Summary of key points: -

- Financial markets hold their “Rinse and Repeat” conviction on Trump policies

- Aussies now price for a February interest rate cut

Financial markets hold their “Rinse and Repeat” conviction on Trump policies

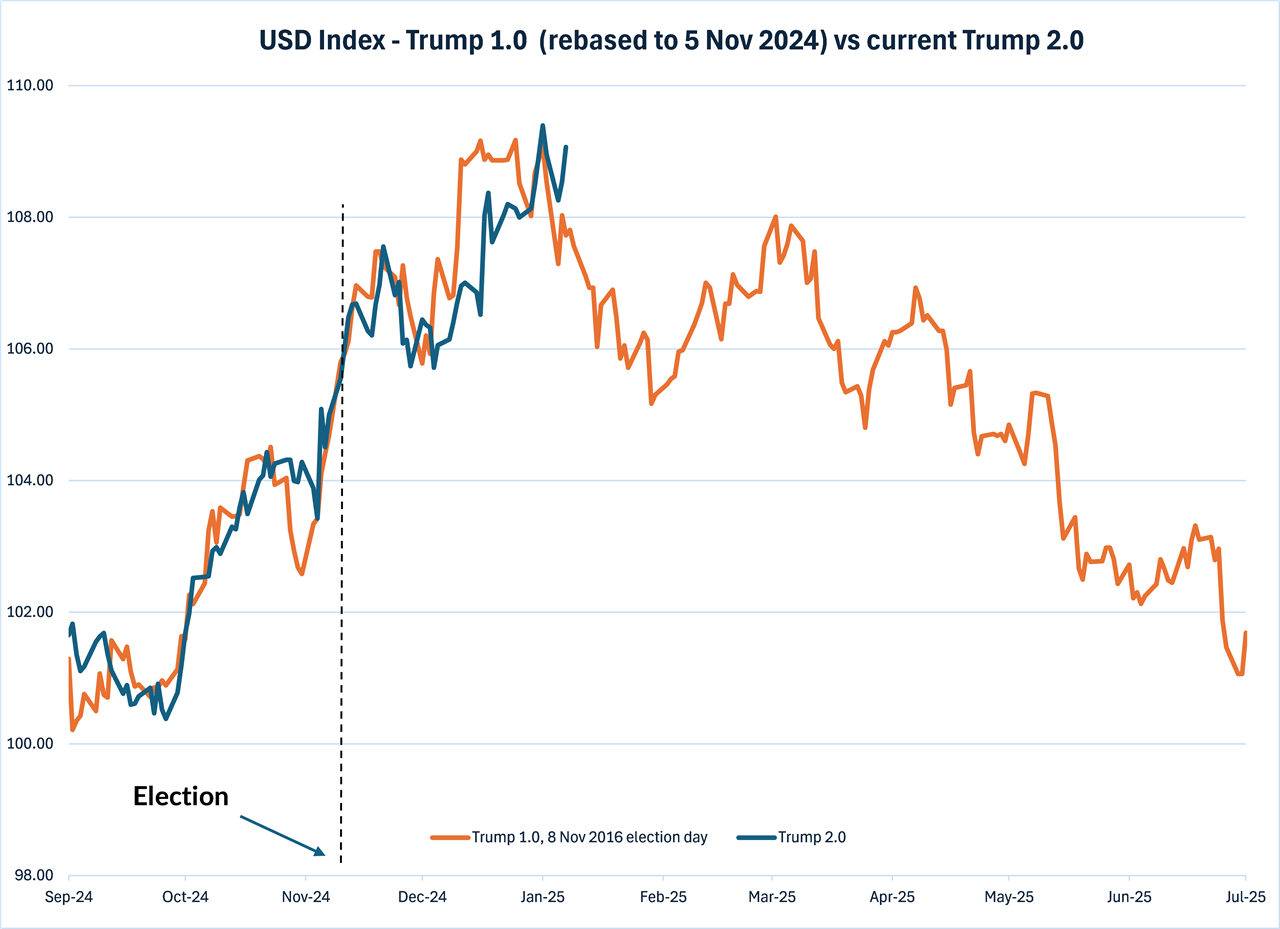

The appreciation of the US dollar on global foreign exchange markets since October last year on the back of Trump’s tariff intentions, perceived higher future inflation and the Fed winding back on their interest rate reductions this year, is proving to be an exact mirror of the initial USD appreciation when Donald Trump was first elected President in November 2016 (refer chart below). The Trump 2.0 “rinse and repeat” displayed by the FX markets is a remarkable action replay of the previous Trump 1.0 FX price action. According to the 2016/2017 script, the US dollar should now start to run out of steam, despite climbing to 109.50 on the Dixy Index following a stronger than expected Non-Farm Payrolls jobs result for December last Friday. We have not yet seen any catalyst in the form of weaker than expected US economic data to cause unwinding of the profitable Trump Trades (long USD, short-sold US 10-year Treasury Bonds). The US dollar has continued to appreciate, and the bonds sold off again to nine months highs of 4.76% on the employment news.

Back in January 2017, the US dollar did not appreciate any further once President Trump was sworn in. The currency markets progressively unwound all the previous USD gains, sending the USD Dixy Index down 8 points from 101.00 in January 2017 to below 93.00 by July 2017.

Are we once again on track for an eight point drop in the USD Index over the next six months as history eerily repeats?

Current financial market sentiment, positioning and commentary would not suggest that the US dollar is about to do an “about turn” and fall away over coming months. The markets are expecting (and have priced for) a “big bang” tariff announcement from Trump once he is elected, which is contrary to the more “layered” approach to tariff protection favoured by his Treasury Secretary, Scott Bessent. Donald Trump is often quoted as wanting lower US interest rates and a lower US dollar value to help US manufacturing exporters. Off course, his stated policy intention with tariffs causes the opposite impact. He will not be happy with the current trends of higher long-term interest rates in the US and the stronger US dollar currency value. Expect come social media ranting on this subject. Like all matters with Donald Trump, nothing adds up or is coherent. The “America First” protectionist and isolationist economic policies are polar opposite to his “Putin-like” imperialist expansion plans with Greenland and Panama. However, there is always more to Trump’s statements, it is likely that he is repaying his mining industry mates for financial support to his election campaign with the Greenland annexation intentions.

The financial markets and the Federal Reserve are both expecting US inflation to increase over 2024 due to tariffs and a robust economy.

However, two key upcoming pieces of economic data have the potential to upset the applecart in respect to the current market conviction.

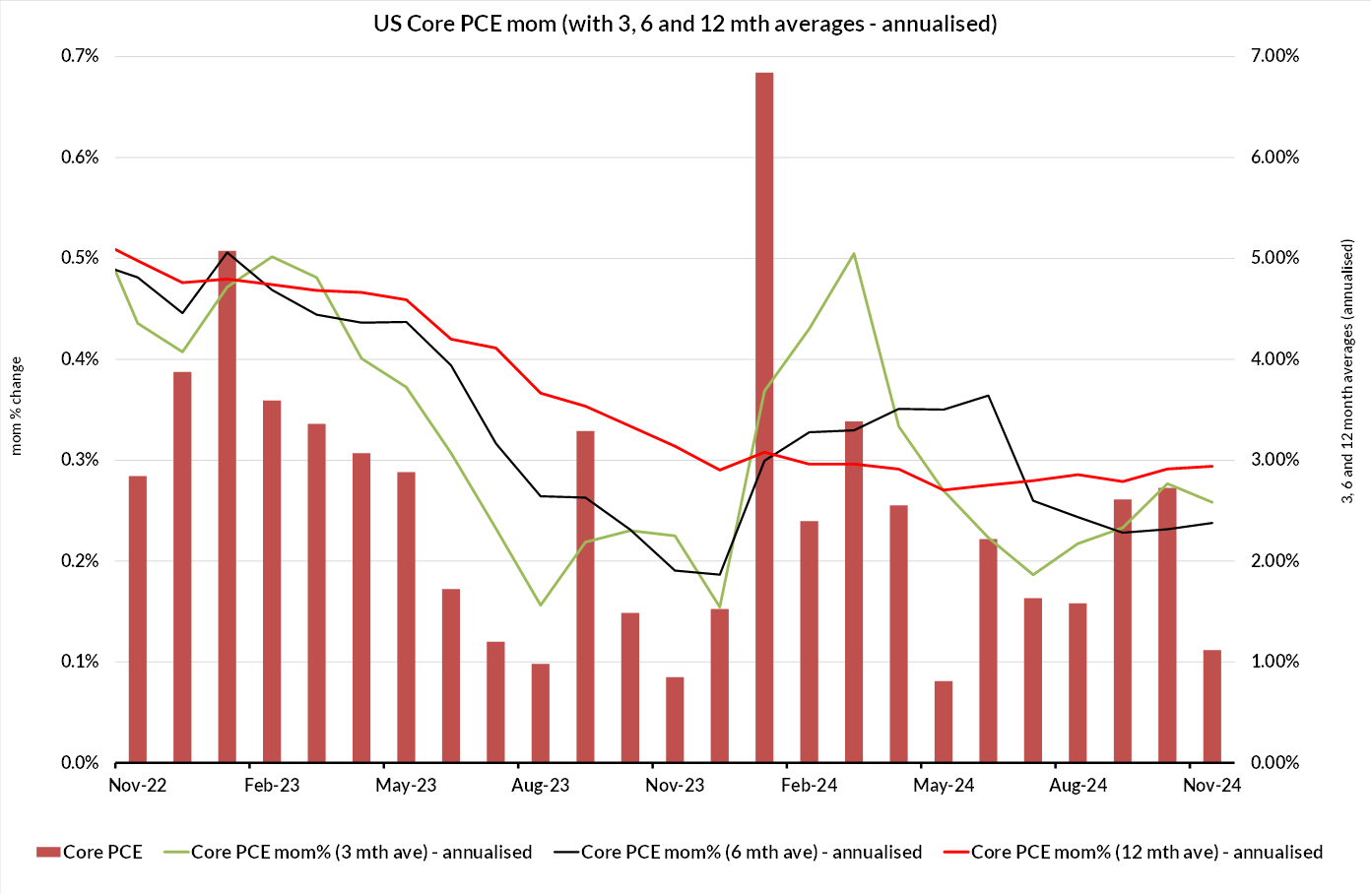

Core PCE Annual Inflation Rate to January 2025 (due for release 28 February 2025)

The FX market’s expectation that inflation will increase this year may be in for a nasty surprise when the extraordinarily high 0.70% increase in the core PCE measure in January 2024 rolls out of the annual rate calculation. Large increase last year in housing (rents) and health costs are not going to be repeated this year. The annual core inflation rate is likely to decrease from the current 2.80% level to 2.40%, or lower – which is the opposite to what the markets are currently anticipating.

More largescale historical revisions to the Non-Farm Payrolls (due for release 7 February 2025)

When the January employment data is released on 7 February, the US Bureau of Labour Statistics are expected to release significant downward revisions to the previously announced 2023 and 2024 monthly Non-Farm Payrolls numbers. The notoriously inaccurate monthly figures are surprisingly still the key focus for the financial markets in terms of being an accurate indicator of the strength of the economy and inflationary impacts from the labour market supply and demand (through wages trends). Back in August last year the Bureau of Labour Statistics revised down the job increases to March 2024 by 818,000. A second major revision is now due as part of their “annual benchmark revisions”

The markets also appear to have conveniently forgotten that Trump’s DOGE (“Department of Government Efficiency”) taskforce headed by Elon Musk and Vivek Ramaswamy is going to slash and burn costs (i.e. jobs) in US Federal Government agencies, institutions and departments in an attempt to secure US$1 trillion to US$2 trillion in spending reductions to reel in the budget deficit. As most of the increases in Non-Farm Payrolls jobs over the last two years have been in the Government sector (under Bidonomics policies), it is not rocket science to come to a conclusion that employment data will trend to the softer side this year (with or without the historical revisions!).

Should the two economic data releases discussed above evolve as expected (i.e. softer), the Federal Reserve members may be forced to once again to change their stance back to three of four 0.25% interest rate cuts this year, rather than the two cuts signalled from the 18 December Fed meeting. The US dollar would give up its recent gains under this scenario.

Aussies now price for a February interest rate cut

The Australian dollar remains under constant downwards pressure from the stronger USD and weaker Chinese Yuan exchange rates. The AUD/USD exchange rate has depreciated 11% since the 0.6900 level on 30 September 2024 to 0.6145 today. The weaker AUD has been the major factor behind the NZ dollar’s similar 12% depreciation form 0.6340 to the current 0.5560 rate over the same three- and half-month period. There continues to be no separate or independent investor or trader interest in the Kiwi dollar as our interest rates remain below those of the US. We simply follow the Aussie dollar movements in day-to-day FX market trading. Therefore, any assessment of future NZD/USD shifts from the current cyclically low levels has to be based on future developments with the Australian dollar.

Following last Wednesday’s Australian monthly CPI indicator outcome for the month of November, a number of Australian bank economists have once again adjusted their predictions to that the Reserve Bank of Australia (“RBA”) will now cut their OCR interest rate at their 18 February meeting.

Previously, the majority of forecasters were picking a May rate cut. The interest rate change was a little surprising as the annual inflation indicator increased from 2.10% in October to 2.30% in November. There will be a much more accurate gauge of Australian inflation trends when the official CPI figures are released for the December quarter on Wednesday 29 January. A 0.50% increase is expected for the quarter, lowering the annual rate of inflation from 2.80% to 2.20%. However, it should be remembered that Government subsidies on electricity prices are artificially reducing the annual inflation rate by 0.40%. The RBA exclude the electricity price subsidies in their deliberations, and they also focus on the “trimmed-mean” CPI number, which is still running at 3.50% per annum.

Should the December quarter’s inflation result be above RBA and market consensus forecasts and the December employment data on 16 January again be another strong increase (as was the trend all through 2024), then the February rate cut predictions may be forced to change once again. The Australian dollar might finally find some support with the potential above forecast inflation and jobs outcomes.

Whilst the domestic economic data may have a minor impact on the Aussie dollar, the dominating influence is still all things related to China. Recent Chinese economic data has printed on the softer side and long-term bond yields in China are tumbling (down from 2.60% to 1.60% over the last 12 months) as the economy enters a deflationary cycle similar to what Japan previously experienced. Negative economic news out of China is always bad news for the Aussie dollar as it is traded as a proxy for the Chinese economy. There is always speculation that the Chinese authorities will step in to assist the economy with large monetary and fiscal stimulus packages. The stimulus measures enacted through 2024 do not seem to have prompted Chinese households to spend more and save less so far. Households are still worried about falling property values.

It does seem that the Chinese Government has come to the point that they will need much larger fiscal policy injections into their economy. Watch this space over coming weeks on this front.

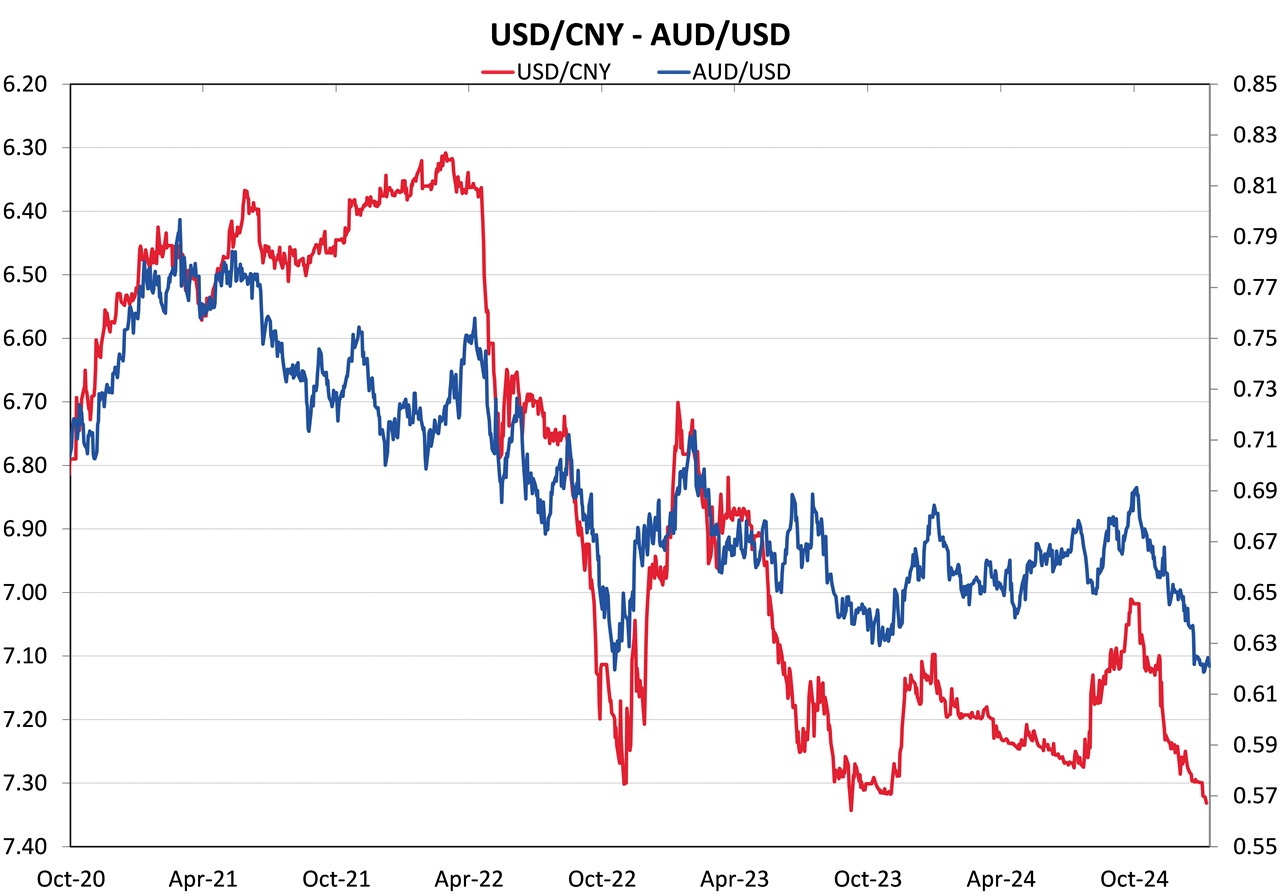

The Chinese central bank, the People’s Bank of China (“PBoC”) has been actively defending the Yuan from depreciating further and moving above the 7.3500 level against the USD. The Chinese Yuan has recovered from the 7.3500 level on three previous occasions since October 2022 (refer to the chart below), however the overall USD strength since October 2024 has it forced back to that level again. Upcoming Chinese economic data to look out for includes retail sales, industrial production and GDP growth numbers on Friday 17 January. The Aussie dollar remains closely correlated to the Yuan movements.

The timing of interest rate reductions in Australia could play a crucial role in their upcoming general election, which must be held before May 2025. The Albanese Labour Government is under pressure for causing a good part of their inflation problem (therefore elevated mortgage interest rates) through excessive State and Federal fiscal spending. Yet another change of Government in Australia back to the right of centre, Liberal/National Coalition would follow similar trends all around the world we are observing at this time. The US, Canada, New Zealand, France, Italy, Finland, Greece and several others have all moved to the right following voter dissatisfaction with the cost of living increases from the left of centre regimes in power through the Covid pandemic years. Federal elections in Germany are to be hold on 23 February (originally scheduled for September 2025) after the collapse of Chancellor Olaf Scholz’s three-party coalition government.

A change in political power in Australia back to the Liberals would be viewed as positive for the Australian dollar, however the dominance of the USD and Yuan movements over the AUD’s fortunes will still prevail.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

8 Comments

I am going to come back and have several more reads of this effort Roger. It has so much to digest and appreciate. No pun!

Thank you.

The U.S. dollar will continue to strengthen against other currencies, in my view, in 2025.

I expect to the NZ$ to revisit the past low of NZ$ buys US$0.48c.

It will continue to pay dividends to hold assets valued in US$.

The past low was a touch below 0.40

Yes, Frank - as you say, I too make the low at 0.3998 on October 9, 2000.

Notable highs were 0.8135 on March 10, 2008, which then crashed a monumental drop of 0.3139 down to 0.4996 on Feb 23, 2009.

The 2nd all-time high appears to be 0.8792 on June 25, 2011.

And the #1 high 0.8812 July 7, 2014.

Numbers from macrotrends.net

Cheers

Colin

A well written informative article. Thank you Roger.

Roger's prediction from 2 December article hasn't aged too well

The NZD/USD rate closely tracks the USD/JPY movements, so interest rate changes in Japan is another good reason why the Kiwi dollar is headed back above 0.6000 before Christmas. The Yen appears headed back to 140.00 again, which would see the NZD/USD exchange rate above 0.6200.

I find his bias against "the left' to cloud his analysis.

Thank you, IR.co and Roger Kerr - there is lots of meat in this sandwich...

...and not the least because of the completely new global financial territory where the U$ is losing its reserve currency status - also the fact that it will begin to lose its default currency status as well, as the true state of the economy and its currency is gradually revealed.

Note too that Indonesia just signed up to BRICS and the list of countries has become so long that they have had to suspend applications to enable them to process the prospective members. Just to add to the volatile mix Brazil (the 'B' in BRICS) is under attack by the Western financial/military hegemon that desperately wants to maintain its unipolar hold on humanity.

https://globalsouth.co/2025/01/13/brics-under-attack-in-brazil/

Some personal observations...

#1 The latest U$ job reports point to a FIRE (Financial, Insurance, Real Estate) based economy in continual decline with the latest employment data showing jobs in manufacturing and construction flat, with most of the growth in service, retail, and govt. employment. The UE data has to be taken with a sack of salt anyway given that multiple part-time jobs are lumped in, plus people no longer looking for jobs and as such are not included in the data either.

#2 Two months into the latest U$ fiscal year (beginning Oct 1, 2024) shows a $624 billion fiscal deficit, which could run out to anywhere from a $2 - $3.7 trillion deficit by fiscal year's end.

#3 Will DOGE be able to trim Federal spending to even match the negative offset in revenue received from a floundering economy? - I doubt this very much. This strategy has been estimated to knock out around $2 trillion in GDP, or around 7% - but they were calling for a 3% growth rate before this idea - this nets out to a dismal negative nominal 4%.

#4 There are huge unrealised losses not shown on the bank's balance sheets because they loaded up on Treasuries and mortgage-backed securities when rates were 1-2% and now with rates at 4-5% they are trading at under 1% (down to 70-80 cents on the dollar). They will mature at par - but this is a gut punch because real inflation is at least 10% meaning these assets are losing value at a compounding -9% annually.

#5 As I see it, Dah Fed has only two options - (how would you like to die?) -

(i) Fire up the printing press like crazy and KILL THE DOLLAR.

It's 99% gone anyway - why not go for broke - this is historically the choice that those in the hot seat make.

A very simple calculation is to look at the price of gold in 1971, just before the U$ went off the gold standard - a 40 oz bar of gold cost $11,000. Around the year 2000 it was up to around $100k, and today at say $2,600/oz it comes to ~ $1.1 million for the same bar.

That, as near as damn is to swearing, amounts to a loss of 99% of its purchasing power in 53 years. Incidentally, as I have mentioned on this forum before, the average lifespan of all fiat currencies in history is only 35 years - it appears that king-dollar is already 18 years overdue for the great fall off the wall.

(ii) Cut back on everything, tighten the screws and KILL THE ECONOMY even faster - normally not the option chosen as the politicians don't want the implosion on their watch.

#6 As I see it, the risk-weighted organic direction for global interest rates, regardless of what tricks dah Fed and other CBs try, is upwards. That said, I cannot see IRs reaching the 7-10% territory without the entire fiat casino coming down like a house of cards - let alone even remotely approaching the territory during the Paul Volker debacle when the prime rate peaked at a mind-numbing 21.5% in 1981.

A MAJOR CAVEAT FOR #6 - IR manipulation as a monetary tool is a complete crock anyway - it is a sleight of hand designed to thieve from the real economy and to continually transfer wealth to the rentier* sector.

*(The term “rentier” refers to an economic agent or individual who primarily earns income through interest, dividends, and other financial returns from investments, rather than from labour or entrepreneurial activities. This class of income is often termed “unearned income” since it does not arise directly from productive work or business endeavours.)

IR (Interest Rate) hikes are directly and immediately inflationary, just as hikes in energy prices are too. Indeed it is completely farcical to even suggest that they could ever be an inflationary control tool - they are the 180˚ polar opposite of what they are dressed up as.

Historically, with the incorporation of the constitutionally illegal U$ Federal Reserve model, it became the precursor for the central planners to expand their theft from Mainstreet on a grand scale - all the while, the key private banking baron culprits remained ensconced behind the scenes as the puppet masters, busily tugging on the strings, and aided by all manner of smoke and mirrors.

The Fed is one of three 100% privately owned banks on the planet - the other two being Italy and South Africa. A private cartel monopoly ownership is the perfect model to enable the theft of a nation's wealth by a tiny group of plutocrats - as the trite saying goes - "the easiest way to rob a bank is to own it" - also, being their own in-house regulators, plus not being audited since 1953, makes this about as easy as stealing candy from a baby in a pram.

This coup was all about centralising money creation, but it was sold to Congress on the basis of the Fed being the mechanism that could step in and save banks in the event of a run on deposits. They did exactly the opposite, and in the 1930s, as a direct result of the pump-and-dump debacle that they themselves had orchestrated, there was a huge attrition of small banks, and of course, along with them the liquidity they provided for the real economy, and especially the rural sector.

The Fed sat on their hands and let these banks go under, whilst their biggest member banks gobbled them up for a pittance, and the depositors (read unsecured creditors) lost all their money. Worse still, the farmers were made to repay their loans to the big banks or forfeit their farms. This in turn, led to a massive plummet in agricultural production and abject starvation for much of the vulnerable sectors of the economy.

This was a huge coordinated land grab - precisely what they are gearing up for right now - the DTCC, and Cede & Co. wait in the wings like vultures hovering overhead for the next big land grab.

"The Great Taking", a very concise free PDF (in the link below), explains what they have in store for those of us who fancy that we own paper assets and mortgaged real estate.

WE DON'T - we are the last in line unsecured creditors - how is that going to pan out when the total nominal value of derivatives is between $2.5 - $3.7 quadrillion. In fact, we are merely discretionary beneficiaries in a giant shadowy trust set up without our knowledge - the 'T' in the DTCC acronym gives that away - it designates the word 'Trust'.

'Cede' means to surrender possession - TPTB love to taunt us with word games and labels on one hand, as they thieve from us with the other.

https://thegreattaking.com/read-online-or-download

Back to the global derivative debacle - IOWs it is 26 - 40 times the annual global nominal GDP. What makes this even worse is the fact that a huge chunk of the nominal GDP figure should never have been included in the calculation in the first place.

National income accounting (GDP tripe) harks back to the late 1600s when a couple of Dutch bankers ran the numbers in time for the launch of the Bank of England in 1694, and to try to arrive at a figure where govt. debt obligations could be reconciled accordingly - the system appears to be some 330 years out of date - time for an update perhaps?

Some of the individual bank's derivative books are outrageous too - from memory, Goldman Sachs about a year ago was roughly 1200:1 (Derivatives:Equity) - with Citigroup (the largest shareholder at over 40% of the New York Fed), a whopping 330:1.

#7 The more banking is centralised and the local community banks are restricted by regulation, the more money creation flows into asset portfolios - IOW existing assets, rather than Mainstreet's entrepreneurial sector, which is the engine of activities and sustainable societal wealth. Generally, within the status quo financial system, banks are in effect penalised if they lend for productive business purposes - this involves following the Basel, (Swiss-based) BIS (Bank for International Settlements) - NZ is one of the 62 member-bank affiliates.

As I have said before ~97% of money is created by these banks (NZ has a pitifully small number of banking entities) and is devoid of any window guidance whatsoever as to where the available liquidity is placed.

When banks lend there are 3 main scenarios...

(i) When this money is used for consumption it naturally leads to consumer price inflation because it adds to the money supply, but not to the supply of goods and services - more demand chases the same fixed supply of G & S (Goods and Services).

(ii) When this money is used for financial and asset purchases it leads to asset price inflation, with extreme examples like the Japan property bubble of the 1980s that ended up bursting spectacularly and only very recently regained the market cap ground that it had lost 30-something years earlier.

(iii) If banks conduct adequate due diligence in their lending for productive purposes, this by definition creates more G & S, creating sustainable income flows for the borrower to both service and repay the loans.

In an economy that has many banks, that are also backed up by non-banks making loans for productive purposes, then economies could be looking at sustainable real growth of 10-20% as opposed to low single-digit growth or even negative nominal growth, let alone growth that is inflation adjusted.

= LEADING TO MINIMAL CPI INFLATION OR ASSET PRICE INFLATION

Case in point - the EU - the ECB has killed off some 5000 banking entities in the last 20 years. However, the appointed (read unelected) financial European Commission executive, shills for the global financial plutocracy, and this situation can never be addressed without massive fundamental political reform.

Conversely, under the U$ Federation's Governance System, where individual states have constitutional monetary and fiscal policy autonomy, with a modicum of common sense this can be readily achieved.

In fact, from small beginnings with just one solitary, but spectacularly successful model - the 105-year-old Bank of North Dakota, we now see ~35 states moving towards implementing sound money, state depositories and Public Banking Solutions (PBS), so that they can begin to protect their locally generated wealth, and insulate themselves from the profligate federal financial casino.

With this number of states wanting to insulate themselves from the suicidal Federal govt's. 'policies' it kind of beggars belief that any Canadian, with more than half a brain, would even entertain the idea of their resource-rich country becoming the 51st U$ state.

I wonder (sarc) if the sales package includes the disclosure that the average U$ taxpaying citizen, when you include unfunded liabilities, has a total debt burden of between $1 and $2 million dollars? On the contrary, many U$ states are talking more and more openly about secession.

IN THE YEAR 2025

The only certainty for me in 2025 predictions is that the year will be a hats-off wild ride - barely two weeks in and the geopolitical uncertainties compound on a daily basis, to the stage where it is very difficult to keep up. For the life of me, I cannot see us getting to the end of 2025 without a systemic financial meltdown.

Both the EU and NATO are now toast, particularly with Germany being rendered an uncompetitive industrial cot-case by its occupier - the one that also severed its energy umbilical cord from Russia. Theoretically, if the population can lift itself out of its current terminal case of Stockholm Syndrome, vote in a government that is devoid of an economic death wish, and begin looking East and South, not West, there might be a faint chance of some degree of modest recovery, otherwise, IMO Germany is gone for all money.

The two next biggest EU economies are France and Italy and they have monumental financial challenges too.

In the meantime I will be looking closely at the big European G-SIB institutions and their equity positions - these include HSBC/Barclays/Credit Agricole/Deutsche Bank/Groupe BCPE/UBS/ING/Societe Generale/Standard Chartered/etc.

A liquidity event in any one of those giant institutions could trigger a global domino effect, especially as the derivative positions unwind like a broken spring in a worn-out builder's tape measure.

Europe is the birth place of the global private banking con - it may well turn out to be its nemesis too - poetic justice perhaps?

The scenes remain familiar - from Venice to Holland, Basel, the City of London, and the 'Old Lady of Threadneedle Street - fascinating - a play that spans 300 years lurching towards its final act - black comedy drenched in the blood of impending financial carnage.

And thanks once again for your article Roger - it certainly got my grey matter ticking over.

Warm regards

Colin Maxwell

I have every expectation that Roger will find this post extremely insightful.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.