields were trading at 4.70% and US yields peaked at that time at 4.80%. NZ yields have remained static at 4.70% since then, however US bond yields have decreased by 50 points to 4.30%. The NZ:US bond yield differential has swung 50 basis points in a very short period, with NZ yields now 40 points (0.40%) above US bond yields.

A summary of the change in bond yield differentials between the Euro, Japanese Yen and New Zealand dollar against the US is as follows: -

Looking ahead, the closing of the bond yield differentials for both Germany and Japan looks set to continue as US 10-year bond yields have the momentum to decrease another 0.50% to below 4.00%. The sharp slowdown in the US economy is driving US bond yields lower. Historically, there is a close correlation between bond yield differentials and movements in the EUR/USD and USD/JPY exchange rates as the charts below confirm. Further Yen and Euro gains against the USD have to be expected.

USD has further to fall under Trump’s chaos

The US dollar has followed a strong upward trend since the GFC in 2009. There have been periods when thew USD Dixy Index (see chart below) has depreciated, however the upward sloping channel has continued. At 103.70 today, the USD Index is sitting in the middle of the channel, having dropped sharply from the 110.00 level in January.

In 2017/2018 during Trump’s first term as US President, the USD Index depreciated 14% from 104.00 to a low of 89.00 as the high expectations of stronger US economic growth under Trump’s policies did not eventuate. It appears that history is repeating, as investors around the global are today selling the US dollar as they see all the indications of Trump’s chaos causing a slowdown in US economic activity. The USD Index has so far depreciated 6% from the January 110.00 high and judging by what happened eight years ago repeating itself, the USD Index has another 8% to go.

Since 2022, successive USD sell-offs have all stopped at 100.00 on the Index, found support and have rebounded back up again. That pattern has repeated three times over the last three years. As the upcoming and evolving US economic data confirms a dramatic reduction in jobs and consumer retail spending in early 2025, the US dollar looks set for further depreciation to 100.00 initially and then potentially to as low as 95.00 (completing the identical 14% depreciation).

A lower USD Index at 100.00 equates to 0.6350 in the NZD/USD exchange rate. A continuation of the USD depreciation to 95.00, if it eventuates, is the equivalent of 0.6700 in the NZD/USD exchange rate.

The risk of further significant USD depreciation for its own reasons, nothing to do with New Zealand, is the reason why local USD exporters must maintain high hedging levels to protect the future profitability of their businesses.

Should the Fed “look through” one-off impact of tariffs on US inflation?

US economic data continues to weaken, with both CPI inflation and PPI wholesale prices for the month of February printing below prior consensus forecasts last week. US consumer confidence and sentiment is slumping. The University of Michigan Survey of Consumers for March released last Friday posted a reading of 57.9, a 10.50% decline from February and well below forecasts of a stable 63.2. Consumer confidence in the US is down 27.10% over the last 12 months and the 57.9 level is the lowest since November 2022. US households are hunkering down, worried about tariffs pushing up prices, as well as their job security.

Against this backdrop of a rapidly deteriorating economic performance, the US Federal Reserve has many issues to weigh up and deliberate on when they meet this Thursday morning at 6am. The Fed meeting incorporates a full update of their economic projections and the “dot-plot” of individual member’s interest rate forecasts for 2025 and 2026.

The big questions is whether the Fed will “look through” the US tariff increases on imports as a “one-off” impact on inflation that has come from the US Government and has not been caused by economic supply and demand factors? Prudent monetary policy management by central banks typically “looks through” such Government tax changes, and they do not adjust monetary policy settings. A recent example of such a monetary policy response was the Reserve Bank of Australia ignoring the reduction in their official inflation rate caused by Government subsidies decreasing household’s electricity costs. The RBNZ “looked through” the GST increase to 15% a few years back as the impact on inflation is temporary and caused by the Government. The US tariff increases are no different.

The Fed, unfortunately, have some previous “form” on regarding price increases as temporary and not adjusting monetary policy to tighter settings early enough. In 2021, they regarded the lift in inflation as a result of the Covid stimulus packages as “temporary” and did not adjust to a tighter monetary stance. The inflation increase was not temporary, which meant they had to go much harder with interest rate increases to 5.50% in 2022 when inflation soared to 9.00%.

Understandably, the Fed members will be somewhat gun-shy about cutting interest rates this year when the tariffs are forecast to increase US inflation. Since the 2021 policy mistake, the Fed have stopped forecasting forward expected future economic and monetary conditions. They now only look back at historical economic data and adjust their monetary policy setting accordingly. For this reason, this week’s Fed statement should be more dovish than their December statement, wherein they reduced four x 0.25% interest rate cuts in 2025 to two x 0.25% cuts. The US interest rate markets is now pricing in three x 0.25% cuts over the remainder of this year.

If the Fed are looking backwards, all the recent US economic data has been significantly weaker than what they were expecting in December. Retail sales numbers for February due for release the day before the Fed meeting are forecast to increase by 0.70% after the 0.90% decline in January. An actual retail sales increase below forecast, coupled with a sharply weaker labour market, should force a number of the Fed “dot-plotters” to flop to the dovish side again.

Whether the Fed can afford to “look through” the tariff impact on inflation comes down to whether the Government forced price increases will lead to other more general price increases. If the economy and consumer demand is strong that could well happen. However, demand in the US economy is currently softening at a rapid pace. For this reason, the Fed should be adopting a less hawkish and more dovish tone at this week’s meeting. Further interest rate cuts may not come until the Fed’s May meeting; however, the markets will price US interest rates lower and the US dollar lower if the Fed see the writing on the wall with all the recent weaker economic data.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

2 Comments

The wide assumption that tariffs will be inflationary continues. The last tranche of them wasn't too bad. What is the basis for this assumption? Surely it depends on assessing, at least, their effect on the money supply, and whether any particular tarrif is directed towards correcting an existing mercantilist imbalance. If the latter is true in any case then there will be a net efficiency increase not vice versa.

Agreed. It amazes me that some economists are not looking at the 2016-2020 period of last Trump tariffs. No discernable inflation. These are not cost plus economies. Tariffs will be absorbed in margin or compensated by price reductions from the source. Maybe through currency changes. Either way, they are not necessarily passed on to the consumer. Especially if the competition is within the US, which will have no tariffs at all.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.