By Patrick Watson*

Just three months ago, a US recession seemed unlikely. The economy was humming along by most measures and Federal Reserve officials had even paused their rate cutting, convinced inflation was a bigger threat.

Now recession talk is everywhere. We know why, too. President Trump imposed tariffs far more quickly and aggressively than most people expected. Meanwhile, DOGE czar Elon Musk is busily slashing federal programs he considers wasteful.

Without debating whether those are good ideas, let’s look at their economic effects. The first has been to generate fear.

- The prospect of a global trade war makes investors and business owners afraid costs will rise while profits shrink.

- Millions of federal workers and contractors who haven’t already lost their jobs fear they will soon.

Both groups respond the same way: By postponing spending plans until they have more confidence in the future.

Such “demand shocks” always cause problems. This one is already showing itself in consumer confidence, corporate earnings, and stock prices. That doesn’t necessarily mean recession, but it could. We don’t know yet.

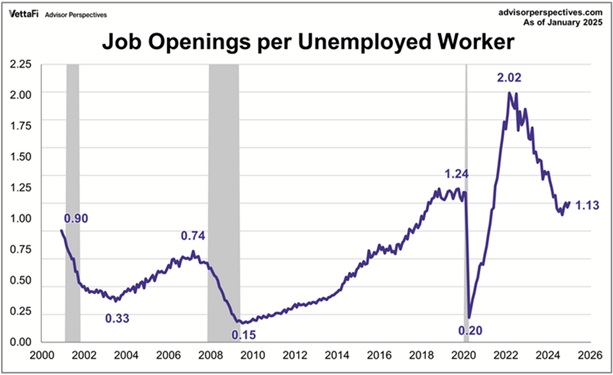

One optimistic factor: the demographic situation. The growing imbalance between working-age people and retirees means there’s not much slack in the labor supply. The latest data shows the economy still has more job openings than unemployed workers who could potentially fill them.

Following big COVID-driven swings, the ratio seems to be stabilizing near the 1.1 to 1.2 range where it was in 2019. This could change if labor demand drops, which is likely if DOGE keeps cutting and consumer spending keeps weakening. It will drop even more if unemployment rises. But barring another pandemic-level event, the labor market should stay historically tight.

Resigning by Proxy

Low unemployment, if it persists, will disappoint some CEOs who want to delete pesky humans who demand things like “breaks” and “vacations.” Google co-founder Sergey Brin recently longed for a return to 60-hour work weeks, which he sees as the productivity “sweet spot.”

Brin might get his wish if AI systems prove as useful as tech enthusiasts expect. But for the moment, demand for human workers still exceeds the available supply.

In Japan, which is a few years ahead on the demographic curve, young workers are hiring “resignation agencies” (taishoku daikou) to inform their bosses the terms of employment are no longer acceptable.

hat’s quite a change for a culture famously devoted to hard work, but it’s really just supply and demand. The supply of any scarce good, including labor, eventually flows to wherever it gets the best terms.

US employers who were quick to shed workers in 2020 have tried to avoid mass layoffs. They learned the costs of finding, hiring, and training new workers during a labor shortage can quickly exceed the “savings” of firing people in a recession. Now the sensible ones find other ways to reduce payroll costs.

If that’s how businesses respond to the DOGE/tariff shock, it may not reach the point of “recession.” Workers may have less spending power, companies may see their earnings drop, but it won’t be as bad as 2008 or 2020.

There are more negative scenarios, though.

Inflation hasn’t gone away, and the trade war could make it worse. Combine that with lower growth and we could be looking at 1970s-style “stagflation.”

Ask anyone who lived through that era; they’ll tell you how miserable it was.

No Checks

The bigger risk is that no one can be sure where government policy is going.

As I wrote before the election, presidents have tremendous power to impose tariffs. Trump is using every bit of that power in unpredictable ways. Maybe he has some grand plan that will make the chaos worthwhile. But if so, it’s not apparent to anyone else.

The authority Trump has given Elon Musk to slash federal spending is equally sweeping. And again, we don’t know how he will use it.

Moreover, there are no checks on this power.

In the first Trump term, more conventional Republicans like Mike Pence, Paul Ryan, Mitch McConnell, and others had a moderating influence. Those guardrails are all gone now.

This time around, the Republican majorities in Congress are giving Trump everything he wants. Courts, financial markets, and public opinion aren’t slowing him down, either. Democratic opposition has been hapless at best.

So as a practical matter, Trump will do whatever Trump wants, and none of us know what that is. Trump himself may not know. He seems to change his mind a lot.

Given the wide range of choices Trump could make, the prudent response is to delay big decisions and wait for more “clarity.” Jerome Powell says that’s what the Fed is doing.

Unfortunately, Trump doesn’t do clarity. He likes to keep everyone guessing.

Trump’s method served him well in the business world. Maybe he’ll make it work for his second presidency, too.

Or maybe not. Meanwhile, the waiting has costs.

*Patrick Watson is senior economic analyst at Mauldin Economics. This article is from a Mauldin Economics series called Connecting the Dots. It first appeared here, and is used by interest.co.nz with permission.

17 Comments

The World is soon going to beg Trump..'Please make up your mind once for all and impose 30% tariffs on all imports into America from anywhere in the world. We shall plan our businesses accordingly. This repeated flip flop is worse'.

This is one of the best article I've read on these topics. Absolutely nailed it. Unemployment and, more importantly, the 'fear of unemployment' have a much bigger impact than most economists realize.

I believe this is exactly what happened last year in NZ after the May 2024 budget delivered job and spending cuts. Nearly every NZ economist was surprised by the un-expected drop in economic indicators by the end of the year - even though they got their unemployment forecasts spot on. What they didn't forecast was the 'fear of unemployment' and what that does to overall spending and demand in the economy.

If someone loses their job that impacts everyone in their social group - who all start to second guess their own confidence in having a future income.

A NZ based economist comfortable to include 'fiscal policy' in an article about economics. That is exceedingly rare.

NZ?

But economists - wherever they are based - fly totally blind.

Sorry, but they don't count resource stocks, sinks or entropy. They only look backwards - on which basis you will live forever because you ain't dead yet. Not much use as a basis for forward projecting, eh?

Trump is a symptom, not a cause. Ask what the cause was?

You make a good point - there are so many details about how the economy works that are never talked about or acknowledged. The one that blows my mind and completely confuses people is the operations of a 'fiat currency monetary system' - governments 'create and spend money' before they tax it. Which means 'tax revenue does not pay for government spending'.

Elon Musk and DOGE have actually discovered this real world operation on computers at the US Treasury and are completely freaked out by it.

Elon Musk and DOGE have actually discovered this real world operation on computers at the US Treasury and are completely freaked out by it.

DOGE are not freaked out that this function exists, they were well aware of the US National Debt prior to finding these machines. What surprises and makes this a big deal is that these machines have existed within the Executive Branch and were not governed by the budgets enacted by the Legislative Branch. This means the Executive Branch has been delegated power to set expenditure years ago and everything DOGE is doing now is merely a continuation of this pre-existing structure - albeit that they are now creating much less money.

Whether Musk was unaware or not is irrelevant...his goal is the capture of all resources to the oligarchs...aka the end of government.

Patrick is not a New Zealander FYI. He's American.

My apologies to Patrick for that assumption. Although, I could probably extend the same statement to US economists as well.

Google co-founder Sergey Brin recently longed for a return to 60-hour work weeks, which he sees as the productivity “sweet spot.”

Surely the "sweet spot" is a 40-hour work week as the employment contract where employees are interested and motivated enough by the work they do, to work 60+ hours without compulsion. To make it work, one has to be able to give employees access to the work system remotely and/or after (normal) business hours.

And that comes down to incentives. If the incentives for outstanding performance and productivity are good enough, people put effort in above and beyond. But the company has to pay handsomely for that performance. The key is in getting the incentives right, such that with every outgoing dollar paid as an incentive, the businesses bottom line improves a bit more than double the dollar amount paid out to get there.

I found the1/3rd to 2/3rds ratio was my "sweet spot" when drawing up incentive schemes.

According to JM Keynes our sweet spot should currently be around 15 hrs per week....but then we misallocated the benefits of increased productivity.

v/interesting - I did not know that was said by him. Yes, what he did not know is that with the introduction of technology we used it as a means to downsize the human capital costs, as opposed to make the existing workers more productive - i.e., being able to get a greater throughput from your existing staff.

If I recall correctly, Marx's labor theory of value posited that under a capitalist economy, an improved bottom line would always be achieved at the expense of labor.

"Yes, what he did not know is that with the introduction of technology we used it as a means to downsize the human capital costs, as opposed to make the existing workers more productive - i.e., being able to get a greater throughput from your existing staff."

All capital cost IS labour...nothing happens without work...that is why energy is critical....it is a work multiplier.

To repeat a quote that pdk pointed out to me;

“Capital without energy is a statue; labour without energy is a corpse.”

Steve Keen, 2019

It's a favourite of mine these days too!

CAPTAIN CHAO$ - cause or symptom?

The opening sentence is a mystery to me, given that Mr Watson is a co-founder and senior economic analyst at Mauldin Economics.... "Just three months ago, a US recession seemed unlikely. The economy was humming along by most measures..."

So what measures were these? - and how does this opening statement sit with their mission statement, quoted from their website...

"From the Financial Crisis of 2008, to the Covid crash and subsequent run up, rampant inflation, geopolitical turmoil... the decade-long run of the FAANG trade, and more…

Mauldin Economics has served self-directed investors with institutional grade research you can rely on to make smarter, more timely portfolio decisions and grow your wealth responsibly over time."

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Trump (AKA Captain Chao$) was in wrecking mode long before he declared a tariff/trade war on the entire planet.

Indeed the US casino was an increasingly fragile house of cards - the enormous paper band-aids the Fed and the Treasury applied to cover up the fact that the entire U$ financial system was nothing more than a constitutionally illegal casino. This was all designed to transfer wealth from Mainstreet and the real economy, into the parasitic rentier' FIRE economy.

After 112 years the model is broken. As dreadful and incompetent as Trump is - Chris Hedges said it best - "TRUMP IS NOT THE DISEASE - HE IS THE SYMPTOM VOMITED UP OUT OF THE MORASS"

I GOT A SHOCK WHEN I CRUNCHED SOME NUMBERS RECENTLY

The figures don’t lie – there they are on the Fred chart – go into the St Louis FRED site and check for yourself ... https://fred.stlouisfed.org/series/WALCL

During the 12 years of Obama and Biden's undisputed bungling of the U$ economy, the Fed balance sheet grew by a total of $1.8 trillion – that’s + $2.4T under Obama’s 2 terms whilst during Biden’s term it was a negative -$600 billion (due to QT)

Working this out on a yearly basis under Trump, the growth was $750 billion per year, and under the other two it was a mere $15 billion per year.

Under Trump, the balance sheet growth per year worked out at exactly 50x that of the other two bunglers.

With Trump just raising the debt ceiling by a whopping $4 trillion, it’s pretty obvious that he is laying the groundwork to be an even more reckless spender than in his initial debacle.

Trump was personally bailed out of bankruptcy on at least 6 occasions by the very banks that are his handlers to this day – when it comes to bankruptcy, he has a proven track record – this is not going to end well.

WHY IS THE WORD TARIFF HIS "BESTEST" WORD IN THE ENGLISH LANGUAGE?

Well maybe the key reasons is that tariffs are the only tax collected which goes directly into the Treasury Account - IOW there is scant congressional oversight on how he spends this revenue.

The executive, ie, the #47 admin, and their favoured bureaucrats, can blow this pretty much however they like without seeking congressional approval.

Remember he has such an uncomfortably narrow majority and enemies within his own party (so much for the famed "landslide victory) - out of 435, the Republicans only hold 218 seats vs 213 seats - IOW the more revenue he can funnel directly into the Treasury coffers the more freedom he has.

IT WAS ALL SET TO BLOW ANYWAY

If we cast our minds back to September 2019 when none of us had even heard of Covid, the repo market blew up for a number of reasons, including the fact that no banks trusted one another's collateral any longer.

A measure of the interest rate on overnight repos in the United States, the Secured Overnight Financing Rate (SOFR), increased from 2.43 percent on September 16 to 5.25 percent on September 17. During the trading day, interest rates reached as high as 10 percent.

The New York Fed stepped in and injected $75 billion on Sept 17, and subsequently had to run to the rescue with trillions of dollars in cumulative loans that went on for months.

Nomura was heavily exposed to derivatives; Deutsche Bank, a major counter-party to the derivatives of Wall Street’s megabanks, was in a death spiral; and $2.7 billion in credit default swaps blew up the very day before the Fed launched its repo bailout.

This was not a “broad base” of the U.S. financial system being bailed out - 62% of a cumulative $19.87 trillion in rolled-over repo loans went to just six trading houses: Nomura Securities International ($3.7 trillion); J.P. Morgan Securities ($2.59 trillion); Goldman Sachs ($1.67 trillion); Barclays Capital ($1.48 trillion); Citigroup Global Markets ($1.43 trillion); and Deutsche Bank Securities ($1.39 trillion).

AND GUESS WHO NOMURA IS? - oh, that'll be Japan's largest investment bank.

In October 2008, Nomura acquired most of Lehman Brothers' Asian operations for pennies on the pound when they went belly up. It was one of the world's largest investment banks with £138 billion in assets under management at the time. In April 2009, their global headquarters for investment banking was moved out of Tokyo to London, as part of a strategy to move the company's focus from Japan to global markets.

The contagion had to be stopped, hence the massive support from the Fed.

Quoted from WSOP...

"Imagine if you were the Federal Reserve and had been thoroughly disgraced by waging more than a two-year court battle to prevent the press in America from doing its job and publishing the granular details of the Fed’s 2007 to 2010 bailout of Wall Street and its foreign bank derivative counterparties.

Then the Fed was further disgraced after losing the court battles when in 2011 the details of the $29 trillion bailout were published. Chances are that the Fed would not be anxious to let the public or Congress hear the latest details of bailing out hedge funds for the 1% that were using leverage of 50 to 1 obtained from the very banks the Fed is supposed to be supervising.

That background might also help to explain why the Treasury Department’s Office of Financial Research (OFR) wrote a research paper attempting to shift hedge fund turmoil in the Treasury futures market to March of 2020 – after the onset of the COVID-19 pandemic in the U.S. – but slipped up and included two graphs that move the onset of the turmoil to smack dab in September of 2019."

SO WHAT ARE THESE "MEASURES" THEN?

Just me, but I can't think of one single "measure" that doesn't suggest that the U$ economy, and by definition its currency was already in terminal decline. This was made even more imminent when they chose to weaponise their reserve currency status and as such to seriously compromise their ability to endlessly sell their debt.

You have to hand it to the Fed, along with the able support of the Treasury - they have succeeded in reducing the purchasing power of the dollar by 99.31% from what it was in the early 1970s. They are only outdone by the UK - they have got the £ down to 1/550th of its purchasing power.

I couldn't bring myself to crunch the numbers on the Kiwi dollar's purchasing power - far too depressing.

BTW my calculations are based on the one reliable and constant measure of goods and services that has remained stable for some 5000 years (physical gold). It is a complete waste of time to use any analysis based on fiat tokens because they are all completely meaningless as a yardstick.

CONCLUSION

It seems that the author missed these shockers too...

#1 U$ household debt of $18 trillion.

#2 Government, business and consumer debt combined, is now well over 100 trillion dollars.

#3 More than 100 million U.S. adults that do not have jobs are considered to be “not in the labour force”. During the 2008 GFC, this number never exceeded 100 million.

I could go on all night and trip the word counter limit - simply put, the U$ is in a debt death spiral along with most of the other Western-centric economies. It seems that Mauldin Economics has fallen for the same old eCONomics mysticism which completely ignores how 'money' is created.

Do they also choose to ignore the fundamental difference between real money and credit? - which is the primary reason why, particularly since 1971, the debt/credit bubble has spiralled completely out of control and we are now poised on the edge of a financial meltdown

Regards to all

Col

Thanks Colin - that is a lengthy critique and might be overlooked by some readers due to it's length. I thought the article was an excellent and rounded analysis of the US economy as it stands now. Economics is a predictive practice (I was going to use the word 'science' but I don't think economics qualifies) and that will never be perfect.

All good, Keynes - I hear you.

It's just such a huge subject, the roots of which date back more than a century - so very difficult to tackle with piecemeal comments.

I was late posting too, as I had a problem logging in to contribute.

This escalating global tariff/trade war, on top of everything else, will affect every country on the planet.

I figured it was my duty to put my spoke in too - especially if it might help readers to understand where some of the motivation is coming from when so much of this debacle makes zero sense on any practical level.

Regards

Col

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.