Summary of key points: -

- Trump wants a lower USD, however his policies just look like volatility

- Lower NZ inflation – “great news” or maybe not?

- Aussie dollar pulls back from earlier gains

Trump wants a lower USD, however his policies just look like volatility

As all followers of US political news will testify to, Republican candidate Donald Trump has an opinion on just about everything, even the future direction of the US dollar.

Whether any of his boastful claims and predictions are backed by any facts, analysis or evidence is another matter entirely! In picking JD Vance as his running mate, “the Donald” has delivered an unmistakable signal that, should he win the Presidency, weakening the value of the US dollar would be a priority policy. Trump has always questioned the benefits of a strong dollar policy as he sees it as being a negative for the competitiveness of US manufacturing exporters. He has always desired to return manufacturing from China to the US and a weaker dollar would enhance that change. However, as foreign exchange market followers well know, desiring a certain shift in direction of a currency’s value against another will never cut the mustard on its own. Interest rate differentials and relative economic performance are the main drivers of exchange rate shifts. Proclamations by politicians rank down the list as major influencing factors.

A number of Trump’s economic policies are potentially positive for the US dollar. Import tariffs increase inflation, which in turn keep US interest rates higher than where they otherwise would be. Lower corporate tax rates and less regulation are positive factors for the economy and thus the US dollar value. When Trump first won the Presidency in 2016 the above set of policies initially strengthened the US dollar, however the overall direction of the USD through the four years (2016 to 2020) of his term was something of a mixed bag. Introducing import tariffs on Chinese manufactured goods coming into the US, runs the risk of retaliatory measures and outright trade wars. Such a contentious global trading environment is never favourable news for the NZ economy or the NZ dollar.

On the other hand, Trump policies to cut taxes will only result in even larger US internal Government budget deficits (depending on GDP growth), resulting in a weaker US dollar value. Foreign investors will not fund US Government debt (from the larger fiscal deficits) if the US dollar’s value is too elevated. The financial markets will force the US dollar downwards to a level that foreign investors will be prepared to come in and buy US assets, such as Treasury Bonds.

Another plank to Trump’s economic policies is to blunt the independence of the US central bank, the Federal Reserve, should he win power in November. Trump thinks the Fed should be cutting interest rates tomorrow, as like all property tycoons he always believes that lower interest rates are “better”. Removing the Fed’s strict independence would be an attack on the US dollar’s status as the world’s reserve currency and it would immediately undermine its value.

Donald Trump does have some support for his view that the US dollar is overvalued. The USD’s “real narrow effective exchange rate”, as determined by the Bank of International Settlements, is more than 12% above its long-term average going back the mid-1960’s. There is a precedent for the US Government stepping in to bring down the value of their dollar. In 1985, under President Ronald Regan, the US Secretary of the Treasury, James Baker signed up to the “Plaza Accord” agreement with Japan, the UK, West Germany and France which instigated coordinated FX market intervention to depreciate the US dollar. It proved successful. However, it is extremely difficult to see Trump getting any support from the Europeans, who he has lambasted over NATO contributions. A weaker US dollar would be associated with poor performance by the US economy, something that Trump would not want to be seen as responsible for.

In summary, when it comes to policies on foreign exchange and the US dollar’s value, Donald Trump is a bagful of unsubstantiated contradictions that adds up to total incoherency! The only conclusion one can draw from Trump’s exchange rate policy is that the US dollar has the potential to be much more volatile compared to times when he is not “President of the Free World”.

Trump is correct in stating that the weaker Japanese and Chinese currencies do provide an international trading advantage for those countries. However, the Japanese have been intervening directly in the FX markets to slow the Yen’s depreciation. That policy will only be successful when the Bank of Japan takes the inevitable decision to increase their interest rates for the first time in 30 years.

Despite Trump’s intention to weaken the US dollar value, the reality is that a lot of hot air statements only work if they are followed up by decisions and action. Citibank recently summed up the situation with Trump and the USD as “Absent a coordinated, international effort to weaken the USD, we do not expect Trump policies to be USD negative despite the rhetoric”.

What will determine the direction of the US dollar against the major currencies over coming months will be the timing and extent of US interest rate cuts by the Federal Reserve. The 31st July meeting of the Fed now stands as a potential fresh negative for the US dollar as Chair Powell starts to lay out the path for interest rate cuts. The PCE inflation result for June of 0.00% (or lower) on 26th July could well by the final piece of the evidence/confidence jigsaw the Fed members need to make that “cut” decision. The PCE annual rate of inflation will only reduce marginally to 2.50%, however the Fed will be looking forward (just as the markets will be) to the August and September PCE results where the annual rate will fall away to 2.00% as the larger +0.40% increases in August and September 2023 drop out of the annual calculations. Chair Powell has already confirmed that they will not be waiting for inflation to be actually at 2.00% before cutting, they will move beforehand in anticipation. We are now at that point. The 31st July meeting will lay the ground for the first cut at the mid-September Fed meeting.

Lower NZ inflation – “great news” or maybe not?

The local media reported the June quarter’s inflation result as “great news” for the economy and everyone in New Zealand. Lower mortgage interest rates were on the way, and all could celebrate. Whilst the quarterly increase of +0.40% was below the RBNZ’s forecast and prompted the money markets to immediately price-in three x 0.25% cuts to the OCR interest rate before Christmas, the RBNZ will be very aware that the problematic “non-tradeable” domestic inflation rate only marginally reduced on an annual basis from 5.80% to 5.40%. The overall annual inflation at 3.30% was entirely due a sharp reduction in the tradable inflation component i.e. imported cars and TV’s.

Therein lies the rub as to why the inflation result was not such “great news” for the average Kiwi household. Discretionary and one-off consumer items such as vehicles, TV’s and washing machines may have reduced sharply in price as retailers discount in tough trading conditions. However, the “staple” items and regular household payments for electricity, rent, insurance, rates and internet/mobile services all increased, reflected in the annual increase of 5.40% for non-tradable inflation. Households are not buying a new TV every week, but they are still suffering from the continuing high price increases for the regular staples. Thankfully, food price increases have come to an end and fuel prices are stable.

You do not read of this form of analysis from the “rah-rah” economists celebrating lower interest rates. Unfortunately, households will continue to pay the price as no-one addresses the elephant in the room, which is the permanent non-tradable inflation of 3.00% plus every year.

We see the first RBNZ interest rate cut coming at their 27 November MPS meeting, the first meeting after the mid-October release of the September quarter’s inflation numbers. The RBNZ are forecasting a 1.30% increase for the September quarter, and they will want the confidence that it has not blown out above that before cutting interest rates.

The lower NZD/AUD cross-rate at just under 0.9000 represents the pricing-in of upcoming interest rate cuts in New Zealand and no cuts on the horizon in Australia. The NZD/USD exchange rate has not directly reacted to the CPI inflation result; however, it trades at the lower end of the 0.6000 to 0.6300 range due to recent AUD and USD movements.

Aussie dollar pulls back from earlier gains

A week ago, the prerequisites were firmly in place for further Aussie dollar advances against the US dollar, the currency pushing up through the 0.6750 resistance level to 0.6800. The probabilities were growing that the RBA would have to hike interest rates in early August and the economic data during the week in the form of stronger than expected jobs growth in June, all pointed to further AUD gains.

However, as foreign exchange markets are prone to do, the opposite has occurred. The Australian dollar has pulled back sharply from 0.6790 on 13th July to trade at 0.6690 at the close on Friday 19th July. The one cent AUD depreciation has dropped the Kiwi dollar from 0.6100 to 0.6015 over the same time period.

The reasons behind the unexpected AUD pull back appear to be: -

- Donald Trump’s comments on Taiwan have slammed the share prices of semi-conductor chip makers linked to Taiwan. The resultant risk-off investor sentiment on Wall Street has hurt the AUD over recent days.

- The rapid movements in the Japanese Yen on FX market intervention last week have dissuaded carry-trades selling Yen, buying the AUD. A source of AUD buying disappeared.

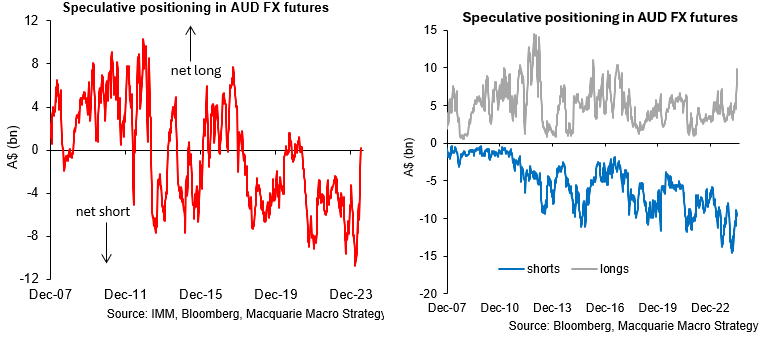

- Over recent weeks the change in the speculative positioning on the Australian dollar in US futures markets has been nothing short of spectacular. The previous 100,000 futures contracts net “short-sold” the AUD (anticipating a weaker AUD) have reduced significantly (refer charts below). However, the futures market data reveals that the change is due to new “long-AUD” positions matching off against the existing “shot-sold” positions still in place to produce the big change to the net positioning. The “short-sold” AUD punters are still hanging in there and maybe the new speculators entering long AUD positions have pegged back their bets, resulting in the AUD selling over recent days.

- The USD itself strengthened last week from lows of 103.40 on the USD Dixy Index to close at 104.06. The various “Trump Trades” in the markets were encouraged by his one and half hour speech to the Republican National Convention and the divine intervention that allowed him to walk away from an assignation attempt.

The above factors are all short-term changes that are delaying the expected AUD appreciation, not fundamentally negating it. To break above 0.6800 the Australian dollar needs a weaker US dollar, it looks like we will have to wait until the 31st July Fed meeting to get the next impetus down in the USD.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

4 Comments

It is unclear as to who Trump intends to appoint to the high offical positions and his cabinet. Some of that positioning will be tempered by whether or not the Republicans secure majorities in both houses. However on past and current form you would have to conclude the whole damn shooting box will be brimming with yaysayers. Trump enjoys and thrives on chaos as continuous dust ups and dust clouds provide great camouflage. Chaos, unpredictability, turbulence, the US$ will just have to, like everything else, buckle in for the ride.

Great article. It is difficult to obtain such balanced analysis elsewhere. Only a very few economists have similarly analyzed the possibilities of the "Trump trade" on the U.S. dollar.

Thanks - good update

I continue to be amazed by the support Trump has - and especially from those who should recognise his serious flaws and the risks

Self interest appears to win out in the US of A. Maybe the messaging will change now that Joe is standing aside

Trade tariffs could put a spanner in the gears and drive inflation which could ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.