The coming months are expected to see further falls in interest rates, but is it possible our actions might yet sabotage this?

The last quarter of this year is already looking like one you won't want to take your eyes off. And neither, dare I say, will the Reserve Bank (RBNZ).

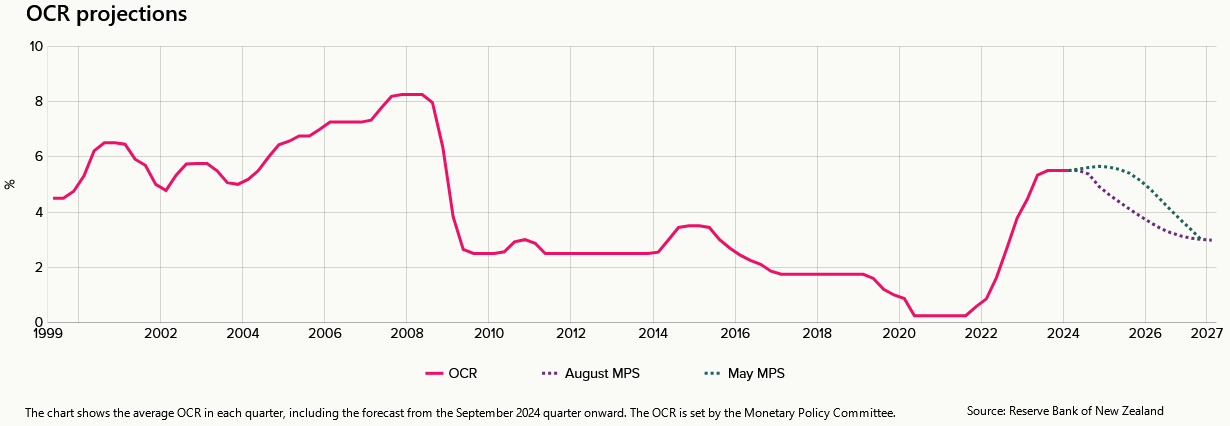

It was only as recently as May that the RBNZ, still concerned about stubbornly high domestic inflation, was indicating we would see no cuts to the Official Cash Rate until the second half of 2025.

And yet, now the RBNZ has already cut the OCR by 25 basis points (to 5.25%) and it is indicating there will likely be two more cuts before the end of this year and probably four more next year, which would take the OCR down to 3.75%.

But of course, the RBNZ can change its mind, particularly if we give it reasons to do so. And just maybe, we might.

I don't think the RBNZ would have been thrilled at all by the extraordinarily strong result in the latest ANZ Business Outlook Survey.

Perhaps this was just letting off steam, a business community giving a collective 'hurrah!' to the fact that interest relief was coming a year earlier than the RBNZ had indicated. And perhaps this will give way to more 'reality' as people realise things are still tough out there.

Maybe not though. Remember, it is estimated that only around a third of the population have mortgages. And they have been the ones bearing the brunt of the high interest rates. What we've seen in the past few months, I think, is that quite a lot of people not necessarily directly affected by high interest rates have stopped spending because, well, they've heard things are tough, so, best to save at the moment.

This mood could quickly switch.

There's a lot of things up in the air. And the fact is the RBNZ can't have been pleased at the part in the business survey in which more firms said they will be looking to increase prices over the next three months. The RBNZ's hell bent on achieving inflation between 1% and 3% so, won't have room for unpleasant surprises.

Inflation figures will be important

The next reading on inflation, as measured by the Consumers Price Index, will be for the September quarter and it's due to be released on October 16. That will be big. The RBNZ has its next OCR review on October 9 and it would be reasonable to assume there will be another 25 bps cut (to 5.0%) then. However, if there's any 'nasties' in those inflation figures the RBNZ might be tempted to pause the interest rate easing.

And will the central bank appreciate, already, that headlines are appearing in the mainstream media questioning when house prices will start to rise and by how much?

I've already said previously that the kind of default setting for the housing market in this housing-centric country is 'frothy' and we never seem to need much encouragement to get the market bubbling again - sometimes from the most improbable circumstances.

I thought it was notable that the July mortgage figures showed the highest level of investor involvement for three years. The investor grouping took only 20.5% of the total mortgage money in the month, but that was up solidly from just 18.6% the month before.

Since hitting heady highs of 35% of the mortgage monies in 2016 the investors have generally been reined in by particularly high loan-to-value ratio (LVR) limits imposed on them. But it is worth noting that the limits have been relaxed recently, although also now augmented with new debt-to-income rules.

The last time the investors had a big surge in activity was amid the pandemic in 2020. In February of that month the investors took just 20% of the mortgage money, but after the RBNZ inexplicably dropped the LVR rules altogether, this share rose to 25% by December of that year.

What will the investors do?

And significantly, this gorging by the investors helped kick the FOMO (fear of missing out) levels up to 11 for the first home buyers. The resultant free-for-all saw us experience a 40% rise in house prices, during a global pandemic.

For me, the investors will unquestionably be the key to the housing market in the next 12 months. If they get heavily involved again then - even though it looks unlikely now - there could be fireworks.

So, there's no doubt the RBNZ will be watching the (currently dormant) housing market like a hawk for any signs of trouble.

Much really depends on the extent to which the recession we are in has been fuelled directly by hardship (and that's got to be the case for at least some mortgage holders). But it's really hard to get a reading on that.

How much of the downturn, particularly in the June quarter, has as much as anything been mood-driven? Things are tough, rein it in - even if you CAN actually afford to buy things.

Well, moods change and the mood of the country has seemingly already lifted. How much difference will that make? And how quickly?

I was intrigued by a comment ANZ chief economist Sharon Zollner made in her weekly podcast, noting that this recession had been caused by interest rates and not some other negative shock. "...Rates are normally cut because something really bad has happened and that’s not the case this time."

And it's a very fair point. The RBNZ even conceded it was engineering a recession. I can't recall anything quite like this before.

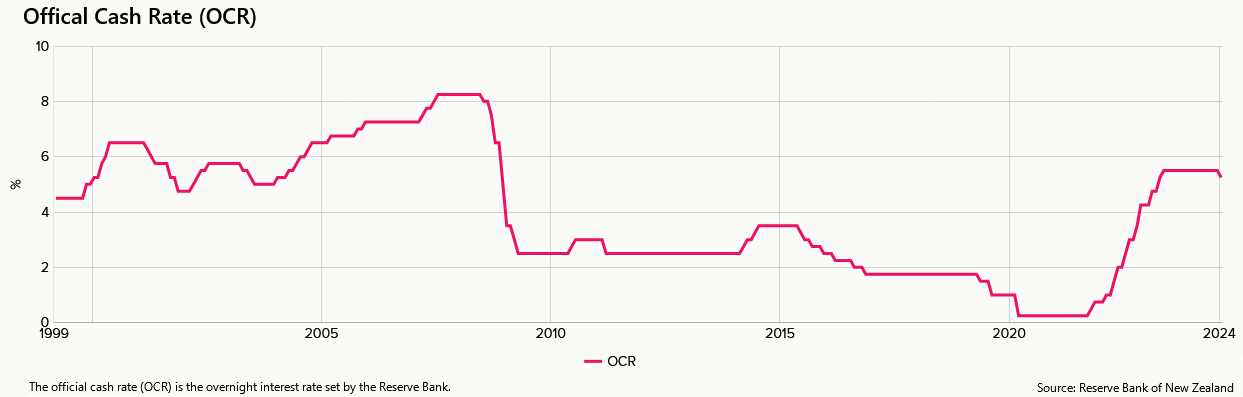

Consider for a moment, the path of interest rates in the past 25 years...

The OCR was introduced in 1999. Between then and 2005 it bounced around in a 4.5% to 6.5% range, before then being ramped up all the way to 8.25% in 2007 and through to June 2008. When it came down it was because of the Global Financial Crisis and in fact it dropped like a brick to 2.5% in April 2009.

Such a massive drop in such a short space of time might be expected to have a huge stimulatory effect - but of course the economy had been well wrecked, and took ages to recover.

And that was the last time we saw a high OCR followed by a drop. So, this time it will be quite different. In many respects it's going to be unchartered waters. And we don't really know yet whether the economy might start to heat quite quickly again. And what does the RBNZ do if there are signs of this? - with the housing market, as ever, the first place to look.

Remember how quickly the economy bounced back from the lockdowns? Nobody expected that. But at the time everybody, including the economists, had tried to apply the usual logic of how quickly an economy recovers from a 'recession' - and therefore expected recovery would take a while. It didn't. The lockdowns didn't create true recessions as we can now fully acknowledge. Once the tap was turned on again, the water flowed. Might we now be looking at a situation not directly comparable, but at least with some similarities?

Spend, spend, spend?

It all depends on how quickly people might feel they can start to spend again. And in that regard, I don't think the RBNZ would be all that pleased with how well organised the mortgage holders have been this year in 'going short' with their fixed rate mortgage terms en masse in anticipation of falling interest rates.

As of July three-quarters of the country's $360 billion mortgage pile was either on floating rates or fixed for a year or less. Around half of the pile was on either floating or fixed for six months or less.

People are therefore going to get some interest rate relief quite quickly. It could be this will be more quickly than the RBNZ is truly comfortable with. And the more the RBNZ cuts rates, the more relief will flow.

Will we see spending start to ramp up again quite soon then?

One thing that will likely mitigate against that is the rate of unemployment, which is expected to continue rising strongly into next year. But how much of a dampening impact will that have? Again it's not really that clear, but my suspicion is less impact than might be expected.

There's a lot of questions surrounding the current economic situation. I'm not making any bold predictions, but, I just think we can't take for granted that there will now be a steady continuing fall in interest rates and all will be sweetness and light. The RBNZ may yet have a few surprises for us. Much will depend on what we do.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

47 Comments

The greed around tax free gains is very strong. Picking the usual suspects will be sweating around how to max out borrowing under the new DTI constraints.

Example. Rented for $1100 per week but wants $900k. Going to require near enough 55% equity. As the price goes up, the equity required rises as well.

The influence of animal spirits and vibes are over-rated imho. Let's look at some hard facts:

- It is the effective mortgage rate that matters - the average yield on all mortgages. This is what determines how much cash flows from mortgagors (spenders) to savers. The effective rate is still going up - it was 6.33% at the end of July and will be 6.4% by now. Last time OCR and mortgage rates fell hard, it was 6 months before the effective rate started to fall, and it dropped painfully slowly (effective rate tracks the one year card rates in usual times)

- Mortgage interest costs are running at $1.9bn per month, $22.8bn a year, or 5.6% of GDP. Mortgage payments in total are probably around 10% of GDP. That's a quarter of total wages and salaries!

- The top end of town is doing great, and they have rammed as much cash as possible into term deposits. That cash is banked for a while yet.

- Govt spending is reducing quickly but our current account deficit is not coming down. So we have reduced govt stimulus and a sizeable cash drain offshore, at the same time as relatively low bank money creation (borrowing). This is contractionary as hell.

- Businesses are busily un-saving because they are in trouble (in aggregate) and job growth will go negative in August despite massive increases in the working age population. We look to be firmly in the 'jobs go - demand drops - jobs go' doom loop.

So, I don't have any optimism about a turnaround. Recessions end when Govt goes fiscal. Central banks are even more hopeless at stimulating the economy than they are at 'controlling inflation'.

I disagree, it's 100% vibes and 0% data.

Yep if the RBNZ signals more cuts to come it will be all on again.

Lol, the data shapes the vibes. If you are sat on cash and inflation is falling away, house prices are on pause, and term deposits are on a 'last chance' special offer at 250pts above CPI... the vibes will be save!

The business model of landlording was capital gain and it worked That was then.

Why would you get into it now? The big gains have been had. The big leveraging idea is now very perilous.

You can bet on central banks and fiscal authorities to come up with creative ways to keep feeding the populace increasing amounts of debt on way or another.

What's worse is nobody really cares where the money comes from or what the long-term repercussions are as long as they can spend money they don't have on investment properties, overseas holidays and home renos.

The business model of landlording was capital gain and it worked That was then.

Why would you get into it now?

For me, as a long term landlord who is increasing my portfolio i am looking to future subdivision with plan changes to make my margin. Capital gains are still to be had but only when selling your parcel in parts.

Slightly off topic but has anyone heard about banks being very stingie on lending on apartments? I thought it was a thing of the past

Have an acquaintance with a 350 deposit. He wanted to buy a circa 800k apartment. Bank said ‘no’, only prepared to lend him 250k for the apartment.

Yet would happily lend him 800k for a detached house (which he doesn’t want or need)….

Apartments and Townhouses are high risk for lending. Just buy a cheaper apartment, no way I would spend $800k on an apartment built to "New Zealand standards"

I thought needing a 50% deposit for an apartment was a thing of the distant past. I thought banks now considered 20-25% deposits.

Apparently not.

All banks have different tolerances on apartments... shop around.

Could it be the building in which the apartment exists? The banks are well aware some buildings are better than others (and a few are outright dogs).

Maybe a 'dead cat bounce' somewhere in the future but young folk are jumping on a plane and chasing better wages elsewhere. The skilled and talented are on the same plane... imported cheap labour will drag the economy . Lots of price increases ahead regardless of lower cash rates . Everyone will have good roads to go speeding on ...but where are they going to in such a hurry , hopefully not that understaffed run down hospital ?

At least you'll be able to drive to hospital fast when the ambulance fails to turn up.

Hopefully there is a bed left when you arrive:

'Its chief executive Tracey Martin said they were only getting piecemeal information, but what they had seen was worrying, with indications that Health NZ intended to cut 200,000 hospital bed nights a year to save money, a directive from Health Minister Shane Reti.'

And then wait 8 hours to see a Dr (if things are slow)

There are a lot of businesses just hanging on by the skin of their teeth, suffering through a lack of demand and an inability to increase prices. As soon as they get the whiff that demand is picking up again they will take advantage and jack their prices up to restore their margins and profits (and make up for the last couple of years). This is how its always been, and its how it will be. Thats why inflation has often viciously rebounded after rate cuts are started (see 1970s-1980s) - and why central banks like the Fed and RBA are so determined to not cut rates until they are 100% sure that inflation is dead and buried. The RBNZ is out there on its own, cutting rates BEFORE being certain inflation is back to 2-3% and permanently settled there.

I agree that businesses will quicky seek to restore profits and balance sheet - and some will have even less competition than they did before. But important to remember that the surge back in inflation in the 70s and 80s was driven by several imported oil price shocks. You can see them here. Same with the inflationary episode of 2022 and 2023 of course.

Both good and valid comments.

Strangely though no surge in the early 90s nor late noughties....high energy prices will certainly displace spending patterns but wont necessarily cause increased credit creation.

https://www.macrotrends.net/1369/crude-oil-price-history-chart

Sorry I was talking about inflation. Oil prices dominant cause of every inflationary episode and reprisal. RBNZ were hiking rates to tame inflation in the noughties.

How will that demand pick up however IF the availability of credit does not eventuate?....we will still have businesses in the throes of failure, households that have exhausted (or nearly) their savings, unemployment still increasing and optimism dented.

A risk manager will look at those circumstances and be very wary until such time as it is clear the rot has been removed....and that takes time.

Nevermind the RBNZ

Demand picks up once people start getting more cash to spend. You dont need credit to buy groceries, have a cafe lunch, get your hair done, or take a holiday. If you look at the ASX, consumer discretionary and non-discretionary companies are booming now, in anticipation of better sales, better margins, and bigger profits. (Dont look at the NZX, it is and will remain, a basketcase of underperforming NZ businesses, all the good ones shift to the ASX).

"Demand picks up once people start getting more cash to spend."

Yes it may...assuming there is more cash to spend...there is increased costs for existing services/goods, debt to be paid down (including arrears) savings to rebuild, uncertainty around ongoing employment and a changed environment around the ability to secure additional credit.

As said, it will take time for all of that to unwind...and meanwhile the pressure on budgets remains.

As to NZX...it isnt a consideration.

Businesses seem to believe that marginally lower interest rates will lead to a big recovery in spending. That's unlikely. Workers are spending what they can, while onshore and offshore rentiers are collecting all the cash up. If we want the economy to pick up we may have to accept that the consumption / saving rate of the wealthy needs to fall (taxed) and govt transfers need to increase.

Or (as you have previously noted) private equity (offshore in all likelyhood) into PPPs at scale (arrrgh)...but again, it all takes time.

Yes, I am pretty confident that the Govt think that a whole pile of expensively financed PPPs will provide the economic boost needed to win the 2026 election. They are probably right. Future generations don't vote.

Yep

will need another year before lower rates stimulates spending in any meaningful way

@K.W. The RBNZ's average longterm NIR is 2.5, sh*t we're still double that...quite contractionary surely? It will be months before people "start getting cash to spend", and I would think a fair chunk of that extra cash will go back into the household war chests which have been decimated over the last couple of years. The Fed will cut in ten days so RBNZ hardly jumped BEFORE them by much...I'm not real sure that was worth shouting about 😂

The risk of any pending inflation could be if they panic and slash rates and lending restrictions over the next 12-18 months because NZ Inc is doing so poorly...maybe it could go berko on the back of that if the wealth effect kicks in again...the three 0.25 cuts we will see over the tail end of this year won't do bugger all...but, hey, your crystal ball might be better than mine so who knows 🔮

US inflation has been hovering around 3% for 15 months now (having first hit it in Jun 23). NZ hasnt even gotten to 3% once yet, let alone spent a year monitoring the situation to ensure inflation is completely dead. Thats why the RBNZ originally had no rate cuts scheduled until mid 2025 - this is what I meant by "before" (not "before the Fed"). Now they've completely panicked and have started cutting rates whilst inflation is still above target, going against the more cautious stance taken by other central bankers.

I feel like if National goes the PPP direction as above, then it is going to make the reserve bank panic again.

The other possibility, which has been explored here at all, is that interest rates fall much harder and stay lower than currently predicted There are many factors that determine that path for example the US economy and the Fed.

Those are extremely long odds. As mentioned by others already, even if they do fall there will be a significant lag, there's no silver bullet Tonto.

From memory there are 2 huge reasons why investors poured into real estate in 2020:

1) TD rates were extremely low. Weren't they in the 2%range, or less even? This made rental yields of 2-3 % still attractive enough, especially given the next point:

2) Interest rates were expected to stay low for a long time, some thought they might even go negative! This gave investors some optimism that house price growth was going to be supported by low interest rates for the foreseeable future (of course in hindsight we know how wrong that all was).

That second point seems to be at play once again, as in - interest rates are expected to keep dropping supporting house prices for the foreseeable future.

That first point is not at play yet but it is the direction we are headed in. So it's possible that investor share in the market will increase from 20% to 25% again (and maybe more) as yields on R.E. investments start to look attractive relative to other options.

Of course, once again, most people might be wrong in their expectations (as in 2020) and the escalation in global wars or some other event might send interest rates rising again. Will be interesting to see what will happen.

Side question (sorry) anyone know when the Auckland City 2024 RVs are due to be published? It’s been well over 3 years now (June ‘21 for most). As someone trying to buy a home, they can’t come soon enough… kinda feels like the vested crowd are delaying this data as long as possible

Not sure but there has to be an objection and review process, which they have to allow time for. I imagine that this time many values will go down, and that will trigger lots of objections.

And then those who successfully object move on to their next journey, complaining about the increase in their rates bill.

"As someone trying to buy a home, they can’t come soon enough"

Why do you say that?

From what we're experiencing, vendors still have expectations set at 2021 prices - But in an economy of high interest rates, high stock volumes and lower borrowing power these old valuations in many cases do not reflect accurate value for the buyers. I'm not saying all houses are worth less, but I would argue that many are. Wouldn't the release of updated RV data help balance expectations on both sides of the fence?

Whilst CVs are not a fully accurate market valuation, they are close to one. And it will assist vendors to divorce themselves from the idea that their house is still worth what it was in 2021. And a more flexible vendor is better for buyers.

I just think we can't take for granted that there will now be a steady continuing fall in interest rates and all will be sweetness and light.

it is now all about unemployment rate.

The big difference between the last RBNZ OCR (dramatic) cut and now is the employment. Last time, OCR was low and plentiful of jobs available, people felt financially secure to sign up to big financial commitments.

Now, OCR is heading down but jobs market is a bit gloomy!

Only those with hardened steels balls will sign up for a big mortgage. And good luck to them!

What do you consider a big mortgage? More than 5 x your household DTI?

I know two lots with millions dollars mortgage, but they are on good income. Both are in the 7+ DTI and worrying about their jobs situation!

.

Anecdotal, but I have seen all my clients in the construction sector fall off - some in a big way. Far less people looking to build or undergo renos. Interestingly though, strong demand for outdoor-type products like these (https://www.shadetech.nz/outdoor-louvre-roof-system-christchurch, https://www.weathermasterak.co.nz/awnings). People still willing to spend spend spend, but more on smaller projects around the home.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.