Summary of key points: -

- Fed likely to cut rates more aggressively if US employment continues to weaken

- Second wave of USD depreciation likely to be driven by funds repatriation

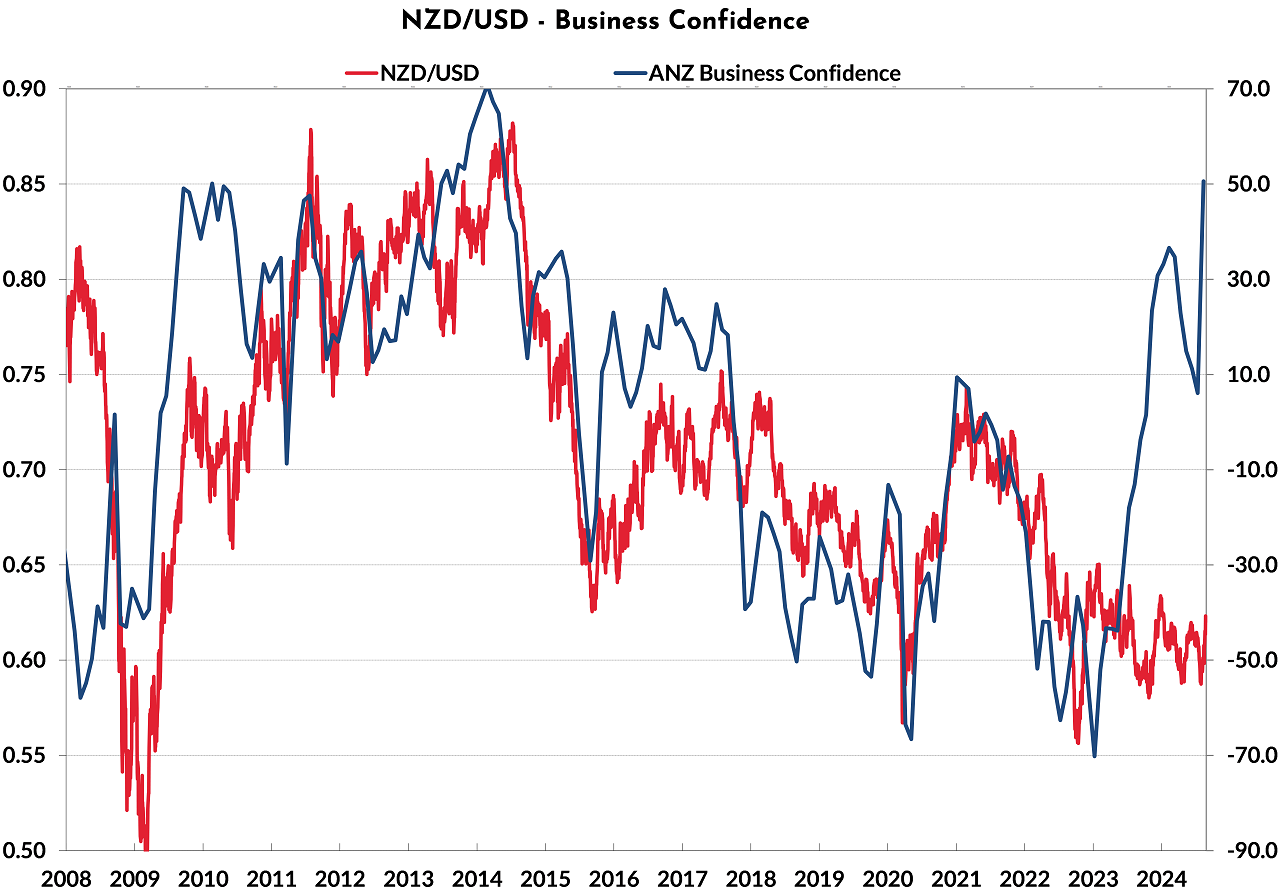

- Stunning leap in NZ business confidence

Fed likely to cut rates more aggressively if US employment continues to weaken

The Kiwi dollar posted impressive gains against a weakening US dollar over the month of August, appreciating four cents from 0.5900 to a high of 0.6300.

All but the last half cent push up from 0.6250 to 0.6300 was due to a slumping US dollar value as the FX markets price-in widely anticipated significant and constant US interest rate reductions over the next 12 months. The Kiwi dollar found some buyers on its own account on Thursday 29th August when the monthly ANZ Business Confidence/Outlook Index jumped up from 27.1 in July to a 10-year high of 50.6 in August. The RBNZ cutting of the OCR interest rate during the month clearly lifting the spirits for better times ahead. However, there was no immediate follow-through buying of the NZ currency and the NZD/USD rate has returned to 0.6250 as the US dollar gained some traction on month-end book-squaring by traders and investors.

The four-cent appreciation of the Kiwi dollar over a few short weeks once again demonstrates the absolutely dominant influence over NZD/USD movements rate from the US dollar side of the currency pair. The long-held thematic of this foreign exchange commentary column is that the USD direction will determine the NZD/USD exchange rate levels and that local NZ economic changes, or performance levels really do not come into the currency equation too much. The last four weeks of sharp Kiwi dollar gains is convincing evidence of why the FX market analysis, insights and contemplating what is ahead is concentrated on the US economy, US interest rates and what that means of the US dollar currency value.

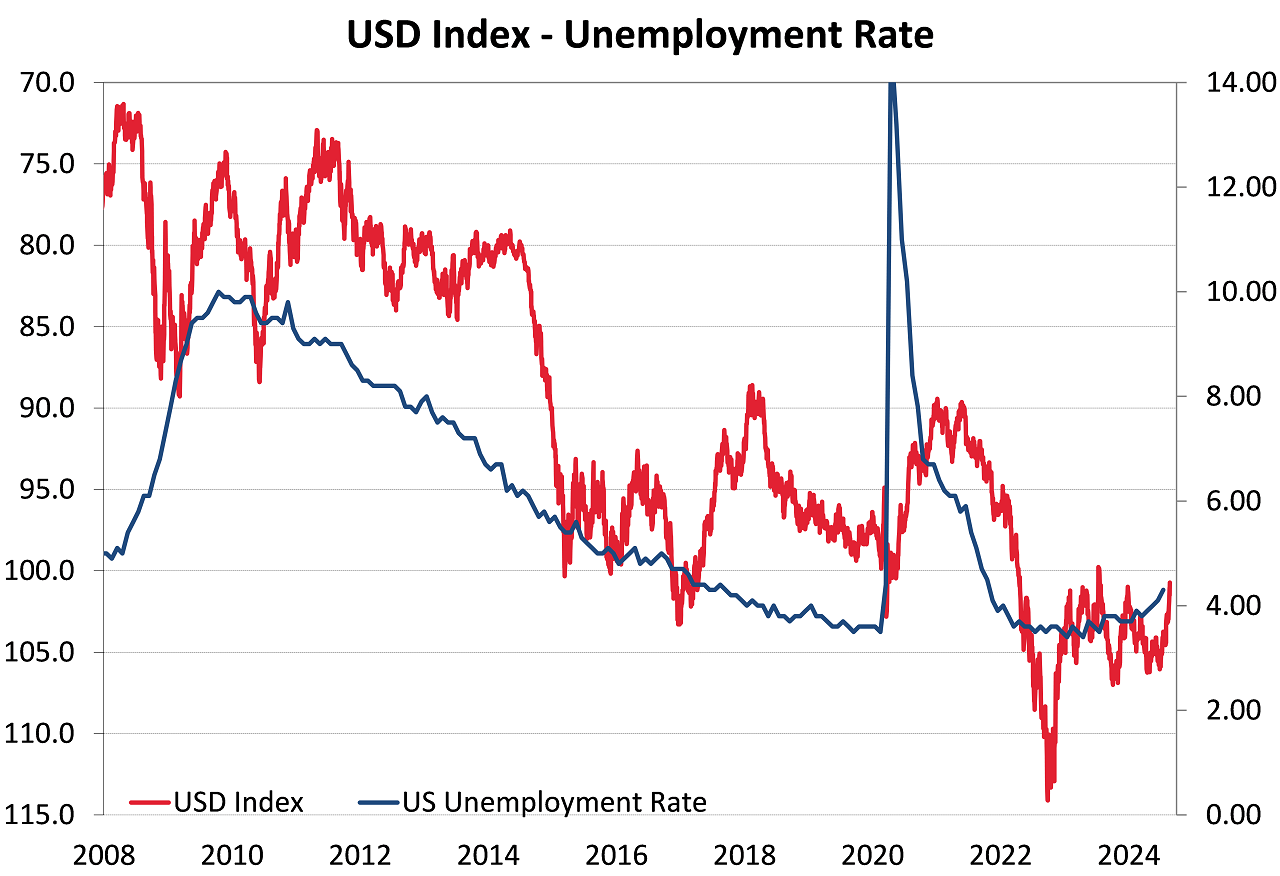

The connection between US inflation outcomes, US labour market statistics, the Fed’s monetary policy position and US interest rate market pricing has been the prime determinant of US dollar direction over the last 12 months. There have been several false starts to the strongly held view that softer US inflation and jobs data will drive US interest rates and the US dollar lower. Distorting the inflation and economic picture has been the ridiculously lagged housing cost/rents (Shelter CPI) measures and Non-Farm Payrolls data that has been subsequently and inexcusably revised down by 800,000 over the 12 months period to 31 March 2024. There is no question that up-to-date and accurate economic measures of rents and jobs in the US economy would have resulted in the Fed cutting interest rates many months earlier than their first 0.25% cut on the 18th of this month. A better understanding by Fed members that US companies always increase their prices once per year in January and February, leaving minimal changes in the other 10 months of the year, would have resulted in much earlier confidence that annual inflation would reach the Fed target of 2.00% in this third quarter. Nevertheless, the US dollar is now under substantial selling pressure as the rise in inflation, interest rates and the US dollar in 2022 is reversed completely in 2024.

After depreciating to a 30-month low of 100.46 on Wednesday 28th 2024, the USD Dixy Index had recovered some ground to 101.66 by Friday 30th August on the back of US annual GDP growth (second estimate) coming in at +3.00%, above the prior forecast of +2.80%. PCE inflation for July was an increase of 0.20% as forecast. Interest rate market pricing for a 0.50% cut on the 18th of September has reduced substantially, contributing to the short-term USD correction upwards.

The US dollar is expected to be under renewed selling pressure over this coming week if US ISM manufacturing/services data prints on the softer side and the Non-Farm Payrolls jobs numbers (Friday night 6th September) are below the consensus forecast of +163,000 for the month of August.

Economic forecasters are not expecting an increase in the US unemployment rate in August from its current level of 4.30%. However, the household survey of employment which produces the official unemployment rate has been weaker than the Non-Farm Payrolls (survey of employers) data for most of this year. Therefore, a tick-up in the unemployment rate to say 4.40% would be particular concern to the Federal Reserve as they observe employment conditions weakening at a more rapid pace. The Fed will cut interest rates more aggressively and earlier if the unemployment rate moves higher than that what they have been forecasting. The US dollar would be under a massive second wave of selling to 95.00 on the Dixy Index should this potential scenario transpire into reality.

Excluding the gyrations of the 2020/2021 Covid years, the US dollar has broadly strengthened on positive US economic growth producing a lower unemployment rate. A rise in the unemployment rate towards 5.00% over the coming 12 months would point to the USD returning to its previous trading range above and below 95.00 on the USD Dixy Index.

Second wave of USD depreciation likely to be driven by funds repatriation

When the US Federal Reserve increased their interest rates to 5.50% in July 2023 they created a massive incentive for investors, traders and companies all around the global to hold excess cash reserves in US dollars. The interest rate yield return was higher than home currencies and the US dollar was likely to appreciate against all currencies as well, delivering double whammy return incentive. The USD Dixy Index appreciated from 95.00 to 114.00 as a result of capital flows into the USD.

We now stand on the cusp of that whole series of events completely reversing i.e. the USD depreciating, as all the capital flows the other way back home. To date, the USD sell-off of the last two months from 106.00 on the Dixy Index to 101.00 appears to be related to hedge funds and currency speculators unwinding their long-USD positions.

The second wave of USD selling is expected to come from an entirely different cohort i.e. physical cash piles parked in USD for the last 12 to 18 months converted back to home currencies.

One London-based fund manager specialising in Emerging Markets, Eurizon SLJ Asset Management, estimates Chinese companies may be enticed to sell a USD1 trillion pile of USD denominated assets as the US cut their interest rates. They see an “avalanche” of these repatriation flows of money which would cause a 10% appreciation of the Yuan exchange rate. We have already witnessed outsized movements in the Japanese Yen due to the closing up of the interest rate differential (Japan up, US down), these analysts are seeing a similar carry-trade unwind strengthening the Chinese Yuan. Macquarie Bank estimates that Chinese exporters and multi-national companies have amassed US$500 billion in USD holdings since 2022.

There is mounting evidence that these investors and companies who have done so well out of holding USD’s over recent time, will take the opportunity to crystallise their FX gains and shift the funds home.

Stunning leap in NZ business confidence

The cynics amongst us have long held the view that business confidence in New Zealand moves up and down based on whether the Chief Executive of the company being surveyed believes his/her own residential property value is moving higher or lower!

There is no doubt that the RBNZ’s early cut of interest rates has buoyed confidence and expectations about investment, the economy and personal asset values. However, there is arguably much more to the lift in sentiment than just interest rate changes. It should always be remembered that a good proportion of our population have investments in bank deposits, resulting in their income going downwards when interest rates decrease.

An economic downturn does force many businesses to seriously look at their costs, efficiencies and ways of doing things. When the upturn in demand subsequently comes, they are well positioned to increase profitability, and with that lift investment and expansion. The leap in confidence also reflects growing expectations of an export-led economic recovery next year, led by rising dairy prices. Business confidence does not drive the NZD value, however the chart below is spectacular!

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.