The Reserve Bank (RBNZ) has cut the Official Cash Rate (OCR) to 3.75%, from 4.25%.

After this widely expected move, all eyes will be turning to what comes next. And it looks like there will be more cuts.

The RBNZ's new forecasts contained in the February Monetary Policy Statement show the RBNZ is forecasting the OCR will likely be around 3.00% by the end of 2025. That's about 50 basis points lower than the central bank forecast in its last review of 2024.

The official record of the RBNZ's Monetary Policy Committee meeting said expectations of future inflation, the pricing intentions of firms, and the degree of spare productive capacity are consistent with the CPI inflation target being sustainably achieved.

"This provides the context and the confidence for the Committee to continue lowering the OCR, and at a faster pace than projected in November."

The committee said consumer price inflation in New Zealand is "expected to be volatile in the near term", due to a lower exchange rate and higher petrol prices.

"The net effect of future changes in trade policy on inflation in New Zealand is currently unclear," the MPC said.

"Nevertheless, the committee is well placed to maintain price stability over the medium term. Having consumer price inflation close to the middle of its [1% to 3%] target band puts the committee in the best position to respond to future inflationary shocks," the committee said.

"If economic conditions continue to evolve as projected, the committee has scope to lower the OCR further through 2025."

The Kiwibank economics team have long been pushing for the OCR to go much lower than the RBNZ has been indicating.

Kiwibank chief economist Jarrod Kerr said on Wednesday the main message from the latest OCR review is the lowering (again) of the OCR track.

"The RBNZ are signalling more cuts, sooner. The RBNZ has effectively matched market pricing, and moved closer to our long-held view of a 3% terminal rate," Kerr said.

"It pays to be stubborn. And we agree with the move. We're all on the same page, now."

Wednesday's decision means the RBNZ has now trimmed the OCR by 175 basis points since August of last year, taking it down from the peak level of 5.50% it was at for over a year.

Moving on mortgages

Banks have been similarly trimming their mortgage and deposit rates. They had been moving rates ahead of Wednesday's OCR decision and more falls are quickly following.

Over half of the country's $370 billion mortgage pile is due to have an interest rate reset in the first half of this year, so, customers will soon get the benefit of cuts.

The 50 point cut had been widely anticipated by the market because Reserve Bank Governor Adrian Orr had given clear guidance after the last OCR decision for 2024 on November 27 that the bank's forecasts were "consistent" with another 50 point cut in February.

The RBNZ has been cutting the OCR after gaining confidence that the period of elevate interest rates has helped to rein in inflation.

Inflation soared through 2021-22, peaking at 7.3% in June of 2022. The RBNZ responded by hiking the OCR all the way from just 0.25% till the start of October 2021 up to that 5.50% mark in May 2023.

Inflation responded slowly at first, but was as of the December quarter on 2.2%, putting it well within the aimed for 1% to 3% range and just above the RBNZ's explicit target of 2.0%.

However, the RBNZ is expecting that a lower exchange rate and higher oil prices will help to drive up 'headline' annual inflation again this year, reaching a peak of 2.7% in the September quarter, but the RBNZ says inflation will stay in the 1% to 3% range.

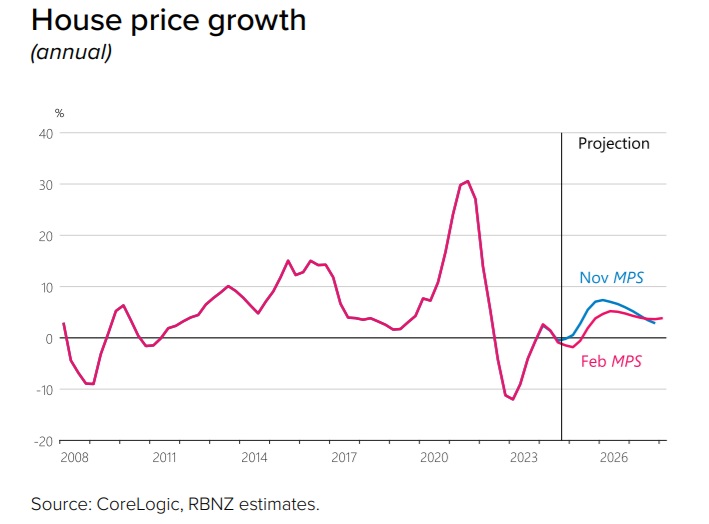

Lower house price growth

Although it doesn't comment on it directly in its February Monetary Policy Statement (MPS), the RBNZ has quite sharply trimmed its house price inflation forecasts compared with the last MPS in November.

In November the RBNZ was forecasting house price inflation for this calendar year would be 7.1% and the house price gain would peak at 7.4% in March of next year.

However, now, the RBNZ's forecasting house prices will rise just 3.8% in the 2025 calendar year and the peak annual growth will be 5.2% in June of 2026.

The 3.8% forecast for house price growth by the RBNZ for this year now puts it somewhat lower than some of the major bank economists, who see 6%-7% growth this year.

This is the statement from the Reserve Bank:

Annual consumer price inflation remains near the midpoint of the Monetary Policy Committee’s 1 to 3 percent target band. Firms’ inflation expectations are at target and core inflation continues to fall towards the target midpoint. The economic outlook remains consistent with inflation remaining in the band over the medium term, giving the Committee confidence to continue lowering the OCR.

Economic activity in New Zealand remains subdued. With spare productive capacity, domestic inflation pressures continue to ease. Price and wage setting behaviours are adapting to a low-inflation environment. The price of imports has fallen, also contributing to lower headline inflation.

Economic growth is expected to recover during 2025. Lower interest rates will encourage spending, although elevated global economic uncertainty is expected to weigh on business investment decisions. Higher prices for some of our key commodities and a lower exchange rate will increase export revenues. Employment growth is expected to pick up in the second half of the year as the domestic economy recovers.

Global economic growth is expected to remain subdued in the near term. Geopolitics, including uncertainty about trade barriers, is likely to weaken global growth. Global economic activity is also likely to remain fragile over the medium term given increasing geoeconomic fragmentation.

Consumer price inflation in New Zealand is expected to be volatile in the near term, due to a lower exchange rate and higher petrol prices. The net effect of future changes in trade policy on inflation in New Zealand is currently unclear. Nevertheless, the Committee is well placed to maintain price stability over the medium term. Having consumer price inflation close to the middle of its target band puts the Committee in the best position to respond to future inflationary shocks.

The Monetary Policy Committee today agreed to lower the Official Cash Rate by 50 basis points to 3.75 percent. If economic conditions continue to evolve as projected, the Committee has scope to lower the OCR further through 2025.

Summary of Monetary Policy Committee meeting:

Annual consumer price index (CPI) inflation is sustainably within the Monetary Policy Committee’s 1 to 3 percent target range, and measures of core inflation are continuing to converge to the midpoint. Measures of firms’ inflation expectations sit close to the target mid-point.

A period of restrictive interest rates has reduced demand in the New Zealand economy and contributed to lower inflation. Subdued global economic activity, falling net immigration, and lower government consumption have slowed domestic demand. Increased policy uncertainty associated with global trade developments is also expected to decrease business investment. Headline inflation is expected to increase in coming quarters but remain within the target band. This increase reflects a lower New Zealand dollar exchange rate and higher oil prices. The Committee expects these relative price shifts will not affect inflation over the medium term. Expectations of future inflation, the pricing intentions of firms, and the degree of spare productive capacity are consistent with the CPI inflation target being sustainably achieved. This provides the context and the confidence for the Committee to continue lowering the OCR, and at a faster pace than projected in November.

Global economic activity is expected to remain subdued

The Committee noted that GDP growth for many of our main trading partners remains below potential. In contrast, economic growth in the US has remained strong. Trading partner GDP growth is assumed to decline slightly over 2025. Global economic uncertainty has risen significantly since November, following recent trade policy announcements by the United States. In the near term, we expect that heightened economic uncertainty will constrain business investment amongst our trading partners and in New Zealand.

Global headline inflation has increased modestly, reflecting higher energy prices

The Committee discussed inflation amongst New Zealand’s trading partners. Headline inflation has declined over the past year but has increased slightly in recent months. The recent increase in headline inflation in many of our trading partners is largely accounted for by higher fuel and energy prices. Market participants expect most central banks in advanced economies to continue reducing policy interest rates over the coming year. Market pricing implies that US policy rates are projected to fall by less than assumed at the time of the November Statement.

GDP growth in New Zealand is expected to rise, reducing spare capacity in the economy

The Committee discussed recent domestic economic developments. Domestic economic activity remains below trend. This reflects falling activity in interest rate sensitive sectors such as construction, manufacturing, retail trade, and business investment. In contrast, activity in the primary sector has increased. New Zealand’s export prices have held up, despite subdued global growth. Global supply conditions in beef and dairy markets have supported export prices. This, coupled with a lower New Zealand dollar exchange rate, will increase export sector incomes in New Zealand.

Timely indicators of economic activity, including a range of business surveys, have improved in recent months. Lower interest rates and higher export earnings are expected to support economic growth. The pace is expected to be modest, as potential GDP growth is constrained by ongoing weakness in productivity growth and lower net immigration. Government spending is expected to decline as a share of the economy over the medium term, in line with the Half-Year Economic and Fiscal Update 2024.

GDP revisions better explain the evolution of core inflation over the past two years

GDP data was revised significantly since the November Statement. These revisions show that the level of New Zealand’s economic activity in 2024 was higher than assumed in November. However, the revisions show the New Zealand economy experienced a larger contraction during the middle of 2024. Overall, there is significant spare capacity in the economy, and slightly more than we had assumed in November.

The new profile for GDP helps explain the evolution of core inflation and broader measures of capacity pressure over the past two years. The higher level of GDP over the start of 2024 aligns with the signal taken from high frequency data at the time. The subsequent decline in GDP over the middle of 2024 also aligns more closely with high frequency data, which was one of the factors that contributed to a downwards revision to the OCR outlook in August.

Employment remains subdued, but is expected to improve later this year

The Committee discussed conditions in the New Zealand labour market. Wage growth is slowing, consistent with lower demand for workers and lower CPI inflation. Employment levels and job vacancies have declined, reflecting subdued economic activity. As employment growth typically lags economic growth, it is expected to pick up in the second half of the year. Net immigration to New Zealand has reduced significantly from high rates over recent history. The number of migrant arrivals has slowed over the past year, and departures of New Zealanders have increased, partly in response to subdued labour market conditions relative to Australia.

Lower OCR continues to pass through to mortgage and term deposit rates

The Committee noted that wholesale interest rates in New Zealand have generally declined since the November Statement, in response to a lower OCR and weaker-than-expected economic activity. This decline in wholesale interest rates has been reflected in lower mortgage and term deposit rates. The average interest rate on outstanding mortgages has now peaked and is expected to decline over the next 12 months as borrowers refix their mortgage interest rates at lower levels.

The financial system remains stable

The Committee agreed that there is currently no material trade-off between meeting inflation objectives and maintaining financial system stability. Some households and businesses are continuing to experience financial stress. While non-performing loans remain low compared to past recessions, some financial stress will persist in the near term, even as the economy recovers. The banking system remains well capitalised and in a strong financial position to support customers.

Inflation is expected to remain within the target band

The Committee discussed domestic inflationary pressure. Headline CPI inflation and firms’ inflation expectations at all horizons are close to the target mid-point. Measures of core inflation continue to converge on the target mid-point. Surveyed household inflation expectations remain more elevated and volatile.

Non-tradables inflation has fallen but remains high. With spare productive capacity remaining in the economy over the next 12 months, the Committee is confident that domestic inflationary pressures will continue to abate.

Headline inflation is expected to increase in coming quarters, reflecting a lower New Zealand dollar exchange rate and higher oil prices, but remain within the target band. However, underlying inflationary pressures are expected to continue to ease, and annual headline CPI inflation is forecast to remain near the 2 percent mid-point once the effect of recent increases in petrol prices on inflation wanes. The near-term increase in headline inflation is unlikely to significantly affect wage- and price-setting behaviour given excess capacity in the economy. The Committee noted that the monetary policy remit directs it to discount disturbances in inflation that are expected to be temporary, in a manner consistent with meeting the medium-term inflation target.

There are near-term risks to the economic outlook

The Committee discussed near-term risks to the outlook. The Committee noted that while lower interest rates are expected to underpin a recovery in the domestic economy, the speed and timing of the recovery is uncertain. In particular, recent revisions to June and September 2024 quarter GDP growth suggest momentum in the economy was considerably weaker than previously measured. The Committee noted that tighter international financial conditions presented downside risks to global growth, particularly for those countries with high debt levels or fixed exchange rate regimes. The Committee discussed global asset markets and the risk of a fall in equity prices if elevated earning projections are not realised, or if market participants reassess their appetite for risk.

There is a risk of increased trade barriers and broader geoeconomic fragmentation

The Committee discussed the risks posed by increased trade barriers. Over the medium term, these trade barriers could be increased much further. This is not currently incorporated into our central projection given uncertainty about the timing and magnitude of any potential changes. This uncertainty is heightened given trade protection is being used to pursue both economic and geopolitical goals.

Increased trade barriers will reduce global productive capacity. As a small open economy, New Zealand cannot avoid being affected by these international developments. Monetary policy cannot offset the long-term negative supply-side effects of higher barriers to international trade. More generally, global economic activity is likely to be more exposed to economic shocks given increasing geoeconomic fragmentation.

An increase in trade restrictions is likely to reduce economic activity in New Zealand. But the effects on inflation are uncertain, as these depend on how trade disruptions transmit through the global economy. Such shocks are likely to take time to materialise, giving the Committee flexibility to react as necessary. Any monetary response will depend on the impact of trade restrictions on medium-term inflationary pressures.

The global economy faces a range of structural challenges

The Committee discussed the long-term structural challenges faced by the economy in China and the broader region. In addition, the Committee noted that geopolitical and climate-related risks pose uncertainty over the medium term. There may be higher relative price volatility and more unpredictability in headline inflation. The Committee agreed that having consumer price inflation close to the middle of its target band puts it in the best position to respond to any shocks to inflation.

The Committee agreed to lower the OCR

With headline CPI inflation close to the midpoint, measures of core inflation converging on the midpoint, stable business inflation expectations, and significant spare capacity in the economy, the Committee agreed that a further reduction in the OCR was appropriate. The Committee agreed that a 50 basis point reduction would be consistent with their mandate of maintaining low and stable inflation, while seeking to avoid unnecessary instability in output, employment, interest rates and the exchange rate. If economic conditions continue to evolve as projected, the Committee has scope to lower the OCR further through 2025. On Wednesday 19 February the Committee reached a consensus to lower the Official Cash Rate by 50 basis points to 3.75 percent.

90 Comments

No suprises there. 50 bps cut. 75bps jawbone with maybe one eventuating.

Surely you must be surprised, given your 0.25% cut prediction of last week.

Yep, that was your post of this week, would you like to share what you wrote last week ?

Calls change depending on new information - my latest call was very much in line with what happened.

Some people, like Yvil, don't change their calls based on new information.

That is why he is calling house prices incorrectly for about 3 years now.

Here is another one that we could all benefit from that didn't eventuate:

by Yvil | 22nd Jun 21, 9:55am

It has been made abundantly clear to me over the last weekend by multiple posters that this forum is no longer a place to exchange ideas and help each other but a place to vent frustration, complain and blame.

This is not my idea of participating in discussions and I will therefore now stop posting (but still reading Interest's great articles).

Good luck to you all!

So you admit flip flopping in your calls, but hey, you made the right call 2 days before the announcement, amazing, kudos to you LOL.

Adjusting calls based on new information. You know that is how these things work right? Oh wait, no you don't, house prices up forever.

People were already sick of you four years ago. Can you please enable your promise above, thanks.

@Toye I am not sick of Yvil

Neither. But when I see a post from Toye I know it will soon blossom into a long thread of defensive whinnying.

It'll be worth the pay-off if it turns out to be a Doctor Yvyll and Mister Toyde type situation.

It's quite bizarre that people would "get sick" of certain monikers on a financial news website, turning them into a sort of "arch nemesis".

But I guess we're all different, some people are more sensitive than others.

I often don't notice the moniker when reading a comment but realise who they are after reading half way through the first sentence, look at the name and think, damn, I'm not wasting any more time reading more of that. It's probably that comments are just repetitive, you already know their position, and that they are set in their ways.

by Yvil | 22nd Jun 21, 9:55am - "I will therefore now stop posting"

Ooops, someone dropped the ball. Perhaps next time consider your own credibility.

@Toye - are you suggesting this is the last cuts and due to Trump - if so trademark that call please.

They may be, or more accurately, they should be. Orr has been wrong plenty, plenty times before, and he may overcook it on the way down too.

Currently the world is a geopolitical powderkeg and most of this deterioration is inflationary. It doesn't bode well going forward in terms of price stability.

@Toye could be should be ? Your comment stated it is no longer going to go down - Trademark it.

You're suffering from TDR.

He's bringing the wars in Ukraine and the Middle East to a close. The world is healing.

Given what Governor Orr has said (and the tone/ conviction with which he has spoken) it's on the cards that more house buyers will emerge from the woods in the near-term. The sweet scent of cheap money is enticing to NZ property buyers - and there are plenty of them.

We know that market stagnation always has an end-point ......

We might well look back in a while and recognise today as being the market's turning point.

TTP

Disagree. I think we are still 75-100 BPs away from a real turning point in the property market. And even then, a gentle upturn

People bragging about getting their predictions right might be the most inane part of the comment section of this site, especially when it is about something as widely signaled as this OCR cut

Bye Bye NZD... Hello housing Ponzi?

.8951 against the Aussie.

As it drops the incomes in Australia look even better, so more people leave, further slowing inflationary pressures, so rates fall further, dollar drops some more, making incomes in Australia look even better...

Houses in Aussie look even dearer as the exchange rate drops.

Most would be lured by the multiples more they'd earn in Aus over the coming years compared to what they lose from a lower NZD/AUD while transferring their cash/super.

The people who go to Australia are battlers who have struggled to get ahead and younger gen’s for the more vibrant city life. The semi-well off and above have tremendous lifestyles in NZ and don’t need to go anywhere.

Dollar drops but prices don't go up? That'd have to be stacks of people leaving, surely?

He'll probably take the OCR to 1.5 - whatever it takes for us to start borrowing $$ again. That's how it works, it's a game, then you die - Game over.

I said this before, rates will be slashed to protect the banks at all costs while the Kiwi $ is thrown into Mount Doom.

The new marketing strategy may be brilliant, the country is on fire sale if you can access hard currency. We squabble over whether house prices are crashing or not, that they are in freefall in hard currency terms is irrefutable.

Shock and Orr, who would have thought a 0.50% cut was coming ???

Almost everybody with an ounce of understanding though the goalposts were certainly shifting for the last few weeks.

May I introduce you to the Interest comments section, which you must be very unfamiliar with. Many posters predicted a different outcome than a 0.5% cut, even a guy called "Toye" who wrote just last werk that a 0.25% cut was the most likely outcome

May I introduce you to the comment where I said 50bps with a 50 jawbone two days ago.

The situation is constantly changing so clearly the calls will as well.

If I had to bring up all the wrong things you've posted over the last few years I'd need to quit all my hobbies to write a book.

Given that over the last 3 months you have said 0.5, no cut, 0.25 last week on 0.5 two days ago, you're chances of getting one prediction right is pretty high !

Its almost as though new information has pushed me from a lower cut position to a correct 0.5bps position as we got closer to the OCR date. Who would have thought?

What were your house price predictions again?

My house prediction for 2024 was down -10%, and I admitted several times that I was wrong. You should try saying/writing these 3 simple words too "I was wrong", it's very liberating

BTW, good attempt at deflecting from the OCR subject.

The issue is I wasn't wrong about this particular call, even though I've been wrong about plenty things before - just like you.

So, would you like to admit you were wrong about your earlier post today saying that I claim :"house prices up forever" when I predicted a fall of 10% in 2024 ?

by Toye | 19th Feb 25, 2:58pm

Adjusting calls based on new information. You know that is how these things work right? Oh wait, no you don't, house prices up forever.

You guys are like a couple of immature bickering teenagers on instagram. Maybe grow up a bit, both of you?

There's like 30 posts on here between you offering nothing of value. Brilliant contributions, you should be proud.

I have 100% record of forecasting it's raining. The trick is to wait until you feel a few raindrops

Or is the trick to forecast the rain 3 months early? That's what the Met does, right?

That was the easy part. Where to from here Yvil? After this 0.5% I have been predicting 3 consecutive 0.25% cuts then hold for a while now. What are your predictions?

It always looks easy once the decision has been made (and you have made the right call).

Calling it months in advance, not flip flopping at every new data release and using the prediction to fix your mortgage for the right term, thus saving thousands of dollars, seems a bit trickier though.

Sure, I called it months in advance too (in fact the RBNZ basically told us). Can we get your future predictions a few months in advance?

Nope, sorry.

I will play the game!

I think there’s a good chance you will be right.

But just to be different - I go 50BPs then 2 x 25

I think economic news over the coming months is going to keep looking ugly

The 50 point cut had been widely anticipated by the market because Reserve Bank Governor Adrian Orr had given clear guidance after the last OCR decision for 2024 on November 27 that the bank's forecasts were "consistent" with another 50 point cut in February.

Got to keep the house ponzi going...if they can? The system can only run on continued credit..it seizes up if no new loans are minted.

Thank you for your acknowledgement Baywatch, much appreciated!

Orr continues his signature style. Wild oversteer, follow by wild understeer. Rinse and repeat. NZD takes a nose dive. Wait till that flows thu on inflation on all imported goods and everything moved by fuel.

Incapable of learning from their last mess. How long will they look through the new incoming inflation before they’re compelled to raise again?

Any inflation over the next few year or so is "transitory", don't you know it

The rest of the drops are a jawbone. Even Orr isn't stupid enough to drop into rising inflation. By April we should see more signs of it, maybe one more 25er

Yes the market will start discounting the reality of the next 50 points if inflation rises.

In an overheating or even neutral economy businesses pass those costs on and people are confident enough to absorb those costs.

In this economy people are not confident enough to absorb costs and will change purchasing patterns. Businesses will not be able to pass those costs on then. This will be offset by cheaper money into businesses i hope, because otherwise businesses have to pull back or cease trading.

"Orr continues his signature style. Wild oversteer, follow by wild understeer. Rinse and repeat"

Since you understand this, you should be able to predict his future OCR moves quite accurately, as long as you differentiate between what you think he "should" do, and what you think he "will" do.

Should have dropped 75bps. Economy is flatlining.

"Economy is flatlining." - how do we know? I suspect we are growing now (or will be very soon), but we won't know for a long time as GDP stats are so laggy.

JimboJones ; "I suspect we are growing now (or will be very soon)"

And you have facts to back up that "I suspect" statement?

Or is it just another 'reckons'?

And by the way, we'll need to be growing at 7% to make up for the ground our awesome monetary policy (/sarc) has robbed us of over the last 20+ years !!!

No I don't have any facts, I thought that was obvious when I said "I suspect".

We won't know for a fair while whether we are growing right now. But the thing that stopped us growing (increases to OCR) is now going in the opposite direction, hence my suspicion.

Ah. So let's be clear, statements like:

"No I don't have any facts, I thought that was obvious when I said "I suspect".

Will be the sole reason why I'll not be paying for a interest.co.nz subscription.

I.e. if I want to waste my time with drivel, FB works. But X is even quicker!

Don't you pay for the subscription to support the content of the site?

Also the subscription requirement should cut out a lot of the drivel should it not?

We aren’t growing. We are still going backwards. I own business interests in five countries. A manufacturing business focused on the NZ market is the only one struggling, i.e. I am always considering whether shutting up shop is a better option. It’s really tough out there, I have no idea how the really small operators keep their chin up day in, day out.

Agreed. I now expect the next two reviews to be 0.5, whereas today should have been 0.75 followed by 0.5 followed by a closer assessment that would have been .025 or 0.5. But my guess now locked in for another two 0.5ers!

I do find it odd that when inflation is flat and perfectly inside the mandates band and unemployment isn’t particularly bad, that people are calling for emergency .75 cuts to the OCR.

But when inflation is 5% and miles outside the mandated band and unemployment is at record lows they also call for a ‘wait and watch’ approach to lifting the OCR.

The double standards are at the extreme.

Agree - although you forgot about the fact we have also had many quarters of GDP decline and unemployment is a lagging indicator.

I think they will take it a bit more cautiously from here, probably only 0.25% cuts back to 3% then hold. Unless we get some significant changes in data.

This is NOT going to make NZ a more attractive place to live or do business. NZ has momentum - just in the wrong direction.

There will be some winners/wins though. Obviously mortgage holders will be happy and the weak NZD will see some nice agricultural returns.

Celebrating small wins based off an extremely weak NZ dollar, in a prolonged recession with record government spending is a sign of a very sick economy! The tourism and housing Ponzi tricks may seem like tried and true methods to drive the economy forward, unfortunately for both the government and RBNZ this could be the last kick-of-the-can left.

It's all brick wall from here baby!

Sensible stuff from the RB. They're willing to look through tradables while moving to underpin what is a poorly performing economy.

Sad state of affairs that once again a housing boom is the only game in town and that is what's ultimately going to come to the rescue...if you want to call it that.

The captioned graph evidencing the rocketing up of house prices in 2020 says it all. Crash diving interest rates, too low and then too long, promoted a stampede into property investment/speculation and resultant boom! boom! boom! Simultaneously the RBNZ wilfully printed money and the sixth Labour government wilfully spent it. And here we all are then.

Exactly and those with TDs were getting under 2%, so were pulling their money out of banks & into property. I was lucky as I missed the boat on an affordable property, so bought gold instead.

New all time high for gold in Kiwi pesos - $5,174. Now up close to 50% in past 12 months.

Meanwhile Ted Cruz is enthusiatically saying he and others should check out the gold stored at Fort Knox as it has been checked on forever. Actually Steve Mnuchin did when Trump was President the last time.

Regretting selling mine late last year, thought we must be getting near the top at NZD$4300/oz. Got that one wrong.

Well anything but a 50 basis point cut would have a wee bit of a surprise but to be honest I'd have held steady.

We have to borrow from somewhere and getting Foreign investtors to place their money into NZ bonds won't be quite enough Nicola.

Do we really think a housing boom will come to the rescue? Possibly some affordability for FHBs, and lighter load on existing mortgages. But the bidding up madness? I don't see it happening.

There will be more confidence in the business world.

Labour killed the economy big time and any business person will tell you that.

If you are a Public Servant or rely on welfare then you will not like What ks going on to try and get NZ moving again in the right direction.

The last government set NZ back a decade or two which is going to affect most people for a very long time.

good bidding at an auction room today with 17 from 22 sold in ChRistchurch but then again so many people are wanting to live here.

"so many people are wanting to live here" - 408,000 of 8,025,000,000

Geez knew there was immigration growth but up 3 million since yesterday?

He is referring to the worlds population!

Yeah nah, property investors, incompetent governments and a negligent central bank have set NZ back a decade or two.

If there is another boom in prices, it really only benefits older generations and increases the wealth gap with the young who have not purchased a house. But anyone who only owns the house they live in don't really benefit from house prices increasing, add you can't eat your house

I think there is a benefit to everyone if the median wealth increases, people spend more when they have wealth, even if it is paper wealth. But yes obviously it isn't great for FHBs.

If it's just paper wealth, they have to borrow to spend? How's that been working out for us?

I felt better 3 years ago than now.

you have the same life only your paper wealth has changed.. especially if you belong to the church of

Time in the Market....

why worry in 50 years house will be worth more remember... the church of holy house price rises welcomes all

only us traders can ever win or lose....

Interesting Orr seems to think current DTI/LVR settings will stop another housing bubble. They seem pretty loose...

100% agree.

But to put this into context, Orr & the MPC must construct an economic 'revival' ready for the next election.

And, as past history has shown, the economy 'booms' when house prices rise. Saddly though - we all feel poorer. Why is that? [rhetorical question]

What if - this time - we get smart and don't feed the banking Ponzi? What then?

(Jfoe is likely to have a view.)

Some take home points:

The public has helped Adrian dig himself out of a hole he dug through bad decisions 3 years ago - not the other way around

The Reserve Bank predictions in Nov werent as good as the big banks (despite having employed more staff)

Ok banks can borrow for 3.75% and lend for 6.89% nice almost100%+ mark up chaps

I don't know if media understand that the OCR doesn't change fixed rates which are set from other factors - nor does the media understand if you are on a fixed rate for 1 year this doesn't mean any improvement in the next 12 months

Exactly right.

The media relies on general ignorance to be able to peddle that OCR drops = immediate fixed rate drops when they largely occur in the days and weeks before.

Lets all remember that NZME own both the Herald and Oneroof.

With headline CPI inflation close to the midpoint, measures of core inflation converging on the midpoint, stable business inflation expectations, and significant spare capacity in the economy, the Committee agreed that a further reduction in the OCR was appropriate

Idiots who don't understand control systems.

A lot of hopium in their talk too - and I note the little touch where they may define inflation as 'temporary' by basically ignoring it when they feel like it.

ANZ have just dropped the 2 yr rate to 4.99% on the app!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.