Summary of key points: -

- Massive unwinding of Yen carry-trades hits the antipodean currencies

- Fed set to signal first interest rate cut

- Australian CPI inflation outcome crucial pointer for the RBA

Massive unwinding of Yen carry-trades hits the antipodean currencies

In has been a good number of years since the Japanese Yen has held centre stage in global foreign exchange markets, however, over recent weeks the unwinding of Japanese Yen “carry-trades” has swiped the NZD and AUD sharply lower.

The 0% interest rate policy Japan has adopted over the last 20 years has incentivised large scale currency carry-trades over the last three years when US, Australian and NZ interest rates all increased to combat the high inflation problem. Hedge funds and currency investors around the world essentially borrowing Yen at 0% interest cost and investing in the three higher-yielding currencies at 5.50% (or 4.35% in Australia’s case). The interest income is attractive from the trade without any favourable currency movement over the period of the borrow and deposit. If sufficient volumes of carry-trades are transacted, selling the Yen to buy USD (or NZD and AUD as well), the Yen will depreciate. And that is exactly what has happened over the last three years, the Japanese Yen depreciating 47% against the US dollar from 110.00 in July 2021 to a high of 162.00 two weeks ago.

Without any form of prior warning, the Japanese Yen has dramatically reversed direction against the US dollar over the last two weeks, appreciating from 162.00 to a low of 152.00 on Thursday 25th July. Many currency investors sitting in the Yen carry-trades have suddenly decided to unwind their positions and have bought Yen, sold USD, causing the Yen appreciation to 152.00. The unwinding of sold Yen/bought NZD and sold Yen/bought AUD carry-trades has caused the 2.5 cent sell-off in the NZD/USD exchange rate from 0.6130 on 10th July to 0.5880 at the close on Friday 26th July.

Surprisingly, it has not been any decisions by the Bank of Japan on currency market intervention or interest rate changes that has sparked the sudden Yen appreciation. It has more to do with the US dollar itself and the recent lower inflation outcomes in the US increasing the market pricing for three interest rate cuts by the Fed this year and therefore the expectation of a lower US dollar that goes with that.

Unfortunately, at a time when both the RBNZ and the RBA need higher currency values to reduce tradable inflation (to offset the sticky/high non-tradable domestic inflation in both countries), the antipodean currencies, in the short-term, have been caught up in the sidewash of the Yen carry-trade unwinding. It does seem that the unwinding may now have run its course, so the expectation is that the NZD and AUD should stabilise and reverse back upwards over coming weeks.

The chart below shows how the general Japanese Yen weakness over the last three years against the USD (due to the Bank of Japan 0% monetary policy settings) has also weighed down other Asian currencies such as the Chinese Yuan (red line), the Thai Baht (purple line) and the Korean Won (blue line). As the chart aptly demonstrates, the Kiwi dollar (black line) has generally followed these Asian currencies in weakening against the USD over the last three years. The Kiwi and the Asian currencies have not weakened as much as the Yen, as none of the currencies have held 0% interest rates like the Japanese have. The reasons behind the broad correlation of the Asian currencies to the Yen lies in export trade competition. Chinese manufacturing exporters have to maintain price competitiveness against Japanese export product into the US and Europe. If the Yen weakens substantially, the Chinese Yuan has to go with it to some extent so that China keeps its export markets against Japanese product.

The question for the NZD/USD exchange rate’s future direction is whether it will follow the Japanese Yen in the other direction? Over the last two weeks that has not been the case as the unwinding of the carry trades has seen NZD selling and Yen buying. However, after that unwinding ends, and the Yen continues appreciating back to 140 and 130 against the USD due to increases in Yen interest rates and decreases to US interest rates, there is a high probability that the Kiwi dollar will follow the Yen and the other Asian currencies in strengthening against the US dollar.

The Bank of Japan hold their next meeting this coming Wednesday 31st July, wherein the financial markets will be looking for fresh nuances that they need to lift their interest rates to bring their inflation rate down. Over the last six months they have shown little intention to do so, despite the substantial depreciation of the Yen increasing all imported goods costs and adding to inflation. Japan’s inflation rate zoomed up from 0.00% to 4.30% in 2022 as the rest of the world experienced similar rapid post-Covid increases. Over the past 18 months since, their annual inflation rate has been remarkably stable around 3.00%.

Fed set to signal first interest rate cut

Whilst the Fed will not be actually reducing their Fed Funds interest rate this coming Thursday morning (7am NZT), a subtle change in their statement wording should provide a sufficient signal that they are preparing the ground for their first cut at the next mid-September meeting. The inflation path has tracked down nicely towards the 2.00% target over recent months, following the “bump” higher in inflation over the first quarter of 2024. There seems very little risk of inflation reversing higher (oil prices are falling again) and the employment conditions in the US economy have weakened significantly over recent months as well.

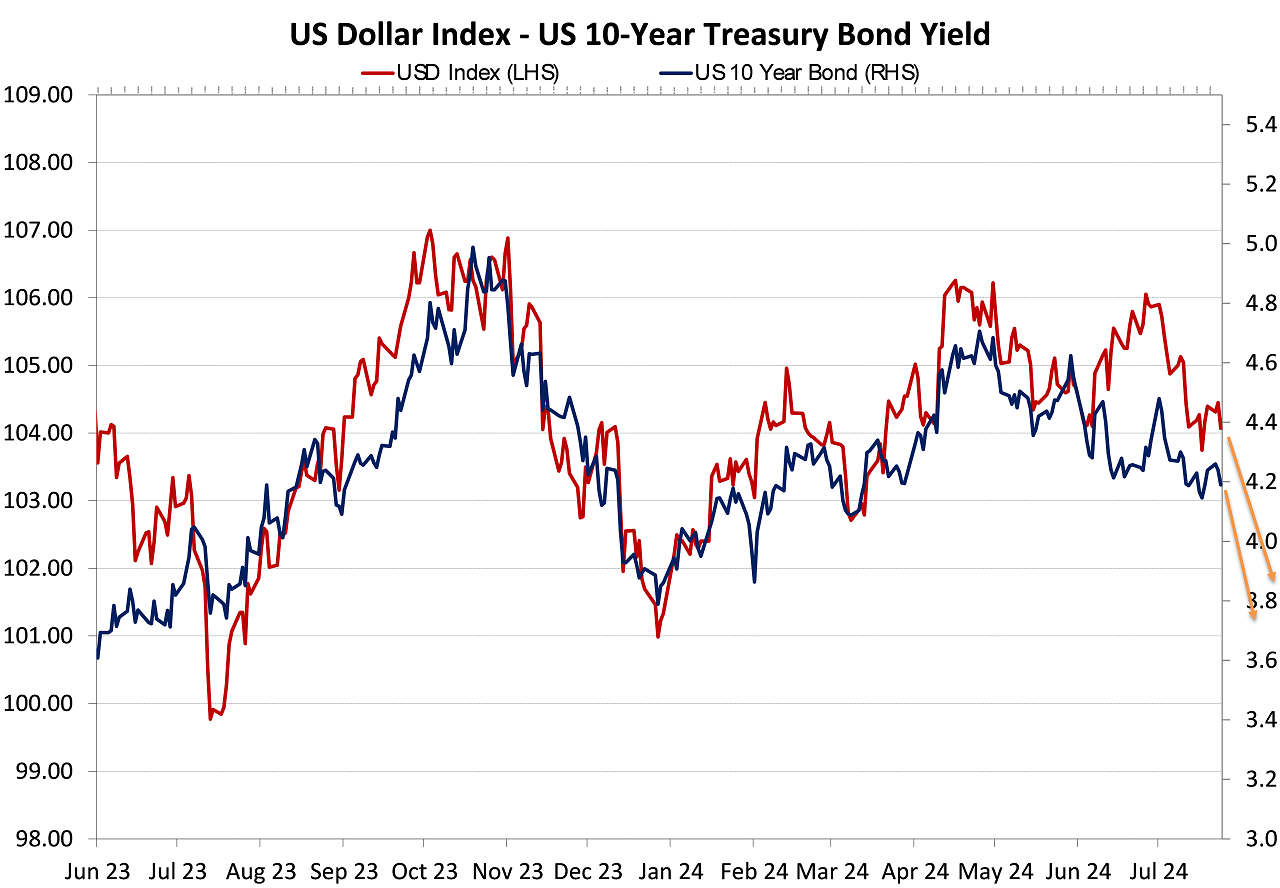

US interest rate markets are now pricing-in three x 0.25% cuts to interest rates before the end of the year. Cuts to come at the Fed meetings on 18 September, 7 November and 18 December. The US bond market has already responded to the lower inflation track and weaker jobs environment over recent weeks, the 10-year bond yield decreasing from 4.70% at the end of April to 4.19% today. A confirmation from the Fed this week, an actual cut in rates coming up in September and weaker US economic data should all combine to continue to push these yields lower to below 4.00% over coming weeks. As the chart below depicts, the US dollar Dixy Index does follow the direction of the 10-year bond yield very closely, therefore further depreciation of the USD to near 102 (currently 104) seems likely. The USD depreciated to below 102 when the Fed first pivoted in December 2023 and 10-year bond yields decreased to 3.80%. There is a lot more certainty today that the Fed will cut three times in 2024, than there was in December 2023. Since December 2023, the US interest rate markets have priced in as high as six cuts and at other times zero cuts. We are back to the original Fed dot-plot forecast of December 2023 of three cuts this year.

A weaker USD dollar for Fed interest rate reasons over coming weeks is expected to allow a quick recovery in both the NZD and AUD from their recent Yen-related selloff’s. The Kiwi dollar has always displayed rapid recoveries from spikes below 0.6000 in the past. For these aforementioned reasons local importers in USD should not panic, use existing hedging for current USD payments and have confidence that they will be able to enter replacement hedging above 0.6200 over coming weeks.

Australian CPI inflation outcome crucial pointer for the RBA

Global currency market changes with the Japanese Yen carry-trade unwinding have hurt the Aussie dollar over the last two weeks, despite the domestic Australian economic data suggesting a higher AUD. Australian jobs increased by 43,300 in June, were well above prior consensus forecasts of +10,000 to +20,000. The employment market is considerably stronger than what the RBA have factored into their inflation forecasts. The CPI inflation data for the June quarter is released this Wednesday 31st July and forecasts are for another 1.00% increase for the quarter, on top of the 1.00% increase in the March quarter. Such a result will lift the annual rate of inflation from 3.60% to 3.80%. The reality is that the 4.35% interest rate level in Australia has not tightened monetary conditions sufficiently in the economy to slow activity, change price setting behaviour and reduce inflation. The residential property market in Australia is on the rise again, clearly mortgage interest rates are not high enough to dissuade buying demand.

A June quarter inflation result above +1.00% may well push the RBA to hike interest rates at their 6th August meeting. An inflation result at or lower than +1.00% may allow them to hold rates at 4.35%. However, they will signal that the sticky high inflation problem they have will not allow them to cut interest rates until well into 2025. The smart money may well be buying the AUD against the USD, at these unexpected lower levels of 0.6550, well ahead of the RBA meeting on 6th August.

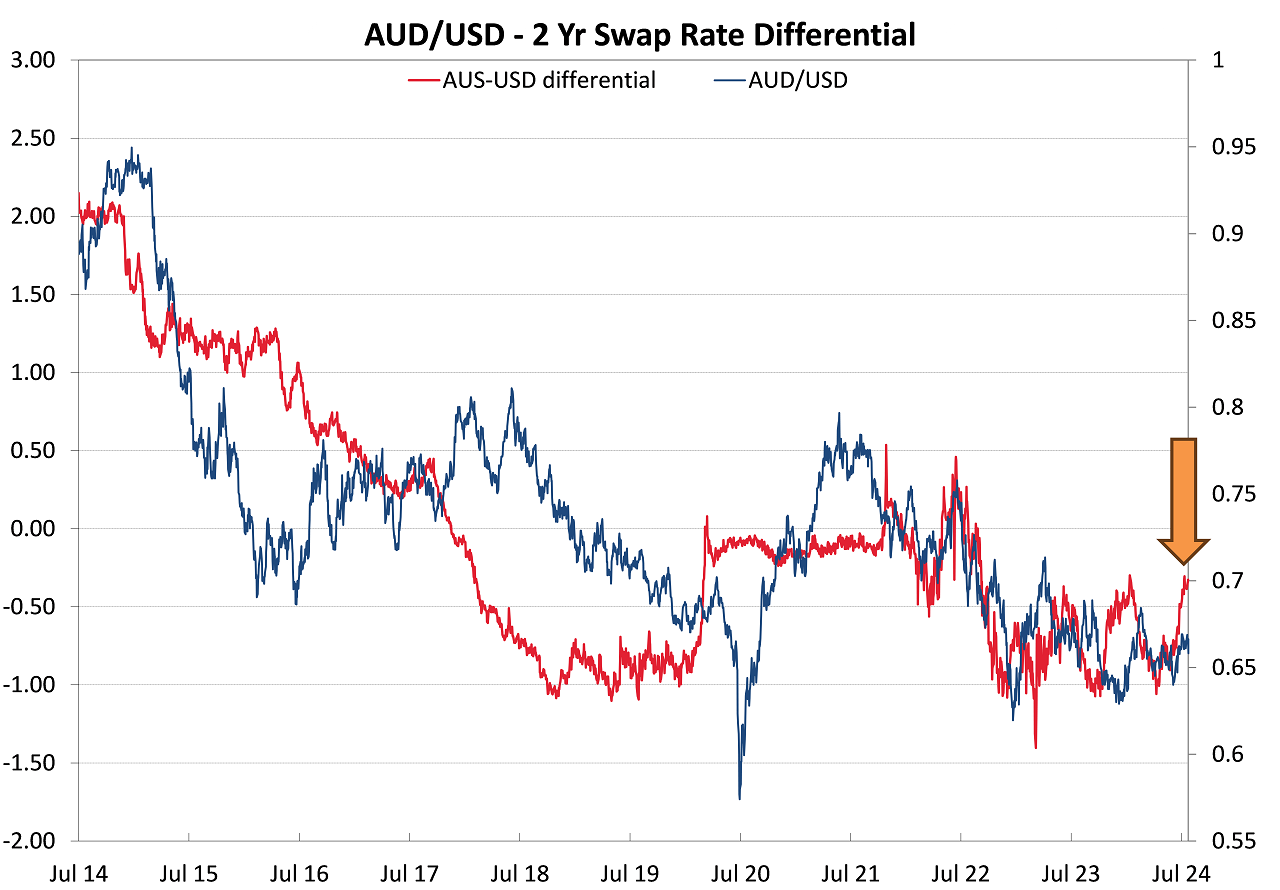

The evidence that the Aussie dollar should rapidly recover from the recent sell-off comes in the chart below. The interest rate differential (red line) between US and Australian interest rates has changed abruptly over recent weeks. US two-year swap interest rates have reduced and are set to fall further as the Fed cuts rates. Australian two-year swap interest rates have increased as the market re-prices the fact that a 4.35% OCR in Australia will not be changing for quite some time. The net result is a sharply narrower interest rate differential, reducing from Australian rates 1.00% below US rates to now just 0.35% below US rates. The AUD/USD exchange rate tracks the interest rate gap, and that interest rate differential points to an AUD/USD exchange rate well above 0.7000.

As we have seen over the last few weeks, the NZD/USD rate follows the AUD/USD rate very closely. The odds are favourable for a rapid NZD recovery on the back of the Australian CPI result this week and the subsequent RBA statement the following week.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.