Summary of key points: -

- Why the “counterfactual” is as important as actual economic results for FX markets

- Will the US dollar continue to follow bond yields and oil prices lower?

- Is New Zealand at risk to a credit rating downgrade?

Why the “counterfactual” is as important as actual economic results for FX markets

The analysis, insight and interpretation of economic events, trends and developments that determine the likely future foreign exchange rate direction is often based on what has happened and whether the FX markets had accurately priced-in the actual outcome in advance (or not).

However, it is equally important to understand and analyse the “counterfactual” situation of how the FX markets react to something that did not happen (however was widely expected to happen). Global currency traders and investors build up positions (long or short a particular currency) based on a view of future economic/market performance or events. There are several examples in recent years of significant shifts in currency values where the expected economic outcome failed to materialise, and speculative FX positions were forced to be unwound as the central premise for the original short or long FX position was no longer valid. The moving sands of sentiment in FX markets continually build-in higher and lower expectations of certain economic outcomes. What makes FX market pricing even more intriguing (and difficult!) to understand is that you are not dealing with just one single economy and its performance. Exchange rates are “relative” prices between the two economies of each side of the currency pair. In the case of the New Zealand dollar value, it could be strongly argued that there is a third economy in the equation, the Australian economy (in addition to the NZ and US economies). The overall stability and narrow range of the New Zealand dollar against the Australian dollar over the past decade is testimony to how highly correlated the NZD/USD exchange rate is to the AUD/USD exchange rate movements. The decisions of the Reserve Bank of Australia on setting monetary policy and interest rates is just as important for NZD/USD exchange rate direction as Reserve Bank of New Zealand decisions.

To understand and interpret FX markets you must consistently monitor the sentiment, views and reasons as to why the traders, speculators and investors are increasing or decreasing their currency positions (i.e. the underlying economic drivers). The related currency buying and selling actions have a large bearing on short and medium-term exchange rate direction. In the longer term, currency values are more typically aligned with relative GDP growth, inflation (economic/cost competitiveness), external Current A/c position, internal Government fiscal position, credit rating changes and the cross-border investment capital flows that occur because of all the aforementioned. Capital inflows if positive (outflows if negative) pushing a currency higher (or lower).

Recent examples of actual and potential exchange rate, interest rate and commodity/energy price movements occurring because something did not happen that was expected to transpire, include: -

- USD strengthening on the global economy falling into recession: Some 18 months ago when central banks ramped interest rates up sharply due to high inflation, there was an expectation that the global economy would move into recession, resulting in the US dollar (according to history) always appreciating in that situation. Large-scale “long” USD positions were entered in expectation of that outcome. The global economic recession did not happen with the US, China, Australia maintaining positive GDP growth through the subsequent period. In addition, the UK and European economic downturns from the Ukraine war related energy crisis turned out to be not as severe as many had expected. Whilst US interest rates have remained above the level of other countries the US dollar has not (yet) been aggressively sold on the unwinding of the long positions built up in 2022 and 2023. It seems it is only a matter of time until the long USD positions are adjusted to lower levels.

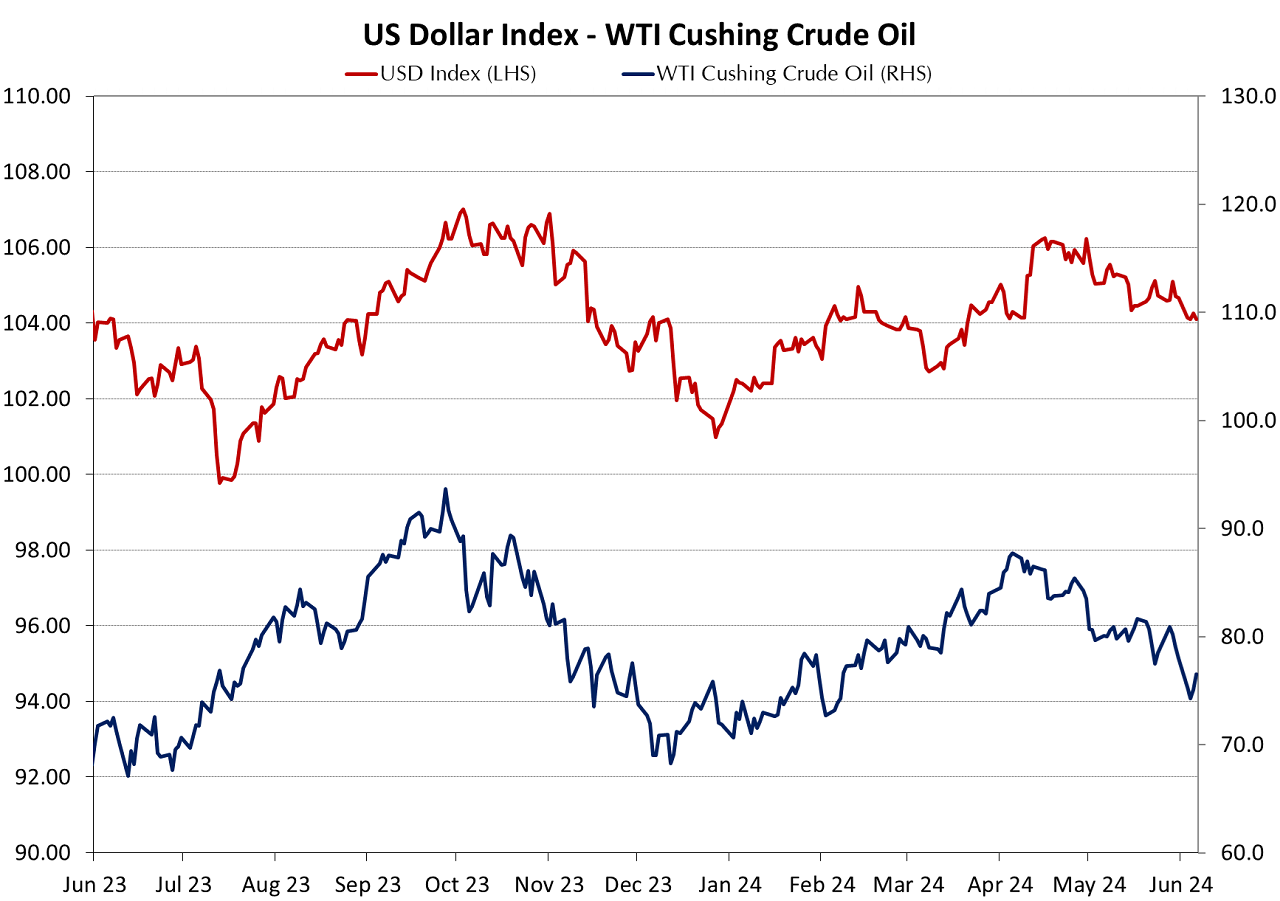

- Oil prices increasing to over US$100/barrel on supply disruptions: Crude oil prices (WTI) spiked higher from US$80/barrel to US$95/barrel when Hamas attached Israel in early October 2023. Several US investment banks concurrently published forecasts of oil prices continuing even higher to over US$100/barrel in 2024 due to Middle East political/military tensions and OPEC agreements to reduce supply volumes. However, oil prices moved completely in the opposite direction in November and December 2023, falling away to almost US$70/barrel. As the Palestine Hamas/Israel conflict continued into the early part of 2024 oil price increased again to US$87/barrel, however they have again fallen away recently to US$74/barrel. It is fair to conclude that the main reason why oil prices have been sold lower over recent months is that the speculative “long” oil positions in oil futures markets built up on the back of the investment bank >US$100/barrel forecasts have all been unwound as the forecast oil price increase never happened. Lower oil prices will now be giving a lot more confidence to central bankers everywhere that they can reduce interest rates as a resurgence in inflation is unlikely. Lower gasoline, freight and energy prices in the US economy over recent months will work to push headline CPI inflation lower than what most have been forecasting for the balance of 2024. Tensions in the Middle East do not have the impact on global oil prices that they once did, due to the US now producing all its own oil supply and therefore they are no longer reliant on supplies from the Gulf States.

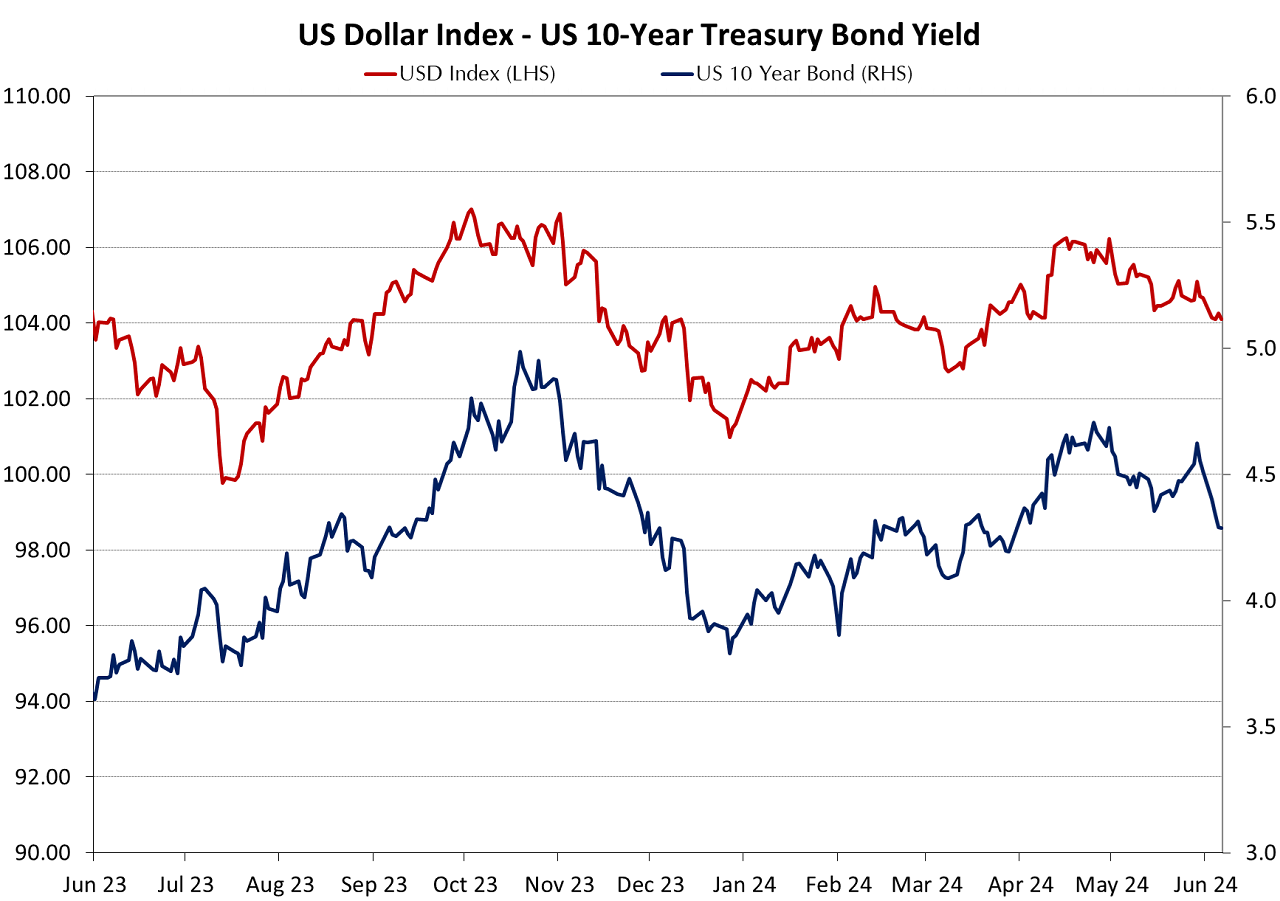

- US 10-year bond yields moving above 5.00% to drive inflation lower: From June to November 2023 US 10-year bond market yields increased from 3.60% to 5.00%, as again global investment banks produced forecasts of higher interest rates being required for longer to bring down inflation as the US labour market remained strong. Increase bond supply from the US Federal Government to fund the growing fiscal deficit added to the bearish outlook for bonds (lower bond prices = higher bond yields). The US dollar value (yet again) was forecast to remain strong on the back of the higher bond yields. How wrong the guru investment bankers were again! The Fed pivoted on monetary policy settings in December as inflation continued to reduce. Bond yields tumbled from 5.00% to 4.00% in December 2023 and January 2024. Whilst 10-year bond yields subsequently increased again to 4.75% in April as “the last mile” of inflation proved difficult to reduce over the first quarter of 2024, weaker employment and inflation data in April and May are again sending yields lower. The sustainably high bond yields have not materialised into fact and many bond fund managers are now starting to extend the duration of their portfolios (buying more longer dated bonds) as they anticipate lower yields over coming months.

Will the US dollar continue to follow bond yields and oil prices lower?

The strong expectation that the US dollar would continue to depreciate on lower US bond yields was hit by a setback on Friday 7th June as the monthly Non-Farm Payrolls for May printed well above prior consensus forecasts. The number of new jobs added in the economy in May came in at a more robust 272,000 against the forecast of 170,000. Yet again, the job increases were all in healthcare, government and hospitality. Average hourly earnings (wages) were also stronger than anticipated at +0.40% for the month (above consensus forecasts of +0.30%). Interestingly, the US unemployment rate which comes from the different household survey increased from 3.90% to 4.00%. The increase in the unemployment rate is consistent with other recent softer labour market data from the ISM survey, ADP private sector jobs and the Conference Board jobs index. The number of people actively looking for a job decreased perhaps because the labour market is softening, and candidates see less chance of being successful with their job application. The JOLTS (number of job openings) report was also weaker earlier in the week. The latest contradicting and volatile employment data for May again appears to be a rogue/spurious number and should not upset the overall trend of weaker data now coming through on the US economy. The Fed meeting next Wednesday 12th June is not expected to rock the boat, as it could be anticipated that the Fed member’s own individual interest rate forecasts (the “dot-plot”) will not be materially changed from their last forecasts in March. Overall inflation and employment trends do not provide any justification for Fed members to increase/prolong their interest rate forecasts. The hawkish group of Fed members still do not seem convinced that inflation will fall further from current levels. However, remove the incorrect and distorting rents measures from the CPI and factor in tumbling oil prices, there is plenty of evidence available to start cutting interest rates in September. There is no longer any need for “very restrictive” monetary policy settings.

The following two charts confirm the strong influence of bond yields and oil prices over the US dollar currency direction.

Following the stronger May jobs report, the USD Dixy currency index is up to 104.70 from 104.00. However, the lower oil prices and lower bond yields over recent weeks do suggest that the USD Index has some serious catching up to do and should eventually move to lower levels below 104.00. Therefore, we do not see the pullback in the NZD/USD exchange rate from 0.6200 prior to the US jobs report, to 0.6100 afterwards due to the stronger USD, as being too sustainable. The Kiwi dollar has climbed three cents from 0.5900 to 0.6200 since the start of May on a weaker US dollar. Nothing has changed the outlook that the US dollar will continue to weaken on global FX markets over coming months and therefore the Kiwi maintains the potential to put on another three cents to 0.6400 over coming weeks.

Is New Zealand at risk to a credit rating downgrade?

Over the last two years since the NZ Government’s fiscal position has deteriorated on excessive Government spending by the previous Labour administration and more recently a slowing economy reducing tax revenue, there has been bouts of speculation that our sovereign credit rating would be under threat of a downgrade. Any threat of a downgrade by rating agencies, Moody’s or Standard & Poor’s, has not happened to date. However, the general view would be that the Kiwi dollar would depreciate on its own accord if the Government’s sovereign credit rating was put on negative watch or was downgraded.

Last week, the third big global rating agency Fitch, fired a few warning shots our way with a statement that our “negative rating sensitivity” would increase if we continued to project returning to fiscal surplus and then consistently underperform in that respect.

Our view remains the same as we have previously stated on this subject, New Zealand will not be downgraded on its credit rating unless our export commodity prices collapse, and we therefore struggle to service domestic and foreign debt. To date that has not happened. New Zealand’s Terms of Trade Index (export/import prices) increased last week to 1,365 in the March 2024 quarter after plunging to 1,299 in the December 2023 quarter. The Terms of Trade Index is still well below the 40-year highs of 1,500 reached in 2020 and 2021.

The Government’s fiscal and debt position is not the only factor that determines credit rating decisions; however, Finance Minister Nicola Willis will be hoping that New Zealand’s economic downturn will not be as severe or as prolonged as some of the doomsayers are projecting. Lower interest rates across the globe over the next 12 months will be positive news for international investment and trade. Therefore, our view is that the export-dependent NZ economy will recover earlier and stronger than what most are currently projecting.

The risk of a lower NZ dollar value on a credit rating downgrade remains small and contained in our view.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

4 Comments

Excellent analysis. Spot-on.

Petrol prices have taken a big fall since last filling up.

It is an excellent piece! The only part I slightly disagree with is 'the export-dependent NZ economy will recover earlier and stronger'. Export is only 24% of our GDP so the effect on the NZ economy will be limited and with tourism still not beating pre-pandemic levels the account deficit remains a challenge!

US fossil fuel production is at ATH... so much for reducing carbon emissions eh.

Im glad our politicians are reinvigorating gas/oil exploration. Without natural gas we dont have enough electricity certainty during winter. Thats the priority over what may or may not happen with the climate

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.