Economists are now forecasting higher household spending on the back of interest rate falls, but they have left their GDP forecasts virtually unchanged.

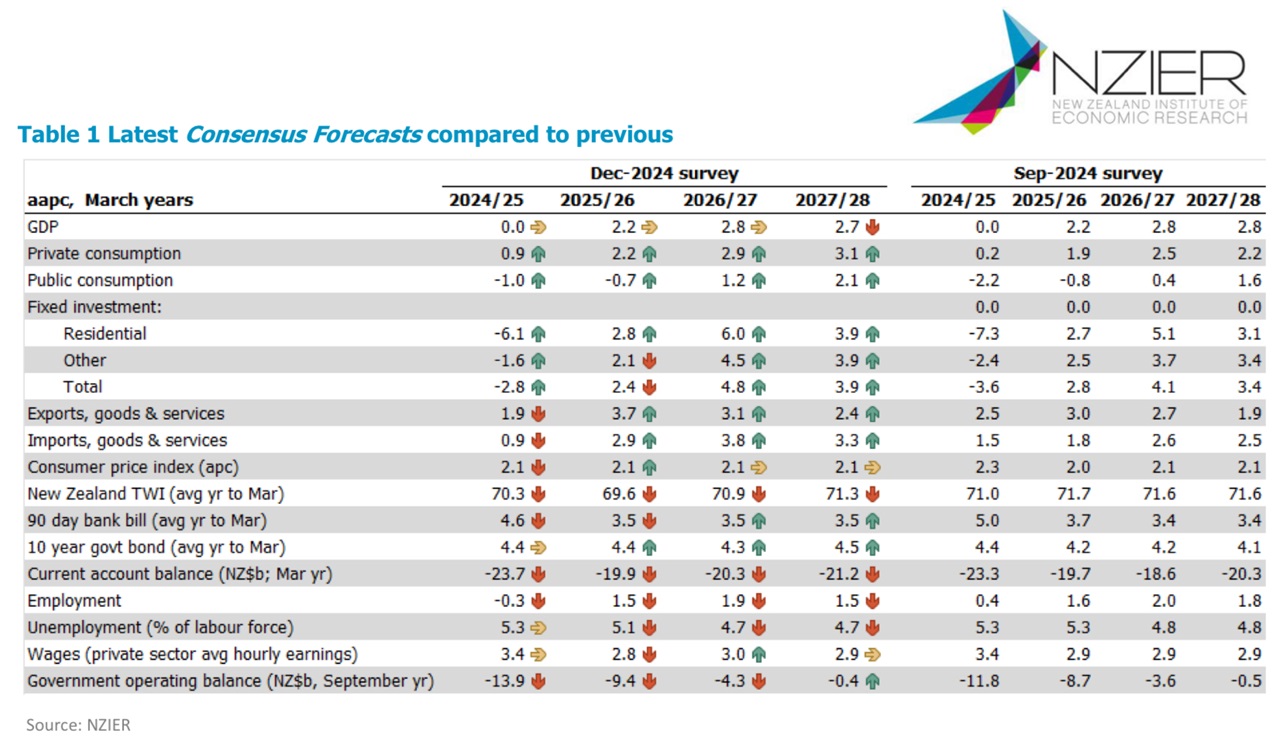

According to the NZ Institute of Economic Research's latest quarterly 'consensus' forecasts, there will be zero GDP growth in the year to March 2025 - and that's an unchanged forecast from the previous consensus release in September.

The economists' consensus forecasts come from the big five banks, the Reserve Bank (RBNZ), The Treasury and NZIER.

With much of the year already finished, it's perhaps not surprising the GDP forecast for the current year is unchanged. But also largely unchanged are the GDP picks for subsequent March years.

The pick for GDP growth in the March 2026 year is 2.2%, unchanged from the forecast made in September, the pick for March 2027 is unchanged at 2.8%, while the March 2028 consensus pick is actually slightly reduced at 2.7%, from 2.8% picked in September.

While the rapid-fire interest rate reductions that have been seen in the latter months of this year haven't convinced economists that GDP will fare any better - they do see household spending levels rising now.

Private consumption growth for the March 2025 year has been bumped up from an anaemic September forecast of just 0.2% to 0.9%.

For the March 2026 year private consumption growth is now forecast to be 2.2% versus 1.9% previously, while for March 2027 the forecast is 2.9% (2.5% previously) and for March 2028 it's 3.1% (2.2%).

NZIER senior economist Ting Huang said more households in recent months have been fixing their mortgages at shorter fixed terms in anticipation that interest rates will decrease.

"With over half of the New Zealand mortgage book due for repricing within the coming six months, many households will roll onto lower mortgage rates and face reduced mortgage repayments.

"This, along with the income tax cuts, is expected to support a recovery in discretionary household spending over the coming years."

Huang said that, similarly, the residential investment growth outlook has been revised higher, reflecting the expectations that lower interest rates should support a recovery in residential investment over the coming years.

The consensus pick for residential investment in the current year to March 2025 is -6.1%, an improvement on the September forecast of -7.3%.

Positive growth is expected to resume in the year to March 2026, with a 2.8% lift (2.7% previous pick) and then in March 2027 the consensus pick is 6.0% (5.1% previously) and 3.9% in March 2028 (3.1% previously).

Huang notes that the consensus GDP forecasts "reflect the expectations that activity in the New Zealand economy will remain soft in the near term".

"BusinessNZ’s PMI and PSI measures of manufacturing and services sector performance and NZIER’s Quarterly Survey of Business Opinion measure of firms’ domestic trading activity also point to continued weak activity in the economy. Beyond 2025, lower interest rates are expected to drive a pick-up in growth."

Huang says the export growth outlook for the years beyond 2025 has been revised higher.

"This reflects the expectations that the continued strengthening in commodity prices, especially dairy, and the constrained global supply of food commodities should underpin New Zealand’s export growth over the coming years.

"Although the new US Government’s trade policy setting may present a downside risk to New Zealand’s export demand, this may be offset by the potential recovery in China’s demand with its new economic stimulus package in place," she says.

21 Comments

Perhaps ask someone about the physical underwrite?

These folk are tea-leaf-readers.

Cheers

Or the billions of dollars the big banks and corporations siphon offshore every quarter bleeding us dry.

"Huang says the export growth outlook for the years beyond 2025 has been revised higher.

"This reflects the expectations that the continued strengthening in commodity prices, especially dairy, and the constrained global supply of food commodities should underpin New Zealand’s export growth over the coming years."

So a falling NZD or commodity prices continuing a steep increase or a combination of the two. Production has been flat for a decade, indicating volume output has plateaued.

If, and it is a big if given the global growth prospects, prices in NZD for commodities do extend what then of imports and domestic consumption?

Its not as if we are running a trade surplus in case nobody noticed.

So the $64,000 question is ... Will per capita GDP rise?

Or will all the benefits of this anemic growth flow to the top?

Means real gdp/ capita continues to fall as pop is increasing.

This govt is a disaster for NZ.

Should've kept up the deficit funded spending on the Wellington $1000/hour (+GST, +disbursements) consulting set like the last lot.

No. Shouldn't have been such stupid sheeple,voting for any of the parties in parliament and expect something different.

Indeed. Plenty of people are still convinced of the fundamental difference between blue label Pepsi and red label Coke.

Tis govt didn't open the floodgates for immigration, and until they address universal super, they will keep importing more workers to pay tax every week so it can somewhat be funded. Structural reform is needed.

Economists are now forecasting higher household spending on the back of interest rate falls, but they have left their GDP forecasts virtually unchanged.

OK. The first bit I understand. Lower debt servicing so more income is spent into the economy under the assumption that our economy is largely based around 2 personas: the paycheck-to-paycheck segment (who spend pretty much everything and wait until the next income transfer) and the drunken sailor segment.

But surely GDP must increase on the back of this spend, given that our GDP framework is largely built around private consumption.

GDP formula is consumption plus investment plus gov spending plus exports less imports....private consumption is but a part of the equation.

I know what it is. Do you disagree with what I said? Please outline why.

Pvte consumption accounts for approx 57.4% of New Zealand's nominal GDP.

https://www.ceicdata.com/en/indicator/new-zealand/private-consumption--…

Look at the equation and ask yourself if export receipts increase due to dollar movement or commodity prices there will be a greater negative impact from the greater volume of imports...in addition government spending is being reduced in relative terms which leaves investment to provide the required increase in consumption....where does that investment come from?

More borrowing in the private sector? or offshore investment into the NZ economy?....neither looking likely at this stage, especially when our major industry (dairy) has plateaued and RE is oversupplied and a risky looking bet.

Maybe some pension funds will front up with some instant infrastructure spend?...bugger we take years to even work out what we want and then cancel it half way through...you see the problem?

You skirted around what I pointed out.

I asked you what supports that consumption?

OK got it. To a large extent, greater private consumption has been driven by credit creation for non-productive purposes. My argument is that this is the path we have chosen for national wealth. Typically the 'have nots' have benefitted from the 'haves' rising asset prices thereby enabling them to borrow and spend more. It's a synergistic relationship. Nevertheless, when the 'have nots' cannot continue to spend, then you have issues. I directly addressed the contradictions what the bureaucrats seem to be saying.

Was not commenting on the path we have chosen, was simply questioning the projection based on reality. I agree the private credit fueled consumption appears to have hit the ceiling not least because the pool of credit worthy (middle class) is diminishing....it is a global problem.

Good. As you're probably aware, China is looking to pvte consumption as an economomic engine growth over public investment. As I was suggesting, it's the difficult to understand what the strategic intent of the ruling elite of Aotearoa is.

Im not sure they know themselves....other than being in power.

Great read. The Centrists on both sides are between a rock and a hard place. Both can't fully unleash themselves physically and mentally from Ponzinomics. That is consistent with my point.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.