It's the Great Reset. The great mortgage reset of 2025.

Over $200 billion worth of mortgages on either floating or short term fixed rates are up for a re-fixing in the first half of this year. That works out at an average of well over $30 billion a month.

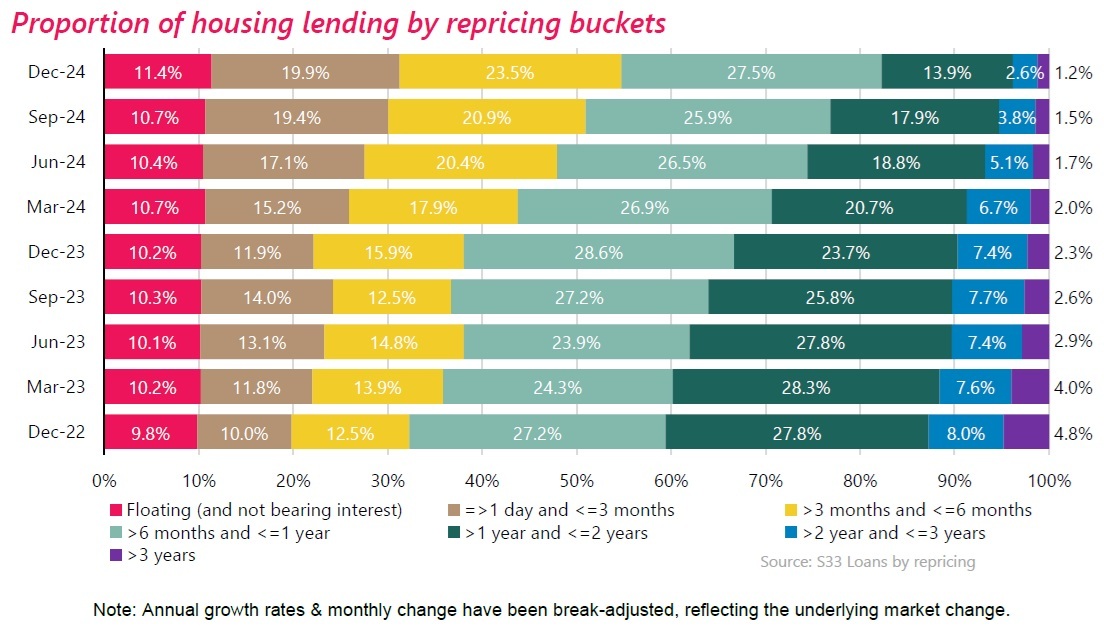

Reserve Bank figures for the last month of 2024 show of the grand total of $369.546 billion of outstanding mortgages, $159.899 billion was fixed for six months or less and $42.8 billion was floating.

That's a combined total of $202.699 billion either fixed or floating that either must be, or can be, refixed before the end of June.

And it makes up 54.9% of the total mortgage pile, demonstrating how the country's home owners have been going shorter and shorter with their mortgage terms as expectations of interest rate falls have grown.

As the below graphic taken from the Reserve Bank's summary of the monthly mortgage figures shows, the 54.9% of fixed or floating mortgages up for a reset in the first six months of the year compares with a percentage of just 38% as of December 2023, and 32.3% in December 2022.

To look at a slightly longer timeframe, as at December 2024, a total of $304.139 billion worth of mortgages was up for a refix by the end of this year.

This means 82.3% of the current $369.546 billion mortgage pile will see an interest rate reset this calendar year. A year ago, in December 2023 the comparable percentage figure was just 66.6% and in December 2022 it was 59.5%.

What it means in practice is that the vast majority of the country's mortgages will be quickly responsive to whatever changes there may be to market rates in coming months.

As the move to shorter and shorter term mortgages has gathered pace, then so the homeowners have looked to become more and more nimble.

Looking at the figures for October 2024 through to December 2024 shows some major swapping between fixed and floating - and then back again.

In October there was $42.744 billion of mortgages on floating and $323.317 billion fixed (that's all terms, both long and short).

In November 2024 the amount on floating had blown out to $53.651 billion (highest monthly floating total since October 2016), while the fixed total had shrunk to $314.172 billion.

In December the floating total virtually shrank back to where it had been before, at $42.8 billion, while the fixed amount grew again to $326.746 billion.

For comparative purposes it's worth saying the grand total of all mortgages in October 2024 was $366.061 billion, rising to $367.823 billion in November, and $369.546 billion in December. So, it didn't grow by all that much during that three month period, meaning comparing the movements of figures within the totals is reasonably apples-with-apples.

In terms of trying to work out where the nearly $11 billion worth of mortgages that apparently went from fixed to floating and back, well, we can't exactly, based on the figures.

But what we can say is amounts of fixed rate mortgages up for refixing in between three and six months time blew out by around $8.5 billion between November and December, rising from $53.723 billion to $62.208 billion.

The Reserve Bank began cutting the Official Cash Rate (OCR) from the cycle high of 5.50% in August, with a 25 basis-point cut. This was followed by 50 point cut at the next review in October.

The last OCR review for 2024 was on November 27.

Ahead of that November review it was widely expected another 50 basis points would be trimmed from the OCR. This was duly done.

Now all eyes are on the first OCR review for 2025 on February 19. Reserve Bank Governor Adrian Orr was surprisingly explicit (compared with past Reserve Bank conventions) in his post-November review press conference in strongly indicating another 50 basis-point cut will be coming in February.

Assuming that comes to pass and we have a 3.75% OCR come February 20, those $200 billion-or so mortgage holders looking to refix by the end of June will need to work out a couple of things.

Firstly, how much lower will the OCR go? The Reserve Bank's November Monetary Policy Statement (MPS) implied the OCR might not go lower than 3.50% this year. But other economists are suggesting it will be 3.00% by the end of the year.

Secondly, how much lower may mortgages go? Cuts to the OCR do not guarantee equivalent cuts to mortgage rates, particularly not if banks have been cutting mortgage rates ahead of OCR reductions - and they have been.

So, plenty to think about.

While the rises in mortgage rates that began in the second half of 2021 in reaction to rising inflation have added considerably to some monthly interest bills, the levels of non-performing loans - while up - have not risen precipitously.

The Reserve Bank's monthly 'loans by asset quality' data series shows in December there was a $26 million increase in non-performing home loans, to a total of $2.16 billion.

In the whole 2024 calendar year the non-performing home loan total rose by $643 million (42.4%).

The $2.16 billion non-performing loans total represents 0.6% of the total outstanding mortgage pile.

While you have to go back to 2013 to find a non-performing loans percentage as high as 0.6%, the current figure is still well below the levels seen in the post-Global Financial Crisis 2009-2012 period when the non-performing percentages frequently hit 1.2%.

*This article was first published in our email for paying subscribers first thing Wednesday morning. See here for more details and how to subscribe.

112 Comments

Well it is a better problem to have than 2023/early 2024

And not 2 or 3% option in sight. Already many non performing loans everywhere and according to the RBNZ, the amount is set to double. Do banks continue to extend and pretend, or do they start for force sales and let, finally, true market discovery take place...

25 is the year the popcorn starts to burn.

I see prices stabilising this year. We're now starting to see interest rates that should underpin current prices. Auckland may have a bit further to drop, but the other cities, provinces and tourist centres, should do better going forward. The only possible fly in the ointment could be mild inflation returning but I don't see levels such as that seen in 2022 any time soon.

@Averageman

Non-performing home loans are sitting at 0.6%, but, more significantly, impaired home loans are sitting at just 0.1%.

You seem to be cheering for banks to reposess people's homes. Why would you want people to become homeless?

Not at all. Homeowners...value your job and stay employed. Specustackers, value your tenants and stop trying screw them every rent review so you can stack another house.

Summary. Don't lose your job...or you tenant.

So why the comments such as this is the year the popcorn starts to burn?

Banks cleaning out the over leveraged will create a rush to the exits for speculand. This will effect everyone, even those eating popcorn watching. Hence burnt popcorn, just like 87. Probably why Banks have tbeen writing 30 year loans, allowing more interest only, and ignoring straight default.

Other points.

NZ is in recession. Future tax payers are leaving. Unemoyment is up. Jobs dare own. Bankruptcys are up. Retail and discretionary spend is in the crapper. Govt debt is at record levels and the govt is cutting spend left and right. One would think Banks should be, or getting ready to, "pull the weeds" to reduce non performing loans.

If you look closely at the our Banks, and while making record billions in profit, they have been quietly reducing headcount, closing branches, and removing cash machines. Normally you are expanding, looking at acquisitions, and fighting for market share when making super profits. Significant overhead reduction has been taking place instead. One cant help wondering what are they preparing for.

NZ has started 25 with a big rise in listings. No buyers are in sight. What are the current owners preparing for...

Hard not to see all in on leverage to the moon as pretty risky this year.

Banks are not benevolent societies. Repossession of homes can be for a variety of reasons but I should think loosing job is probably the biggest one. Where there were two incomes contributing to the mortgage its fine but the loss of one immediately puts the repayments in jeopardy. I'd think where % of the mortgage is being repaid, say at least 40% then some form of extension is required but certainly no more than six months. The repossession should be made much more clear in the mortgage agreement so there's no wailing a gnashing of teeth when the bank says times up.

I'm under the perception that the banks are very lenient.

These percentages don't mean much to me. Surely impaired loan amount needs to be compared with the tier1? bank capital available?

The worst case scenario would be non-performing loans becoming impaired and so need to be compared with bank capital available. An intermediate calculation would be at what percentage of non performing and impaired loans be against available bank capital. The banks would not loose all the impaired or non performing loan amounts so perhaps my doomsday scenario won't happen. It likely requires the banks to take a stab at what they could actually recover in a fire sale and then compare that with the banks capital. I'm sure RBNZ keeps their eye frequently on this.

I guess that the point I was making, in reply to Averageman, was that the statement "there are many Non-performing loans everywhere" is not a true statement, though it depends on how you define "many". In my view, if 99.4% of loans are performing, and 0.6% are not performing, then you can hardly say that there are many. The "Aoteoroa Legalise Cannabis Party" achieved 0.45% of the vote in 2023, and I never heard anyone say that they got many votes!

Non performing loans are not a massive threat by themselves to the banking system, they become very problematic if the house is in negative equity. Another leg down and suddenly the banks themselves start to get impacted vs just the borrowers.

The non legal responsibility of the banks to make a fair an accurate view via CCCFA of your ability to repay the mortgage complicates things, and maybe why banks are being much nicer with those who fall behind then in the past.

This will be a developing story during 25/26 IMHO.

Thanks ITGuy, I appreciate your answer.

For instance, friends paid $1.4 at the peak for a lower hutt rear section house. It's worth about $950k to $1mil today.

This means that the bank will likely not recoup their debt if they default. So the bank is hyper incentivised to do everything they can to keep the mortgage on the books with a payment holiday, interest only, extend the term and pretend that's its still an AAA debt.

Where have we seen this before?

There's no loss unless realised. Extend and pretend is the go to by banks - they know the contagious effect of mortgage sales and will do everything they can to prevent it, but even they have limits.

Indeed, where have we seen AAA loans that were in fact rubbish.

Most NZ banks only syndicate loans for RBNZ repo security.

You're looking at this through the wrong lens. Those fixing now will have taken 6-12 months recently, betting that rates would be lower in the short term and they are all about to be proved right.

RBNZ publish the average weighted mortgage rate and business loan rate. At end November these were 6.35% and 7.12% respectively. We get December figures next Monday.

It is fair to assume given previous trends and current bank rates that the average mortgage and business rates right now will be a bit above 6%.

That takes the average mortgage rate back to March 2024 levels and the more quickly adjusting business loan average rate back to November 2022 levels.

Now, rates became restrictive around the end of 2022; that's when all the data started to turn south. In May 2023, we saw the start of serious job losses, benefit numbers growing, companies wobbling etc. The big 'snap' - the sudden acceleration in crap data - came in early 2024. By this point, total interest paid on mortgages was about $2bn per month - double what it was in mid-2019 and mid-2022 (it was a bit lower between these dates).

Now, we are still firmly in decline mode - negative job growth of around 1% yoy, unemployment numbers increasing at around 25% yoy, benefit numbers going up at around 8% yoy, company liquidations stacking up etc.

My point, if it wasn't obvious, is that if we are going to rely on lower rates for stimulus, then we probably need average weighted mortgage rates of around 4% and business loan rates of around 4.5% - that would take us back to late-2022 & late-2019 levels.

Now before anyone starts, I am not saying that we should rely on an OCR In the 2s for stimulus, or even that we could move that far from the Fed. But the alternative, superior approach - significant public investment and an expansion of the Crown balance sheet, is off the table because our idiot politicians have fenced themselves into a corner with commitments to fiscal (ir)responsibility.

Insightful commentary as always Jfoe, thanks.

I'm actually of the belief that National is purposely trying sink the economy quicker:

1. Certain MPs and other interests dump property near top of cycle and buy them up for cheap when the property market is at its bottom (pending)

+

2. Open the immigration gates, increase spending and get the economy out of the semi self generated rut just in time for the next election - people have short memories. House prices go BRRRRRRR.

= $$$ + re-election

"My point, if it wasn't obvious, is that if we are going to rely on lower rates for stimulus, then we probably need average weighted mortgage rates of around 4% and business loan rates of around 4.5% - that would take us back to late-2022 & late-2019 levels."

This is exactly what it's going to take for rates to become stimulatory. Economists claiming that rates won't fall much further while predicting a housing market recovery are kidding themselves. The evidence is clear that rates at their current levels (including the 50 points yet to come off the OCR) are still strangling the economy.

An alternative viewpoint could be its the amount of debt held that's strangling the economy.

Too many people whinging about the interest rates on a debt that would take them a decade of their entire after-tax income to clear!

That's exactly the problem. Outstanding principle grows during each boom, needing ever lower interest rates to stimulate another boom. Hence we're at the high to mid fives and not a lot of action.

Spot on. And too much debt because too high house prices…how did we allow 30 year mortgages to become the norm? What is average age of FHB? What is average retirement age? Nothing adds up….

The economy is not and should not be a welfare scheme for property! The fact if has been operated as such in recent times is not a good thing.

Policy should be incentivising hard productive work instead.

So when your 6 month fix ends ... Think about another 6 month fix. [Before you do though ... do the maths!]

This has to be significant for the economy. A huge number of people will become much better off in the next 6 months. Sure many of them may keep the repayments the same and smash their mortgage, but that debt reduction is also significant for the economy and consumer sentiment. I feel like we should get some good GDP growth this year.

I have a bridge to sell you

Now, we are still firmly in decline mode - negative job growth of around 1% yoy, unemployment numbers increasing at around 25% yoy, benefit numbers going up at around 8% yoy, company liquidations stacking up etc.

What fairy magic do you know of, or do you think willis and luxy can turn this ship around?

I don’t think it has anything to do with Willis or Luxy. The RBNZ created this recession, and now they are doing the opposite.

Good luck with the line of thought.....

We’ll see I guess. What is your GDP prediction for 2025? Negative?

Like the economy ..flatlining...

I see us bumping along the bottom, positive here negative their per Q, perhaps 0.5% positive for the year.

The problem is no one has any belief that NAct has a plan, thus people and business keep their horns pulled in...

Confidence is more contagious then a virus, so is fear.

I reckon we will get 2% or more growth. Not amazing but better than nothing. Then maybe 3% next year. I should save these posts for next year to declare the winner.

My bets are obviously worth a bit more then honor ... but yeah 2% and then 3% would be nothing short of a miracle,

NActNZFirst would be in power for decades....

Like your understanding of Bitcoin Jimbo expect to be disappointed 😔

Yes. Sideways at best with the current settings.

Animal spirits are hard to control why would rbnz want to create an inflationary boom

with DTIs banks may be limited ability to loan to resi and they have no willingness for any other purpose

The RB may be doing the opposite in the sense of dropping the OCR, but they're a long way from reaching a neutral or stimulatory rate for the economy.

To create the opposite of a recession (economic expansion) they'd need to drop the OCR another 200bp

He went to low, then he went to high, is he stupid enough to go too low again? or , my opinion not actually go low enough here to actually try to put a bottom in, its been my belief for a long time he will go low enough but only once he starts to panic about the housing market.

I think that we are not there yet, its when averages are down 1/3 or more from peak ... more then that and banks may need more capital.

Orr is plenty stupid enough to drop rates too low again. I believe global inflationary pressures are, and will continue to hinder his ability to pull the lever as low as he desires though. The fed’s pause cannot be ignored, he'll be stuck.

@TL I think you are right, what has Orr done to prove he won't f**k this again, if DJT navigates things well and the fed don't cut then surely Orr is hamstrung, I do think we'll still see the 50 this month, then maybe a couple of drawn out 25's over the rest of '25, is 100bp over this calendar year enough to ignite NZ? We seem pretty cooked...I'm not sure it is eh.

Maybe he will he try to look through some of the global inflation/damage to the NZD and just cut anyway if the economy is still hurting and our govt still refuse to deliver any fiscal stimulus as the year progresses? What does that do, lower dollar great for exports/tourism, will the pain at the pump be too hot though.

If DJT slips up and the fed starts to cut again, maybe we'll see Orr push all the chips on the table and roll the dice on stupidly low rates again 😂...lets hope DTI's do their job in that case.

Yep, we desperately require another cut in Feb. I can see Orr delivering the full 50bp followed by a pause. A 25bp cut is not off the cards in Feb but may require another cut down the line. I struggle to see a full 100bp rate drop delivered this year with how the cards are falling.

Trump is busy rattling cages as expected early in the term, we’ll need to reassess the outlook once the dust begins to settle. Until then it’s tough to speculate on how Orr will navigate the situation.

If the Fed resumes cutting then you can expect Orr to jump on the opportunity to follow suit - NZ needs cuts much more than the US does. Orr is praying to the gods the US is forced to resume their rate cut cycle. Otherwise he’s cooked.

NZ doesn't desperately require a cut. The primary need is to keep inflation under control.

You’re correct that inflation is the RB mandate. But what will drive NZ’s “growth growth growth” if the OCR remains restrictive and government deficit spending is decreasing, with a projected surplus by 2029?

That's the point - we need better govt action on spending and taxation instead of more Reserve Bank pandering to property.

I completely agree with you Rick. Problem is the Govt are yet to prove themselves capable of this with no plan in sight. And the RB has proved they love slamming the lever in each direction.

They can’t drop much without tanking currency and setting inflation off again

Only one example I know, but job numbers on Trademe are increasing. About a month or so ago down to about 9300 now up over 11000.

I know the place I work at is struggling in finding job seekers, especially ones for the more technical and qualified positions.

A month ago being the first week of January when people mostly weren't back at work?

For a better comparison what was it in mid November vs today?

Ok. Good point. I don't remember that month either.

I cannot see how to look back at past months for total numbers. Just been having a look.

I know the place I work at is struggling in finding job seekers, especially ones for the more technical and qualified positions.

This is consistent with my industry. The technical and qualified have left the country as they saw the direction NACTNZF was going and attempted to flee the sinking ship which is creating vacancies. NACTNZF then removed the requirements to be technical or qualified to enter the country, the people leaving are being replaced by immigrants but not technical and qualified ones.

In the next six months, let's say that the average weighted yield on mortgages drops to 5.5%. This would require RBNZ to drop rates more aggressively than planned.

What happens to disposable incomes?

By then mortgages will be around $380bn. So, 5.5% x $380bn / 12 = about $1.74bn interest payments per month.

That's about the same amount of interest payable as in January 2024 (5.9% x $359bn / 12) when conditions were firmly contractionary Mortgage interest payments got as low as $0.7bn per month in mid-2021!

Now, as we get back to borrowing, the banks will pump billions of credit into our economy. This will give us some stimulus. There is always a seller at the end of every chain of house sales after all. But, my view is that we are going to slide sideways for the next 6 - 12 months unless we see big falls in oil prices or major Govt investment etc. The idea that the economy will turn on a dime in a couple of months (as per RBNZ forecasts) seems outlandish to me.

Here's the total interest payable on loans by the way.

Well Westpac pulled rates down a lot lower yesterday and we will keep cutting the OCR until things improve. USD rate be damned.

Still I agree that there is no switch that can be flicked here.

That seller at the end of the chain may be a bit more conservative then in the past as well....

Think of the credit created this way when investors where leveraging up their sites.

The mis-allocation of 100's of billions of funds against assets that produce low yields is now the albatross around our necks that will cause a lost decade. People will not want to clear that debt as it will often lock in loss, or they are scared they will never qualify for that loan again due to age and new DTIs.

The leaves have fallen off the money tree....

In some situations people have invested as families or groups, can you imagine trade management and risk management dynamics.

We are at least 9 to 12 months out for any meaningful improvement in the economy

Yes yield inversion only normalised in the 2nd half of last year after the deepest and longest inversion we’ve witnessed since just prior to the Great Depression. Typically it would be anywhere from 12-36 months after that before improvements are seen in the economy after that but given how deep and long the inversion was it could be significantly longer than that - I mean after the 1920’s boom when did economies really find their feet again? There were a couple of lost decades there. It took some sharemarkets 20 years or more to return to some of the highs of the late 1920’s.

Like the OCR increase there's a lag between them and lowering inflation, we are only now feeling the effects of the first few OCR cuts, by Q3/Q4 we will feel the effects of these cuts. For me that's approximately $150 a week, this extremely cash will provide A LOT of relief to families and will be the fuel for GDP growth.

I agree.

That’s about 20 items in a shopping basket not exactly growth just surviving but yeah gd news for many against the wall

maybe it allows people to stop cutting back

Except it will be on top of the the shopping they already do. That's the difference that could help a family save or invest $50-100 a week.

Or the differences that means on a summer trip to the beach they stop in at the fish and chip store instead of driving past.

Watch our GDP skyrocket if that happens....

That's about the size of the tax cut national gave us.... I did not notice a personal sugar rush...

This country will simply not turn around, and neither will housing based on a takeaway meal spend.

As mentioned we are missing the billions of dollars that used to exist at the end of property chains (downsizing etc etc).

The velocity has collapsed as well.

I sold my own house in Oct 2021, I cleared a $2,400,000 gain. This year my employer is giving me a $4,720 pay rise this year.

One of these things is not like the other.............

Yip that $2.4 mill gain is now debt some other market participant/s is trying to service in this poor/weak economy.

They paid over 3.2 mil for that dump, intended to develop townhouses, they have dropped about 35k into it to make it rentable and are asking $900-950 per week so a gross before rates and interest costs yield of 1.5%

proper f&^%$%^d

If they put in no capital and used existing equity from elsewhere they are bleeding $3,400 a week in interest @ 5.5%

Time in the market made the money, timing the market allowed me to get out before it all evapourated.

Crazy stuff - when people say ‘no point trying to time the market’ I’m always extremely sceptical because there are certain times when buying makes a sense and times when it doesn’t. 2021 - now has been one of those periods where buying really hasn’t made any sense other than accepting a huge amount of risk from the selling party with potentially very low ROI.

So basically the opposite of a good investment that is low risk but potentially high ROI - our housing market of late is high risk but potentially very poor ROI.

Just wow....

Out of interest how have you invested the cash you had as a result of your sale? Just diversify across asset classes or holding in cash funds/TDs for now? (no problem if you don’t want to answer this)

We moved rural swapping 800 sq m in AKL Central for 150,000 sq m, we can subdivide this, just need to plant some bush etc, we are now breeding dressage and show jumping horses as a startup for my partner, I still work in IT, we banked some money from that trade and its with Milford in funds.

We do not live a $$$ life, we eat out maybe once a month max, drive cars all 5 years plus and not European, and I have not been overseas for about 8 years. The house we sold was crap, would have probably got more $$ if it had been bare land. Now we have a modern warm house and way way better lifestyle. Have home kill beef and sheep.

I carry a bit of debt as its easier to raise personal debt then on commercial real estate assets, the assets are well cash flow positive.

Many of the Spruikers call you me gutless never take a risk DGM, I am all for risk at the right time in the cycle.

You can love property historically but hate it as an investment at this point in time. Most of the Spruikers here cannot tell you who they will sell there amazing cashflow negative assets too.

For houses prices to double from here I assume that the debt probably has to nearly double to 5-600 billion and that interest payments per month would then be about 3-3.4 billion a month. Its not going to happen. There is not enough income to secure that flow.

I think gold is a good risk trade here. I think the majors USD / EUR / JPY may feel safer then the commodity currencies going forward thus that helps you in gold as well being based in NZD.

"They paid over 3.2 mil for that dump, intended to develop townhouses, they have dropped about 35k into it to make it rentable and are asking $900-950 per week so a gross before rates and interest costs yield of 1.5%

proper f&^%$%^d

If they put in no capital and used existing equity from elsewhere they are bleeding $3,400 a week in interest @ 5.5%"

If the location of the property is in an area affected by Watercare capacity constraints, the developer may now be sitting on bigger unrealised losses as the market value of the land has fallen.

Holding onto the property will depend on how much borrowing was taken on and how deep the pockets are to support the negative cashflow property. The developers cash reserves may run out at some point if the developers do not have access to sufficient additional capital. Alternatively the valuation fall of the property by say 20 - 25% may prompt lenders to reassess any breach in loan covenants. If the developer financed their purchase with a short term loan - say 5 years to allow for construction, then the developer may face a liquidity event at the maturity of the loan and may face a credit crunch.

What was the 2021 CV of the land value?

$3.2 million paid for 800 sq metres is $4,000 per sq metre for the land.

The CV is around 2.7.. yeah it was over 4,000 a sq m, I repurchased rural at about $21 a sq m, though I do not think the vendor understood they could subdivide.

They are a HK Chinese family who bought it sight unseen, its will not be banned re Watercare BUT the numbers no longer work for that location, if you wanted to build the density they do you should be doing it in st helliors.

"The CV is around 2.7"

Just reconfirming my understanding of the above number on the CV.

The land value ONLY (i.e excluding the improvement value) was $2.7mn?

"They are a HK Chinese family who bought it sight unseen"

Very interesting. Out of town buyer with out of town income levels (which can be much higher than local residents) & assets used to purchase the asset perhaps? - this is how out of town buyers can outbid local owner occupier buyers on local earning incomes in the existing residential dwelling market.

I'm assuming someone in the family was an eligible NZ resident to register the purchase in their name to overcome the foreign buyer ownership rules currently in force. Or if they weren't eligible NZ residents perhaps they used some other owner name to bypass the foreign ownership rules with the assistance of legal manoeuvring?

RV (Jun 2021)

$2,725,000

Increased by 47% (Compared to 2017)

=

Improvement value

$200,000

Reduced by 38% (Compared to 2017)

+

Land value

$2,525,000

Increased by 65% (Compared to 2017)

HK family live in AKL, it was during lockdown level 3 they only drove past no on site view though the other bidders did, Rank group where the under bidder, that was the rate at the time...

Hart wanted it as it was a par 4 from his house.... he would have put exec house on it and put one of his execs in it, the down side from living so close to hart is that he hates the noise of his helicopter so it circles the park just out of his noise range... he often pops back from waiheke to feed the cat etc

I think I know the address of the property which has 834 sq m of land. Will keep the address undisclosed to respect your privacy.

FYI, the current QV valuation is 28.9% lower than your sale price (currently valued at $2,310,000)

For those who are unable to see:

1) If IT Guy wanted to continue living in the same area, he could have taken his profit / net equity of $2,400,000, and put it in the bank earning interest on a 1 year time deposit earning 4.55% p.a (3.185% after tax). The interest after tax would be $76,440, then he could rent the same property for $49,400 per year ($950 per week) for a net saving of $27,040.

2) if the new owners purchased the property using an LVR of 80%,then they would now be in negative equity (excluding any "forced savings" of principal from P&I mortgage payments)

There are conditions when it is better to rent rather than buy.

If the market tanks I could buy back at 50%.

But I am much happier in the country... not going back to the city.

I was in the place for just under 12 years. lots of people who bought the bottom of GFC and sold the top also did well.

Personally I thought property was overpriced around 2017.

House near us sold over 2mil in 2021, it would sell today at best 1.1m. Probably under 1m in a year.

Eyewatering losses are to be seen and likely forcibly realised, in the next 2 years of this property crash.

"House near us sold over 2mil in 2021, it would sell today at best 1.1m. Probably under 1m in a year."

That is very interesting. That is a very significant fall relative to the purchase price, larger than most.

1) What is the address?

2) was it purchased by buyers with an intention to develop or landbankers?

You don't seriously think you are going to be able to fact check that do you ?

"You don't seriously think you are going to be able to fact check that do you ?"

That is an incorrect interpretation of the purpose.

The reason for asking is to understand why was that fall significantly larger than most of the others. Perhaps something uncommon about the situation or the property.

There are properties that were sold for more than 90% below the vendor’s purchase price in NZ. These had commonalities. For these vendors, their property may have been the majority of their net worth and they had to realise a 90% fall from their purchase price.

That's about the size of the tax cut national gave us....

It is not! I got $20 from that tax cut, meaningless, $150 on the other hand changes things quite a bit, in my case 10 years of the mortgage.

Oh I see now why you have your opinion on the housing market, you're one that profited from being in the right place at the right time.now you like oh na that was bad should never let that happen again...🫣🤑

No I am not saying that, I am saying it cannot happen again because the banks cannot lend credit into a fairy tail...

you sound a bit jealous of past trading opportunities?

You will be able to participate in the next rise... if you wait until it bottoms out...

You sound like you would ban the share market because sometimes it crashes...

Just an aside, there's a certain irony in that last sentence, when we consider the property market and central banks/govts efforts to ban crashes.

Exactly since 2008 our government and the RBNZ have done everything in their powers to prevent house prices from ever falling and keeeping our private debt to GDP at extremely high/risky levels (140-160% of GDP). Even investors were then saying things like ‘they will never let house prices fall because look at what they’ve done in the past’ and ‘it’s too big to fail now so it’s impossible to lose as it will always get bailed out’. Then I would say in reply ‘do we have free markets in this country or is our housing market controlled by the state (ie communist that sets the price of housing?’ To which there was silence. Vested interests are/we’re happy getting rich off housing as governments/central banks propped up their investments through OCR drops, high migration, ridiculous amounts on welfare/accommodation supplements (that go into the pockets of investors and not the poor/needy, mortgage holidays when the going got tough, Fundung for Lending programs paid for by the taxpayer/provided by the central banks used to allow retail banks to lend more against the housing market as an ‘investment in the country’ - instead meaning to prop up house prices to prevent them from falling. These same people would then say how lazy and corrupt poor people are, who also happened to be the tenants in their rentals, and how lazy the poor are needing so much support from the government to make rent, and how stupid poor people are/were because they were pro nasty socialism - and yet it has been those with the most capital who have been receiving almost all of the financial benefits of this country’s socialist type policies. The hypocrisy is completely off the charts.

Almost all our problems stem from having far too much private debt (in housing) relative to our productivity (GDP) - and yet almost every action governments and central banks have made we’re done to ensure this root problem never got resolved. And I still don’t think they get it - that unless private debt to GDP falls back down towards 100% or less, we are going to be a complete cluster of a country (so still need another significant drop in either nominal price terms or real terms via higher inflation). And fixing that is going to be extremely painful for those who have gambled on it remaining extremely high and never falling

The problem is that if the money expansion is not underwritten by RE will it be expanded (sufficiently) at all?

Correct ma and pa paying down housing debt will not be lent money to develop AI based coding startups...

Most didn't even know how to buy an investment property until Propellor, Staircase, property apprentice etc showed up...

They used to do Manurewa but when that flow dried up they went townhouses units and apartments etc.

Our share market is income based NZ monopoly companies, mainly, and if you do have a tech startup your exit strategy is a sale before IPO or listing offshore. Kiwis, unless they have a mil of there own cash have no easy access to startup level funding, like the ice house.

Most of the property investment companies where selling a leveraged super scheme to the gullible. Property together is still advertising its the only way to have a retirement.

Therein lies the entire problem?

Expanding the money supply, introducing new money via RE at the bottom of the pyramid, and storing it at the top. It works until it can't.

Productivity isn't going to happen when all that money is simply chasing the easiest, guaranteed return.

EVEN the rich seem more willing to back tax free property gains,

then new business startups or further investing in there own business interests...

Think about this... what chance for the average IQ Joe ( and 50% are ... less then average IQ....)

So if in NZ even the smart (or lucky) rich do not seem to historically wanted to sink their dosh into "growth growth growth" then

who can now ?

Maybe my past experiences of tax free massive capital gains makes me look at the "growth growth growth" opportunities in NZ and say Yeah nah.

I suggest that the wealthy NZers, in general, are donkey deep in property here and now, and cannot be relied on for any form of

"growth growth growth" funding.

Disclaimer: My use of "Growth Growth Growth' acknowledges its possible trademark to the National Part....

Amen. Worth noting that the economic growth and productivity increases through the 90s and 00s were mostly the direct result of that expansion of the private sector balance sheet - the increase in private debt as % of GDP you reference. We can only contract the private sector balance sheet by reducing private sector bank account balances (shrinking GDP). Unless, the public sector balance sheet expands to compensate of course.

Sh*t yes...I am most definitely jealous of past trading opportunities!! 😂

We've done ok, created some equity (yep...still in the positives), but certainly haven't turned water into wine like you did with that one!

Surely your "time in the market" is the key phrase eh, is property a good investment...maybe, if you can afford it, I do believe it is cyclical and looking at history I disagree with the comparisons to Japan, I think we lean more towards Ireland, so if people are patient (and able to ride out the storms) then they will see long term returns, maybe it'll take longer this cycle. But if the only way to do it is to leverage yourself up to the eyeballs then maybe don't, I listened to a podcast with the fella from Opes recently and couldn't help but think it was a bit dangerous how they "teach" people to maximise leverage.

I also think that the NZ property mentality hasn't changed as much as a lot of commentators on here think, some of the younger more intelligent kiwis might not touch it with a barge pole, such as those who take the time to read and comment on this website...but I think it is fair to say that there are lot more of the opposite out there and when that pendulum swings, and test rates drop and access to $$ eases it will kick-off, when is that...f**k knows, probably not anytime soon, unless Orr panic slashes and eases/removes restrictions then it might be closer than we like to think.

If the latter does happen then I really hope it can be focused on new builds (decent ones) that at least put a share of that $$ back into more areas of our economy, yep probably including Ford and Stabi dealerships, and not just the rinse/repeat of selling existing houses to each other.

Maybe that makes me a spruiker 🤷🏻♂️ Maybe it just makes me a fella with an opinion who has a sh*tty crystal ball 🔮

I was only in that property for 11 years from the low of the GFC to the month of the peak of the covid madness

Timing is everything when using leverage.

You are trading land not property if you want to make those numbers, stay well away from sites that cannot be developed,

It cost as much as a ponsonby villa when i got it, but it had land...

Interested if you've run the numbers on what the actual profit after all costs was on that place? Minus interest, insurance, rates, maintenance, purchase and sales costs. Given it was pretty much the best possible case scenario over those 11 years, I wonder what the true return was per year?

"I wonder what the true return was per year?"

Based on publicly available data, the house price grew 11.87% p.a from the purchase price in 2009 to the sale price in 2021.

I bought it as a great investment but I lived in it the entire time, my kids could walk to a great school and not have to cross the road.

Max i dropped in was 30k to add a deck, a 2nd hand in deck old spa, a para type pool, and re did my girls rooms myself so they where warm in winter and new carpets etc... we had a 1970s bathroom ourselves with curtain over an old tin bath. I put insulation above and under myself to save money.

Anything we dropped in would have been lost $$.it was all about the land.

I never calculated interest etc as I did not care, it was a home.

When we got there, no fences between either sides... lawn cricket was amazing, as a homebrewer we hosted more then a few keg parties. It was well leveraged as we had other investments, so the actual return was well higher then the 11% PA.

I am no DGMer but this is not going to happen again in my lifetime.

if it was I would be in boots and all.

Well don’t worry about bank profitability in the great refixing - margins over swap rates are still well above Oct 2023 and banks will continue to hold onto the bulk of those margins while throwing out some peanuts. More to the point are all the comments on articles coming from “supporters” of interest dot co dot nz. Going to be interesting after March how many sprukers will be able to afford registering and commenting

When that tide goes out, I am going to look away.

But the Emperor has a new suit, cut from the clothe of growth?

I am a right voter, but as i posted on another forum ...

And you can see that as soon as interest rates rise the entire economy tanks, because that is all there is. The NZ economy is like a heavy drinker who is dying from drinking, but also will die if they go cold turkey. It has reached a stage of impasse at the democratic level – neither of the big parties wants to do anything meaningful because to do so guarantees a recession which the other party will exploit.

I do not believe that the left is willing to make the necessary changes either, I am not sure that NZers would vote for cold turkey.

They would all rather linger on, hoping they can dump their property/investment at the next boom to another sucker...

I have and did last time. Resounding defeated. No one leveraged cares about the next generation and complains when grandchildren can only be visited in Straya or further.

I like a "drink" as well, but in moderation and avoiding parasitic addiction.

Yes, it was interesting to see only Bishop and the odd other saying prices need to drop (hamstung by Lux etc though so could be performative), while Kieran McNulty and others continue "well, we don't want house prices to fall"...

Labour's name is pretty meaningless now

We are refixing next month at a much lower rate, however I'll keep the repayments the same. I wonder how many of those refixing at lower rates will use their surplus to spend, could we see a resurgence of inflation perhaps.

Interestingly, in Australia the recent tax cuts that were implemented did not result in extra spending, but was directed to paying down debt. So did nothing to stimulate the economy or inflation. I can imagine a scenario where interest rate reductions are simply used to also start paying down debt. Often when you've gotten used to not spending on things, you get out of the habit of spending even when you get more money, and simply start saving it.

Investing it elswhere.

4.95% fix for 5 years runs out December 2026. I'm hoping the 5 year rate is the same when we to go refix.

Well done! You've managed to avoid the nasty rates of the last 24 months. By late next year you may well be rolling on to a similar rate :-)

current about 5.7... back before the GFC i fixed at about 5.85 5 year and it was a great rate the entire 5 years, rolled off onto a 9.75% float... then the gfc cuts rolled in....

historically 5.75 for 5 years in NZ has been considered cheap, very cheap.

its only since QE and covid we seem to think low rates are required...

The savings on mortgage repayments should just about be enough to cover 2025 increases in local authority rates and home insurance premiums 😊

I'd love to know what these people think rates are going to drop to. Is there a % who are expecting 2-3% again? Are those who are floating are planning on selling or otherwise paying down their mortgages or they are floating to wait for the big drop? If they are waiting for the big drop I wonder if they've done their sums and know how much it needs to drop by so it makes it worth paying the higher floating rate.

Those low rates are not coming back anytime soon. Anyone can see the damage they did when property prices went ballistic, they were just handing out free money that will take a decade to recover from. Rates are already low, I never had a mortgage on rates this low the best I can remember was 6.3% and that was only because my partner worked for a bank.

Quite a few will be coming off low rates going onto higher rates, more people than you would realise

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.