The last major fixed rate home loan change was from BNZ and Westpac on Tuesday, February 25. It has been nine days since, and rate changes have been quiet over this period.

In the background, wholesale rates are moving very little at the one and two year end of the swap curve. There is a minor easing, but from January 6 to March 6 the one year swap rate is only down 14 basis points (bps), and the two year swap rate is actually up 4 bps.

These are not moves banks could use to fund home loan rate cuts. As we have noted before, it is the tolerance of savers for matching rate cuts to savings and term deposit rates that have allowed the 2025 home loan rate reductions we have had. And that in turn is why observers think over the next few months, even past the next expected Official Cash Rate cut on April 9, there are not likely to be large movements and we may be at or near lows for mortgages in this cycle.

A quick check of benchmark NZ Government bond rates also shows little net change so far in 2025.

If home buying picks up, banks will need savers funding more, and the scramble for that will put a harder floor under current carded rates.

As has been noted elsewhere, there is a huge flood of mortgage refinance activity coming, in fact is underway. Because borrowers have a penchant for trying to game the home loan rate situation (probably egged on by mortgage brokers), the duration of fixed terms for home loans is now historically short. Dangerously so for many borrowers, many of who have even gone on [high] floating rates, gambling that future fixed rates will be lower. But it is a gamble.

The high refi activity levels will mean banks who win more market share with low offer rates, probably have to offer better term deposit rates to keep their non-market funding levels in line. The effect of this also puts a floor on how low mortgage rates can go.

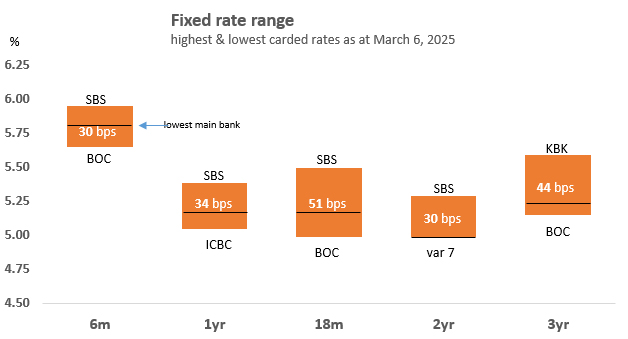

That has left the current mortgage rate cards settled currently like this.

And this shows that the most competitive challenger banks offer a 10 bps to 15 bps rate advantage over the best (lowest) main bank carded rates, at this time.

Also coming into play are non-rate incentives. We have set these out on our regular tracking page, here. But be aware that in most cases you will be faced with a choice of a rate discount below card, or a non-rate incentive. Not both (unless you have pristine financials).

The reader-reported mortgage rates are showing less of an advantage now, but please record them if you have them. We need you to record them in the comment section below, which helps us stay on top of this fast-changing corner of the home loan rates market.

And still negotiate. How flexible they may be will depend on the strength of your financials.

One useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is below.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market, like now.

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at March 6, 2025 | % | % | % | % | % | % | % |

| ANZ | 5.89 | 5.29 | 5.19 | 4.99 | 5.29 | 5.99 | 5.99 |

| current reader-reported rates | |||||||

| 5.89 | 5.25 | 5.19 | 4.99 | 5.35 | 5.79 | 5.79 | |

| current reader-reported rates | |||||||

| 5.79 | 5.29 | 5.19 | 4.99 | 5.29 | 5.69 | 5.79 | |

| current reader-reported rates | |||||||

| 5.79 | 5.19 | 5.19 | 5.59 | 5.79 | 5.89 | ||

| current reader-reported rates | |||||||

| 5.89 | 5.29 | 5.19 | 4.99 | 5.39 | 5.39 | 5.39 | |

| current reader-reported rates | |||||||

| Bank of China | 5.65 | 5.25 | 4.99 | 5.15 | 5.15 | 5.35 | 5.35 |

| China Construction Bank | 5.89 | 5.29 | 5.19 | 4.99 | 5.29 | 5.99 | 5.99 |

| Co-operative Bank (*=FHB only) | 5.69 | 5.19* | 5.29 | 5.19 | 5.49 | 5.79 | 5.89 |

| Heartland Bank | 5.25 | 5.19 | 5.19 | 5.35 | |||

| ICBC | 5.89 | 5.05 | 5.19 | 4.99 | 5.39 | 5.49 | 5.49 |

| |

5.95 | 5.39 | 5.25 | 5.29 | 5.35 | 5.69 | 5.69 |

| |

5.89 | 5.19 | 5.49 | 4.99 | 5.39 | 5.79 | 5.89 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

Comprehensive Mortgage Calculator

16 Comments

So the old WWAFL

Where We Are For Longer

Coalesce.

Sorry not normally a grammar pedant but this one jarred.

I have to admit that I had to google "coalesce". I have learned a new word, thanks.

The next circuit breaker has indeed just been sprung!

Agent Orange, in the land of the Brave, (or Bravado perhaps) - has set the bond market afire!! HFL Big-Leage/Bigly.

Interest rates are at the bottom now and the Debt noosed should be worried, very worried.

Its all upwards from here, sorry to inform the hapless DDDebt jockeys. Bad and Bigly Ass Rash, is a coming your ways. The softer saddle of the required 3.5% mortgages- is a distant mirage now.......

Upwards from here biatches

Rates & Bonds - Bloomberg

The black swan event would be a US Equities crash ie 20% noting that the MAG 7 are already 10% off peak, and many portfolios are over weighted to these ....

Anyone else hear Milford on the radio telling people not to panic re Kiwi saver, and if it falls you just by more units, also known as dollar cost averaging. Indeed its probably to late to panic if we are already half way there.

We all know its bad, when they tell the sheep to keep their wool on, just keep your head down and eat the grass...... and don't panic.

Buyer Beware Here!

My wife and I applied for a loan with ASB, and it’s been nearly three weeks now. They say it’s taking longer than normal because so many people are applying. We’ve bought properties before and would only need a small mortgage this time. We’re not in a rush, won’t be buying until the Auckland RVs come out, and might not even buy until next year since I think prices could drop another 10% this year. Every other time we’ve applied, banks got back to us within a couple of days… so this wait is pretty unusual.

Ummm this could be a reason why they're not rushing with your application perhaps lol...?

We’re not in a rush, won’t be buying until the Auckland RVs come out, and might not even buy until next year since I think prices could drop another 10% this year.

We haven’t said anything to the bank about when we’re planning to buy, my wife just filled out the forms with the info they needed. Anyway, I was just curious if anyone else is seeing delays. I told my wife they’re probably focusing on people in financial hardship. She's keen to buy, she would make a good real estate agent. I'm the one saying wait.

Got a phone call from KB only a day after submitting query re bridging finance. Emil straight back after ph call confirming that based on the facts in ph call it would be no problem at all. Not a mortgage i know, but fast and helpful response.

Can you begin to imagine how long it would take if you where applying for a loan for a "productive business venture"

Growth growth growth cannot be based on bank lending...........

This is pretty poor by ASB, at a time when banks are quite keen to write new mortgages. You're in a good position not to be in a hurry, but the bank employees processing your request don't know that, so, yes, a poor job by ASB.

Kraken, be mindful that, if you plan to buy in more than 6 months time, you will have to re-apply for finance with your updated financial position.

I think most banks hold the approval for 90 days depending on any conditions in the approval

No extra work for me, my wife fills the forms out

Feels like ASB being shit in handling their applications, banks are fighting like crazy on who approves faster to increase chance of conversion

US 10 year bond yield looks to be forming a new floor above 4% - well above what we’ve witnessed in the post GFC period where it fluctuated in the 1-3% range.

People mock the higher for longer (HFL) concept but I guess it depends upon what your cognitive anchor is to compare against. If the anchor is rates of the past 10 years, then it is quite possible HFL is true.

If your anchor is what rates were this time last year then it’s probably untrue to you.

So the statement can simultaneously be true and false depending upon what anchor you wish to use in your cognition (for those praying for lower rates it appears to be anchored on the recent peak, for those analysing from a longer term trend then it’s probably some type of average from the past 10 years or so).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.