Summary of key points:-

- Long US dollar “Trump Trade” conviction wanes

- RBNZ 0.50% OCR cut already fully priced-in to Kiwi dollar market

- The Aussie Dollar will fly if RBA Governor Bullock wrong-foots the markets

- Good news for our export/import sectors – sea freight costs plummet

Long US dollar “Trump Trade” conviction wanes

The “Trump Trade” bull-run higher in the US dollar value from 101.00 on the Dixy Index last October to a high of 110.00 in late January has certainly run out of steam over the last two weeks. The USD buying was based on the election of Donald Trump as President would be positive for USD GDP growth, cause higher inflation due to tariffs and therefore remove any interest rate cuts by the Fed in 2025. US interest rates remaining higher than others is US dollar positive.

The market conviction around those expectations turning into reality this year has sharply reduced for two principal reasons:-

- The telephone call between Russian leader Vladimir Putin and President Trump last week, wherein they agreed to start peace talks on the Russian/Ukraine war, has been a negative factor for the US dollar value as global geo-political risk has de-escalated. Readers will recall that the USD appreciated three years ago when the war commenced as it benefited from safe haven flows out of the nearby Euro currency. It naturally follows that the USD depreciates as geo-political risk decreases.

- US Retail Sales for the month of January fell away sharply on the December levels. Prior consensus forecasts were for January to be flat with December, however they declined 0.90% with severe weather and the LA fires weighing on consumer spending.

There are now clear signs that the US economic “exceptionalism” period of continuous robust GDP growth and gains in equity markets, despite restrictive monetary policy settings over recent years, is coming to an end. There was clearly an element of consumers buying goods up in December before tariff-induced price increases, however that has not continued into January.

The US dollar Index depreciated last week despite US CPI inflation figures for the month of January coming out much higher than expected. The CPI Index lifted 0.50% in January, well above the +0.20% expected. However, the Fed will not be reacting to one month’s numbers that appear to be an “outlier” result. The largest contributors to the price increases were eggs and gasoline due to the bird flu problem and higher crude oil prices in early January to US$78.70/barrel. Oil prices have since dropped away to US$70.70/barrel on the Israel/Hamas ceasefire in Gaza. The Putin/Trump telephone call hitting the newswires a matter of hours following the CPI release, reversing the USD direction from higher to lower. Wholesale prices (Producers Price Index) for January released last week were also above prior forecasts. However, the FX markets interpreted some trends in a number of the sub-components of the index as indicating reduced upward pressure on general inflation over coming months.

Since the start of February, the USD Index has dramatically reversed in direction, tumbling from the 110.00 peak to close at 106.67 last Friday. There is no question that the sharp reversal in the USD direction would have dented the confidence of the USD bulls that the USD an continue its upward trajectory. We have already seen some profit-taking on the long-USD positions (i.e. USD selling to unwind) and we could witness a whole lot more as the USD Index breaks below key support levels around 107.00. After a number of false starts, the “Trump Trades” finally appear to be unwinding as all the positives are fully priced-in and some negatives, as outlined above, seed doubt and uncertainty in the minds of the USD bulls.

The USD Index is now following US 10-year Treasury Bond yields lower (refer to the chart below). The Treasury Bond yields have the potential to fall considerably further to below 4.00% (currently 4.47%) over coming weeks/months for the following prime reasons:-

- The Trump regime is reducing Government spending, reducing the size of the fiscal deficit, and in turn reducing the amount of new debt being issued. Less supply equates to higher bond prices, which equals lower bond yields.

- Weaker Non-Farm Payroll jobs numbers over coming months as the big growth sector for jobs over the last two years, the Government sector, reverses to job losses as Elon Musk’s DOGE (Department of Government Efficiency) brutally slashes Federal Government institutions and jobs.

- The Fed preferred PCE Price Index measure of core inflation being released on 28th February showing a sharp decrease in the annual rate from the current 2.80%, as the large 0.50% increase in January 2024 drops out of the annual calculation.

A series of softer economic data prints, similar to the Retail Sales numbers last week, will lead to a rapid shift in interest rate market pricing for Fed rate cuts this year and then the inevitable flip-flop from the Fed FOMC Committee members as they adjust their “dot-plot” interest rate forecast lower again. The expected change in US interest rate market pricing to lower yields is all negative for the US dollar.

RBNZ 0.50% OCR cut already fully priced-in to Kiwi dollar market

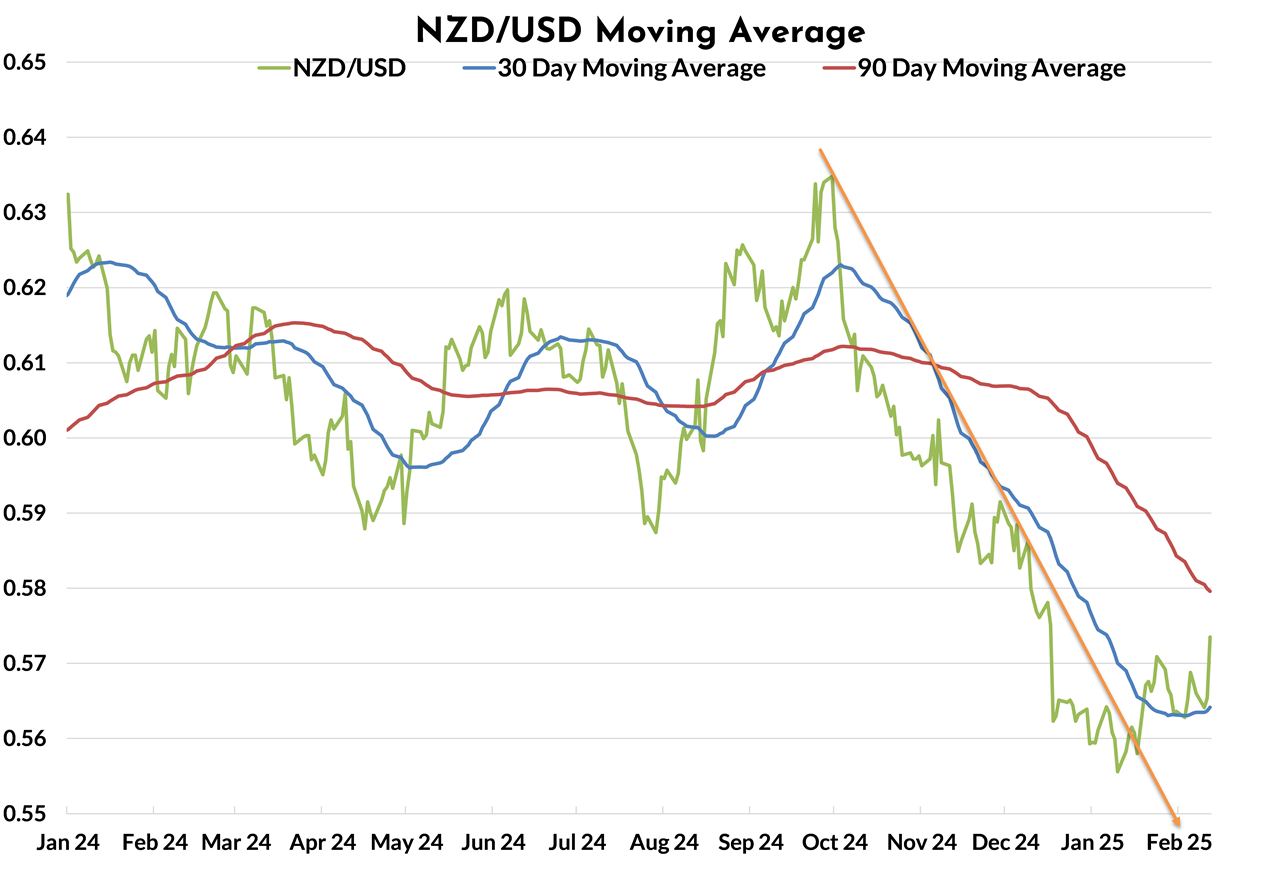

The weaker US dollar from 110.00 to 106.67 over the last two weeks has allowed the NZD/USD exchange rate to recover from trading in the 0.5500’s to move above 0.5700. The NZD/USD spot rate has already moved higher to above the 30-day moving average line and further gains to above 0.5800 will have it dissect the 90-day moving average line (refer to the chart below). The several historical NZ dollar plunges below 0.6000 to 0.5500 have never lasted too long, this current dip is now displaying all the hallmarks of following the previous pattern. As the USD related profit-taking gains further momentum over coming weeks, the Kiwi dollar looks set to return to above 0.6000 without too much trouble.

It is easy to see the USD side of the currency equation continuing to dominate the NZD/USD movements over coming months. Therefore, it was a little surprising to hear our Finance and Economic Growth Minister, Nicola Willis pontificate last week that the Kiwi dollar would adjust downwards if tariffs were imposed on NZ exports into the US. It is never too wise for a Finance Minister to offer a view on our dollar’s direction (up or down) and she should have been briefed on the fact that the USD has already strengthened (NZD weakened) on the expectation of Trump’s tariffs. If the NZ dollar is essentially a proxy for a share price on New Zealand Inc, it is somewhat alarming that the CFO sees and desires a lower share price! There is no indication that Trump will impose tariffs on food imports from New Zealand. New Zealand has no tariffs on US imported goods and we are in a balanced trade position with the US.

Do not expect the NZ dollar to depreciate on its own account following the RBNZ’s 0.50% cut to the OCR this Wednesday 19th February. The updated RBNZ economic forecasts and OCR forward track will be the focus of the markets. It will be interesting to see if the RBNZ even recognise the boom taking place in our export sector with commodity prices going through the roof. Their economic assessment and outlook for 2025 should be considerably more upbeat than their November Monetary Policy Statement. If it is not, you just wonder what the 641 employees at the RBNZ (up from 275 in 2019) are actually doing to keep abreast of developments in the economy at a grass-roots level. It is not as if they don’t have the resources to find out!

The Aussie Dollar will fly if RBA Governor Bullock wrong-foots the markets

The local interest rate market pricing and consensus forecasts of economist sits at a 90% probability that the RBA will cut their OCR by 0.25% to 4.10% on Tuesday 18th February. However, the RBA does have a history of wrong-footing the market and not doing as they confidently expect. The question for RBA Governor Michele Bullock and her Board is whether there is enough evidence that inflation is sustainably reducing to their 2.00% to 3.00% target range and therefore they can ease off on the restrictive monetary policy. Their preferred measure of inflation, the “Trimmed Mean” is running at a 3.20% annual rate, however over the last six months the annualised rate is 2.60%. The proponents for rapid interest rate cuts in Australia point to this trend and that is why there is a high level of expectation that the RBA will cut.

A “no-cut” decision by the RBA would be a major surprise and would send the Aussie dollar soaring higher.

The argument for the RBA to hold off to see more evidence of inflation reducing is based on the following factors: -

- Wages growth is only marginally moderated to 3.50% and productivity is still poor, therefore inflationary.

- The labour market remains strong with monthly increases in jobs over the last 12 months averaging 37,000, substantially above the level of RBA forecasts. Under the RBA’s dual mandate for stable inflation and low unemployment there is no reason to reduce interest rates as employment is strong.

- The Australian dollar currency value has depreciated 9.00% against the USD over the last six months from 0.6900 to 0.6300, causing tradeable inflation to increase in early 2025.

The timing of the RBA’s meeting on Tuesday could not be any worse if it was orchestrated that way, with wages data for the December quarter being released on Wednesday and jobs increases for January on Thursday. Governor Bullock could be embarrassed before the politicians at a select committee on Friday if she cuts interest rates and then both the wages and jobs numbers are stronger than expected.

The most likely outcome, in our humble opinion, is a “hawkish cut” from the RBA, where they message that further interest rate decreases will be some time away whilst the labour market remains strong, and productivity remains weak. The 0.25% interest rate cut is already priced into the AUD FX market, so further Aussie dollar gains appear likely on the “hawkish cut” scenario.

Good news for our export/import sectors – sea freight costs plummet

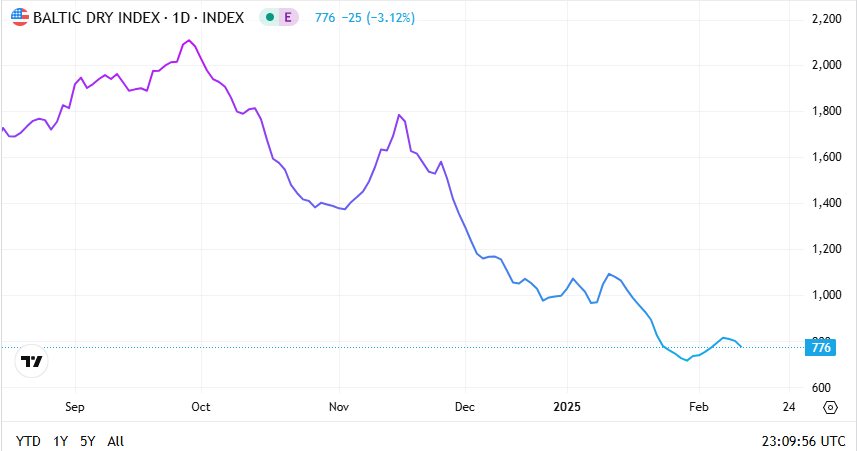

In a dramatic turnaround to previous years, shipping freight costs have plummeted around the world as excess capacity floods the market.

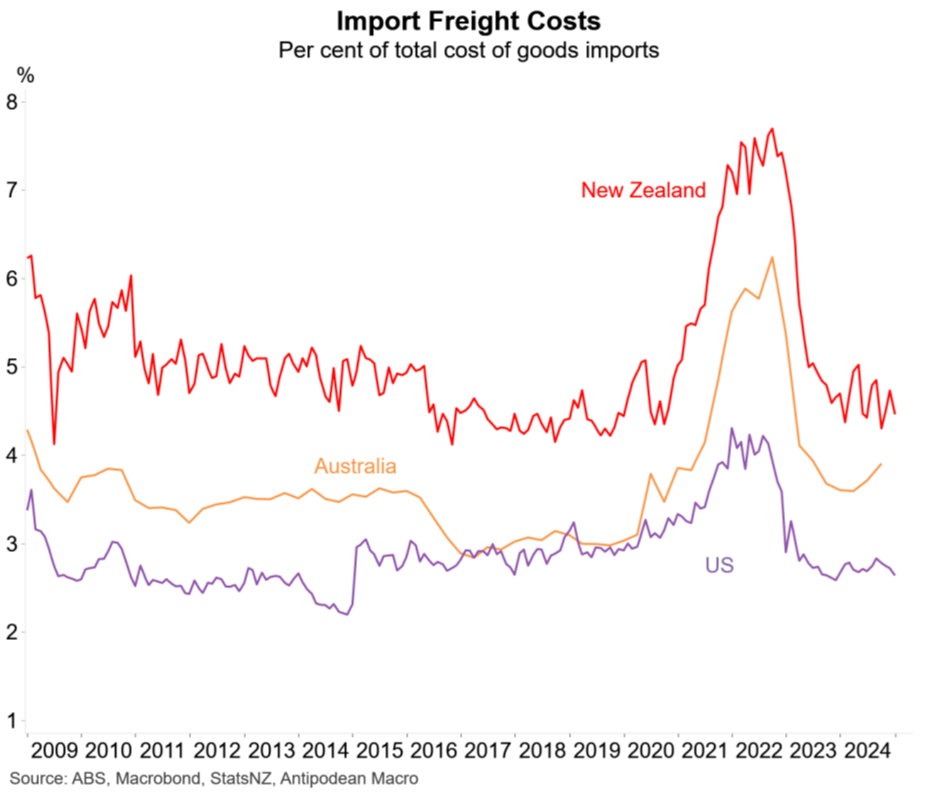

Due to our geographical location on the globe, freight costs as a percentage of imported costs is above Australia and the US (refer to the chart above). The good news is that the percentage will continue to decrease over coming months as the Baltic Dry Index for shipping costs (chart below) has more than halved since October – from 2,000 to 776. Exporter profitability will get a shot in the arm as a key cost of doing business reduces.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

8 Comments

Excellent analysis. Thank you!

“it is never too wise for a Finance Minister to offer a view on our dollar’s direction, ” politely said. It need not have been so much so.

The telephone call between Russian leader Vladimir Putin and President Trump last week, wherein they agreed to start peace talks on the Russian/Ukraine war, has been a negative factor for the US dollar value as global geo-political risk has de-escalated.

This has to be a major concern for society when the value of a countries currency increases when a war is started. raises some questions doesn't it?

How do you think wars are funded Rookie...?

Lets hope Europe will strap on some big boots and start marching because no one can trust USA from now on.

The UK, France, Germany, Italy have economies larger or similar to Russia. The Netherlands, Spain & Sweden not far behind. The USA post WW2 gifted the Continent the Marshall plan. Out of that grew the EEC the ambition of which was self reliance and shared security for all. Yet all thar has happened is a quagmire of infighting, selfish and dismal bureaucracy and a dependence on Russia for energy, China for manufacturing and the USA for defence. As a group they vastly out muscle Russia economically yet they all fear Russia because they have not troubled themselves to set sufficient defences and instead demanded the USA do the heavy lifting. It is their patch. Europe has had century of century of warfare, sides and allegiances ever changing. Have they even forgotten their own history, how many armies have marched through Belgium for a start. Until WW1 there was no involvement from the USA why is their predicament now the responsibility of the USA. Why then too has Europe always been littered with graffiti - go home Yank.

Totally agree Fox. Trump is actually doing Europe a favour. Pity they never listened in his last term. Now they have wasted a lot of time hand wringing and bickering.

Yes nobody with either an equitable or historical mind could disagree. As it happened after I posted that I sat remembered Paul Keating, must be thirty years ago or so, his speech about the flower of youth of the ANZAC serviceman that lie buried in the ground of France and Europe. Yet while the actual people of France, the villagers and so, have remembered paid tribute continuing over the years, not even a sniff of recognition let alone gratitude from the French political leaders. If you needed some hard truth and said in very few words, then Keating was your man and here he was at his best.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.