Summary of key points: -

- US consumer’s mood turns sour against Trump policies

- The Japanese Yen appreciates and has much further to go

- Positive impulses to the NZ economy being underestimated

- Is the NZ Dollar really at “Fair Value”?

US consumer’s mood turns sour against Trump policies

The confidence and sentiment of US business firms and households, which was so positive prior to the election of Donald Trump as President late last year, is progressively turning the other way as the economic ramifications of his aggressive policy shifts sinks in.

The sharp downturn in US retail sales numbers for January was the first indicator of consumer’s hesitancy, the pullback in the University of Michigan Consumer Confidence survey released Friday 21st February confirming that household spending will be very subdued over coming months. The consumer sentiment index coming in at 64.7 against prior consensus forecasts of 67.8. A whopping increase in US credit card debt levels is one reason why a slowdown in inevitable. Many US households have paid for the large price increases over recent years by putting it on the plastic, and they are now maxing out on the limits. The more cautious households are reflecting worries about potential price increases from tariffs and interest rate not falling as much this year as expected a few months ago. US business firms are also less optimistic about the future, the S&P services and manufacturing PMI surveys released last Friday were all much weaker than expected.

Many other key US economic indicators are expected to print on the softer side over coming weeks/months as a result of the financial pressures mentioned above, as well as the Trump regime’s chainsaw attack on Federal Government institutions and jobs: -

- The PCE inflation result for January being released this coming Friday is expected to be close to +0.30%, causing the annual core rate of inflation to reduce from the current 2.80%. The markets are pricing for the opposite direction in inflation, therefore anticipate some surprises and further decreases in both US bond yields and the US dollar value as a result.

- Non-Farm Payrolls employment data the following Friday 7th March will also be prone to a negative surprise as Government jobs decrease after two years of consistent increases. All other industry sectors in the US (except healthcare) have recorded absolutely no increases in jobs over the last 12 months.

- New builds in residential property is slowing abruptly as interest rates for new mortgages move above 7.00% again, which few people can afford.

The financial and investment markets received another reminder of the economic reality for Americans at this time, when Walmart reported lower profits and a bleaker outlook for retail sales. The tumble in their share price reflecting the uncertain times as Trump creates chaos to implement change. The “exceptionalism” the US economy has enjoyed over others in recent years is coming to an end as their GDP growth looks set to disappoint this year and European share markets have outperformed US markets since the start of the year.

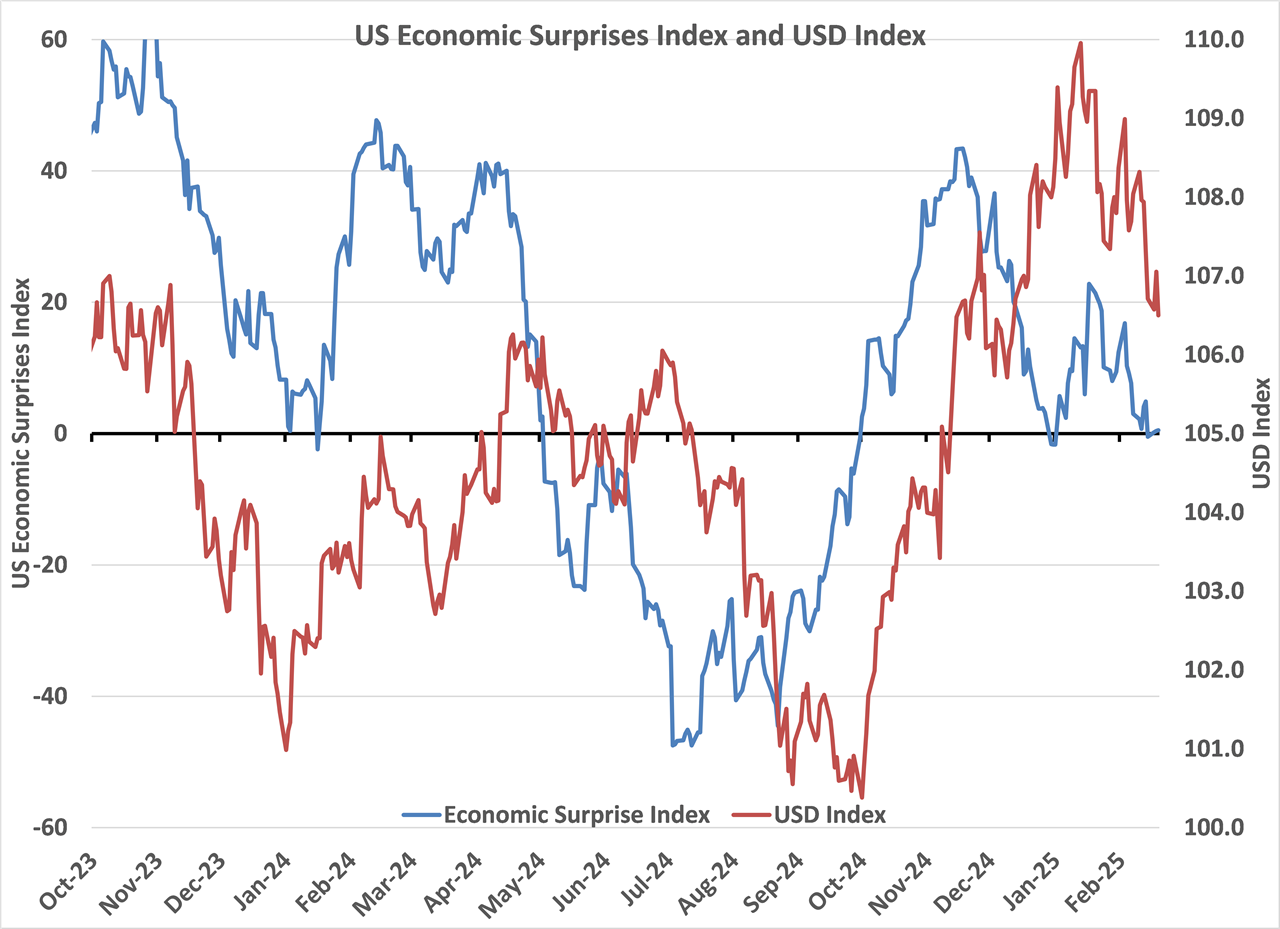

The chart below illustrates the relationship between “economic surprises” and the US dollar value. When the Economic Surprise Index (blue line) moves below zero, all the actual results of economic data releases are coming out weaker than prior consensus forecasts (and vice-versa). The blue line is heading for a period below zero over coming months (similar to the May to October 2024 period) which points to further depreciation in the USD, as the markets reverse again to pricing more Fed interest rate cuts.

The Economic Surprise Index decreasing below zero would send the USD Index back to 102.00.

The Japanese Yen appreciates and has much further to go

The next major influence at this time on the NZD/USD and AUD/USD exchange rate movements, after general US dollar changes due to US economic data, is the direction of the Japanese Yen against the USD. The Japanese are set to increase their interest rates again soon as their inflation, wages and GDP growth are all increasing at a more robust pace than forecast. The Japanese interest rate increases are occurring when everyone else in the world is cutting their interest rates. The complete opposite situation to recent history.

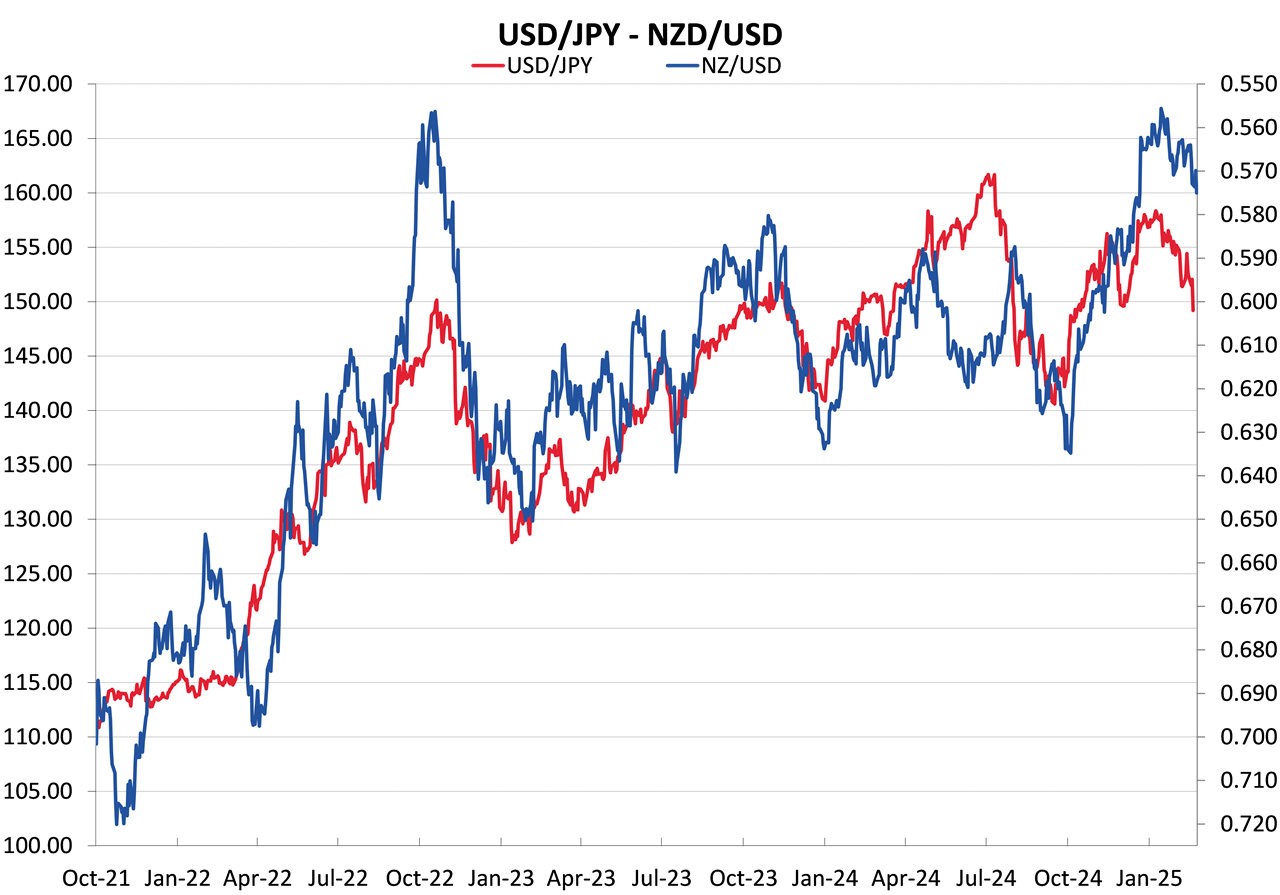

Japanese 10-year bond yields will be increasing at a time when US 10-year bond yields are rapidly falling back towards 4.00% (currently 4.40%). The bond yield differential reducing from the current 3.00% to 2.50% will force Japanese investment houses to repatriate funds home as the attraction of US bonds reduces. They buy Yen, sell USD to implement the re-allocation of funds. The USD/JPY exchange rate in tracking the bond yield differential is poised to decrease further from the current 149.20 level to 140.00 and possibly 130.00 over coming weeks/months.

In decreasing their USD investment weightings, the Japanese are not necessarily only re-investing all the funds in their home markets. There was news out this last week that Japanese giant Mitsui has made the biggest investment in its 78-year history, paying $US5.34 billion (A$8.4 billion) for a stake in the Rhodes Ridge iron ore project in the Pilbara in a bid to secure guaranteed reserves of the resource to make steel and counter the rise of China. Cross-border capital inflows into Australia have in the past been major forces in pushing the Aussie dollar value up. Looks like the cycle is finally turning back to such influences merging again.

Forecast additional gains in the Japanese Yen exchange rate against the USD to 140.00 and 130.00 would see the NZD/USD rate appreciating to the 0.6250 to 0.6500 region (refer to the chart below). The Kiwi dollar does have some “catching up” to do against the USD/JPY movements. The projected increases in NZ inflation over the short-term, as the RBNZ highlighted last week, is the sort of economic trend that may single the Kiwi dollar out as being clearly undervalued at rates below 0.6000. If our inflation prints higher in the short term, the pricing of three more 0.25% OCR cuts this year will quickly disappear. One problem with this scenario is that we only measure our inflation rate quarterly! We need a Trump-like attack on Statistics New Zealand to get some change.

Positive impulses to the NZ economy being underestimated

The RBNZ’s monetary policy statement last week in analysing and forecasting the New Zealand economy was consistent with what we currently see from bank economists and other private sector economic forecasting firms. They over-emphasise the importance of domestic economic conditions (retail and housing) and underestimate the power and influence over the main driver of the economy – the export sector.

Looking ahead, instead of looking backwards at the short/sharp economic recession in 2024, there are two very large positive impulses arriving at the same time in 2025 that stand to propel our economy forward with a dramatic recovery to +3.00% GDP growth by the end of the year.

Impulse 1: Export prices, profits and investment

The additional billions of dollars coming into the NZ economy as a result of record high export commodity prices and the cyclically low value of the NZ dollar is about to push regional spending and investment levels sharply higher this year. One simple example is farmers using the extra cash available to buy more fertiliser before 31 March and 30 June year-ends so as to have a higher tax- deductible expense to reduce their tax bill. Dairy, lamb, beef, aluminium and horticulture export prices have increased dramatically and even export log prices have stabilised. The lower Kiwi dollar value is lifting NZD log prices and stimulating increased forestry harvesting. Add in the growing foreign tourist and foreign student numbers again, the positive story becomes even better.

Off course, there is always risks that prices, markets and supply can change. However, prudent risk management with forward hedging is available to mitigate such risks.

Impulse 2: Increased consumer spending from lower mortgage interest rates

Total market weighted-average mortgage interest rates are just over 6.00% currently, with market interest rates decreasing and something like 80% of fixed rate mortgages re-pricing at much lower rates over the next 12 months. The cash released (from that cost adjustment) into the economy is very significant. Provided general job security is maintained, most homeowners with mortgages will be spending the difference after a few years of belt-tightening. With the Kiwi dollar at a low level, more expensive overseas holidays will be down the priority list for most, therefore the extra cash will be spent locally.

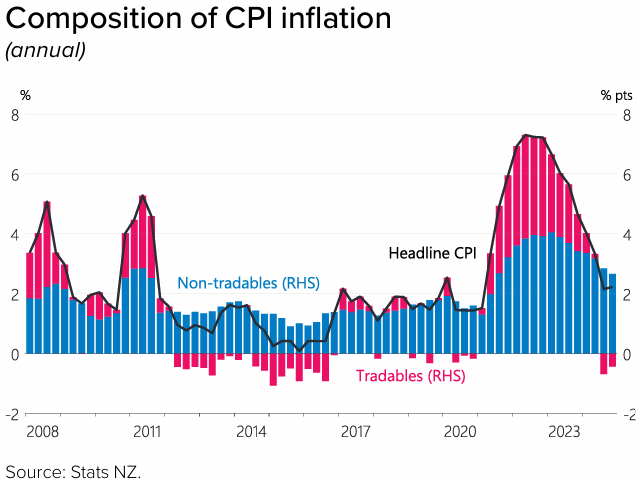

The RBNZ, in their monetary policy statement last week, highlighted the fact that they see tradeable inflation increasing over coming months. However, the are confidently forecasting that non-tradable inflation (blue bars in the above chart) will continue to decline as there is excess capacity (i.e. underutilised capacity) in the economy. Therefore, they do not expect the overall inflation rate increase. It is hard to be as confident as the RBNZ on this outlook, as nearly all the historically sticky non-tradable inflation comes from the public sector and non-competitive private sectors. Price increases still seem to occur from these sources, no matter what the capacity utilisation level prevailing in the economy. Continuing decreases in non-tradable inflation below 2.00% seem highly unlikely.

There is a better than even chance that actual inflation this year will be above RBNZ forecasts, which in turn leads to fewer interest rate cuts than currently priced i.e. NZD appreciation on its own bat.

Is the NZ Dollar really at “Fair Value”?

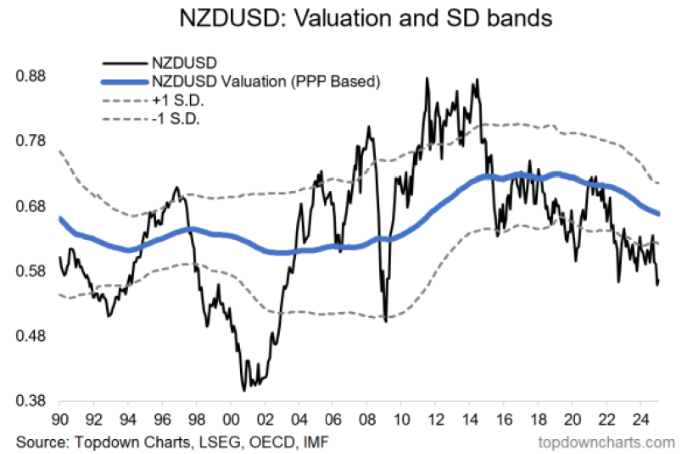

RBNZ Governor Adrian Orr made the statement in the media conference following the release of the monetary policy statement last Wednesday that the “NZ dollar was currently at about fair value”. It may have been a flippant comment or a throw-away line, however whenever a central bank head pontificates on their own currency’s value it always attracts attention from market participants. Whether the NZ dollar at 0.5700 against the USD and at cyclical lows against the EUR, GBP and AUD on the cross-rates is at “fair value” right now is a matter of judgement, normally backed up by some scientific analysis that calculates the fair value based on relative economic variables. The RBNZ do not publish their own fair value (also called PPP – Purchasing Power Parity and Equilibrium Exchange Rate) calculation, the last RBNZ discussion paper on the topic was more than a decade ago.

The following two charts are recent comparisons of a calculated NZ dollar fair values against actual NZD/USD exchange rates (from BNZ and Topdowncharts). From this evidence, Mr Orr is well off the mark in his assessment of the current NZD fair value – about 10 cents off! Fair value comes in at close to 0.6700.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

2 Comments

Councils like Nelson could care less about the impact of non-tradable inflation. These councils have increased rates and spending far, far above the general inflation rate. Somebody needs to bring these councils into line. For councils like Nelson, much of the increases in rates and spending (and borrowing) is for nice to haves, not essentials.

Thanks, Roger. Always much food for thought. Much appreciated.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.