Summary of key points: -

- Action replay on Trump tariff chaos

- Action replay on US dollar movements

- The Aussies move closer to interest rate cuts

Action replay on Trump tariff chaos

It always pays to add in a proviso when commenting on US President Donald J Trump. In last week’s commentary piece, we suggested that “Trump back-tracks on tariffs - for the meantime…” following his Davos presentation wherein he hinted that he might not impose tariffs on China if they would negotiate to meet some of his other demands.

However, true to his chaotic form, he has now announced 10% import tariffs on China and 25% tariffs on Mexican and Canadian imports into the US, effective immediately. There was not a massive reaction in the FX markets as the US dollar has already been bought up over the last four months in anticipation of such tariffs being implemented. Further tariffs on oil and gas are coming on 18th February, tariffs on micro-chips coming “eventually” and additional tariffs on steel, aluminium and copper are also coming with no timing mentioned. How these announcements reconcile with the stated position of a full “America First Trade Policy” due for release on 1 April is anyone’s guess.

The degree of economic change the tariffs will drive in the US to reduce their trade deficit with these three counties also remains to be seen. The overall US trade deficit did not decrease at all in the 2016 to 2020 period on Trump’s tariff increases. The world is a far different place to the halcyon years of US protected manufacturing in the 1950’s and 1960’s that Trump seems to want to recreate. In many respects, Trump won the November Presidential election race by convincing blue-collar oil industry and auto workers that he would save their jobs by tariffs increasing US manufacturing output. It did not happen last time and will not happen this time.

There has always been a strong argument that Trump uses the threat of tariffs as leverage or a bargaining chip to get other countries to change their ways, particular China and Mexico in respect to drug trafficking and illegal immigration. The question to ask is whether the US will ease off on the tariffs in due course if China and Mexico somehow miraculously stop the flow of drugs into the US?

There will be more to come on tariffs from the Trump regime, the Europeans have yet to be singled out, however rest assured, they will be. Whether these tariff changes will result in retaliatory tariff actions from China, Canada and Mexico remains to be seen. It is clear that China is much better prepared for this 10% tariff than they were in 2017, and therefore the probability of a full-scale trade war between China and the US this time around is somewhat reduced. The negative impact on the New Zealand and Australian economies (and currencies) is also therefore expected to be not as bad as eight years ago.

The Trump regime’s Commerce Minister-elect, Howard Lutnick is convinced that the tariffs will not increase US inflation. He does not have many supporters with that view, and he has produced no evidence to support his claim. However, as we have highlighted previously, toys, clothing, furniture and electronic products imported from China amount to a very small percentage weighting in the US CPI Index. Housing and healthcare prices dominate the weightings in the index and therefore these price changes really determine the level of inflation. There will be an adverse impact on the CPI from the tariffs on steel, aluminium and copper, however it is never a straight cost increase fully transmitted through into selling prices and it may take some time.

The Trump tariff and trade policies are all about returning manufacturing, from automobiles to semiconductors, back to US soil. The tariffs failed to achieve that objective last time, and the chances are that this time will be no different. The majority of commentators view the tariffs as being negative for US economic growth.

Action replay on US dollar movements

The US dollar appreciated from 107.60 on the USD Dixy Index to 108.20 when the tariff announcement hit the newswires on Saturday. The US dollar had depreciated earlier in the day when the PCE inflation measure for the month of December came in bang on prior forecasts at a 0.30% increase. The US dollar has appreciated 7.00% since 101.50 on its index in early October 2024. The FX markets are buying USD’s on the tariff news as the potential for higher US inflation will reduce the number of Federal Reserve interest rate cuts in 2025 and place US interest rates well above those of other currencies (Euro, CAD, GBP, JPY, CNY, AUD and NZD).

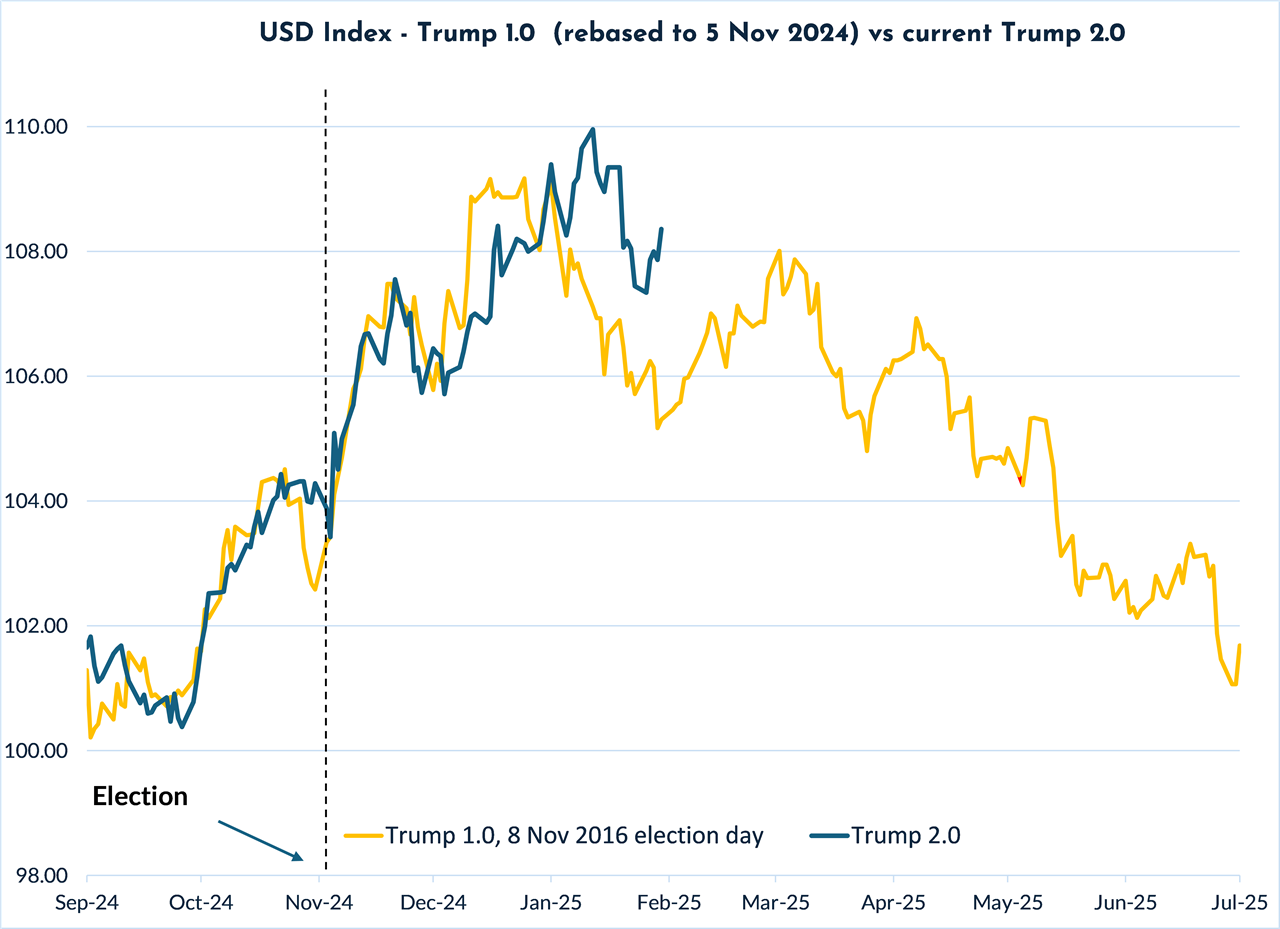

The chart below plots the USD Dixy Index movements since early October 2024 (blue line) under Trump 2.0 against the same period from October 2016 to July 2017 under Trump 1.0 (gold line rebased to November 2024). The mirror pattern is unerringly accurate and scary. The movements in the US dollar repeating exactly the same as eight years previously is a demonstration of currency market psychology and pricing behaviour. The US dollar has been bought up by speculators on the euphoria of the Trump 2.0 regime delivering not only higher inflation, but a stronger US economy and equity markets attracting in foreign capital inflows.

However, if history continues to repeat, the forex markets will soon start to display some displeasure and disappointment that the Trump rhetoric and policy actions are not delivering the actual results of expected higher inflation and superior economic growth. Eight years ago, under Trump 1.0, the USD started to decline some three months after the election and in a bumpy fashion depreciated all the way back to where it started from over the subsequent six months to July 2017. The principal reason for the inevitable USD recoil is that the currency speculators that purchased the USD on the Trump election euphoria eventually have to unwind their positions and take their profits. It is just a question of time. We originally expected that profit-taking to occur before Christmas, however that was thwarted by the Fed doing their pivot in mid-December, reducing four planned 0.25% interest rates cuts in 2025 to just two cuts. There must be a catalyst to cause the speculators to reverse their long-USD positions, to date, we have not had that market event or economic surprise to act as that catalyst. Last week, US GDP growth in the December quarter was weaker than forecast (+2.30% annualised compared to prior consensus forecasts of +2.60%), however that USD negative factor was swamped out by the tariff news.

As is often the case, when markets suddenly change in direction, it is not just one piece of economic data that triggers the change, however a combination of events or economic data releases that push the market pricing over the tipping point. Over this coming week there are a series of US economic data releases that, combined together, could well produce sufficient economic surprises to the downside: -

- ISM Manufacturing PMI for January – new orders and employment likely to be weaker than forecast.

- JOLTS job openings for December – a decrease well below 8 million is expected.

- ISM Services PMI for January – the stronger December number is unlikely to be sustained.

- Non-Farm Payrolls for January – the consensus forecast is an increase of 170,000 jobs and a stable unemployment rate at 4.10%. The final 12-month benchmark revision of monthly jobs data comes out with this report, which will not be positive news for the markets.

US Retail Sales and CPI Inflation data the following week on 13th and 14th February respectively will also be closely watched for indications that the US economy is not as strong as the Fed believe it to be and inflation over the first few months of 2025 will be less than the high monthly increases in 2024 (the annual inflation rate decreasing as a result). Weaker economic growth and lower inflation is not what the FX markets are currently expecting and pricing.

We may be closer to that USD Index tipping point than what most expect if the data is weaker over the next two weeks and Trump focuses on matters other than tariffs.

If history does repeat over the next six months and the USD Index depreciates back to 101.50, the Kiwi dollar will be pushing 0.6350 again. The probability of the NZD/USD exchange rate going to the other way and testing the 0.5550 lows again is arguably reduced, as the USD has already appreciated on the expectation of tariffs and now, they have been delivered, you get an element of the “buy the rumour, sell the fact” market syndrome.

The Aussies move closer to interest rate cuts

Australian interest rate market pricing has moved to an 80% chance that the Reserve Bank of Australia (“RBA”) will cut their OCR by 0.25% to 4.10% on 18th February following the December 2024 quarter’s CPI inflation report last week. However, it is by no means a 'lay down misère' (Australian gambling slang for a predicted easy victory) that the RBA will deliver precisely to the market’s confident expectations. Whilst the December quarter increase in inflation of 0.20% was well below the prior forecasts of a 0.50% increase, the “trimmed-mean” CPI measure the RBA prefer, only marginally declined to 3.20% annual rate - well above the 2.50% target.

The direction of Australian inflation over the second half of 2024 was certainly downwards, however identical to New Zealand, the tradable inflation component will not be decreasing in 2025 like it was last year, as the lower currency values increase imported costs/prices. The RBA will be conscious of this factor, as well as the still strong labour market keeping wage increases elevated. Unfortunately, the next wages and employment data comes out the two days after the RBA meeting on 18th February. A consumer inflation expectations survey on 14th February will provide important insights for the RBA ahead of their meeting. The Fed have paused on interest rate cuts due to the inflationary impact of Trump’s tariffs; the RBA may adopt the same cautionary stance until they see where the markets go and the Aussie dollar lands.

It would be a major surprise if the RBA did not cut rates on 18th February. Further AUD selling based on a rate cut seems unlikely as it is already “priced-in”. However, we would see strong AUD gains if the RBA held fire and caught the markets wrong-footed. The Australian “neutral” interest rate is somewhere between 3.00% and 4.00%, therefore Australian interest rates do not have much room to fall in 2025. Federal Government and State Government fiscal spending is the major source of inflation and uncertainty in Australia and that does not appear to have slowed down under the Albanese Labour regime. RBA Governor, Michelle Bullock does not seem to be a monetary policy manager that will bow to political pressure to cut interest rates just because there is a general election coming up in May.

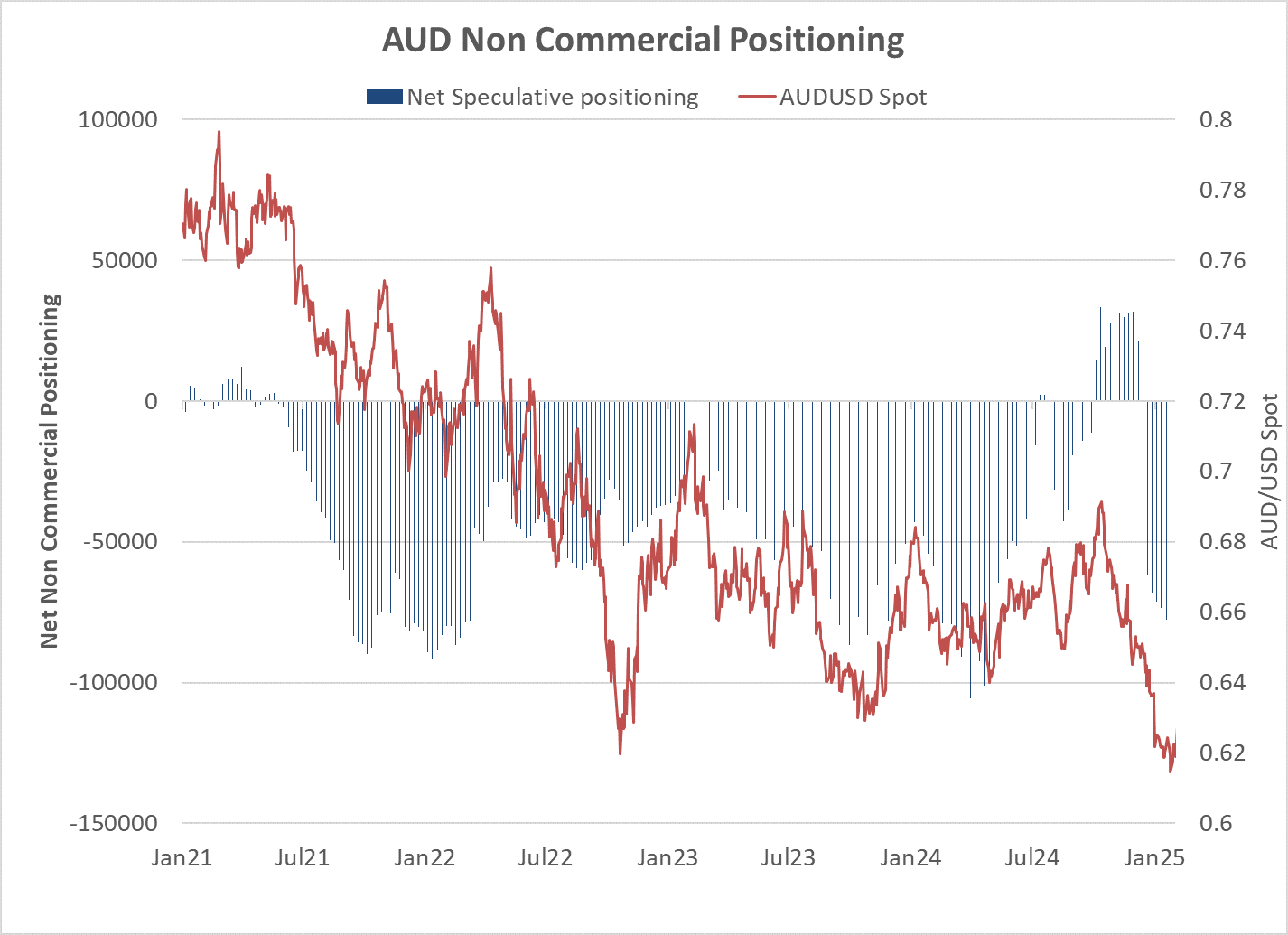

The currency speculators are heavily “short-sold the AUD” again, the overall USD direction and the RBA decision on the 18th will determine whether they maintain their positions or unwind (by buying the AUD).

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.