So are we ready for the latest episode of the Reserve Bank's great juggling act?

That's right. It's that time again. The RBNZ is having its latest review of the Official Cash Rate on Wednesday, July 10. And again this will be the cue for our central bank to juggle with, on the one hand reassuring us it is on track to quell inflation, but on the other hand steadfastly refusing to give us any clues at to when the OCR may be cut. And this of course at a time when there is a growing clamour for lower interest rates.

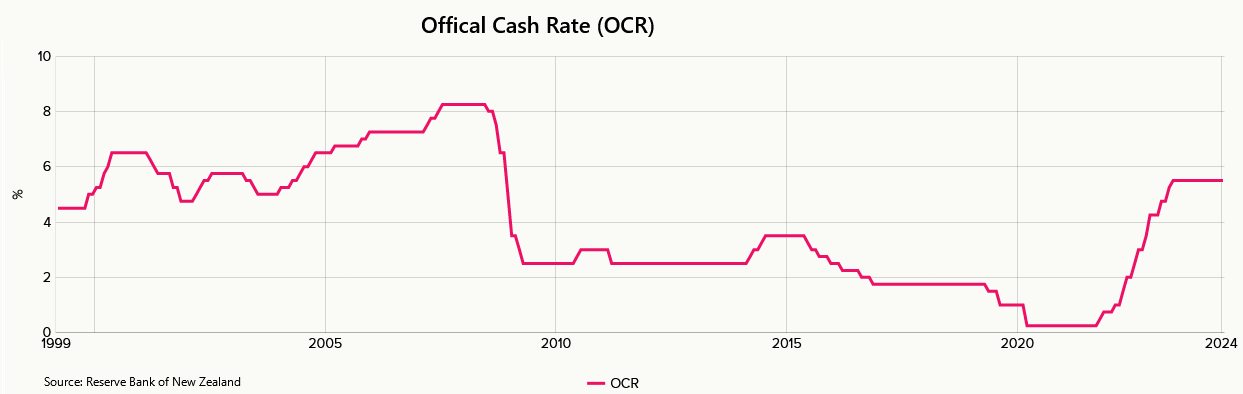

The very easiest of things to forecast about the July 10 event is that the RBNZ will NOT be changing the OCR at the moment. That's a slam dunk.

The OCR will remain at 5.50%, where it has been since May 2023 - on hold following a super-aggressive round of hikes that brought it all the way up from just 0.25% as of the start of October 2021 to the aforementioned 5.5%.

The series of OCR hikes that we saw was the RBNZ's response to galloping inflation that charged all the way up to a peak of 7.3% in the middle of 2022. Remember, it's the RBNZ's job to keep inflation between 1% and 3%, with a specific target of 2%. That's the theory.

Well, inflation has now been outside of the 1% to 3% range for over three years. Which is a while. The most recent annual inflation figure as measured by the Consumers Price Index (CPI) was 4.0% as of the March quarter.

Somewhat frustratingly, the June quarter CPI figures - which will be so vitally important - are being released on July 17, exactly a week after the forthcoming OCR review. (I'll write a full preview of the CPI figures closer to the time.) However, as some indication of what we might expect inflation-wise, the fairly recently introduced monthly Selected Price Indexes, which account for around 45% of what's in the CPI, have been moving very much in the right direction, and food prices had their smallest increase in five years in the 12 months to May.

The RBNZ is forecasting that annual inflation as of June will have fallen to 3.6% and that it will further fall to 3.0% by the September 2024 quarter before ducking its head back under 3.0% (to 2.9%) in the December quarter. Based on those forecasts it will have taken three-and-a-half years to get inflation back into the 1%-3% zone.

However, the RBNZ won't be second-guessing inflation outcomes when its Monetary Policy Committee (MPC) makes its latest OCR decision on Wednesday. It will base the decision on known things. And based on what it knows right now, it won't be contemplating shifting the OCR. Not yet.

In fact, according to its most recent forecasts made in May, the RBNZ is not forecasting any reduction to the OCR till the second half of 2025, while it still sees about a 60% chance of actually raising the OCR again before the end of the year.

Do we really think the OCR might be raised again? No chance. But the RBNZ's keen to keep the ever-eager financial markets from driving down wholesale interest rates and prompting falls in mortgage interest rates. So, having the suggestion of a potential rate hike in the forecasts helps to keep the financial markets on their toes. There's a growing mood though that the RBNZ IS going to have to cut the OCR much sooner than it has indicated.

Since the RBNZ had its last OCR review on May 22 there has not been much key economic data released. But various more timely, second-tier, indicators have all moved pretty strongly in a direction that suggests two things:

•The economy's not exactly on its knees, but it's definitely getting into an uncomfortable crouching position.

•Inflation is on the run. (But is it running fast enough for the RBNZ?)

The biggest piece of economic data that has been released since the May 22 OCR decision was the March quarter GDP figure.

In the run-up to the March quarter figures, the economy went backwards for four quarters out of five (including back-to-back negative figures in September and December 2023 - a 'technical recession').

For the March 2024 quarter the economy managed growth of 0.2%, but nobody was getting particularly excited about this 'move out of recession'.

Economy slumps into reverse gear again

Economists are already forecasting that the economy will have gone back into reverse again in the just-finished June quarter. And in any case we need to very much bear in mind thatt GDP per capita shrank for the sixth consecutive time in the March quarter. The cumulative 4.3% contraction in per capita GDP during that time is more than we had in the aftermath of the Global Financial Crisis.

Other recent economic news has all been consistently downbeat. Retail spending is completely down in the dumps. The BNZ – BusinessNZ Performance of Services Index (PSI), recorded the lowest level of activity for a non-Covid lockdown month since the survey began. Kiwis' confidence in being able to get another job has plummeted. Company liquidations hit their highest level for a May month in 10 years. Both the ANZ Business Outlook Survey and the very long-running NZIER Quarterly Survey of Business Opinion painted a picture of dire economic activity and falling inflationary pressures.

I could go on, but I think you get the picture. It's dark for the economy - but inflation looks like it is in retreat. Which is what we need. But what we also need, or more to the point, what the RBNZ needs, is definitive proof.

Well, we might start to see that definitive proof as soon as July 17, but in the meantime the RBNZ will want to keep us 'on ice', telling us the pressure has to be kept on - and by implication interest rates have to stay up.

Back in April the RBNZ may have set a record for the most brief ever OCR statement, when it virtually said 'ditto' in what was clearly a deliberate (and successful) effort to leave well alone in terms of anything that might fire up market expectations. Move on. Nothing to see here. The RBNZ might just aspire to do similar (very brief) things with the forthcoming statement on July 10.

Ah, but those markets always have expectations. And the expectations have once again been centering on the RBNZ lowering that OCR much earlier than it has indicated it will. The wholesale interest rate markets are now actually pricing a better than 50% chance of the first cut coming in October. It won't. But you increasingly have to think it might come in November. A cut is more than fully priced by the markets for then.

Including the July 10 decision, the RBNZ has four more OCR reviews this year before the three month break till February 2025. These reviews are: July 10 as mentioned, August 14, October 9 and November 27. Two of the reviews - the August and November ones - are also accompanied by Monetary Policy Statements (MPS). That's an important thing to remember, because the RBNZ has a general preference for making the big decisions in tandem with the release of a new MPS. An MPS is generally about 60 pages, chock full of information, with all kinds of charts, graphs and special articles that can fully explain the RBNZ's current thinking; hence the reason it likes to make any significant change at a time when it has a new MPS coming out to explain the change in.

What that all means is that in terms of any significant shift in stance the RBNZ might contemplate before the end of this year, it's more likely to do that during either the August or November review. Or indeed maybe a bit in both.

The RBNZ should, but it won't

So, even though logic suggests the RBNZ should right now be dispelling any thoughts of another OCR hike and maybe suggesting that OCR cuts are in the pipeline, it won't. Not now. If there's to be a perceptible shift in stance then that is not likely to come till the August review at least - although it has to be said that the RBNZ has made something of a habit of trying to surprise the markets in the recent past.

All of which means that those among us who might be looking for clues from the July 10 OCR could well be disappointed. A change in tack is coming but the RBNZ doesn't want us to know about it till it's ready to do it. I leave you with two pithy summations. First from Westpac chief economist Kelly Eckhold:

"We don’t see any net dovish tilt [from the RBNZ] that might bring an easing in 2024 into play – if that’s coming it would be at the August Monetary Policy Statement."

And second, from Abhijit Surya, Australia and New Zealand Economist for global independent economic researchers Capital Economics:

"We expect the RBNZ to leave rates on hold for a seventh consecutive time at its meeting next Wednesday. To be sure, the Bank will probably strike a hawkish tone out of an abundance of caution. However, with the economy in tatters and inflation on its way back to the RBNZ’s 1-3% target, we still expect a pivot to policy easing by year-end."

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

100 Comments

We shouldn’t be paying Orr and his team big bucks to act on definitive proof. I can do that. We should be paying them to exercise judgement and imho they are well behind the 8-ball. Any cuts will have a 9-12 month lag just like hikes and how much needless damage will be inflicted in the economy by the end of this year?

No doubt some here would prefer that the keyword in the headline read “gassing” - rather than “guessing”. 💥

TTP

TTP you young gasbag, I thought you might be left cussing not gassing

This is absolutely crazy!

If the Reserve bank are being paid to tell us they will lower the OCR when the CPI hits their target. Couldn't we save the tax payer money and just make this a basic algorithm?

The economy is slippery when wet and Orr locked up the brakes heading into a T intersection. That is the level of judgement the RBNZ have exercised.

They have a single mandate. We’re paying them to hit 2% inflation. If they abandon that to give an implicit bail out to the middle class, they lose all credibility. People are free to sell up if that’s too hard.

Why are we paying them to do something that you already know how to do? No offense intended to you, but if that is all they have to do, than couldn't we save their salaries?

Be careful what you wish for. We could replace them with the Taylor rule but this would lead to wider variation in the OCR. See the graph here: GDP Live

It would have seen the OCR peak at 8.11% instead of 5.5% and, based on the commentary you see on here, that would be too high :)

This is exactly right! Well said. Surely, the mandate is beyond lowering the OCR when the CPI is below 2% and raising it if it goes higher.

Anyone can lower the cash rate when CPI hits 2%. My youngest child (who I love but isnt a genius) could do that.

Any cuts are not going to be overly material. Sure they’ll bring down the curve but nothing like 2009 through 2012.

The currency is the issue here. Orr is stuck between a rock and a hard place.

Its time to tighten the DTI already and prevent any unwanted house price growth (yes, it’s unwanted by the masses now).

Well said, house price growth is like a cancer growth to the nz economy. We need to cut it out completely. We need to be encouraged (by government) to invest in the productive sector.

Absolutely. Burn Speculand to the ground and then SEAR it into memories.

You’re not Bomber Bradbury by chance?

Not last time I checked.

Who is this mythical person?

What is the productive sector exactly? Certainly not NZ stocks. Agriculture being made to be unprofitable now. Where should someone put their money if not property in NZ?

For the stock market, unless it is a capital raise there is zero change in productivity. Many people don’t see that.

Property in Australia.

Under the matrees

RBNZ are determined to go down in history as the most determined of monetary policy zealots.

They will of course decide to continue to force the transfer of around $42bn a year from people and businesses with debts to:

- Savers ($26bn)

- Bank equity holders (parent banks) ($6bn)

- Bank running costs ($7bn)

- Govt ($3bn tax)

That transfer is 10% of our GDP, or about a quarter of total wages and salaries. Is it any wonder that workers are pushing for wage increases and businesses are holding prices up? We are in a cost of living crisis' and our central bank is making it much worse.

It's important to stress that our combination of high private debt and high central bank interest rate means that we are *leading the world* in the transfer of money from debtors to creditors. It's crazy.

Now, before anyone starts, I know we shouldn't have sent private debt to the moon between 1990 and 2009. But what's the plan here? Crash the economy for a year or so to get private debt down to 130% of GDP and house prices down another 10%... and then power the economy up by dropping rates, boosting private debt back to 150% of GDP, and sending house prices back up again? Then do we go through another cycle? I thought monetary policy was supposed to about acheving stability - not sending the economy into endless boom and bust cycles?

Yep that’s precisely the plan ….😂🤡

In my view this outcome was baked in back in 2020 (or even early say 2013 - 2019) when we decided to pump the housing market through foolish regulations across the board that lead to a euphoric boom in prices. Hence my repetitions on here about the path we were being lead down Including being gaslit by politicians saying that having expensive housing was a good problem to have - ‘a sign of our success’. Such a foolish (self centred and short term thinking) take on a serious issue.

We deserve whatever economic pain comes to us. Unfortunately it will be the poor and uninformed who likely suffer the most from it.

You need your own Column on this site Jfoe..

I agree. Could you please write a concise summary of your thoughts as an article, it would be easier to digest....

When you use monetary policy to create euphoric boom followed by euphoric boom, the consequence is a baked in crash.

It was in the good times that we needed to regulate with wisdom (because in the bad times you don’t have the choice of acting with wisdom, instead you suffer the consequences of your stupidity). For me it was the post GFC 2013 - 2019 period where we could have implemented regulations to prevent people from taking on too much debt relative to their incomes (eg restrictive DTIs, changing tax rules, limiting immigration). This would have stopped house prices rising too far and helped protect NZs financial and social stability if/when the next economic shock occurred.

Instead we’ve doubled down on everything that would make a crash worse if/when the economic shock were to happen.

It doesn’t need to be this way, but until we can get away from this parasitic mindset of debt speculation and using housing as a means of ‘wealth creation’ instead of a place to call home and raise children, then we are going to suffer poor financial and social stability outcomes.

My interpretation of your post above is that you think it must be possible to have euphoric booms without busts which it is not - so instead of talking about how interest rates are too high now (and the transfer of wealth to savers (who may yet now save the day by investing their savings in the coming bust), let’s talk about how we got ourselves into this financially precarious position in the first place (and learn from our mistakes! - but I’m doing so would require seeing the world through the lens of a doom gloom merchant, which in NZ means having a bad attitude!)

Excellent analysis. But I would remove ‘If’ from ‘If/When’.

Shocks will always occur.

Shocks through incompetence are avoidable.

Good points, Independent_Observer,

Over-indebtedness is a villain in our society. Worryingly, it's widespread.

Reducing debt - and inflation - would provide a reset and give the economy a fighting chance.

TTP

Yes. We (the west) has to stop living on private and public debt.

Keeping the OCR high and forcing everyone into a world where we have to earn money before we can spend it.. or at least have a plan for interest rates moves for debt.... isn't a bad idea at all.

What's worrying to me is that whilst the government, businesses and individuals are being forced to deal with their debt.. councils are spending, borrowing and raising rates at out of control levels... not because they need to invest in infrastructure etc nut because of wastage.

All countries east and west live on debt because money is debt. Every dollar we earn and every dollar we have saved was created by banks creating money for loans or Govt spending. So, what do you mean by 'stop living on debt'?

As for local Govt, if you look really closely at this graph you will spot the tiny little yellow blip in some of the bars. That's Local Govt going into debt!

Hence why we BITCOIN.

Surely at its basic level debt is borrowing from the future to pay for things today.

If done conservatively and if risk is managed it works OK. In many cases it relies on gdp or income growth to repay and sustain current standard of living.

Smart debt is accumulated in return for a measured future positive ROI (in today's numbers).

The issue seems to be that it has become the norm to borrow money and not really calculate the real return on investment accounting for risk

For example in nz

1. our productivity is low and our natural population growth is negative and I suspect immigrants don't contribute enough tax to cover their cost to the govt. Any increase in borrowing to fund tosays stuff.. based on per Capita GDP growth and population growth going forward won't work out.

2. People have beenborrowing to invest in property based on historical increases in property values and rents. Without understanding global and local impacts on rates and values.

3. Local governments don't control their costs. Rates are rising faster than inflation with borrowing also rising. To fund what?

My point is that borrowing to fund is only ok if we are experiencing sustainable growth, maintaining what we have and accounting got risk and inflation if we have a truly positive roi.. if not we should be spending on essentials and saving.

- Let’s have an restrictive immigration plan that is sustainable

- Let’s have a capital gains tax on investment property

- Let’s have high restrictive DTIs on property lending to prevent people holding excessive debt (risk) when the next recession arrives

- Let’s change the banking sectors risk weightings away from lending to property and towards other forms of productive business.

- Let’s create a culture that isn’t afraid of the future and their economic survival so that they don’t feel the need to gamble with debt and buy multiple rental properties (ie FOMO is a culture of people living in fear, it is the sign of a sick/mentally unwell culture/society). Instead a culture where you buy your own home, work your job, raise your family and pay off your mortgage (and don’t feel the urge to buy, 3,5..10 rentals which only makes our housing problems worse) - no FOMO! FOMO is our enemy as a society as it results in people making extremely poor financial decisions. If we have FOMO it means that our central bank and government have failed to create conditions of financial and social stability - ie they have failed in their obligated duties to society and their reason for existing. This is where we are at - failing government entities who cannot deliver upon what they are mandated to do.

Government = social stability

Treasury/RBNZ = financial stability

We have neither of the above. Ask around people you know - who feels financial and social secure in todays society? FOMO is a result of these government entity failures.

Agree with this, although you are misinterpreting my point if you think I believe continous euphoric booms are possible.

We can however return to a genuinely full employment economy with affordable housing, decent public services, a regenerating ecosystem, and happy young people that see a future in NZ. The trouble is that we will not achieve those goals with an open, free-market, rentier economy that obsesses over short-term GDP / profit goals. We need to keep money moving around the economy, prevent over-accumulation of wealth (inc across generations), balance our trade deficit, stampdown on destabilising speculation, achieve energy sovereignty etc. We can't achieve those goals with the current economic model.

Take the obsession with GDP. What is it? The dominant measure GDP(P) is basically a measure of financial surplus; the difference between operating costs and sales. We can only have an ongoing increase in that surplus (GDP growth) if Govt deficit spending + private debt increases go up by more than onshore and offshore savings. Look where that is taking us now that the cost of imported stuff has gone up!

So, I am with you on the doom and gloom, but perhaps for different reasons.

‘We can however return to a genuinely full employment economy with affordable housing, decent public services, a regenerating ecosystem, and happy young people that see a future in NZ’

JFoe - could you please bullet point your plan for our path to prosperity based upon this vision? ie what do we need to do in terms of policy/regulation to make this a reality.

And how does cutting interest rates now led to it? That is what I don't understand. I agree with a huge amount of what JFoe says but I can't understand how "cut interest rates ahead of the Fed" ends up as the conclusion here.

As you've said I_O we have had the speculative boom, now we are experiencing the speculative bust. They are a package deal which is why they should be avoided in the first place. I really empathise with people who are getting stung by this especially younger buyers. I have friends who bought at the literal peak because they aren't very financially engaged, wanted a home for them and their family, and were scared they'd be locked out permanently. And now prices have massively declined in their area while payments have increased a lot. And all they wanted was a home of their own (and it is a modest one, let me assure anyone reading). But cutting interest rates now is no real solution especially if it (temporarily) lifts the pressure to solve the fundamental issues that got us into this spot in the first place.

Look, my first choice, would have been to avoid following most of the rest of the world into the neoliberal hellhole through the 1990s and 2000s - liberalising finance and sending private debt, speculation, and rentierism to the moon.

My second choice, like yours and I_O, would have been to stop RBNZ reaching for the debt / housing boom lever in 2020 (see also 2015/16). Govt fiscal policy saved jobs and businesses during COVID, RBNZ monetary policy didn't need to do anything.

My third choice would have been to use fiscal, policy and tax tools to prevent the imported oil / food price shock in 2021 propogating through our low-competition economy and causing sich a significant shift in the price level. My favourite NZer, Bill Phillips (of Phillips Curve fame), told us in 1958 what would happen if imports, being 30% of what we consume, went up suddenly by 25% in a year (30% x 25% = 7.5%).

My fourth choice would be to use fiscal interventions right now to stop the absolute monster we have unleashed with escalating unemployment. Once the labour market starts to collapse, it does not stop until hard action is taken. Ironically, Chch EQ saved us from a grindingly slow recovery post-GFC. What will it take this time?

My fifth choice (and it is a long way back) would be to ease interest rates and release some disposable income into the economy to save some jobs. If we had started very slowly in November we could have managed the exchange rate risks. Or, perhaps we would be better off letting our exchange rate adjust to reality. I mean what are we using our huge current account deficit to buy anyway? International air travel, fossil fuels, fertiliser, cars?

Thanks for the answer, so 1-3 are in the past so off the table so not really relevant. Leaving 4/5.

I'd agree that considering current govt debt levels now would probably be the time for them to pick up the slack with fiscal interventions to get the economy moving. Where we differ is that for me the 5th shouldn't even be an option at this stage. Certainly not without some solid rules in place to prevent a further run up in housing prices and the continuing malinvestment it would represent. The damage this would do in the medium-long term would not be worth the extremely short-term "fix" to the economy it would deliver. We'd just be in this exact same situation but worse a few years down the line (if that).

Although to be honest I have positioned myself personally (investment-wise) under the assumption that option 5 will occur and it will be a disaster. It is the easiest way to kick the can down the road a little bit more and one thing pollies love is taking the easy way out to let future pollies deal with the problems.

"Or, perhaps we would be better off letting our exchange rate adjust to reality."

And that reality is unavoidable. It is a question of when - not if.

And the longer Government & the RBNZ (and Kiwis) pretend there is "nothing to see here" and continue to make the problem worse ...

... The bigger and more painful the adjustment (i.e. NZD crash) will be.

This short term nonsense that the "RBNZ can't drop interest rates as the NZD will fall and inflation will rocket" is unavoidable, i.e. we are living beyond our means. (And if the crash is sudden and substantial, overseas lenders will demand higher interest rates to compensate for the additional risk. What is actually quite terrifying is the RBNZ seems to think - like Muldoon did - that they can somehow control the outcome. They can't. The outcome will be the same.)

Like I said, when, not if. There is no other way out.

I think we can look to the past for many of the answers here - imagine the 1950s and 60s economic model with modern technology aiding productivity / quality of life? But, if you're inviting a rant...

- We need to start with some hard conversations between leaders and the public... The world is getting rough and it is going to get rougher as countries fight over scarce resources. Conflict and climate are going to deliver shock after shock to global trade. We need a plan for NZ that protects our people, our population, our rich natural resources, and provides for our kids, grandkids and great-grandkids.

- First step on that plan is energy sovereignty. We currently depend on fossil fuels for one-third of our power. This puts our economic wellbeing in the hands of oil company price-setters and exposes us to damaging powerplays between superpowers. We are also polluting the air that our kids breathe, and making an outsized contribution to climate change per capita that will win us no friends in the future.

- Our near-100% electrification will require us to import billions of dollars of technology from overseas and dedicate tens of thousands more workers to infrastructure projects over the next 10 - 20 years. These infrastructure projects will also include major climate mitigation works including new sustainable transport infrastructure.

- This will require a warlike effort and we will need to make some changes to how we run the economy to reflect this.

- For example, we will move to full employment. Anyone who wants to commit to a job on local infrastructure projects will be employed and be paid at least a living wage while they train and work. This will disrupt our labour market - pushing low-income wages up as people leave less desirable, precarious work for project work. This will make some things more expensive as firms like restaurants and aged-care residences will have to pay higher wages to secure staff. We will need to work with some companies and sectors on collective pay agreements that allow us to stabilise wages across the economy as we make the transition. This is already done elsewhere (eg Denmark).

- Spending billions of dollars on overseas technology that we cannot make here will only be possible economically if we limit the import of non-essentials. We will use heavy taxation to reduce the import of luxury goods. We need batteries in buses and communities more than we need them in supercars. We need tunneling machines more than millionaires need helicopters.

- We have truly messed up housing in this country and part of our major works will include installing the infrastructure needed for significant housing development. We will also invest in becoming a global leader in sustainable housing design and construction.

- We have grown our economy for the last 40 years off the back of huge increases in private debt driven by our boom and bust housing market. We will use tools like LTV / DTI and diferential interest rates to reduce house prices over the next 10 years while we increase housing supply. The Crown will purchase the land / section under the house of owners that are struggling to pay their mortgage and rent it back at a discounted rate for the remainder of any mortgage term.

- We will aim to be the safest, most sustainable, and (simply the) best place to live in the world. Companies will want their head offices here. People will want their kids to come here and study. We will welcome people and companies to join us and invest in our future - while managing numbers as we catch up on infrastructure.

- Our tax system will be completely re-engineered to focus on 'rents extracted' from the economy rather than income earned from work. That will mean higher land tax, CGT, inheritance, dividend taxes, but much lower taxation of workers' income (and lower taxation of companies). Excess incomes earned from assets will be taxed aggressively.

- The impact of all of the above (and more) will mean that over the next ten years, net Govt debt will be managed up to around 150% of GDP, while private debt will reduce from 150% to 50% of GDP. Critically, Govt debt will be mainly in the form of infrastructure bonds, which will be owned by NZ savers who will receive interest directly from the Crown.

I could go on, but that was cathartic.

Thanks JFoe - I won’t give a detailed response as still trying to digest everything in your comment. But do you follow Dalio’s long debt cycle? Basically history repeats every 80 years or thereabouts. So a repeat of the 50’s - 60’s could be on the cards for the 2030’s - 2040’s. Also aligns with the Strauss-Howe generational theory that predicts this period of insanity will be calmed post 2030 with a new period of prosperity starting from there (once millennials are in charge of society (boomers are in retirement villages/underground) and set policy that will avoid what has happened to them from happening to their children).

Good post.

You have great vision JFoe. If we had a green party that was actually Green they might have had such vision. Which leaves TOP, who may have achieved if Morgan had hung around.

Like but struggling to see how the political class reach a point/have a catalyst that shifts to this. Seems like a big change, could we step towards it or would it require a political earthquake?

Yeah man, I mean, we really don't want to encourage saving.

Whose on the seventh floor

Bewing alternatives

Spare us the cutter

Save up for a rainy day at a household level - sure. Stacking up endless hundreds of billions in financial assets is next level stupid.

An interesting chart but out of context doesn't say too much. Where did you get it btw? I'd be curious to see a similar chart showing Public debt as well as a chart showing movements of major currencies against the USD since, say, 2021.

> I thought monetary policy was supposed to about acheving stability - not sending the economy into endless boom and bust cycles?

I think everyone agrees we are not in a good situation but going from that to "cutting interest rates" is a big leap. Especially as we'd be frontrunning the Federal Reserve which would have a lot of impact. We could (maybe) get away with a 0.25 or maybe 0.5 cut even if the Fed hasn't budged but anything more than that and we'd be looking at a whole different set of problems.

Saying "we need stability, not endless booms and busts" at this point in the cycle is like saying I'm not so sure about going down after having ridden the rollercoaster up....We are in for the full ride at this point. The real question is will we actually change things or just hop back on the ride again.

I can fulfil one of your chart wishes - here's the swap of public (Govt) debt for private debt from 1990 to 2009 and the holding pattern we have been in since. My view is that we would have to reverse back through 1990 to 2009 to have a balanced economy.

I do most of the charts from data I have managed on and off for different jobs. I also have a couple of geeky mates that share some of the offcuts from analysis they do at work on social media (twitter mostly), which I link to.

While people on here always perceive me as a 'cut rates' guy, I never actually argue that is the right thing to do. I have ranked my choices in the comment above.

Thanks for the chart but I meant one which is just like the one you have here except swap out "Private debt as a % of GDP" with "Public debt as a % of GDP". Seems quite relevant to context of these discussions. But obviously can understand if you couldn't be bothered making it but would be a worthwhile addition imo because all govt debt is at the end of the day recouped via taxes on the taxpayer so an important part of the story. So a current and future liability. And if you believe that govts will never pay back that debt....well the implications of that are very far-reaching.

Ffoe: "I have ranked my choices in the comment above."

Might I suggest you push changing the tax system to the top of your list?

When you think about it from a behavioral economics perspective - especially in a NZ context - it probably has the single biggest effect on NZ's economic behavior by a wide margin. And an even greater effect than the RBNZ - supported by successive governments & far too many Kiwis - believing the OCR can do it all.

‘Do we really think the OCR might be raised again?’ Sharon Zolner and her naive friend printer8 do!

I think even Zollner has walked back from that level of crazy now - I think ANZ position is a November cut (unsignalled beforehand).

There is an outside chance he could signal cuts via the statement, I think first one comes in Nov....

Its really dire out in retail land. Given that the track has late 25 but a massive surprise for NZD and it would drop hard.

No one ever cuts once

Retail, hospo and construction are all dire. Collectively they must represent at least 30% of the economy?

Here you go. They make up about 20% of GDP(P) if you include wholesale. Remember that GDP is basically a measure of surplus generated (sales minus costs), so obviously, in NZ, finance, insurance and real estate (FIRE) outgun construction, retail, hospo and construction combined!

If you look at operating income (sales) our retail, wholesale, hospo, and construction sectors make up almost exactly half of the total.

This Housing market crash is a great opportunity.

From Peak NZ housing Ponzi prices......

It's now down on REAL terms by between -40 and -50% in Auck and Wgtn and other large cities, with another -10 to -20% bleed to occur.

Buyers today, should seek big discounts off the asking prices, or walk. The negative equity land is a very Mentally upsetting one, to be in.

The regions will soon catchup with these beautifull "Negative Growth - " Housing numbers. It's a dead cert.

So the RBNZ has the tools now and should continue to chase these Housing Prices down, with a sinking lid DTI.

They should drop it NOW to a 5x DTI FOR EVERYONE. No special favours for the Landlording class.

Then they should drop it to 3.5 or 4x DTI at the bottom of this Crash, in 2027 2028.

Then and only then, should small OCR cuts occur, with retail interest rates falling to around 5% again.

Uber Cheap DEBT has had disasterious social consequences in NZ.

#NEVERAGAIN#

JUST HIGHER INTEREST RATES will be a global phenomenon anyway, given Deglobalisation and ongoing / decade of wars ahead of us.

‘If you’re forced to sell, you’re screwed’ - mortgagee sales expected to rise

The broker said banks were going out of their way to help people struggling financially but when mortgage holidays and interest only options were exhausted the real problems would start.

“I personally think anyone looking at buying a house should wait six months to 18 months. You'll probably be able to get a steal because people will be desperate.”

FECKING ONEROOF!!

The temerity of these Oneroof scrotes !

Those absolute MxxxxxFxxxers and their Writers, were totally complicit in pumping the NZ housing Ponzi to the MAX. They then pumped it higher.

THEN, they went into overdrive, with the countless articles about: "36 million reasons, house prices won't come down"

Now the "Baked in crash" is confirmed as the case and only midway........

That lot should be publicly outed as: PONZI SCHEME PROMOTERS. THEN LEGALLY FLOGGED!

Where the hell is the FMA on this??.

Re the Irish crash

Role of the media

Throughout the bubble, newspapers and media played a vital role in hyping property. No national newspaper was without a glossy property supplement and weekend papers were often equally filled with property ads, reviews of new developments, stories of successful purchases, makeovers, and a gamut of columnists relating their property experiences. TV and radio schedules were filled with further property porn - house-hunting programs and house makeover programs were regular features on every channel. Even in July 2007, Irish Independent journalist/comedian Brendan O'Connor urged people to buy property, even as the bubble was clearly bursting.[42] In April 2011, journalist Vincent Browne admitted that the Irish media had played an important role in adding to the frenzy of the Irish property bubble.[43]

OneWoof, The Comb, Ashley etc etc etc

Surely deep down some of the people writing these articles must have known they were potentially misleading a lot of people about the risks?

The quote from the bible comes to mind on living with integrity - ‘for what shall it profit a man to gain the whole world but lose his own soul?’

How people are happy to get paid to promote a potentially extremely damaging housing bubble on the way up is (and was at the time) completely lost on me.

I think they actually believe it. It’s real estate brain. That’s how you end up with these Pentecostal investment sermon/workshop scams.

In my view a certain woman at the Herald has an awful lot to answer for. A shocker.

FMA staff are probably all property investors.

You are Truly the ultimate Time Lord!

How did you get an 8th July article, today? a real scoop by the looks.

However Its all true. The Crash we all saw 2 years ago, now goes MSM.

Will dearest Catherine Masters job be safe? after uttering such once unheard of, OneWoof Blasphemy?

Or has she thrown for mandatory OneWoof staff meds (Property Ponzo Spruiker meds) down the dunny?

(I will pray for her)

Your "real" figures are nonsense, NZGecko.

The truth is that NZ's median house price (nominal) has risen 60-70% over the last 8 years. (This was detailed in a recent article www.interest.)

Furthermore, rents have increased considerably through this period - so yields have been strong.

TTP

yields have been strong.

At the moment yields are very very weak, and remember residential is not priced by yield is it! , if it is what is the calculation yield to price valuation TTP

Hey TTP,

That's from peak NZ Housing Ponzi REAL prices bud.

But you go screw the Stats, over longer Timeframes (typical Tony A and Ashley tactic) to suit your PBrokers "discussion points" used to condition the housing market vendors/buyers.

TTP, how many of your recent buyers are now near mortgagee sales?? After your spruiking "buynow, bee quick" advice?

Since this time, have you reflected on your past actions and sought forgiveness?

I trust you are stepping up and supporting these thousands of stressed home and rental owners, financially and mentally?

Remember- Those that have so much, have a great responsibility to fellow man.

Prices are not down at all in ChCh!

slower and fewer buyers, but that is not due to lack of demand, loan servicing!

Nothing surer is that if ever a CGT was introduced would ensure prices increased, just like everywhere that has a CGT.

Ozzie prices are higher due to taxes and CGT,

How many units, are you trying to flog off, in old historic swamplands of ChCh?? The Man.

Have got one on the market but it is in the higher price bracket.

buying and selling at the moment is good, and I am never worried about the ChCh market.

Buy well and improve and you just can not go wrong.

Sit on the sidelines and you are missing the opportunities.

So stupidity of cheap printed cash has nothing to do with Aussie prices...tui. There is noise of a rate increase in Straya. Debt punters and filling their pants saying the end of days is nigh if that transpires.

Ace plan…see you ‘28 after your first OCR cut & you can tell me how great it’s been for the country 😂

I’m seriously starting to think that the group obsessed with house prices rising aren’t actually as bad as the group obsessed with it crashing…surely we can use DTI’s to choke price rises, incomes will increase as the economy gets more confidence, if capped then house prices will balance & maybe if we can add in kiwis accepting townhouses which are cheaper than stand alone houses that ratio might start looking happier with some patience.

Or f**k it…let’s burn it all down 🔥👏

On one hand the RB will release another staunch statement this week. On the other hand they'll be eagerly anticipating the Q2 numbers on July 17. They'll be wanting to know to what degree the economy has deteriorated since March.

They'll know as well as we do that there's been significant change. And that it's likely to continue in Q3.

FOMC meeting 31 July.

The next CPI comes out a week later. Couldn’t they close their review dates to align?

They need 3 weeks of meetings in between to decide one thing

How damaging will it be to the reputation of the RBNZ if they are forced to cut pretty much a full year before they are forecasting? Makes the whole process a bit of a joke

reputation with whom?

Overseas lenders. (They provide a huge chunk of our money which we issue as debt.)

I suspect the institutions that invest in NZD have long been well aware of the capabilities of central banks....politicians business and the general public? not so much....and it is likely there that the credibility will be at risk.

Running our country, our businesses and ourselves on masses of debt, damages us. Better we worked on ownership and equity.

Reducing interest rates sends the wrong encourages the wrong things.

You got it KH, high cost of Debt, is a net positive.

Encouraging the robbing of your future-self is indeed foolhardy!

Yet we have the Banks, Mortgage Brokers, Lawyers, Insurers, all want, need and encourage the ever -increasing oodles of Increased Debt on increased Debt...... all useless ticket clippers, the lot of them

Glad its coming to a head this Decade, in a major asset crash.

Let's rebuild from the ashes in 2027/2028, towards a more positive: "Houses as Homes" principle, not an over financialised Housing Ponzi scheme between cut throat, house traders.

Which is probably why the CPI will roar just before that happens. Why? Who is going to keep their savings of a lifetime in the bank if that same bank is going to be bankrupted by the coming asset/property market crash? No one. And what will they do with it first? Withdraw their funds and borrow everything they can, and spend it; on anything, everything that might be needed in the future. = prices will rise; the CPI will rise.

There is only one way to discourage that - a higher OCR, in our case, preemptively. Or stand back, and marvel at the final asset price increases before a 1927 type of ending. But will the RBNZ have the courage to do that? We are about to find out.

Ummm ownership & equity of what after we all decide to never have the evilness of debt…remove debt…money is debt…remove money…no economy to worry about eh…can’t wait to trade magic beans with you all one day 💰🚫 vs 🫘👏😂

KH: "Reducing interest rates sends the wrong encourages the wrong things."

Funny how so many blame interest rates while completely overlooking our tax system.

Could this be why NZ is deep in the poo?

Artificially low interest rates should never, ever, return.

I know some who bought at super low rates, since reset to average rates and have been forced to sell at major losses and the banks are still on their tails, for the deficit.

This Current Crash is the biggest ever seen since over 45 years ago. Many NZ cities are back -40 to -50% in real terms.

This crash will easily beat the 1970's property crash and be the talk of economic textbooks for decades.

The mainstream Media are only now cottoning onto the massive NZ Property Crash. We are so poorly served by the NZ media. No wonder their finances are totally in the swamp.

We are not done yet, this bears claws still wants and needs to do damage to Speculand. Hard Lessons need drumming in, it seems!

This is the 1987 sharemarket toxic moment, for property speculators!

I fully expect we will bottom in excess of -60% is real terms (30- 40% nominal) or a little more by 2027/28.

Yep, if you ain’t got your money out of NZ or planning on how to you are very exposed.

Our business community has become a charity of the ever lending banks.What can’t go on forever won’t go forever.Time for a shakeout.

Going to be painful.

Yes the smart ones are now working out where to put their liquid NZD ?

The NZ economy is totally on the ropes! Sadly true.

ASX company's, USDow/Nas companys, Metals, Aussie/USD Call accounts, NZGBs ??

Better options? (Sorry not doing the crypt co's)

Only Bitcoin matters, the sooner Kiwis cotton on to the philosophy and beauty of Bitcoin, the better everyone will be. The (fiat) monetary issues you've been posting about are global, and regularly discussed in Bitcoin circles.

Hey Gecko I felt sorry you had no upticks not one, so did that for you. Best regards with your property journey

Hey FH. already have sufficient property, amongst other more productive assets.

-Thanks for your concern.

Looking forward to this weeks RBNZ commentary?

Yes I am, but more so the stats dept announcement. And you?

Hartnett: June Was The First Month In 4 Years Without Any Central Bank Hikes

"June’24 was 1st month since Oct'20 with no global central bank hikes; tightening cycle Oct'20 to Aug’23 saw 507 global hikes vs 65 cuts; easing cycle Aug'23 to June’24 sees 108 rate cuts vs 48 hikes"

This. Interest rates down and up nonstop for years. Us average consumers can only consider it funny money.

Hold and hold slowly does it and then make decision and move towards it slowly and intentionally (with regards to central rates). Whether the money and credit is cheap or expensive is what it is for the median consumer who will adjust and continue accordingly in the medium long term. A lot of the pain is the sudden change, these 'crazy' mortgage payments still aren't on par with what most 30yos parents were paying 30years ago.

Or continue doing what's doing until the next unexpected externality (eq, tsunami, 💣 in oecd country, 🌋 NZ , pandemic etc) and drop the OCR to maintain status quo.

Disclosure, 30yo with no borrowing.

Debt has two sides that have to stay in balance. That is, the borrower and the lender each have to meet expectations. The current global financial crisis shows we are out of balance. Foreclosure follows as confidence fails.

Sorry for a non statistical personal story, but a friend who works on building sites has heard of a snowball of builders being made redundant, or those who haven't being asked to take paid leave a year in advance due to no current work...

Sounds very dire to me, (could just be in particular the building industry though which is believable)

I work in civil infrastructure, 3 waters estimator. Certainly a glut of work in our space. Horizontal infrastructure is typically enabling works for the building industry, so could be a sign of worse things to come?

Yeah and the ones on Chris Bishop' knob think these new regs will make developers build houses. Yeah not when there are no buyers!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.