Summary of key points: -

- Monetary policy imbalances show up in exchange rate movements

- New Zealand’s domestic inflation problem – identify causes and enact solutions

- Crucial signpost for US inflation, interest rate and currency direction this week

Monetary policy imbalances show up in exchange rate movements

Global exchange rate movements over this last week have identified and confirmed the differing approaches and settings to monetary policies at this time.

The US Federal Reserve is clearly prepared to be very patient before embarking on interest rate cuts, they want to receive a high level of confidence that their inflation rate is heading to the target of 2.00% before committing to a policy adjustment. In stark contrast, the Japanese and Europeans appear to be a sixes and sevens with managing monetary policy, resulting in both the Japanese Yen and the Euro being sold against the US dollar over the last week. However, the NZ dollar and the Australian dollar have not lost ground against the USD, remaining close to the middle of recent trading ranges at 0.6150 and 0.6650 respectively. The recent message from both the RBNZ and RBA is that they are not comfortable with their sticky/high domestic inflation situations and therefore monetary policy has to remain at restrictive/tight levels for some time yet to pull that inflation down i.e. interest rates stay higher for longer in New Zealand and Australia

The problem with Australia is that the RBA never increased their interest rates in 2023 to a high enough level to change price setting behaviour in their economy. They are now paying the price for that policy error and a number of Aussie economic commentators are now calling for further RBA interest rate hikes from the current 4.30% level to drive inflation down earlier, than otherwise would be the case. The prospect of Australia increasing interest rates over coming months when everyone else (NZ excluded) is looking to cut interest rates is a real and growing probability. The key determinant as to whether the RBA hike rates, or not, will be their June quarter CPI inflation result due for release on 31 July. Current headline Australian inflation is 3.60%, which is forecast to reduce to 3.20% if the June quarter increase is +0.60%. Some economists are suggesting that the quarterly increase could be as high as 1.00%. If the quarter’s outcome is between +0.60% and +1.00%, the end result is that RBA Governor Michelle Bullock will have run out of patience and could well hike. The monthly CPI inflation indicator for May is set for release this Wednesday 26th June and prior forecasts are for the annual inflation rate to the end of May to have increased from 3.60% to 3.80%. The next RBA meeting on Tuesday August 6th stands as a potential major turning point for the Aussie dollar, an interest rate hike will send the AUD/USD above 0.6700 to 0.7000 in a flash.

The Japanese Yen has continued to depreciate against the US dollar as the Bank of Japan dilly-dally on their monetary policy management. Go back a few months, we had confidence that the Japanese would make decisions to change their monetary policy from negative interest rates to positive interest rates as wage increases in their economy were pushing up inflation. Unfortunately, the Bank of Japan appear very reluctant (scared?) to enact the necessary monetary policy changes. Their frustrating hesitancy to do the inevitable has resulted in the FX markets lambasting the Yen as the 5.00% interest rate gap to the US dollar makes it a “no brainer” carry-trade bet. The Japanese have intervened in the USD/JPY currency market to the tune of US$60 billion so far to halt the Yen slide. The intervention may have held the Yen below 156.00 during April and May, however the absence of Japanese interest rate increases has resulted in another Yen sell-off to 159.80 over recent days. The Bank of Japan’s next meeting is also 31 July, however there is a “summary of opinions” report from them on Monday 24th June. The Yen will remain under downward pressure until they actually make a decision to increase interest rates. The fact that the US is about to officially call-out Japan (alongside China) as a “currency manipulator” might be enough to embarrass the Japanese into taking some action.

The sell-off in the Euro from $1.0900 on 3rd June to below $1.0700 today had more to do with political events in France than the decision by the ECB to cut their interest rates by 0.25% on June 12th. The French economy has taken a real hit since President Emmanual Macron called a snap election a week ago. Business activity/investment and services industries (hospitality) have contracted due the uncertainty surrounding the election that takes place in two rounds of voting on June 30th and July 7th. Foreign investors into France are running for the hills and the negative sentiment has hurt the Euro. The Swiss central bank decided to cut their interest rates for a second time last week, adding to the downward momentum on the Euro. The ECB are unlikely to lower their interest rates again for quite some time, that in itself is supportive of the Euro if the US Fed cuts rates in September, November and December.

New Zealand’s domestic inflation problem – identify causes and enact solutions

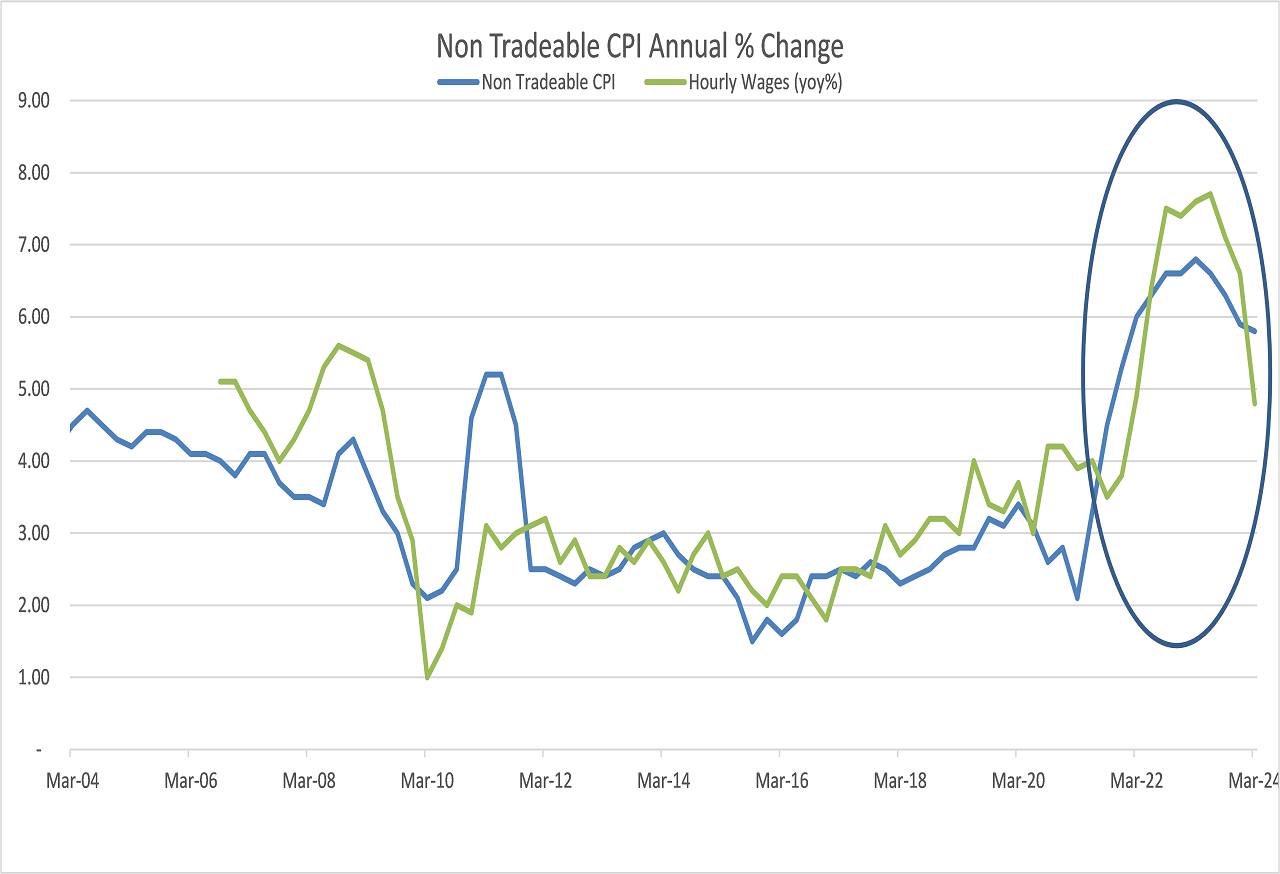

Over recent years this column has repeatedly highlighted and documented the “elephant in the room” problem New Zealand has with permanently high domestic/non-tradeable inflation. The solid rump of +3.00% persistent non-tradeable inflation is by no means new; it has been in place for more than a decade. The imported deflation from China over the 2014 to 2020 years just disguised the problem. The extraordinary and excessive monetary and fiscal stimulus measures in the Covid years covered the problem over again. As the chart below confirms, the immigration policies of the previous Ardern Government that caused acute labour shortages in 2021 to 2023 exacerbated the wage-push inflation problem further, resulting in the 5.70% non-tradeable inflation rate we have today. Percentage wage increases are now declining rapidly; however, it is not just wage increase that is behind the high non-tradeable inflation.

The sources and root causes of our persistently high domestic inflation fall into two categories: -

- Lack of competition in some domestic industry sectors – Open and robust market competition is the best discipline to keep prices/inflation low. Unfortunately, the NZ economy does suffer from a low level of “economies of scale” in many industries to create that fierce competition between suppliers of goods and services. The duopoly in retail supermarkets will not change unless a global player such as Aldi comes in and disrupts (as has happened in Australia). The New Zealand market is just not big enough population -wise for Aldi to make it work. Similarly, competition is more “cozy” than “fierce” in banking, insurance, energy, construction and domestic air travel.

- Out of control price setting behaviour in the public sector – Any examination of the component parts of non-tradeable inflation will reveal that fees, charges and prices are consistently increased by more than 3.00% every year for many years by Government departments, Local Government and Government controlled sectors such as education and health. Imposed legislative and regulatory changes results in cost increases (mainly additional people being employed) being passed through into higher prices charged to households. There is no competition and there is no control. Local Government rates (10% plus increases coming into the September quarter’s CPI numbers) is the worst offender. Housing rents have been pushed up in recent years by the previous Government’s tax and tenancy policies.

Whilst belatedly identifying and highlighting these sources of high non-tradeable inflation (which are just not sensitive to interest rates) in their latest monetary policy statement, the RBNZ offered no suggested solution to rectify the problem. Neither do you see solutions being suggested by politicians or bank economists or business associations to the New Zealand economy’s most pressing problem. Surely, someone has to take ownership and make some bold and innovative changes here. Whilst there are no “eureka” solutions to the first category of root causes of domestic inflation, the second category needs some shock treatment of a Government imposed “price freeze” on their own Government departments, which in turn will incentivise/force them to became smarter and more efficient on their cost side to balance their books. It just needs political leadership and the growing of some gonads to make changes!

As we have previously stated, the RBNZ have not helped themselves to get inflation down to within the 1.00% to 3.00% target band. Under Governor Orr, they have refused to use another tool available to them in their monetary policy kit bag, and that is orchestrating a higher NZD currency value to force tradable inflation down to offset the non-tradeable inflation they have no control over. A stronger NZ dollar will only eventuate if you push NZ interest rates well above US interest rates. The RBNZ have not recognised that or done anything about it. If higher interest rates above 6.00% is just too painful for the economy, they could alternatively “jawbone” the NZ dollar upwards by stating that a higher NZD value would be desirable to push inflation lower. Governor Orr appears frightened of mentioning the NZ dollar value, previous Governors such as Don Brash and Alan Bollard would have played this card by now.

Crucial signpost for US inflation, interest rate and currency direction this week

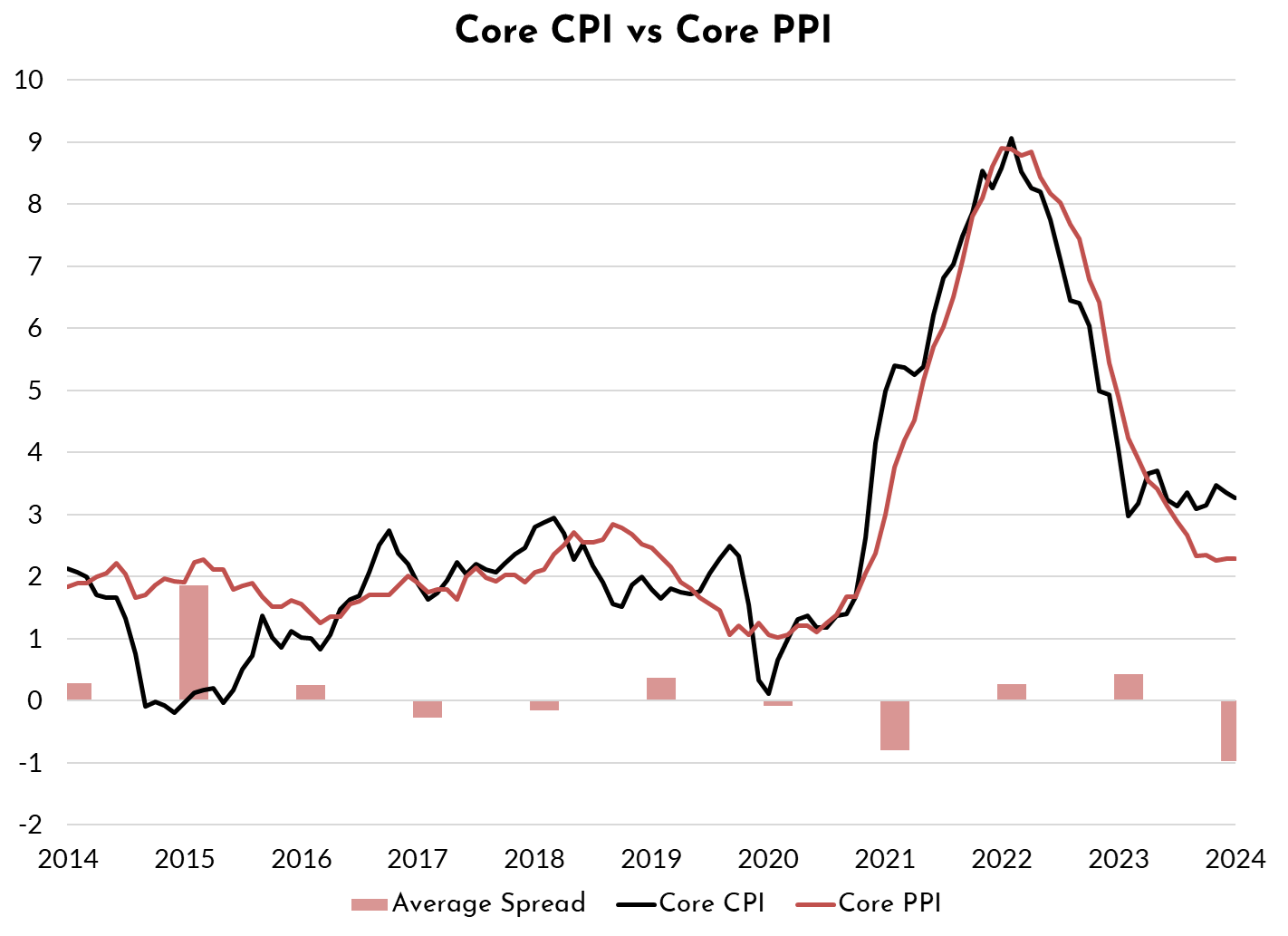

Consensus forecasts are for a 0.10% increase in the US PCE Price Index for the month of May when it is released this coming Friday night 28th of June. A lower 0.10% increase would break the sequence of higher 0.30% monthly increases recorded in February, March and April. A +0.10% change will reduce the annual PCE rate of inflation from 2.70% to 2.60%. The Fed members say they need more evidence and confidence that US inflation is tracking sustainably lower. If June and July monthly PCE increases are also low in the 0.10% arena, the annual PCE rate of inflation will not move down from 2.60%, as the May, June and July 2023 monthly increases were all less than +0.20%. However, if the Fed members observe the trend (and also take into account wholesale PPI prices already reduced to a 2.00% annual increases – refer chart below) and project forward that the August and September 2024 price increases will be a lot less than the 0.40% increases in August and September 2023, they will have a lot of certainty that the PCE annual inflation rate will be hitting the 2.00% target by 30 September. In other words, they are very close to achieving their inflation target over the next three months.

A Fed rate cut is ruled out for their 31 July meeting, however three successive 0.25% cuts cannot be rule out for their 18 September, 7 November and 18 December FOMC meetings. The US interest rate market is today only pricing-in one and a half cuts by year end, however that pricing can shift rather quickly if the inflation scenario painted above transfers into reality. The USD Dixy Index has shot back up to 105.48 on the recent negative Japanese and French developments. The stronger USD is not reflective of generally softer US economic data and the likely PCE inflation picture painted above.

The major risk to the weaker USD (hence higher NZD/USD rate) over coming months is the potential for global trade wars involving China against the US and Europe. Thankfully, China and the EU have agreed to hold-off on tariffs on electric vehicles for the meantime. A Trump victory in the US Presidential election would increase the risk, however there is no certainty about that.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

30 Comments

My Local Body rates in Nelson are increasing 15% this year, but most previous years have seen similar increases. Councils are simply irresponsible in their planning and spending. Non-essentials get more and more ratepayer funds, helping fuel inflation.

Yes. Too many noses feeding from the public trough. And there's little incentive to stop when excesses can be passed on to ratepayers to finance.

Worse, they are spending money on things that deliver zero economic returns. All in the pursuit of woke virtue signalling ideologies like turning roads into cycle lanes or pedestrian only areas, installing speed humps on every single suburban street, funding art installations and paying Maori groups for naming buildings.

Really? Can I see your numbers breakdown on the woke vs non-woke council spending for Nelson this year please?

Here's one. https://www.facebook.com/story.php/?story_fbid=816699703825673&id=10006…

What are we doing?

👉 Installing planter boxes along Kawai Street and Hampden Street

👉 Installing a combination of speed cushions and speed humps

👉 Additional line marking and signage for cycle lanes

👉 Temporary roundabout at the intersection of Hampden Terrace and Kawai Street

Is all of it funded by Council (your rates)? Or is the NZTA (our taxes) helping out?

Speed bumps are woke now?

Totally agree KW

That is exactly what is happening here in Waipa

Speed bumps every few meters ,roads closed off, massive overkill cycle lanes, millions to fix a clock and get consultants reports which don’t give the answers so they get filed away

Recently the council employed local contractors to cut some branches from a tree in our street

At 8am a truck turned up ,three workers got out and started looking at their phones, At 9.30 another truck arrived ,workers got out with orange cones etc, they then cut about 6 very small branches of the tree and by 12 they packed up and left , I would hate to imagine what they charged the council

Local council salaries have gone through the roof, but when you phone to speak to someone you are told to leave your name and number and someone will get back to you

Of course they don’t get back to you

There is no accountability

Inflation is not going away until we see some serious reform

On my 3km drive to the local shops, I now have to drive over 11 speed humps while navigating half a dozen speed limit changes between 30/40/50 kmph zones. All installed in the last couple of years. This is one of the reasons why potholes are not being fixed - all the roading contractors are busy installing speed humps, and they seem to take months to do them as well, so thats why they cost like $450k each.

This is the problem with the new Govt promising to roll back speed limits - they can't go back and make the roads faster. Even if they changed the speed limit back to 50kmph, you can no longer drive that fast due to all the speed humps on the roads. We're stuck with them, because the Council are not going to turn around and remove them.

"3km drive to the local shops"

well there's your problem.

Totally agree.

my council Manawatu council millions and only has a small rate pool to squeeze.

they have spend well over 10 million doubling the size of the library in a time when the internet has removed the need for such large libraries. (Well they certainly shouldn’t be increasing in size).

cycle lanes, spending millions of dollars making the roads less safe for people who actually use them. All these new cycle lanes they have built, I see maybe one person a year use them.

councils need to get back to concentrating on core services.

house insurance is another. Literally increased ten fold in less than 15 years

I don’t know how people on Super afford home ownership these days with rates, insurance and maintenance so expensive these days.

One thing I always look forward to when visiting Westport is their roads. Not a single speed hump, cycle lane or traffic island in sight. Straight "clean" roads with plenty of room for everyone.

But I guess it's only a matter of time before the lefties arrive, telling everyone what's good for them and enforcing their ideologies.

They know that if the homeowner gets behind in their rates, they can contact the bank and make them pay (The Local Government (Rating) Act 2002).

Or seize their house.

https://www.stuff.co.nz/business/114930967/council-is-selling-our-house…

Spot on analysis! It is unfortunate that not all the 'interest.co.nz' regular forum members are reading this.

I still can't quite believe that RBNZ have the chutzpah to blame wages for sticky inflation. Any idiot can see that wages followed the cost of living up. The sequence is very clear

- major imported price shock (oil, fertiliser, then food), which was allowed to march unchallenged into our price structure, leading to an...

- increase in a range of other prices - driving up the cost of living, which drove a...

- response in wages as workers pushed for the money they needed to pay higher bills, which then enabled...

- an increase in rents because our rental market is screwed and we opened the borders and sent demand through the roof

Only the most swivel-eyed of ideologues would look at the above and conclude that the way to correct this dynamic is to use famously slow monetary policy to crash the economy 18 months after the trigger point. The problem was letting the price shock in - the countries that squished inflation did a much better job of holding the price shock at the border.

Agree that wages weren't the trigger, but you keep on and on ignoring the role that demand played. Compare durables and services here:

https://infoshare.stats.govt.nz/SelectVariables.aspx?pxID=2710f146-8524…

to goods and services here:

https://infoshare.stats.govt.nz/SelectVariables.aspx?pxID=f52ac125-65e9…

Very clear that durables consumption surged immediately before and during goods price inflation - that's not consistent with any hypothesis that inflation originated in the supply side, either due to wages as the RBNZ claims or supply shock / disruption as you claim.

Slightly less pronounced, but services consumption also recovered around the same time that services inflation really kicked off - again not consistent with a supply driven inflation.

For sure there were some supply issues contributing, but imo the evidence strongly suggests that demand was a bigger driver, at the very least it's hard to take anyone seriously who does not at least acknowledge demand playing a significant part alongside supply.

So you're going to pretend that the NZRB had zero influence in massively priming the demand (and now likewise ignores it and blames wage rises for it instead)? Seriously?

Not at all! I don't know where you inferred that from. It's very clear on my mind that the RBNZ were heavily culpable in stimulating that demand via their monetary loosening. There were also two other significant contributors to demand pressures - fiscal stimulus visa wage subsidy, without a corresponding fiscal contraction targeted at those who could afford it; and artificial restriction of many services, most importantly international travel, which caused normal demand for those services to suddenly shift to other products. But of those three key causes the RBNZ's monetary stimulus was probably the most significant, and definitely the most avoidable.

HGWR just don't don't hold Orr to account you need to hold Grant Robertson as well re pushing the money printing gravy train. Both as bad as each other

The links don't work but are you linking to the electronic card spending data? If so, you need to remember that total spending in dollar terms is a function of the volume purchased (the demand you think is the cause of our ills) and the price of those purchases! So, if your imported goods price goes up 27% in a single year, what happens to the price and the spend?

If you look at our import data, you can see that the demand for goods never actually got back on the pre-COVID trend. What did change obviously was that the supply chains were gnarled up and the prices shot up as the world re-opened. The demand from little old NZ was irrelevant here.

No, it's not the card spending data. It's the volumes (ie price adjusted) of household consumption data from the national accounts. What you're forgetting in looking at import volumes is that consumption doesn't come directly from imports - it can also come from existing inventory.

Interesting. Digging into the stocks and sales per sector you can still see CPI kicking off after imports and before demand escalated. However, there is clearly a major restocking of inventories going on through the inflationary period, which is not matched by sales. My guess based on other countries is that this was wholesalers filling their stores in case of further disruptions. It would be reasonable to assume that this major restocking would have led to some price increases. Wholesalers passed these costs straight through to customers of course.

I can tell you that the Aussie stock market is pricing in an interest rate rise. I own a lot of interest rate sensitive stocks :-(

Inflation is going to be up - Australia is hosing money at people. With the exception of Victoria, Govts are still fiscally stimulating the economy.

https://youtu.be/7ZBoVeD-SDY?si=rxBKwoY6NjbUOKun

Watch the above and tell me you don't feel depressed about the state of NZ? No wonder everyone is leaving for Australia, Queensland in particular.

A difficult and grating read, probably because of the extremely poor logical structure and ideological bias.

So we have "Housing rents have been pushed up in recent years by the previous Government’s tax and tenancy policies" shunted into a section about Public Sector pricing.

The gist of the piece is

- imbalance in monetary policy results in exchange rate movements,

- criticise historic tinkering which never addressed the root cause,

- pretend to analyse and classify the "root" causes,

- propose more tinkering to paper over the problem of sticky non-tradeable inflation.

The root cause has not been identified and therefore no solution is proposed to address it.

Perhaps a 180% tax on super profits might go some way to establishing what the "root" cause is.

1. "RBNZ has refused to orchestrate a higher NZ dollar currency value to force tradable inflation down" - if RBNZ did this we would have 6%++ unemployment and NZ would be in full blown recession.

2. "Lack of competition in some domestic industry sectors" - Yes, but this is a central govt problem. Successive govts have failed to ensure competition.

3. "Out of control price setting behaviour in the public sector" a) local govt spending should be subject to socioeconomic cost/benefit assessment to ensure it is targeted (asset renewal etc) rather than vanity projects b) central govt is heavily subsidised by not paying rates on most crown land c) (mainly additional people being employed) - FALSE - NZs wider public service is in line with other OECD countries.

4. "Housing rents have been pushed up in recent years by the previous Government’s tax and tenancy policies." FALSE. NZ has some of the highest rent/income ratios in the OECD due to a) excessive immigration at a rate faster than we can build, b) tight planning laws, c) massive underbuilds of social housing (the coalition is committing to only 1,500 when the waiting list is circa 25,000, d) no economies of scale building houses, e) airbnb 29,000 locations etc.

I fail to see why RBNZ includes non-tradeable inflation in the CPI they target. They have NO control over rates, insurances etc. All that happens is that interest rates are raised higher than needed and more poeple and families are thrown on the unemployment scrap heap.

4. "Housing rents have been pushed up in recent years by the previous Government’s tax and tenancy policies.

They have been pushed up because people can pay it and many aren't willing to shoulder any 'risk' of their investments. There are plenty of folk out there with mortgage free homes or with small mortgages left who will pass on any cost they can to the tenant because they couldn't possibly consider having to pay anything out of their own pocket towards an investment that has, or would soon be paid off.

"people can pay", you mean people have to pay. Accommodation is not optional.

Yes, however if a landlord cranks the rent too high than the occupants can afford, they have to move to somewhere else where they can afford or they will get evicted from missed rent. Hence there’s a limit to what people can pay before they either starve and pay the rent, or willingly or forcibly leave.

A higher dollar value?...surely you jest.

Our currency should reflect our abilities and they certainly are not undersold.

If our currency were lower v USD we would be forced to reduce imports and seek local solutions to supply....the much touted living within our means.

We can continue to fool ourselves that the NZD will remain supported forever and a day with a persistent trade deficit and an ever reducing ability to provide a return to those who currently desire to invest in NZD denominated investments, be they Gov bonds or FDI.

Argentina anyone?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.