Summary of key points: -

- The Bank of Japan succeed in the art of currency market intervention

- Will the Fed cut interest rates by 0.50% or 0.25% this week?

The Bank of Japan succeed in the art of currency market intervention

The major development and influence on global foreign exchange markets continues to be the extraordinary reversal in fortunes for the Japanese Yen.

The Yen appreciated against the US dollar to below 141.00 on Friday 13th September, as the markets expect the interest rate gap between the US and Japan (that caused the previous Yen weakness) to continue to close up through decreases in US interest rates and increases in Japanese interest rates. The Yen has already appreciated 13% against the USD since it hit a 37-year low of 162.00 in early July. Further gains in the Japanese Yen over coming months have to be expected.

It was thought by the economic experts that direct intervention by central banks in currency markets to defend, halt or change the direction of a currency did not work anymore as the global foreign exchange markets were far too big and powerful to allow that to happen. The Bank of Japan intervened heavily in the FX markets in July to buy Yen, sell USD. Looking back, it has been a very successful execution of the art of intervention. They caught the markets heavily oversold Yen in “carry-trades”, forced those speculators to reverse their positions as “stop-loss” FX orders placed in the markets were triggered and caused a spectacular reversal in the Yen’s direction. Adding to the dramatic change in sentiment was the clear signal from the Bank of Japan that they would be increasing their interest rates to combat their high inflation. They have so far hiked their short-term interest rates to 0.25%. However, last Thursday a Bank of Japan Board member, Tamura Naoki signalled that the central bank should raise its interest rates to “at least 1.00% in stages for price stability”. Whilst the Bank of Japan was very slow and seemingly reluctant to lift their interest rates earlier in the year (after 0.00% rates for 17 years), these latest statements are the clearest and most specific so far.

The Bank of Japan next meet to discuss interest rates on Friday 20th September, two days after the US Federal Reserve (“Fed”) FOMC meeting on 18th September (6am Thursday 19th September NZT). The Japanese have their inflation data for the month of August on Friday 20th as well, wherein the annual rate of inflation is forecast to increase from 2.80% to 3.00%. Japan is experiencing the same “wage-push” inflation that New Zealand suffered from two years ago. The Bank of Japan is not expected to lift the current 0.25% interest rate at this meeting; however, the messaging will be clear that there are increases in the pipeline.

In stark contrast, the Fed will either be cutting their Fed Funds interest rate by 0.25% or 0.50%, the first cut since March 2020. The bond market in the US has already been anticipating significant Fed cuts over the course of the next 12 months. The benchmark 10-year bond yield has decreased from 4.70% in April to currently trade at 3.65%. The new “neutral interest rate” for the US, where monetary settings allow for non-inflationary economic growth, is considered to be somewhere between 2.50% and 3.00%. If US inflation is stable at 2.00%, then the 10-year bond yields seemingly still have plenty of room to reduce a whole lot further to at least 3.00%. However, inflation, neutral interest rates and “real” interest rates (nominal interest rates less inflation) are not the only factor determining the level of 10-year bond yields. Demand and supply of bonds are probably more important. In that respect, the continuous ballooning of the US Federal budget deficit requires a truckload of bonds to be issued to fund the shortfall. If investor demand to buy bonds does not meet those massive volumes of supply, the bond yield moves higher.

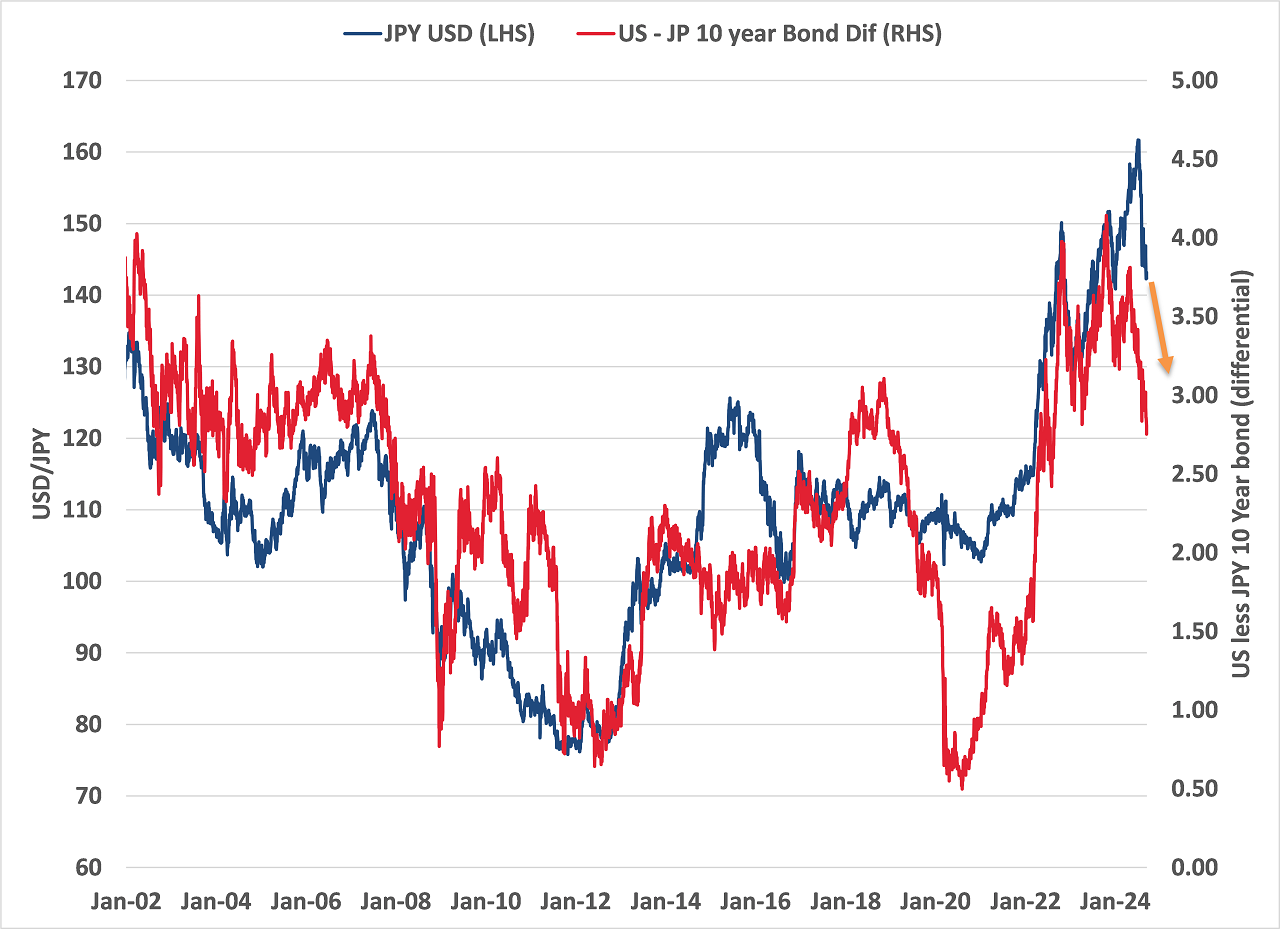

The Japanese 10-year bond yield is currently 0.85%, 2.80% below the US yield at 3.65%. The Japanese bond yield has retreated in recent weeks from the highs of 1.06% in early July. The chart below plots the differential in US and Japanese bond yields against the USD/JPY exchange rate. The close correlation is caused by Japanese investment houses switching their funds into US bonds when the yield differential is high. In doing so, they sell the Yen, buy USD’s causing the USD/JPY exchange rate to track the bond differential. Just a few short months ago, the bond differential (red line on chart) was 4.00% and the Yen was very weak at 162.00. The bond differential has collapsed to 2.80% and the USD/JPY has followed to some extent. The historical correlation would suggest the Japanese Yen still has a lot further to appreciate towards 130.00 and even lower as the bond differential heads to 2.50% through higher Japanese yields and lower US yields.

The implications for the NZ dollar of a 130.00 or 120.00 Yen exchange rate to the USD are obvious.

Will the Fed cut interest rates by 0.50% or 0.25% this week?

Following CPI inflation and PPI wholesale price data in the US economy last week, the interest rate market forward pricing for a 0.50% cut reduced to a 15% probability. However, that changed back to a 49% probability by Friday 13th September following two influential media articles in the Financial Times and Wall Street Journal, both suggesting that a 0.50% cut was justified on the grounds of a sharp deterioration in employment in the US economy over recent months. In addition to the media commentary, former Fed New York member Bill Dudley said there was a “strong case” for a half-percentage point cut this week, emphasising the restrictive impact on economic growth of the current rate of 5.50%. Whilst some may see a 0.50% first cut as signalling a “panic” decision by the Fed, it would serve as a plausible pre-emptive measure if Fed officials feel the economy is slowing too quickly. It may well prove to be the “path of least regrets”. Where have we heard that before?

The Fed can have total confidence that they have achieved the annual inflation target of 2.00%. When the PCE inflation data for August is released on Friday 27th September, the high 0.40% increase in September 2023 drops out of the annual calculation, being replaced by +0.10% or +0.20% for August 2024, which will reduce the annual increase from 2.50% to 2.20%. The PCE annual increase to the end of September (released late October) will reduce again to 2.00% for the same reason. Job done on inflation; however, the other part of the Fed’s dual remit is jobs themselves.

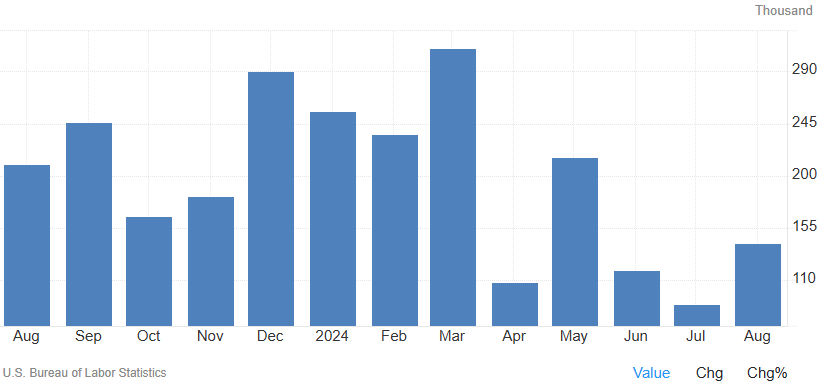

Last month, Fed Chair Jerome Powell stated that the Fed would “do everything we can to support a strong labour market as we make further progress towards price stability”. A few months back he also stated that should the labour market deteriorate at a much faster pace than what the Fed were forecasting, they would not hesitate to cut interest rates more aggressively to fulfil that side of their mandate (full employment). The bar chart below of monthly Non-Farm Payrolls jobs increases certainly confirms a sharp slowdown since March. It is said that the US economy needs to increase jobs by 200,000 every month just to standstill due to the natural population increase. Recent months have been much lower than this, adding support for a 0.50% cut.

The FX markets have been positioning for a 0.25% up until now. Should a 0.50% cut eventuate this week, the US Dollar Dixy Index currently at 101.12 would likely fall away to below 100.00.

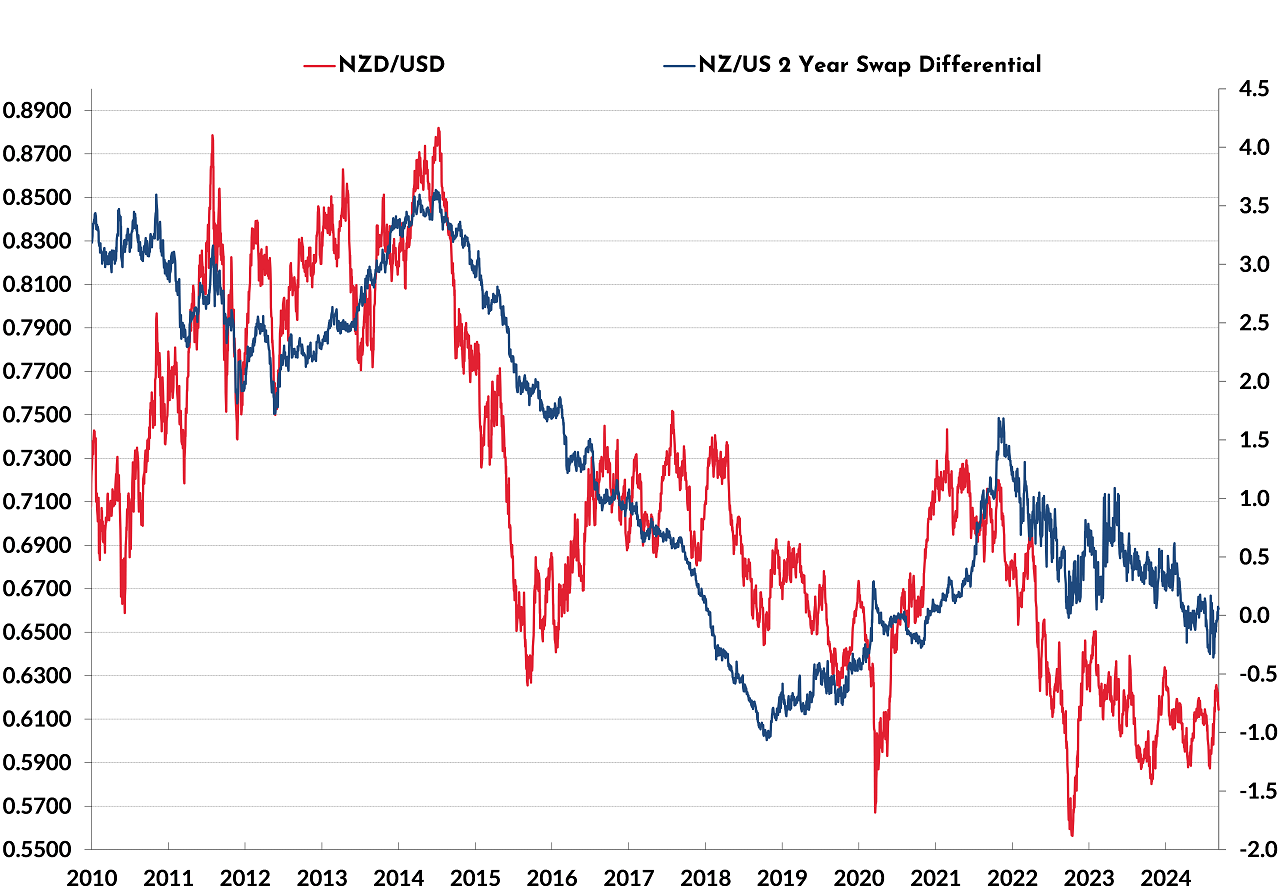

US two-year swap interest rates are currently trading at 3.67%, very close to New Zealand two-year swaps rates at 3.69%. The differential is zero. The question for future NZD/USD exchange rate direction (based on interest rate differentials as a key driver) is whether NZ two-year market interest rates move lower from here, following the US interest rates lower over coming months. One argument for NZ rates not moving a great deal lower is that the local interest rates markets have already priced-in far too much in respect to RBNZ OCR cuts over coming months. The mid-October CPI inflation result for the September quarter may hold the answer to these questions. A quarterly increase significantly above the +0.80% forecast by the RBNZ would send two-year interest rates higher. It looks certain that US two-year interest rates will reduce further towards 3.00% over coming months, there is much less certainty that NZ two-year interest rates will do the same. The net result is that there is a greater probability that the current 0% interest rate differential will move upwards to NZ rates trading up to 0.50% above those of the US. The differential increasing (blue line on the chart below) would be a reversal of the trend of the differential reducing over the last two years.

Changing interest rate differentials between Japan, the US and New Zealand all point to a higher NZD/USD exchange rate over coming months. The Reserve Bank of Australia (“RBA”) sticking to their guns and not cutting their interest rates until early 2025 is also supportive of a higher AUD against the USD (hence a higher NZD against the USD). The risk to the view of a higher AUD (based on the US cutting and the RBA not cutting) is that iron ore prices fall below US$90/tonne due to weaker Chinese demand. Iron ore prices falling away to US$80/tonne would prevent AUD gains. Over recent days the iron ore prices have stabilised at around US$92/tonne.

What may well prevent further decreases in iron ore prices is potential Chinese announcements of fiscal or monetary stimulus to their flagging economy. The Chinese +5.00% GDP growth target for 2024 is under serious threat of not being achieved as recent economic data has been on the weaker side. Production, consumption and investment data has been a lot cooler of late, many stating that the 5% growth target is impossible to achieve without a “bazooka” stimulus package. Watch this space!

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.