It’s been a busy week in tax. Right at the start of the tax year, the Inland Revenue has launched a public consultation on a review of the fringe benefit tax regime which is now 40 years old. The 75 page issues paper titled Fringe benefit tax - options for change reviews the current status of FBT, focusing on issues Inland Revenue has identified. It puts forward a number of proposals aimed at simplification of these rules and a reduction in compliance costs, a long standing issue with major employers. There’s plenty to digest here but there’s a summary of the proposals on pages 6-8 of the paper if you want to get a quick handle on the proposals.

Reimagining FBT

The paper also addresses the separate issue of general compliance with the regime. A particular source of grief amongst compliant taxpayers is the treatment of the ubiquitous twin cab ute and the application of the work related vehicle exemption. Overall, the purpose of the paper is to

“…to review how FBT is assessed now, highlight current issues we are aware of with FBT and then outline some new concepts for how we could think about a reimagined FBT regime that is less complex and more targeted…”

The paper has 12 chapters, beginning with an introductory chapter, with Chapter 2 setting out the aims of the review. Chapter 3 explains how FBT is currently assessed. Chapter 4 picks up the FBT regulatory stewardship review from August 2022 which is really one of the initiators of this project. Chapter 5 then provides some comparisons with international FBT regimes.

Chapter 6 has an interesting discussion about FBT’s connection with remuneration. We tend to forget FBT was mainly introduced to ensure that all types of remuneration were brought into scope. Back in the 1980s, before FBT was introduced and the top personal tax rate was 66% it was common practice to give employees non-cash benefits such as company vehicles. Countering this was a key driver behind the introduction of the FBT rules in 1985.

Chapters 7 and 8 look at FBT and motor vehicles and considers options for change. Chapter 9 considers one of the areas of complexity, the treatment unclassified benefits. Chapter 10 discusses the option of applying FBT on entertainment expenditure, a proposal which will probably surprise a few people. The paper notes that entertainment regime also attracts a great deal of controversy and complaints about the compliance costs involved. Finally, chapter 11 looks at miscellaneous issues before Chapter 12 looks at data filing and integrity.

Why such a tight submission deadline?

There's a lot to consider in this paper but submissions are due by 5th May, which means between Easter and Anzac Day there's barely 4 weeks in total to review the paper and make submissions. The Minister of Revenue, Simon Watts, has repeatedly expressed a wish to simplify the FBT rules so he is keen to get this moving. My understanding the reason for the tight timeline is a desire to have the relevant legislation ready to be part of this year’s main tax bill, which will be introduced around late August or early September.

Proposed changes to FBT on motor vehicles

I expect many will focus on the proposals for motor vehicles. An interesting proposal is to increase the weight limit for vehicles subject to FBT from 3,500 kg to 4,500. Given the weight limit for a person with a full individual drivers’ license is 6,000 kg, my view is the FBT limit should tie into that threshold. Another proposal is to exempt vehicles that are used for providing emergency services.

A key change is removing the tax book value based option for calculating the fringe benefit value of a vehicle. Something worth considering is the suggestion for an optional valuation basis based on the fuel source for the vehicle i.e. electric, hybrid or petrol and diesel.

As part of re-connecting FBT with remuneration the paper suggests the FBT value of the motor vehicle could be calculated by reference to external sources such as remuneration consultations or maybe the AA calculations of vehicle running costs. The paper suggests regular revaluations, maybe every four years. One of the reasons why the tax book value option was introduced was that if people are not changing their vehicles regularly, then there's an issue that the vehicle may be overvalued for FBT purposes. The proposal would address this issue.

However, the Lord giveth, and the Lord taketh. The paper proposes the following new rates for calculating the fringe benefit value of a vehicle based on its cost:

- standard rate: 26% annual or 6.5% quarterly

- hybrid vehicles: 22.4% annual or 5.6% quarterly, and

- electric vehicles: 19.4% annual or 4.8% quarterly.

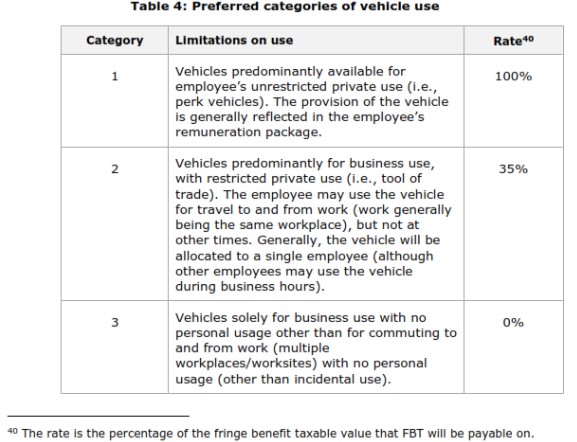

Availability vs actual use

As part of the intention to simplify FBT, the suggestion is to no longer require taxpayers to maintain logbooks to determine the days the vehicle is available for private use. Instead, the focus will shift towards the actual extent of private use the vehicle is available for (for example, is it limited to home to work travel?).

The paper suggests the following categories of vehicle use:

As part of this change, the paper proposes excluding “incidental travel” to ensure that one-off private use of a vehicle can be ignored for FBT purposes. Behind this idea is a “close enough is good enough” approach.

A key proposal is to remove the current work-related vehicle exemption which as the paper says, is a “most misunderstood” exemption. The changes should address the issue of double-cab utes supposedly qualifying for the work related vehicle exemption and avoiding FBT entirely.

Changes to the entertainment regime

The other major proposal of note is integrating the entertainment regime into the FBT regime. Again, the idea behind this is to simplify quite a number of issues that currently exist in relation to the entertainment rules which have never been very popular and compliance is also a problem. As the paper notes many employers are taking a close enough is good enough approach to entertainment expenditure.

The interaction of the entertainment and FBT regimes can be confusing. For example, if an employer takes an employee out to a restaurant that is subject to entertainment rules. However, if the employer gives a voucher for that restaurant to an employee to use whenever they want, then that's subject to FBT. Another example one would be if an employer pays for employees to participate in a front run, and then then provides a BBQ for staff staff at the finish line. Is the cost of the fun run subject to FBT but the BBQ represents entertainment? Integration of the two regimes is intended to address these issues.

Overall, this is a welcome review and as previously noted pretty timely given it’s now 40 years since FBT was introduced. Just remember you've got to get your skates on to submit by the deadline of 5th May.

Inland Revenue ramps up its audit activities with good results

At the start of last week Inland Revenue announced some of the results of its “noticeably increased” compliance activity. For the period from 1st July to 31st December 2024, it opened 3,600 audits 50% up on the same period in 2023. According to Inland Revenue’s Segment Lead for Significant Enterprises, Tony Morris, “Inland Revenue has found $600 million of additional tax that should have been declared.”

Morris went on to add “We’ve had a strong focus on the largest businesses in New Zealand and it's worth noting that half of that additional tax came from less than 10 audits.” In other words 10 audits yielded $300 million.

Furthermore, Inland Revenue screened over three million returns as part of its annual year-end auto-assessment process. 30,000 of those, or about 1% were selected for review which resulted in a further $859 million of tax revenue. That's a pretty good bang for buck on the additional funding it got in last year’s Budget.

Inland Revenue has also been focusing on debt and I thought this particular comment was of interest

“We've been in touch with 200 business owners and told them we know they have multiple properties - some in a company name, some in trusts, some personally. We believe they should be able to refinance to pay their debts to us and told them so.

“...These 200 people had $14 million of debt between them, but within a month more than $10 million had been paid or put under arrangement.”

Inland Revenue’s data gathering around property transactions is second to none and people would be wise to not underestimate this. It has been identifying transactions in this area for quite some time. A colleague recently told me of an audit that he was involved in where the client was saying, ‘Oh well, a number of property transactions were simply renovations of my main home’. That is until Inland Revenue investigators presented a “ream sized folder” full of property transactions for this taxpayer. From that point, the question wasn't about rebutting Inland Revenue’s proposition that he was actually a property trader but trying to mitigate the damage. You have been warned.

“This is Baycorp calling on behalf of Inland Revenue”

However, something that does concern me is Inland Revenue’s announcement on 10th April it would be “running a six month pilot program in partnership with Baycorp to improve our debt collection process.”

Inland Revenue warned taxpayers that during this pilot, “you may be collected, may be contacted by representatives from Baycorp. Please be assured that these contacts are legitimate and part of our authorised programme.”

That's as may be, but I'm not so sure given everyone's growing concern about scams, not too many people are going to accept calls from Baycorp saying ‘you own Inland Revenue money pay up.’ I therefore doubt the pilot is actually going to be as effective as hoped even if Baycorp show the taxpayer incontrovertible proof that they have a debt due to Inland Revenue.

This is just the latest push by Inland Revenue to improving debt collection. As we noted in our last podcast given the rise in GST debt in particular, it's basically no surprise that Inland Revenue is putting resources into debt collection. And as I've said previously, I expect there will be more funding given to it in next month’s Budget.

Is GST a tariff?

Meanwhile, around the world there has been large scale turmoil in the financial markets as everyone tries to work out what exactly is happening with the tariffs proposed by President Trump's administration. As part of this he has indicated that value added tax (VAT) is now seen as a tariff. There's been a huge pushback against this with the basic counterargument being that tariffs are only imposed on imported goods and services, whereas GST/VAT applies regardless of source of the goods or services

If you want more a bit more detailed analysis of why GST/VAT isn't a tariff, I suggest this interesting post by Dan Neidle of Tax Policy Associates. He considers the issue using the example of beer, which is always handy, and the implications of the policy.

Removing GST from fruit and veg - “a well-known solution to every human problem”

The American writer HL Mencken was the source of the quote “There is always a well-known solution to every human problem - neat, plausible and wrong.” This often comes to mind in relation to the frequent proposal to remove GST from fruit and vegetables. It so happened the Prime Minister was asked about this suggestion on TV1’s Breakfast Show. He responded that it was far more complex than people imagined.

I subsequently appeared on Wednesday’s show to discuss the issues involved in removing GST from fruit and veg. To be fair following Mencken’s dictum about the policy being ‘wrong’ would be a bit harsh. This is an extremely well meant suggestion based on the precept if you wanted to try and help people struggling with the cost of living then removing GST is an option or step and no doubt would provide some assistance.

But as I explained it is complex and definitional issues lead to extreme examples such as the UK Mega-Marshmallows which enabled me to sneak in a reference to The Princess Bride. Furthermore, well-meant though it is, the proposal is not perhaps the right solution for the problem you're trying to deal with, which is people with low income who are struggling with rising costs. A targeted response is more appropriate.

The Tax Working Group’s view

This was also the analysis of the 2018-19 Tax Working Group which also addressed a key complaint about GST, that it's seen as regressive for those on low incomes. In response to addressing regressivity by perhaps reducing the rate of GST or introducing a GST exception for food the TWG commented “there are more effective ways to increase progressivity than a reduction in the rate of GST.”

Instead, the Tax Working Group suggested

“…increases in welfare transfers would have a greater impact on low income households. Changes to personal income tax can also have a greater impact on low and middle income earners. GST exceptions are complex, poorly targeted for achieving distributional goals and generate significant compliance costs, and furthermore, it is not clear whether the benefit of specific GST exceptions are passed on to customers.”

I agree with that analysis. It’s also supported by research carried out by Tax Policy Associates on the impact of VAT(GST) changes in the UK, where VAT has been removed from several products again for very well meant reasons. Examples include a reduction in the VAT rate for tampons and other menstrual products and the zero-rating of e-books. In both cases, the analysis carried out by Tax Policy Associates identified little or no benefit going to final consumers. In fact, in the case of e-books, no benefit passed through to consumers, costing the UK £200 million.

A complex and ineffective solution

In sum removing GST from fresh fruit and veg is complex and leads to boundary definitional issues. UK cases such as Mega-Marshmallows or the older Jaffa cake case involving the UK's zero-rating of food are very, very good examples of the sometimes absurd distinctions that arise. Even although accounting systems are much improved the fact remains there are irreducible minimum compliance costs involved. These will fall most heavily on smaller operators such as dairy owners who already have a fairly heavy compliance burden with GST.

Much as I can see why people would want to suggest zero-rating fresh fruit and vegetables, ultimately, you'd have to consider whether the benefit of such a change is actually going to flow through to those who you want to benefit? Remember, if you do apply an exception, everyone benefits from it. As the Tax Working Group noted wealthier deciles spend more on food and fresh fruit and vegetables so would probably benefit disproportionately.

This isn't a matter that's going to go away. My view remains in line with that of the Tax Working Group. Look at what the real issue is, and it’s some families don’t have enough income. The best approach is therefore to give them more income. But we've got an election coming up next year and no doubt the proposal together with other well-meaning but inefficient ideas will be put forward.

And on that note, that’s all for this week, we’ll take a short break for Easter and be back for the ANZAC Day weekend. In the meantime I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day and Happy Easter.

6 Comments

IWHFP

What a socialist article. Re GST: We dont want higher income earners (ie higher tax payers) getting any advantage from removing GST from fresh food products. Tut tut. Canada, UK and Oz manage to remove sales tax from these items. "Too complex" is the well worn socialist mantra in NZ. Nanny state says NZers are too dumb to handle such complexity. Canadians, Australians and British are clearly much smarter than Kiwis and can handle such complexity. Please!

It’s not the Nzers who are dumb re gst on food, it’s those others.

Only reason Aus made the food allowance was to get the all powerful unions off their back when introducing gst in the first instance. They would love to be using our relatively simple and very efficient gst rules.

Would provide an abundance of work for tax lawyers and accountants though (and guess who pays for that) - perhaps you are one of these?

If only that sort of thinking were applied to other taxes and their correspondening transfers. It astounds me that we stick with simple gst but continually adjust and rearrange personal tax by fiddling with the likes of WFF and AS causing more and worse distortions along with extra costs.

I'm sure we're smart enough to cope with a complex system. Are we wise enough to avoid having to cope with such a system, with all the associated inefficiencies?

We are smart enough to avoid doing something that achieves nothing except wastes everybody's time.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.