Summary of key points: -

- The peaks and valleys of the Kiwi dollar movements since free-floating in 1985

- Fed messaging this week to dictate early 2025 US dollar direction

- Two timely local reports endorse the growing optimism for an export-led recovery

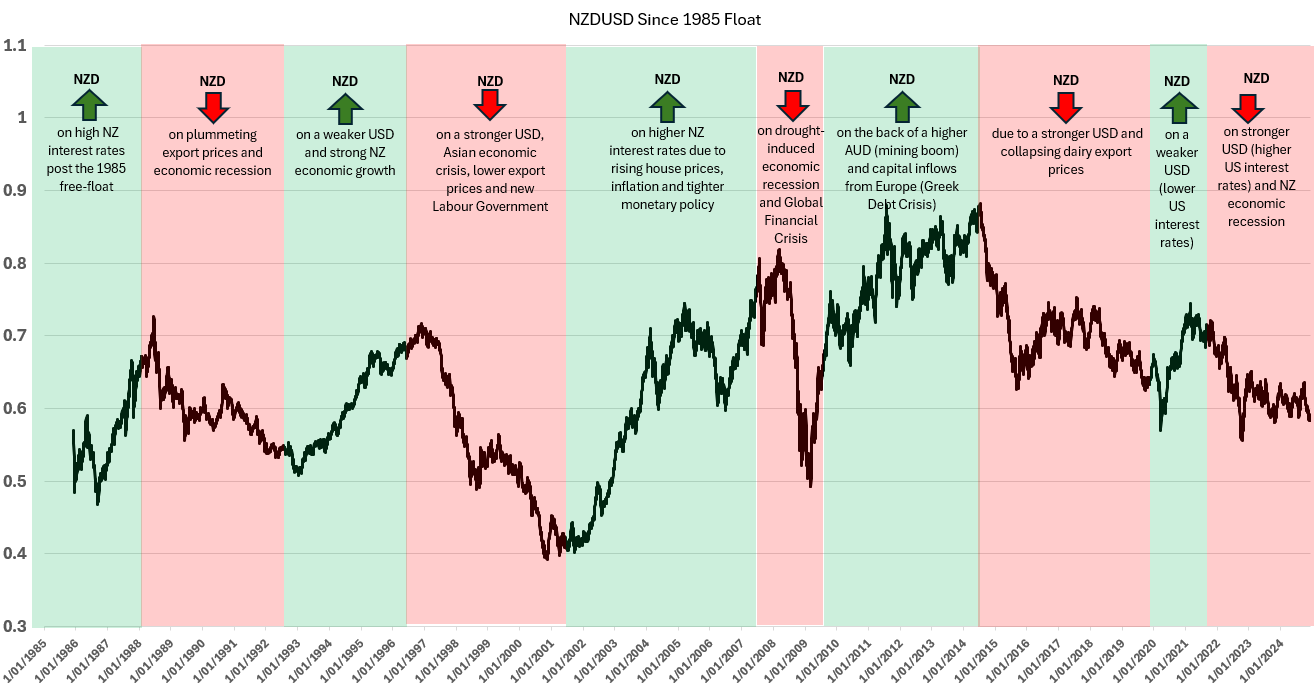

The peaks and valleys of the Kiwi dollar movements since free-floating in 1985

To wrap up the year it is timely to take a look back on some poignant currency history…

In early March next year, it will be 40 years since the Kiwi dollar was free floated on the foreign exchange markets following a 20% devaluation of the currency in the aftermath of the late 1984 general election. At the time, in March 1985, I was a young Foreign Exchange Manager for the merchant bank, NZI Securities. The foreign exchange market was the only industry sector that the then Prime Minister, the late Sir Robert Muldoon, ever deregulated. He issued official licenses to the several merchant banks to deal in foreign exchange on an equal footing to break down the cozy cartel the big four banks were keen to retain.

On a rainy Sunday afternoon in March 1985, we were all called at short-notice to a meeting at the Reserve Bank of New Zealand in Wellington to be told the Kiwi dollar was to be free floated the next day. Floating the currency was all part of deregulation and unshackling of the New Zealand economy under the revolutionary free-market reforms of Labour Government Finance Minister, Sir Roger Douglas. I recall leaving the meeting thinking that did not know a lot about foreign exchange markets, however I was surprised to observe that I probably knew a bit more than the guys and gals at the Reserve Bank…

It has been a rollercoaster ride for the New Zealand dollar ever since. It one point a number of years ago, the Kiwi dollar was the 10th largest traded currency on daily volumes in the world. An extraordinary statistic for an economy ranked 46th in the world (with annual GDP of US$250 billion). The chart below is a potted history of the five distinct periods of appreciation and five periods of deprecation over the 40 years. In March 1985, everyone thought the Kiwi would fall like a stone on being allowed to free-float on market supply and demand, it went up!

The factors that have caused the numerous peaks and troughs in the NZD/USD exchange rate over the last 40 years are summarised as follows: -

- Changes in value in the US dollar against all currencies on the world stage.

- Interest rate changes and differentials.

- Commodity price movements (impacting the NZ and Australian economies).

- Global economic shocks (Asian financial crisis, GFC and the Covid pandemic).

The NZ dollar has been on a broad depreciating trend for the last three and half years from a high of 0.7270 in May 2021. The four previous periods of deprecation since March 1985 had an average duration of four years. If the US dollar depreciates on lower US interest rates in 2025, the Kiwi dollar appears well poised to end its weaker/lower trend and commence a multi-year uptrend on higher commodity prices and relatively superior GDP growth performance.

The unanswered question, of course, is whether US interest rates will decrease throughout 2025 and cause the USD to depreciate.

Fed messaging this week to dictate early 2025 US dollar direction

Do not expect any surprises in the US Federal Reserve’s interest rate decision and statement this coming Thursday morning at 7am (NZT). They will cut interest rates by another 0.25% and predictably state that the speed and extent of further interest rates cuts next year will be ”dependent on the evolving economic data”. In other words, the Fed will continue to look backwards at historical economic results with employment and inflation to frame their decisions. However, the pressure will come on to Chair Jerome Powell in the Q and A media conference commencing at 7.30am. The financial media will want to know how the Fed are factoring into their forward-looking economic projections the Trump regime’s deregulation, tariffs, tax cuts and illegal worker deportation policies to be implemented in 2025. In response to the questions, Chair Powell will be expected to play a non-committal, straight bat in that everyone will have to wait and see how the policies are to be applied and what impact they will have on the US economy, employment and inflation. The Fed will continue to not look forward at forecasted economic conditions, therefore the markets are well ahead of themselves in pushing US bond yields higher and the USD higher on the expectation that the Fed will slow down their interest rate cutting cycle.

Whether the Fed continue to make 0.25% cuts the Fed Funds interest rates at every meeting over the first three to four months of 2025 will be totally reliant on monthly inflation and employment prints. What we do know, is that Government sector jobs in the US have made the largest contribution to job increases over the last two years of the Bidonomics spending programmes. President Trump has vowed to reduce the Washington bureaucracy and abolish state institutions that do not do anything. Sounds very much like large-scale layoffs in Government sector jobs, which will add to the weaker employment trends over the second half of 2024.

The annual CPI inflation rate will decrease sharply from the current 2.70% over the next three to four months as expected 0.20% price increase each month replace 0.40% monthly increases 12 months ago. The continuing reductions in the lagged Shelter CPI (housing rents) over the first half of 2025 will be a dominant influence over upcoming US inflation data and will likely surprise current market expectations of the annual inflation rate rising above 3.00% again due to Trump’s tariffs. Instead, the annual rate of inflation is expected to trend well below 2.00%.

US 10-year Treasury Bond yields have reversed sharply back upwards again to 4.40% over recent days as traders/investors fret about the Fed statement this week. The USD Dixy Index has climbed back to 106.70 from lows of 105.50 earlier last week. US economic data being released ahead of the Fed’s 18th December decision is Retail Sales (+0.50% forecast) and Industrial Production (-0.10% forecast).

Expect Jerome Powell to state that it is far too early for the Fed to be adjusting their current planned monetary easing cycle due to Trump policy changes. There is still time for the “Trump Trades” to be unwound before the end of the year, allowing some recovery in the Kiwi dollar from its vulnerable 0.5765 position.

Two timely local reports endorse the growing optimism for an export-led recovery

The local interest rate market and FX market will be firmly focused on the barrage of local economic data coming at them in the last week before Christmas.

- Tuesday 17th December: NZ Government half year economic and fiscal update.

- Wednesday 18th December: Balance of Payments Current Account, September quarter.

- Thursday 19th December: GDP Growth rate for the September quarter.

The news will be “the glass half empty” for most with large dual deficits continuing and economic growth contracting by 0.30% or 0.40% in the months of July, August and September 2024. Given the timing of the releases, do not expect any great reaction by the FX markets to the data.

For those who see New Zealand’s immediate economic prospects in 2025 as being more on “the glass half full” side, two reports released last provide increased optimism that an export-led economic recovery to positive 2.00% overall GDP growth in 2025 is highly likely.

- The Ministry of Primary Industries SOPI report (“Situation and Outlook for Primary Industries”) painted a very positive picture of food and fibre sector exports bouncing back by +7.00% to NZ$57 billion for the year to June 2025. Higher prices and increased production will increase dairy exports by 10% to NZ$25.5 billion over the same period. Forestry export revenue is forecast to rebound as well, by +4.00% to NZ$6 billion. The rapidly growing horticulture sector is forecast to increase by a whopping 12% to NZ$8 billion.

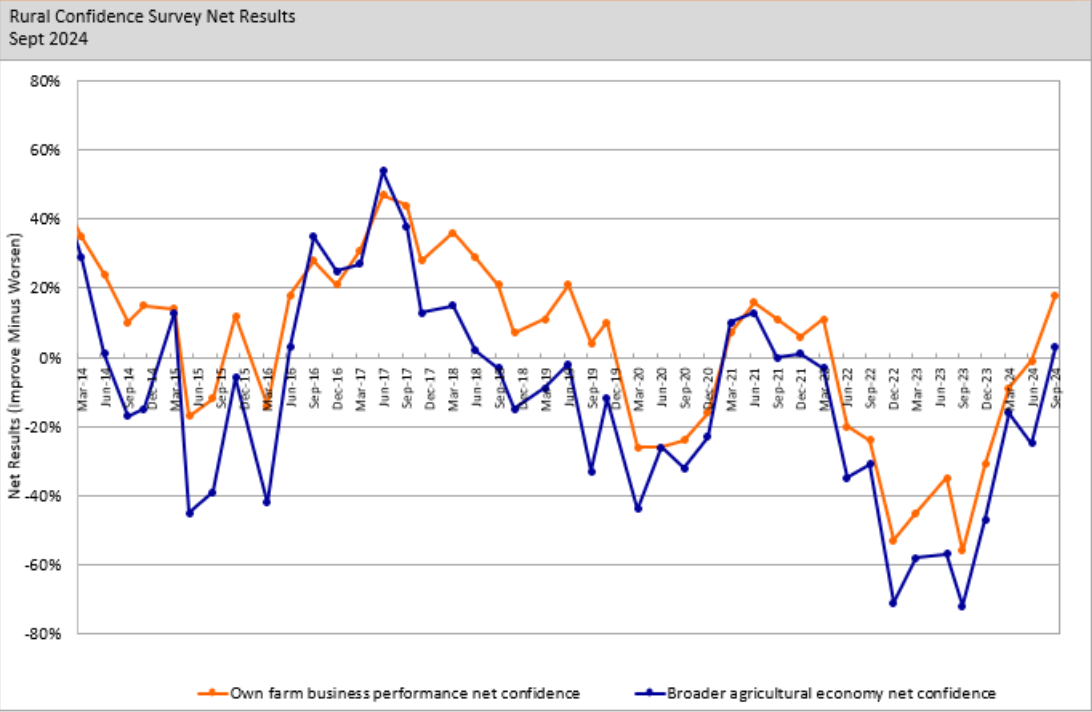

- The Rabobank Rural Confidence Survey for the already historical September quarter climbed to the highest level for “Own farm business performance net confidence” since December 2021. Further increases in dairy, beef and sheep meat prices over more recent months suggest confidence levels will return to the highs of 2017/2018. What all this means, is that farmers will be spending and investing aggressively again for the first time in many years.

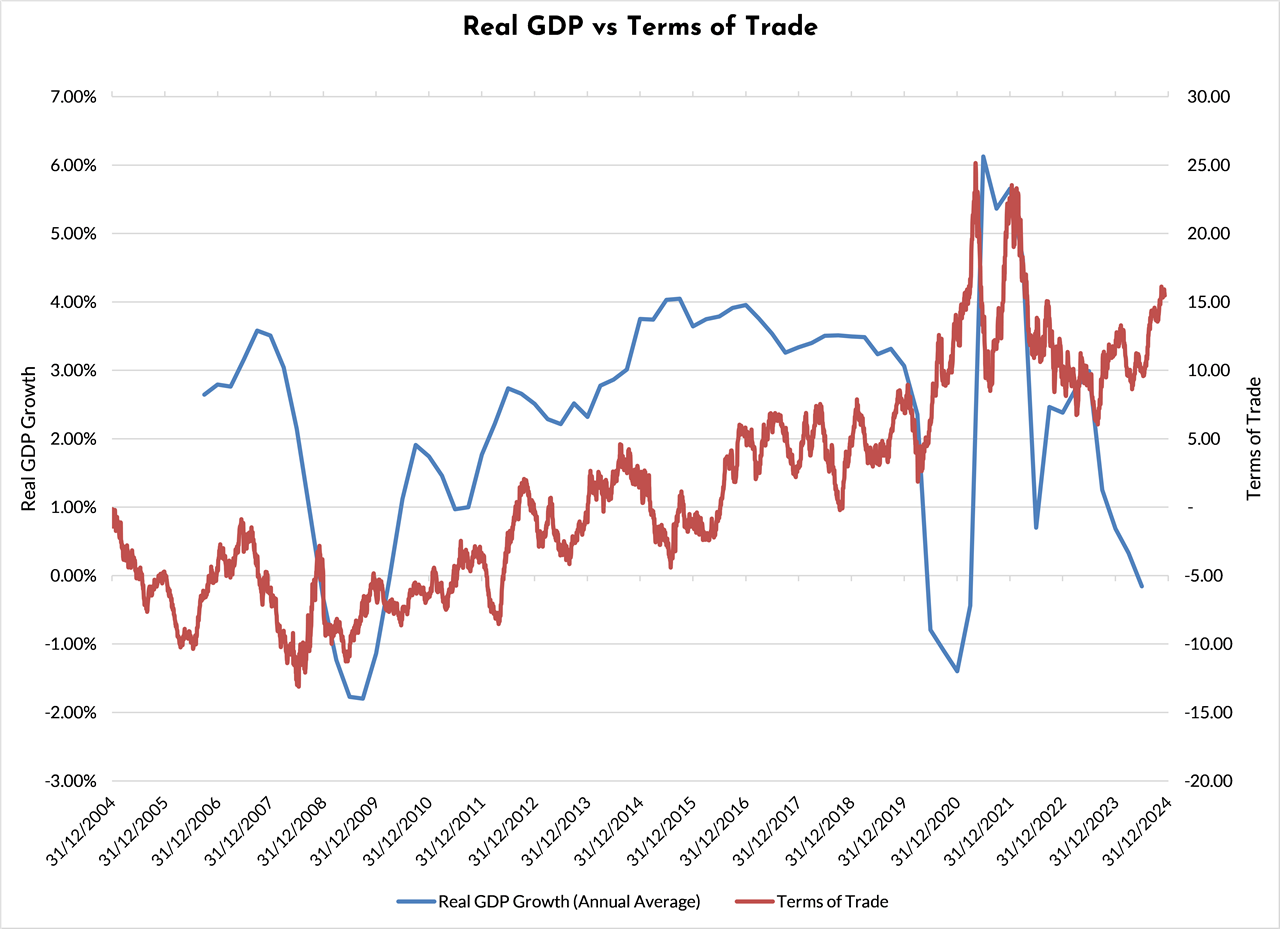

As global interest rate normalise in 2025 to pre-Covid levels of New Zealand rates being above those of Australia and Australia being above the US interest rates, we may well see the FX markets returning to assessing underlying economic fundamentals again as a key determinant of an exchange rate direction. New Zealand’s outlook is very positive with the Chinese likely to stimulate retail/consumer spending in their economy to achieve their required +5.00% GDP growth rate. High commodity prices have always driven New Zealand’s economic growth performance, as the chart below of our Terms of Trade Index against GDP growth confirms.

Wishing our readers a Merry Christmas and Prosperous New Year

Next column will be Monday 6th of January 2025

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.