Summary of key points:-

- White House “spat” risk event spurs the US dollar higher

- The US bond market signals a weaker US economic outlook

- Will optimistic NZ business confidence lead to stronger GDP growth?

White House “spat” risk event spurs the US dollar higher

The fledgling NZ dollar recovery from 0.5500 to 0.6000 has been turned on its head due to a spat between participants at a meeting in the White House.

A continuing de-escalation in global geo-political risk was on the cards last Friday as Ukrainian President Volodymyr Zelensky met with US President Donald Trump to sign a deal that would give the US access to Ukrainian minerals in exchange for security guarantees for Ukraine. The expectation was that this would be a further step to end the Ukrainian/Russian war. Unfortunately, the calm discussion rapidly descended into a slanging match as Mr Zelensky reacted badly to Trump’s boofhead henchman, Vice President JD Vance, stating that Zelensky should have used “diplomacy” with Putin. Trump’s regime does like to re-write history in conveniently forgetting that the Russians illegally invaded another country. The Americans want a deal to end the war, but only on their terms. They attack anyone who questions their stated position (whether their position is correct or not, does not seem to matter!). A ceasefire and the commencement of a peace treaty agreement does seem a lot further away as the meeting ended in acrimony. However, President Zelensky knows that he cannot win against the Russian without US military support. Whilst the Europeans may protest at the US’s bully-boy tactics, the reality is that if Zelensky continues the fight without US support he will eventually lose to the Russians with much further loss of life for his citizens. The Americans do hold the cards, and Zelensky does not, as Donald Trump has been keen to repeat.

As could be expected, the currency markets reacted instantaneously to a situation where an expected reduction in geo-political risk was replaced by increased tensions. The US dollar immediately appreciated from 106.50 on the USD Dixy Index to 107.56. As a consequence, the NZD/USD rate dropped one cent from 0.5700 to 0.5600. The FX market’s response to the deteriorating geo-political risk situation was understandable, however there is more water to go under the bridge on President Trump’s endeavour secure peace by ending the Ukrainian/Russian war. President Zelensky and his European NATO partners must know that they inevitably have to bow to the US’s wishes. Therefore, Zelensky will apologies and come back to the table on Trump’s minerals deal that should end the war.

In the past, the FX market’s reaction to sudden increased global geo-political risk is always extreme US dollar appreciation in the short-term. However, the markets quickly move on to the next economic development and the knee-jerk response to the non-economic shock or risk event is nearly always temporary. Relative economic performance over the medium to longer term ultimately drives exchange rate changes. Three years ago, when the Ukrainian/Russian war started the US dollar immediately appreciated as inflation increased with the resultant higher oil/commodity prices and supply chain disruptions. The US dollar appreciated from 97.00 in February 2023 to a high of 114.00 by September 2023, however it was the Fed’s rapid hiking of interest rates, after they realised that the inflation was not temporary, that caused the USD appreciation. It is not the same situation today, with US inflation still decreasing (albeit risks of increasing again later in the year with Trump’s tariffs).

The spike up in the US dollar could well prove to be temporary if Volodymyr Zelensky works out which side his bread is buttered, which he is likely to do. Therefore, local US dollar exporters should use this unexpected dip in the Kiwi dollar to 0.5600 as another opportunity to add to long-term hedging against the risk of the US dollar depreciation on a weaker US economy and the Fed being forced back to two or three 0.25% cuts to interest rates this year, instead of the current pricing of only one 0.25% cut in September.

The US bond market signals a weaker US economic outlook

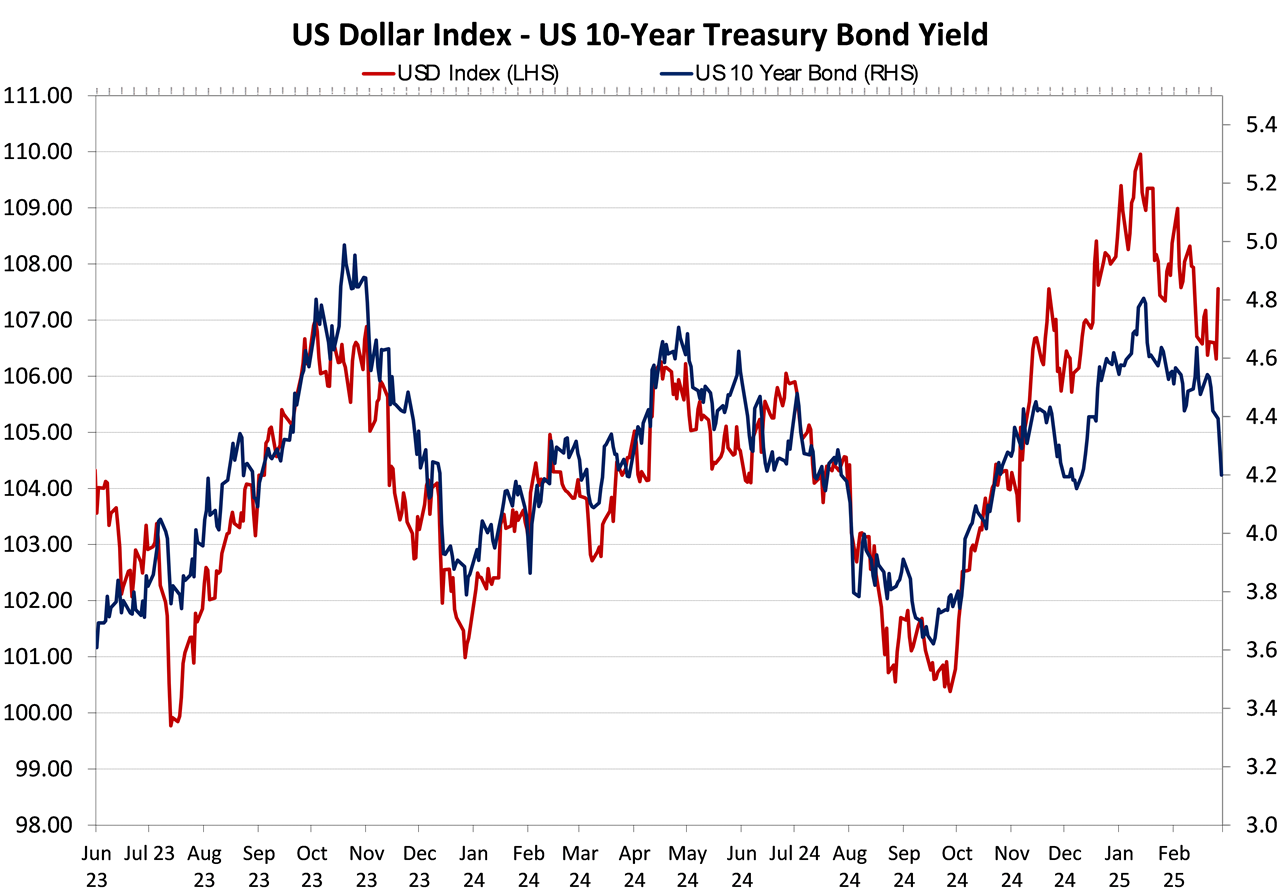

Whilst the USD has gone one way on the White House “spat”, the yields of US 10-year Treasury Bonds have moved in the opposite direction (refer to the chart below). The bond market has disregarded the events at the White House, instead the market has reacted to the latest US inflation result and other softer economic data and priced yields lower to 4.20%. President Trump’s latest claim the US economy is “breaking records” is more likely to be a record decrease in GDP growth from 2.30% for the year to 31 December 2024 to something a lot lower over coming months.

As the chart confirms, the USD Dixy Index is highly correlated to US 10-year bond yields as the bond yields adjust to changing expectations about US inflation direction and likely Fed responses with interest rate settings. The USD Index may temporarily diverge from the bond yields (as it is currently), however the economic reality of what lower bond yields are signalling, in the form of lower inflation and weaker growth, is ultimately negative for the US dollar value. For this reason, we do not expect the spike higher in the USD Index to 107.56 to last very long. It will reverse lower earlier if Zelensky comes back to the table with the Trump “revisionists”.

The sharply lower US 10-year bond yield over the last two weeks from 4.65% in mid-February to 4.20% today has come about as both investors and borrowers’ price-in a weaker US economic outlook: -

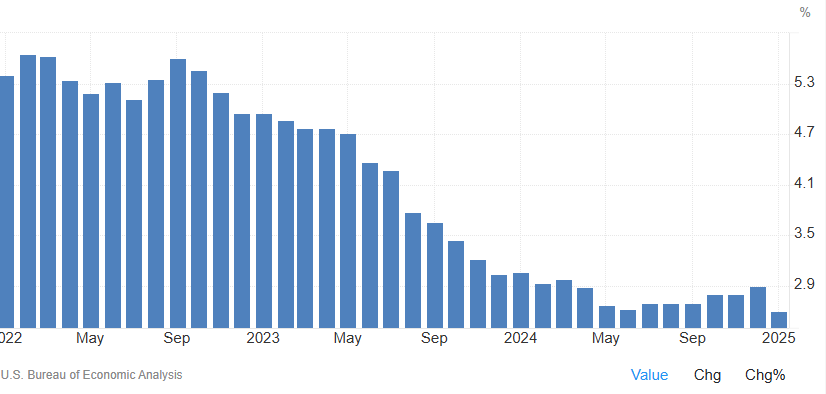

- PCE inflation for the month of January (released Friday 28th February) came in bang on prior forecasts at +0.30% (for both core and headline inflation). The annual core rate of inflation reducing from 2.90% in December to 2.60% in January (see bar chart below). The current lower trend of the inflation rate is the exact opposite of what the markets were earlier pricing and expecting.

- US economic data that printed softer than consensus forecasts last week included the Chicago Fed National Activity Index, Dallas Fed Manufacturing Index, Conference Board Consumer Confidence, Building Permits, New Home Sales and PCE Personal Spending for January (-0.20% versus a forecast of +0.30%).

- Economic releases this coming week which are also expected to be weaker include, ISM Manufacturing PMI, ADP Employment Change, ISM Services PMI, Factory Orders and Non- Farm Payrolls employment figures for February on Friday night, wherein a jobs increase below the 150,000 forecast is likely.

As we have stated previously, the DOGE slashing of US Federal Government jobs must eventually have a significant impact on the Non-Farm Payrolls employment measure, as a big part of the jobs increases over the last two years has been the Government sector (along with healthcare and hospitality). The government jobs increases are no longer occurring. Whilst the number of Federal Government jobs being chopped is only a tiny proportion of the total US workforce, it is the change on the margin from consistent Government job increases to some decreases that will show up as softer overall employment data.

The next Fed meeting is 19th March, so it will be too early for the accumulating weaker trends in the US economy to change their current stance on interest rate cuts. However, by the following meeting on May 7th, several months of softer than expected US data should force a Fed re-think, particularly on the employment side of their mandate as the inflation outlook may be clouded by tariffs. However, falling oil prices (now below US$70/barrel) and much weaker consumer demand in the US economy may well start to offset the inflationary impact of tariffs.

US PCE Inflation – Last three Years

The higher USD Index also reflects Trump’s latest announcements of doubling-down on tariffs with China (increased from 10% to 20%) and Europe (25% threatened and to be announced soon).

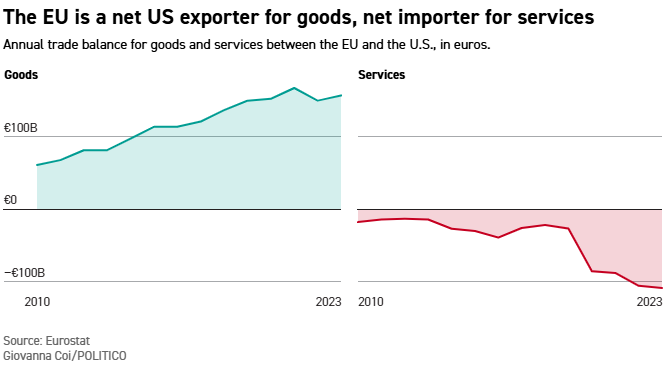

Yet again, Trump’s selective use of the facts with the US’s large trade deficit with Europe as a justification for “evening the playing field” with tariffs on imports from Europe does not stand up to scrutiny. As the chart below confirms, Europe may export more goods to the US compared to what they import from the US, however in respect to services, Europe is a massive net buyer of US services. No-one wins with tariffs, the US economy will be weaker if the Europeans retaliate by imposing restrictions on their companies’ buying services from the US. Trump does not understand how globalised business services and modern economies work, he just thinks the Europeans should buy more US manufactured (gas-guzzling and expensive) motor vehicles.

Will optimistic NZ business confidence lead to stronger GDP growth?

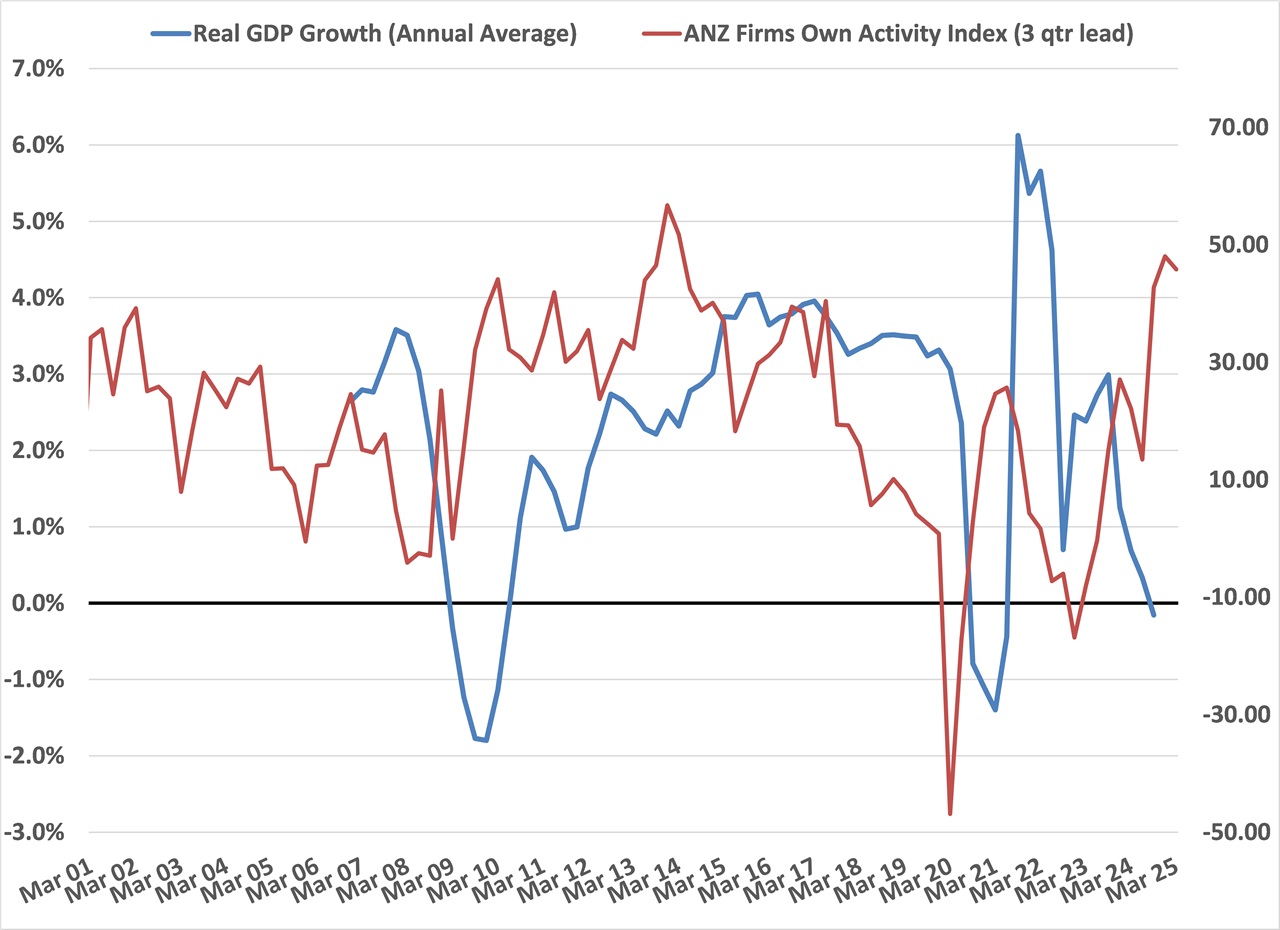

We continue to observe that there are many “doubting Tom’s” when it comes to expecting a strong rebound in GDP growth this year for the New Zealand economy. The chart below of local business firm’s expectations of their own activity levels looking ahead, plotted against GDP growth, points to a rapid lift in overall economic expansion over the next 12 month’s to somewhere near to +4.00%. The last time the own activity index was this high was the dairy commodity price boom in 2014, which propelled GDP growth to 4.00%. Local economic forecasters (including the RBNZ and The Treasury) continue to underestimate the power of record high export commodity prices for the NZ economy.

However, even though the very positive NZ economic story for 2025 will eventually be recognised by offshore traders and investors, it does not automatically mean the NZ dollar will appreciate on its own accord. It also requires the interest rate differential between the US and New Zealand to close back up to zero or positive (NZ above the US). If that happens, the NZD buyers get a positive carry and are not paying away points to hold the Kiwi, as is currently the case. Over coming months, our inflation rate is expected to increase from rising food prices and the lower NZ dollar value on import costs. Therefore, the NZ two-year swap interest rate is not expected to decrease any further and could actually increase from its current low 3.41% level. US two-year swap rates at currently 3.93%, delivering a 0.50% gap above NZ swap rates. The 0.50% differential is expected to close up to zero over coming months as US interest rates continuing to decrease on the expected softer US economic data.

At that point the current disincentive to buy the Kiwi dollar will be removed.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.