Summary of key points: -

- One-way traffic for the US dollar – sharply lower

- Maybe a method in Trump’s madness as oil prices tumble

- The very strange affair of Adrian Orr’s departure

- Big hitter investors absent from NZ investment summit

One-way traffic for the US dollar – sharply lower

The US dollar plummeted in value over this last week, depreciating from 106.60 on the USD Dixy Index at the start of the week to lows of 103.54, before closing at 103.87.

The Euro recorded its largest one-week gain since 2009, a straight line up from $1.0370 on 28th February to highs of $1.0890 on 7th March. The NZ dollar managed to post some gains against the sharply lower US dollar, however it did not benefit as much as the major currencies (EUR, GBP and JPY). The Kiwi dollar lifting from lows of 0.5600 on 28th February to trade up to highs of 0.5757 at one point on the 7th of March, however falling away somewhat to close the week at 0.5705.

Whilst there may be many reasons for investors and traders to reduce US dollar holdings and exposures at this time, the three prime factors behind the US dollar selling have been: -

- De-escalation of global geo-political risks: A ceasefire and temporary truce in the Ukrainian/Russian war does seem much closer today than it did a week ago at the slanging match in the White House. However, Putin’s conditions for a peace settlement are not yet known. The Europeans appear united and taking more responsibility to work with the Americans for a peace treaty that protects Ukraine’s security going forward. The US dollar strengthened dramatically three years ago when the war started, it is now heading in the opposite direction as the war is closer to an end, reducing the geo-political risk.

- Tariffs drive a weaker US economic outlook: The sentiment in the economic forecasting fraternity has turned on a dime from expecting Trump’s policies to produce a stronger US economy this year, to the latest expectations of contracting economic activity levels. The highly respected and reasonably accurate, Atlanta Federal Reserve Board GDPNow predictor model for future GDP growth for the March 2025 quarter (annualised GDP growth rates) has plunged from +2.30% to -2.50% in a matter of days. The official GDP growth figures for the March quarter are not released until the 1st of May, just before the Fed meeting on the 7th of May. The US equities and bond markets are reflecting investors views that the eventual implementation of Trump’s on-again/off-again tariff decisions will be net negative for the US economy as the extreme uncertainty causes business firms and consumers to act more cautiously with investment and spending. As previously highlighted, nearly all of the monthly economic indicators have turned sour in January and February. The honeymoon is well and truly over for the Trump regime with Treasury Secretary, Scott Bessent acknowledging last Friday that there are some signs of weakness in the US economy. Bessent stated “The market and the economy have just become hooked. We’ve become addicted to this government spending, and there’s going to be a detox period”. There was no mention of a detox period or “some short-term pain before longer-term gain” in the Trump election campaign!

- Trump trade long-USD positions finally unwind: We originally expected that the USD would reverse lower in December on the unwinding on long-USD speculative positions built up in October and November 2024 on the Trump euphoria. It has taken the FX markets until now to realise that Trump’s tariff policies are negative for the US economy, and therefore negative for the US dollar value as well. European share markets have outperformed US share markets over recent months, which underlines investors’ loss of confidence in Trump’s policies. Fund managers are hurriedly re-weighting investment portfolios out of USD assets and into EUR assets.

Confirming the softer trend in the US economy, the February Non-Farm Payroll increase in jobs was 151,000, below the +170,000 expected. The January jobs increase was revised lower from +140,000 to +125,000. The decidedly weaker US growth outlook, coupled with much lower oil prices, looks set to force the Federal Reserve to yet again change their interest rate forecasts for 2025. Readers will recall that the Fed cut interest rates in August/September 2024 and at that time they forecast 4 x 0.25% interest rate cuts in 2025. In December, they flip-flopped to just 2 x 0.25% cuts in 2025 in fear of higher inflation from tariffs. The chances are that they will be flip-flopping back the other way in either the 19th of March or 7th May Fed meetings, as they see a sharply weaker employment situation and signal more interest rates cuts to fulfil that side of their mandate. Chair Powell has always stated that sharply weaker labour market conditions would drive earlier interest rate cuts.

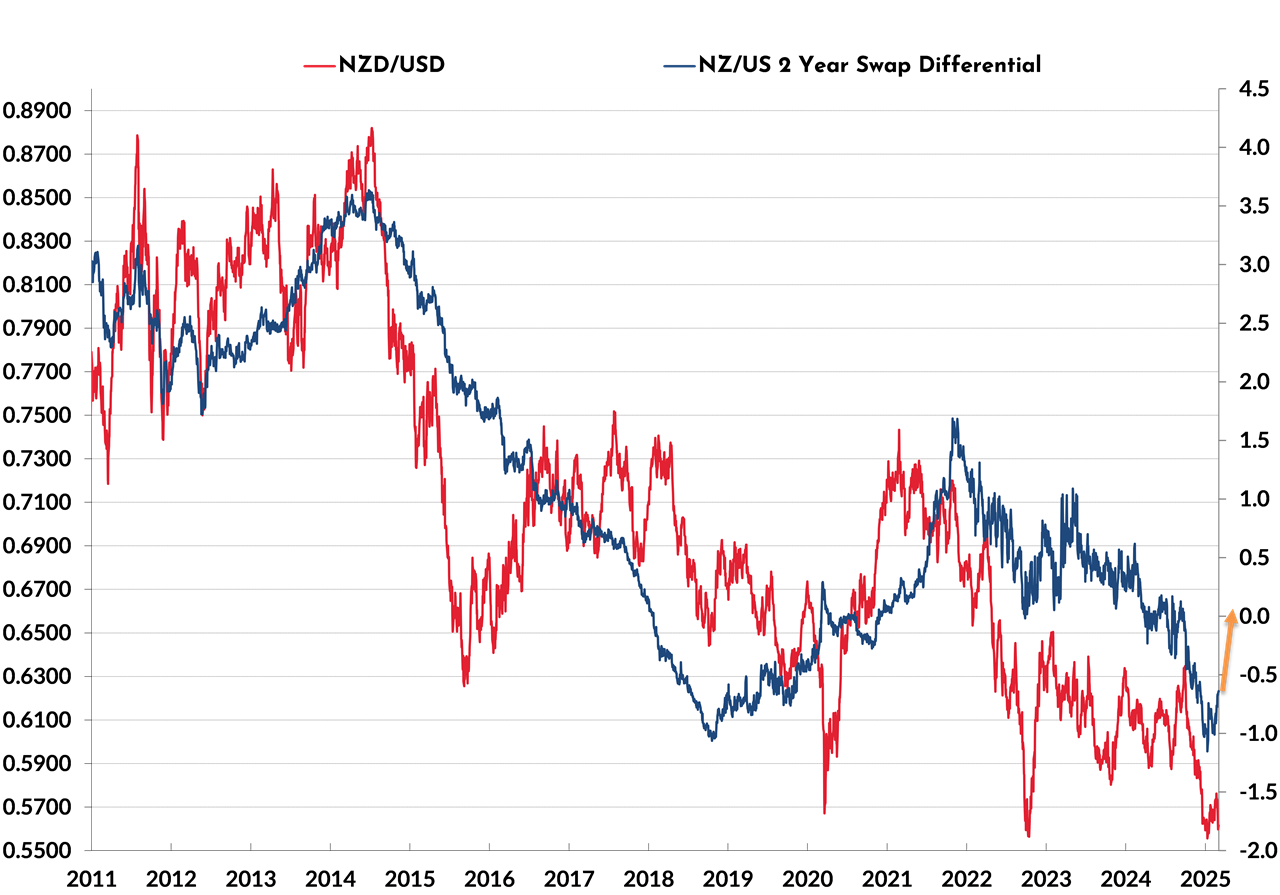

What does the US economic slowdown mean for the NZD/USD exchange rate?

The Kiwi dollar is unlikely to make meaningful gains to back above 0.6000 until the interest rate differential to the USD closes up. Currently, US two-year swap interest rates are 4.08% (they were 4.48% a month ago) and the NZ two-year swap rate is 3.43%, calculating to a 0.65% gap. The NZ two-year swap rate is already pricing in one to two further 0.25% OCR cuts and therefore is unlikely to go any lower. The US two-year rate appears primed for further significant falls as the Fed are forced to more interest rate cuts this year. The current 0.65% interest rate gap is likely to close to zero over coming months. History tells us that when this happens (blue swap differential line in the chart below moving up to zero, right-hand axis), the NZD/USD exchange rate generally follows.

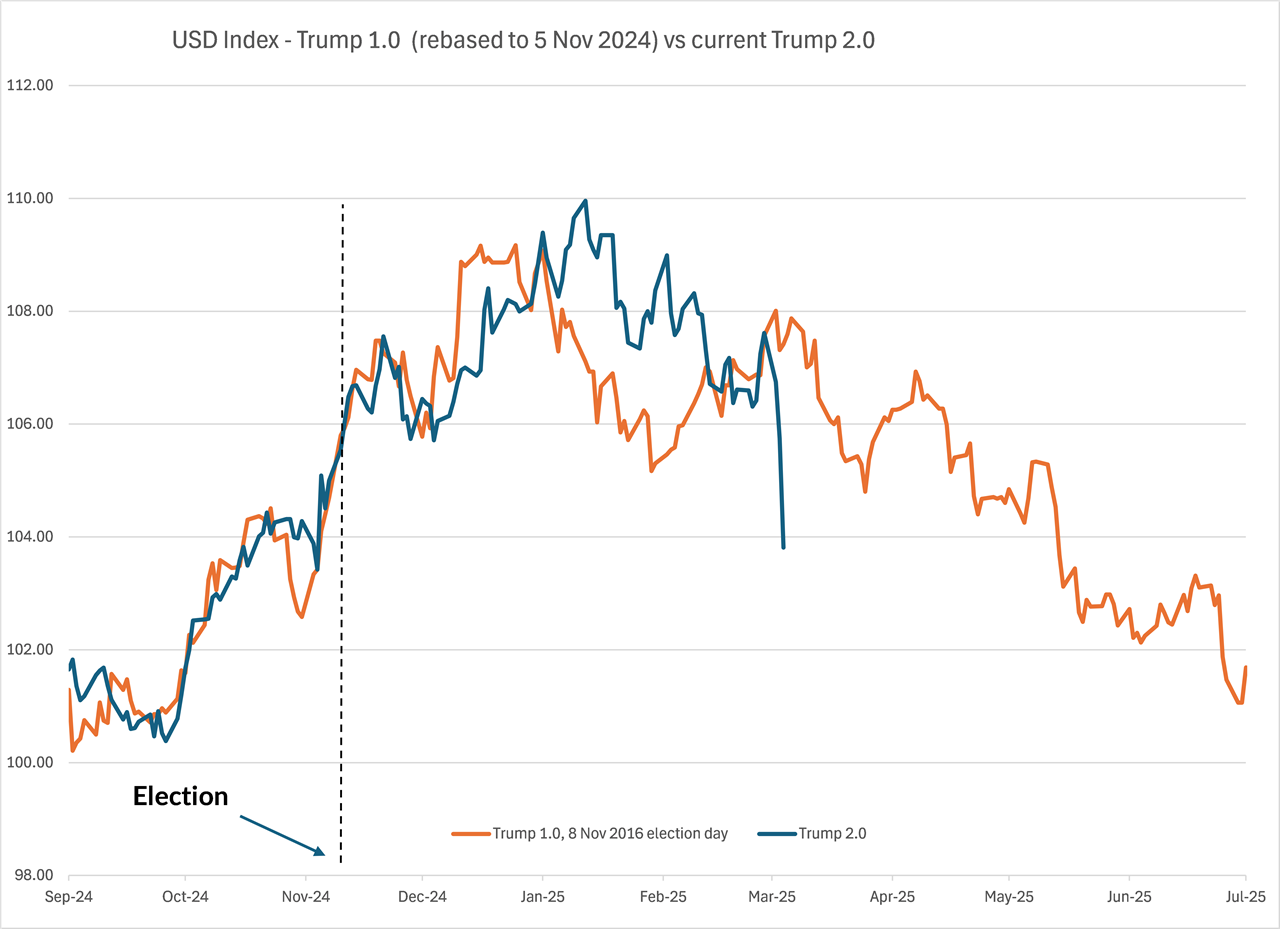

The USD Dixy Index continues to follow the script in Trump 2.0 compared to eight years ago in Trump 1.0. The USD is now falling earlier and faster than eight years ago as the FX markets rapidly price-out US economic “exceptionalism”. A return to where the USD started at 100 on the Dixy Index seems likely.

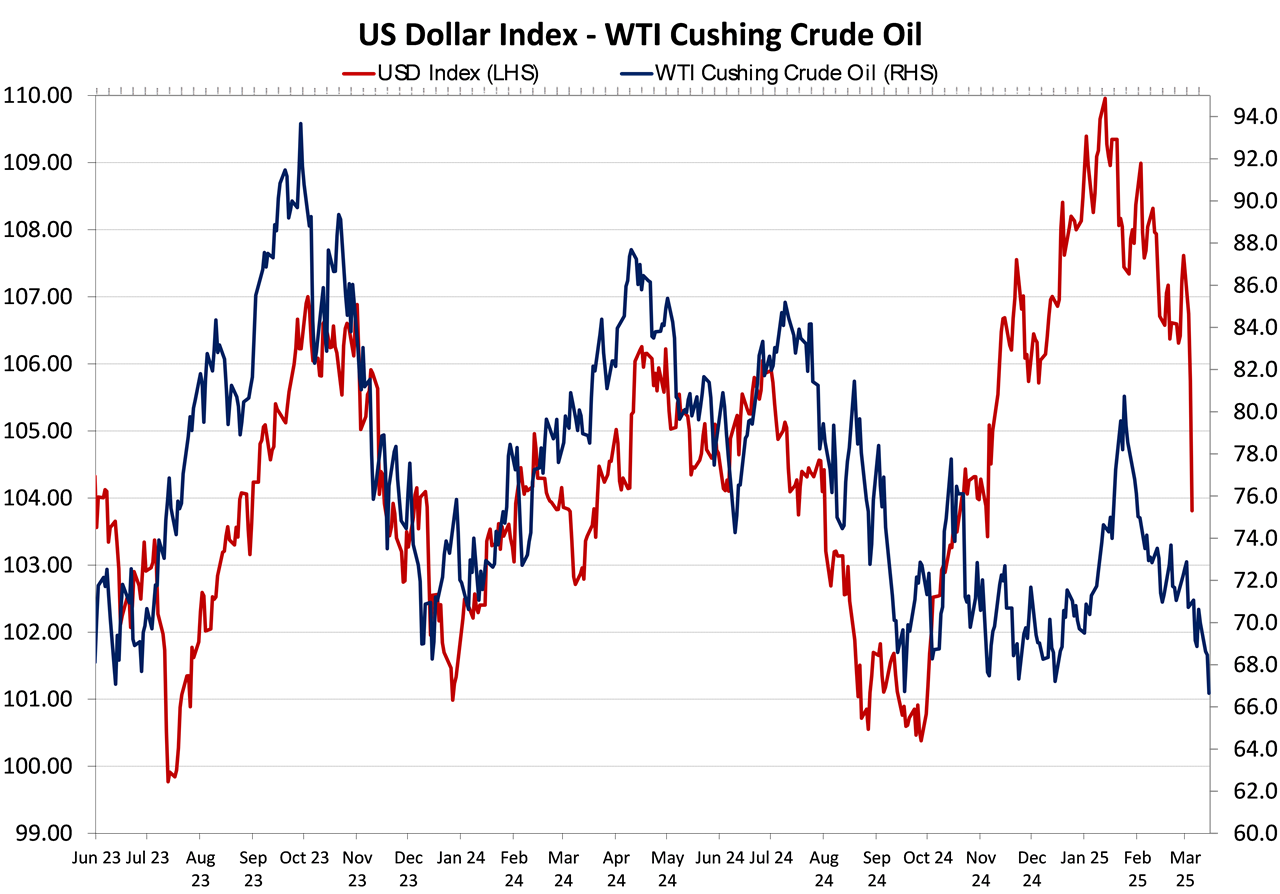

Maybe a method in Trump’s madness as oil prices tumble

The US dollar has been correlated to WTI crude oil prices since mid-2023. Oil prices are currently decreasing as Trump cajoled OPEC+ to remove oil production restrictions and an end to the Ukrainian/Russia war will remove sanctions on Russian exports of oil. Further falls in oil prices seem likely and that will allow headline inflation in the US to move lower, pushing US interest rates down.

The very strange affair of Adrian Orr’s departure

Whatever the real reason for Adrian Orr’s sudden departure as Reserve Bank Governor last week (most likely a combination of factors), the same-day exit is not a good look for how New Zealand runs things. All very embarrassing from an offshore observer looking in and wondering what the hell is going on.

The popular perception of Governor Orr was that he was the guy that allowed monetary policy to be too loose in the Covid years of 2020/2021, that produced 2.00% to 3.00% mortgage interest rates. The ultra-cheap money fuelled a spending and property boom that ended in tears as the RBNZ arguably tightened policy too rapidly by increasing interest rates to 5.50% in 2023, to combat the resultant inflation. All very easy to point the finger in hindsight of course. As all financial and investment market participants know, all decisions are judgement calls at the time and subsequent criticism is not that helpful. The biggest policy error the RBNZ made through that period, which rightfully can be criticised, was the continuation of their lending of cheap money to the banks long after it was needed and with no strings attached.

Whilst the media have centred on Adrian Orr’s falling out with Finance Minister Nicola Willis over the RBNZ cost-base and bank capital requirements, due recognition should be given to Adrian for taking an ultimately successful stance against the Australian Government and banks who wanted to take over New Zealand’s complete financial system a few years back.

Adrian always liked to make a splash and wrong-foot the markets with his monetary policy statements. So, perhaps no surprise that he went out with a non-conformist bang!

Big hitter investors absent from NZ investment summit

We should all hope that this week’s investment summit is a successful event for the Government and contacts are secured for large-scale foreign investment inflows into our infrastructure projects and industry opportunities. The attendee list has been published with the normal long list of local lawyers and bankers, as well some overseas infrastructure investors. However, what is somewhat disappointing is that the organisers have not been able to attract any of the largest sovereign wealth funds from around the globe. The 10 largest sovereign wealth funds are from Norway, the Middle East, China, Singapore and Hong Kong. The Australian Future Fund is the 19th largest in the world by asset size (US$150 billion), but they are not coming. The NZ Super Fund is number 33 on the sovereign wealth fund list (assets of US$48 billion), at least they are attending the summit!

Coming out of the summit, the challenge will be for the executives appointed to the new Invest New Zealand entity to travel the world selling the NZ investment opportunities to these sovereign wealth funds who are always seeking geographical diversification for their funds. The Prime Minister, Christopher Luxon does an excellent job promoting New Zealand when travelling overseas. It now requires a concerted campaign by Invest New Zealand to follow up and cement those opportunities.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

Approaching 250 years ago the forefathers wrote the US constitution and set up the structure of both houses of the US government. In so doing they installed conditions, restraints and safeguards that sought to preclude any Presidency in power becoming totalitarian. Lincoln during the civil war tested this for instance, the Sedition Act and the suspension of habeas corpus. Trump though is being allowed to proceed as nothing that was established in 1789 exists any longer. That this could occur is only due to the weakness and corruption of the Senators and Congressmen that have abetted in the defeat of the careful wisdom of the nation’s great forefathers.

However, what is somewhat disappointing is that the organisers have not been able to attract any of the largest sovereign wealth funds from around the globe.

Lack of faith in the coalition of chaos.

As a purely speculative exercise, I wonder: is Elon Musk is buying back his now heavily discounted Tesla stock and if other giant corporations are doing the same with theirs?

Or is that just far too conspiratorial?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.