Well, it should be better this time.

But then again it was pretty dire last time, so virtually anything is going to be an improvement. Still, onwards and upwards.

It's the economy. And time to have a look at how our GDP fared in the December quarter before consigning the troubled 2024 to history. The figures will be released on Thursday, March 20.

Last year we saw the full impact of the higher interest rates prompted by the Reserve Bank (RBNZ) after it hiked the Official Cash Rate (OCR) all the way from 0.25% up to the 5.5% as it sought to rein in inflation that peaked at 7.3% in mid-2022.

It has worked. Annual Consumer Prices Index (CPI) inflation as of the December 2024 quarter was 2.2%, well within the targeted 1% to 3% range. But the economy has been left bruised, sore, and sorry, in the process. Unemployment's risen from a low point of just 3.2% in 2022 to 5.1% as at the end of 2024.

The economy is widely expected to have grown in the December quarter, but probably by a fairly modest amount. After what we've gone through recently, however, even a 'modest' recovery will be welcomed.

The September quarter figures, released just before Christmas were traumatic. They painted a picture of the economy having its worst six-month period - barring Covid disruptions - since 1991.

The background to the release of the September quarter GDP figures (which was on December 19) is that Statistics New Zealand updates its GDP figures every October with the incorporation of annual data. It says this procedure is in line with international best practice.

Now, this new information always tends to have some impact on previously released quarterly figures - as the more accurate annual information changes the picture once it is added in.

This time, however, the impact of the new information was dramatic. The upshot was that although where the economy finished up at the end of the September quarter was not very different to what was believed previously, the way it got there was very different indeed. The destination was similar, the route to get there was very bumpy.

In short, up to the second quarter of last year, the economy had been performing better than previously thought - but then it fell off a cliff in the June and September quarters.

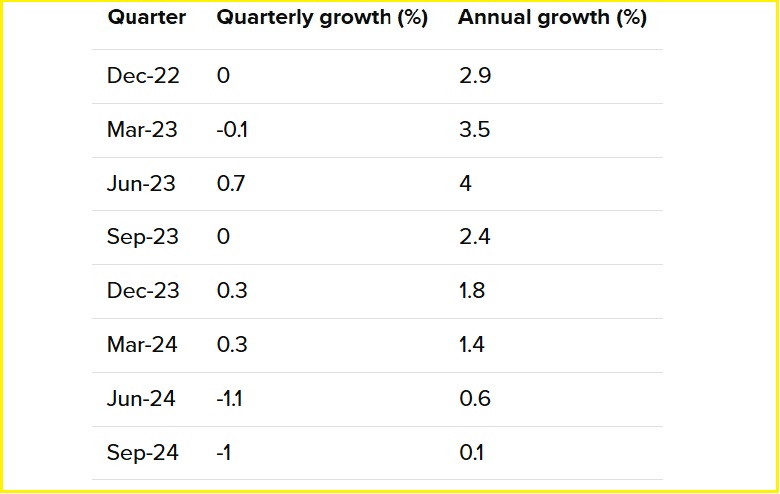

To give some concrete evidence of all this, here's a 'before and after' - showing the recent GDP quarterly figures as recorded by Stats NZ at the time the June quarter figures were released, followed by how the revised figures came out upon release of the September quarter figures.

So here's the 'before' as released by Stats NZ on September 19, 2024 - what we thought the economy had been doing:

And here's the 'after', as released on December 19, showing all the revised figures plus the newly presented September quarter figures:

The big change was that basically all previous indications of a recession had been wiped - but then in June-September we got a beauty. Never mind this 'technical' recession lark, this one was the real deal.

While I guess there's plenty of room for feeling uncomfortable about having official data that changes so much, the way the GDP figures are shown now squares more convincingly with what certainly I thought I saw around me in the middle of last year - IE an economy falling off the cliff.

If your economy's at the bottom of a cliff, you need an ambulance. And that of course was sent on its way from August onwards as the RBNZ began to cut the Official Cash Rate OCR from the cycle high of 5.5%. It's now at 3.75% and with 25-point cuts expected at each of the next two RBNZ OCR reviews, will likely be on 3.25% by the end of May.

The wave of lower interest rates as the OCR comes down has certainly perked up the mood, with business and consumer surveys showing large upticks in confidence.

However, we need to see more tangible evidence that the improved confidence is translating into increased investment and spend. There's signs, but they are still fairly tentative.

No doubt though that some of the 'partial indicators', economic data put out prior to the release of the December quarter GDP figures, have shown an improvement.

Here's some of the key stuff:

Retail sales volumes rose on a seasonally adjusted basis by 0.9% in the December quarter after two successive quarters of falls. The total value of actual retail sales was $33 billion, up 0.2% ($60 million), compared with the December 2023 quarter. These results were better than expected.

The volume of building work put in place fell on a seasonally adjusted basis in the December quarter by 4.4%, with a 4.9% drop in residential work (hitting its lowest activity level in four years) and a 3.1% fall in non-residential. These falls were somewhat worse than expected.

The volume of total manufacturing sales rose 1.1% on a seasonally-adjusted basis, following a revised 0.9% fall (was 1.2% fall) in the September 2024 quarter, while wholesale trade sales had a seasonally-adjusted gain of 0.3% in the December quarter compared with a 1.2% fall for the September quarter.

Overall, that's reasonably encouraging if not exactly hot stuff. Retail and manufacturing particularly have been doing it tough, so, some signs of lifting - albeit off a low base - are welcome. Construction was of course booming, and then it wasn't. Economists have for some time been seeing the bottom of the construction cycle coming - but these latest figures would tend to suggest we ain't there yet.

The RBNZ in its February Monetary Policy Statement forecast that GDP will have grown 0.3% in the December quarter. And it has forecast 0.6% in the March quarter we're currently in.

I didn't have all the major bank economists' GDP previews in front of me at time of writing this, but had seen forecasts from economists ranging from growth of 0.2% to 0.5% for the December quarter. So, growth - but nothing to get excited about at this stage.

I'll finish with some quotes from one of the previews I had seen.

ANZ economist Henry Russell and chief economist Sharon Zollner (forecasting 0.4% growth for the quarter) note that the economy "is climbing out of a deep hole".

"The RBNZ will certainly want to see evidence that a recovery is underway, and while we expect the Q4 GDP data will confirm that, there’s a wide range of uncertainty surrounding our forecast, in both directions," they say.

"In the case that the recovery is not evident to the extent that we and the RBNZ expect, it’s worth noting that these data cover a period that ended nearly three months ago. It will take time for the full impacts of lower interest rates to be felt, but high-frequency indicators suggest momentum is indeed building."

*This article was first published in our email for paying subscribers first thing Friday morning. See here for more details and how to subscribe.

5 Comments

I saw that the ANZ Truckometer moved a touch on the upside. ANZ have been ok at GDP calls lately.

Ironically, the heading included 'gears'. Which of course, stationary trucks posess as many gears as moving ones. It isn't the gear-count which matters; it's the amount of work being done (they merely transmit energy).

In that sense, the truckometer is indeed accurate, and a fair representation.

But not a foretelling of the future...

Not sure why cuts in the ocr perk up the mood! These rate drops reflect how bad things are. Trouble ahead.

Anyone (especially bank economists) should be treated with great scepticism when the making 'confident' predictions in a world that is as volatile as it has been in living memory.

Of course one can never account for the 'power of positive projection'....I guess that may be a factor they hope for.

I suspect it will be flat... for the next 2-3 releases. We certainly won't be getting back to where we were a year and a half ago IMO. We are in a self induced austerity doom loop. Tax receipts look worse and worse every time they come out, leading to government cuts, leading to worse tax receipts...

But you know, Nicola's got this "cos running a country like running a household" and previous experience of every other country that has done this for 30 years is irrelevant.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.