Housing affordability was becalmed in a sea of uncertainty for first home buyers at the end of the summer selling season.

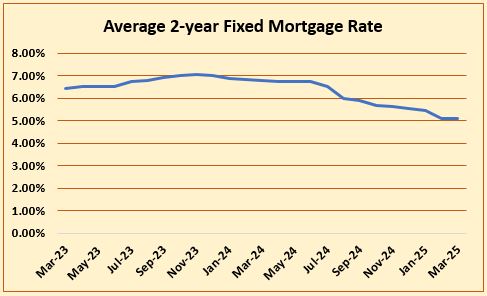

The latest figures show mortgage interest rates, one of the main drivers of affordability for first home buyers, were as flat as a millpond in March.

The average of the two year fixed rates charged by the main banks declined by the narrowest of margins, from 5.09% in February to 5.08% in March, a decline so small it would make almost no difference to mortgage repayments.

That brings an end to the more substantial and steady declines that occurred over the previous 15 months, which saw the average two year fixed rates drop from 7.04% in November 2023 to 5.08% in March 2025.

There is no doubt the decline in mortgage rates improved affordability, and that improvement has been further enhanced because house prices have not had the sort of sustained increases that would normally accompany a substantial or prolonged drop in interest rates.

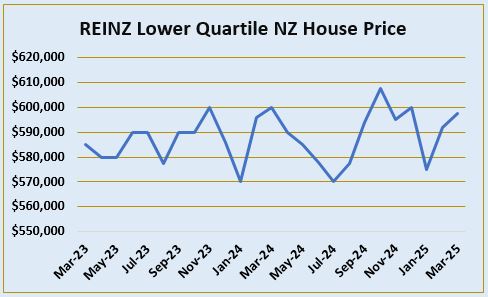

The first graph below charts the monthly movement in the Real Estate Institute of New Zealand's national lower quartile selling price over the last two years.

It shows there have been monthly movements, both up and down, but there has been no sustained upward trend in prices even as interest rates have been falling. In all but one month, October 2024, the lower quartile price has remained within a very narrow $30,000 price band between $570,000 and $600,000.

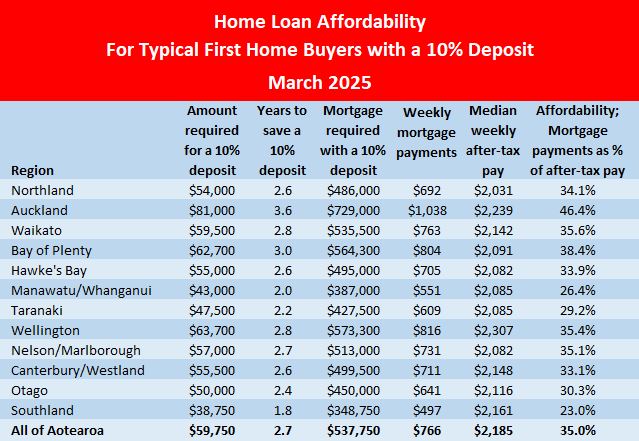

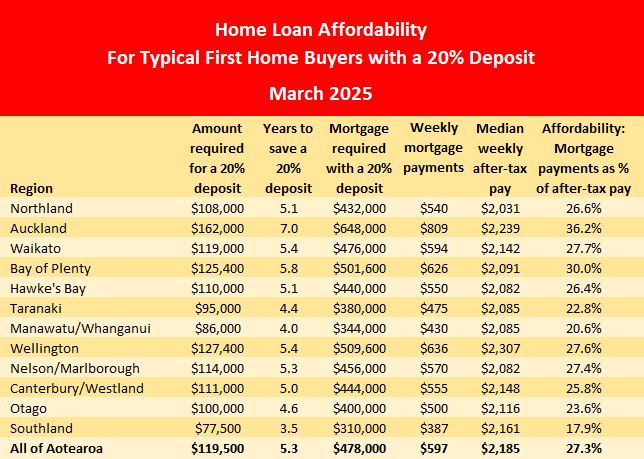

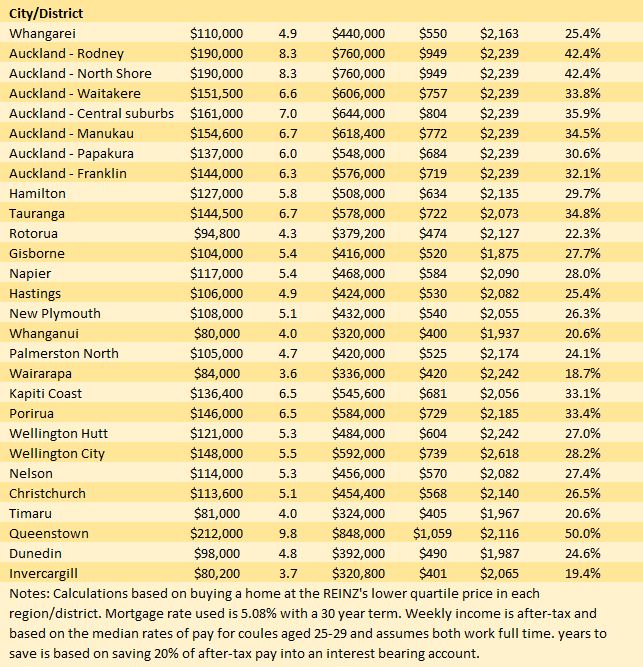

Interest.co.nz measures the mortgage payments on lower quartile priced homes against the median after-tax pay for 25-29 year-olds, to get a measure of affordability for the population cohort likely to be saving for a home, or at least thinking about it.

Over the two years from March 2023 to March 2025, the percentage of pay eaten up by the mortgage payments on a home purchased at the national lower quartile price, with a 20% deposit, declined from 34.2% to 27.3%.

That's a substantial improvement in affordability, and even in Auckland, the region where affordability has been most stretched, mortgage payments declined from 45.6% of take home pay to 36.2% in March 2025.

So aspiring first home buyers are in a significantly better position to buy a home now than they were two years ago.

However, March this year also marked the end of those monthly improvements in mortgage affordability.

It is as if affordability measures are standing still, as the market waits to see what will happen next.

Were the March figures a brief pause before affordability measures continue to improve, will they remain static or start to worsen?

As the housing market heads into winter it is sailing on a sea of economic uncertainty. And uncertainty breeds caution. So we could be in for an interesting few months.

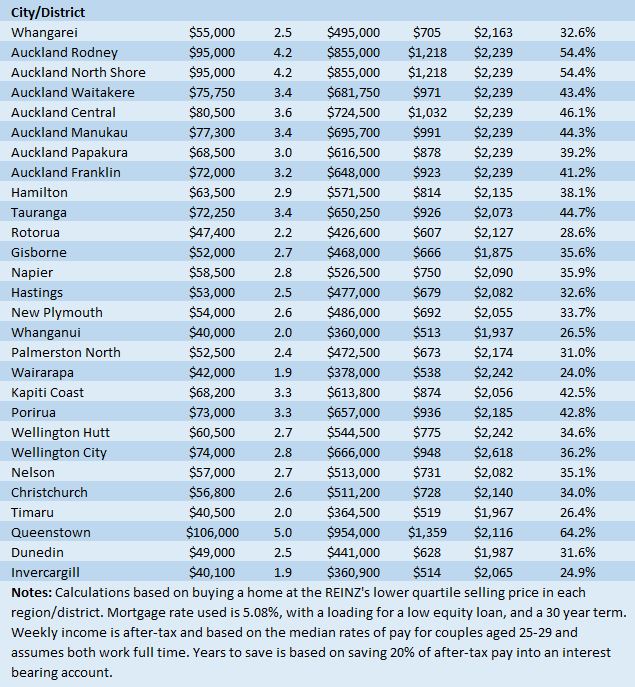

The major tables below show the main affordability measures in all major urban districts of Aotearoa, for purchases with either a 10% or 20% deposit.

The comment stream on this article is now closed.

1 Comments

They could always move to Austin. Rents are down 22% yoy. Austin was the poster child of unsustainably rising rents in a hot housing market and is now leading the nation in rental price declines thanks to an unprecedented housing construction boom.

Also, U.S. house sellers also gave concessions on 44% of transactions in Q1 25. The highest since 2023 when mortgage rates surged.

And to cap it off, median new home prices in the U.S. have now dropped below existing home prices. Home prices almost always command a premium. Newer inventory. No longer. When asked why buyers aren’t buying it’s a lack of confidence in the economy and their job prospects. Not so much the cost.

https://www.bloomberg.com/news/features/2025-02-27/austin-rents-tumble-…

https://investors.redfin.com/news-events/press-releases/detail/1316/44-…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.