Summary of key points: -

- Upcoming US economic data unlikely to support the US Dollar bull-run

- The Japanese Yen strengthens against the tide

- The tale of two central banks – implications for the NZD/AUD cross-rate

Upcoming US economic data unlikely to support the US Dollar bull-run

The bull-run of the US dollar on the Trump election euphoria, tariffs and expected higher US inflation lost some of its momentum over this last week.

As a consequence, the NZD/USD exchange rate has been able to settle in the 0.5650 to 0.5700 trading range after recovering upwards from the 2 ½ year lows of 0.5520 the previous week. As the chart below displays, the USD Index has been moving up and back in rapid fashion over recent weeks between 107.00 and 110.00 as the FX market participants become undecided and divided on whether the USD gains since early October 2024 can be sustained. The rapid up and down pricing action/pattern coming at the end of constant USD gains over a four-month period often indicates that the bull-run higher is coming to an end. The USD bulls are questioning whether all the Trump-trade positives for the US dollar are now fully priced-in to the market and whether weaker US economic data reports will cause the USD to depreciate further and reduce their currency profits. Speculative market positioning does have a major influence on exchange rate direction over the short to medium term, however interest rate differentials and relative economic performance are always the key determinants in the longer term.

Outside of Trump left-field, outlandish and bombastic statements (now regarded as par for the course by the markets!), weaker than forecast US economic data releases over coming weeks appear more likely to exert downward pressure on the US Dollar Index as the long-USD position holders unwind and take profits.

Upcoming US economic data releases that have the potential to cause more USD selling than buying include:-

- 12th February: CPI Inflation for January where a 0.20% increase is forecast, leaving the annual rate of inflation unchanged at +2.90%.

- 13th February: Producers Price Index (“PPI”) for January (wholesale prices) is forecast to increase by 0.30%. The Core PPI is forecast increase by only 0.10%, leaving the annual Core increase at 0.00%. Not a lot of consumer inflation coming from this source.

- 14th February: Retail Sales and Industrial production for January – both forecast to increase by 0.30%.

- 28th February: PCE Inflation for January. The Core PCE measure likely to be +0.20%, well down on the +0.50% increase in January 2024, therefore the annual Core PCE inflation rate reducing from 2.80% to 2.50% - which is the opposite direction in inflation to what the FX markets have been expecting.

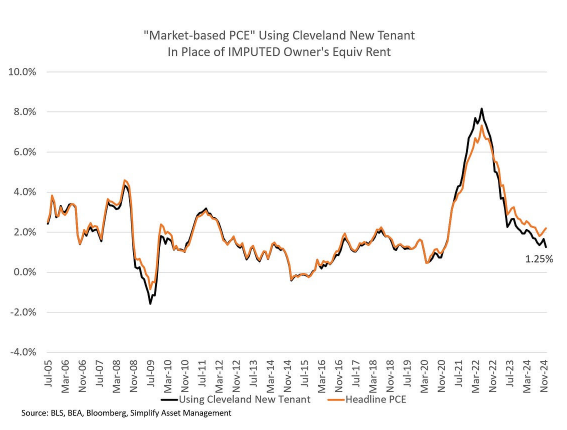

It is far too early for the Trump tariffs on imported product into the US to be pushing up inflation as everyone expects. In the meantime, the continuing lagged reductions in rents (the Shelter component in the CPI Index) will push the inflation rate lower. The chart below plots actual current market rents for houses in the US with the CPI Shelter Index (Imputed Owner’s Equivalent Rent). The CPI Shelter Index has a lot further to fall and it has a dominant 40% weighting in the CPI Index.

It is interesting to observe that both the US Treasury Bond market and the global oil market have not reacted in the same volatile way to Trump’s daily missives as the FX markets have. The US 10-year Treasury Bond yield has drifted lower over this last week from 4.60% to a low of 4.40%, however closing at 4.49% on Friday 7th February. WTI crude oil prices dropping from US$73/barrel to US$71/barrel. Participants in these markets arguably adopting more of a “wait and see” approach as to the economic impact of Trump’s economic policy changes.

After several years of price increases, US households have little tolerance left to pay higher prices on imported goods (from tariffs). The retail stores and business firms know this and therefore do not have the pricing power to implement price increases that they normally would do once per year in January and February. Actual inflation outcomes in the US over coming months are set to surprise the markets as well as the Federal Reserve.

US employment data for January released last Friday night was the proverbial “mixed bag”. Whilst the increase in jobs was much less than forecast at 143,000 (forecast was +170,000 to +200,000), wages increased by more than expected and the unemployment rate reduced from 4.10% to 4.00%.

A voting member of the Fed and renowned “dove”, Austan Goolsbee summed up the situation as follows - “The appearance that inflation process has stalled is largely due to base effects. The view of the economy is full employment, ongoing growth and inflation likely to fall to 2.0%. The first effects of tariffs may be less important than the impact on expectations. We are watching PPIs and listen to industrial contacts to monitor the tariff effect, although the uncertainty makes the environment for the Fed foggier, providing a reason to slow the pace of cuts.”

Hopefully, weaker than forecast economic data will clear some of that “fog” away for the Fed.

The Japanese Yen strengthens against the tide

The Yen weakened alongside all other currencies against the US dollar through January, however over recent weeks the Bank of Japan interest rate hike and higher than expected wage increases (increasing inflation) has turned the tide. The Yen has strengthened from 158.40 in early January to 151.40 today, driving the JPY/NZD cross-rate from 89.00 to 85.70 over the same period. Further gains in the Yen against the USD have to be expected over coming weeks/months as their interest rates will be increased again in May.

The interest rate gap (or spread) between US 10-year Treasury Bonds and Japanese 10-year Bond yields is currently 3.20% (4.49% versus 1.29%). Further falls in US yields to 4.00% and rising Japanese yields to 1.50% should close that gap to 2.50% over coming months. The USD/JPY exchange closely tracks the bond yield differential, pointing to further Yen gains to 140 or 130 against the USD. The Australian dollar and the NZ dollar are closely aligned with the Yen movements against the USD, so it is another reason to support a recovery in both currencies this year from their recent cyclical lows.

The tale of two central banks - implications for the NZD/AUD cross-rate

The Reserve Bak of Australia (“RBA”) next meets on Tuesday 18th February and the Reserve Bank of New Zealand (“RBNZ”) meets the next day on Wednesday 19th February. Whilst the market pricing is for the RBA to cut by 0.25% to 4.10% and the RBNZ to cut by 0.50% to 3.75%, there are alternative permutations/scenarios which would shift the NZD/AUD cross-rate sharply higher and lower: -

Scenario 1: Both cut as expected = NZD/AUD cross-rate remains stable 0.9030.

Scenario 2: RBA do not cut and the RBNZ cut by 0.50% = NZD/AUD rate drops into the 0.8900’s.

Scenario 3: RBA cuts and the RBNZ only cuts by 0.25% = NZD/AUD rate increases to 0.9100.

The lower NZD value driving tradeable inflation back up (opposite of last year) would be one reason why the RBNZ move off their previously indicated 0.50% cut this month. The RBA have the same issue and wages growth/low productivity in Australia is still of concern to them.

The more likely outcome is Scenario 1.

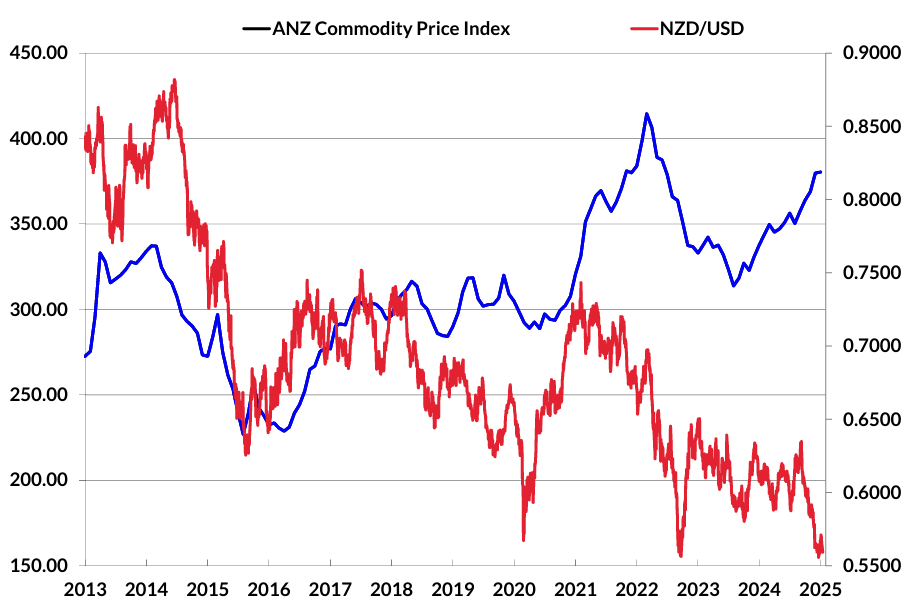

Whilst there is still some doom and gloom around in certain parts of the NZ economy, the outlook for 2025 and 2026 is significantly more positive. It will be interesting to see if the updated RBNZ economic forecasts on 19th February reflect the dramatic improvement in our growth this year from the currently high export commodity prices. Coupled with a low NZD/USD exchange rate (due to the Trump euphoria causing temporary USD strength), the gap between our currency value and our economic fundamentals (export commodity prices) has never been as wide (refer to the chart below).

The 2020/2021 Covid years and the subsequent inflation rise/fall in 2022/2024 have caused an anomaly in the NZ versus US interest rate relationship, which has led to the Kiwi dollar’s value being so misaligned to our commodity prices/economic fundamentals. As interest rates normalise from here, the unanswered question is whether the FX markets and investors return to the previous commodity price determinant?

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.