By David Skilling*

The world at the end of March is a very different place than in mid-January; from changes to the global economic outlook to the shape of geopolitical relations. The US is friendlier with historical rivals than with traditional partners, left wing parties are raising defence spending, right wing parties are removing limitations on public debt, and more. And this is only the start of a reordering of the global economic and geopolitical system.

Much of this is due to the policies of the Trump Administration, as well as the responses by other countries. The next several years will be a highly disruptive, consequential period. And unlike the first Trump Administration, there will be nowhere to hide – from tariffs to the restructuring of security arrangements.

This note selects ten recent developments that provide insights into the nature of these global changes.

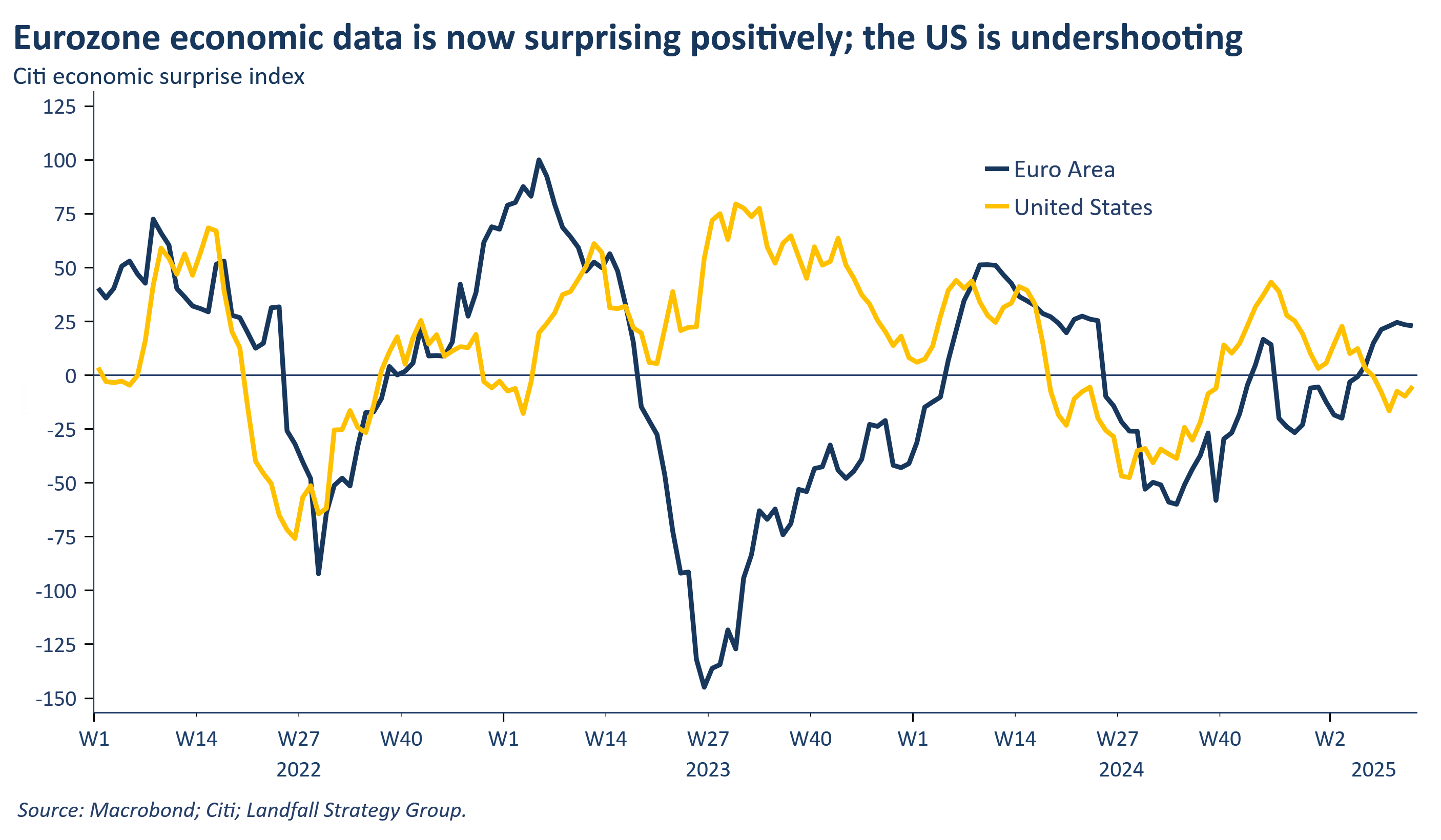

1. Surprise!

One of the big global macro stories of the first quarter has been the building economic optimism in Europe – and concerns about cracks emerging in US economic exceptionalism. The economic surprise index is a useful way to capture this rotation: European economic data has positively surprised against (low) expectations, whereas US economic data has negatively surprised against expectations. Consensus forecasts are likely to begin to shift over the next few months to reflect this trans-Atlantic growth rotation.

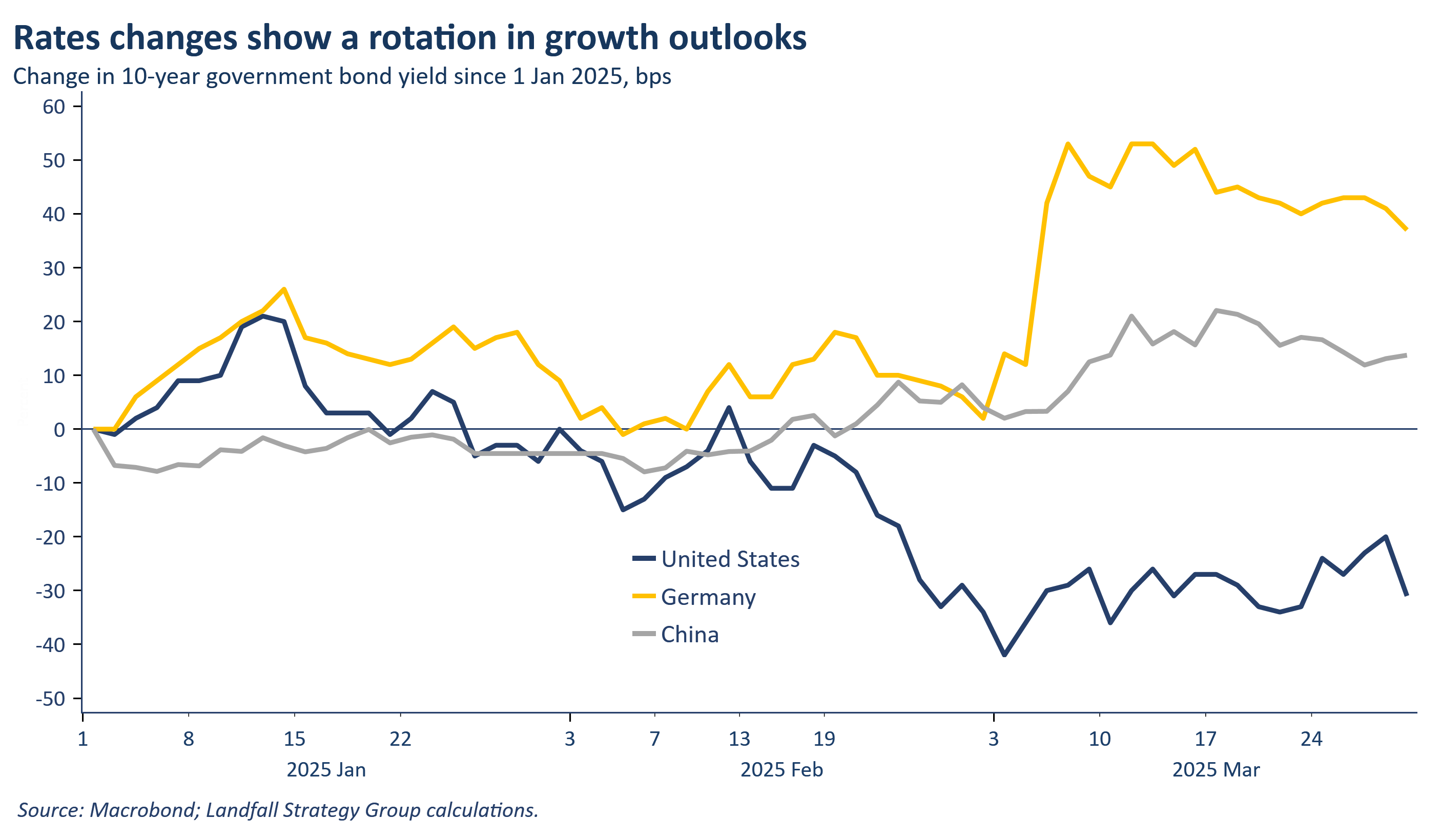

2. Bond spreads

One marker of the speed with which the economic ground has shifted is expressed in bond markets. US government bond yields have fallen on concerns about a weaker GDP growth profile and more rapid Fed weakening – offsetting the concern about the inflationary impact of tariffs. In contrast, German bond yields have moved sharply higher on commitments to borrow more for investment in defence and infrastructure. And lastly, China’s bond yields may be bottoming out. These movements in bond markets are broadly consistent with equity market behaviour: Germany’s DAX index and Chinese equity indexes are strongly out-performing the S&P500.

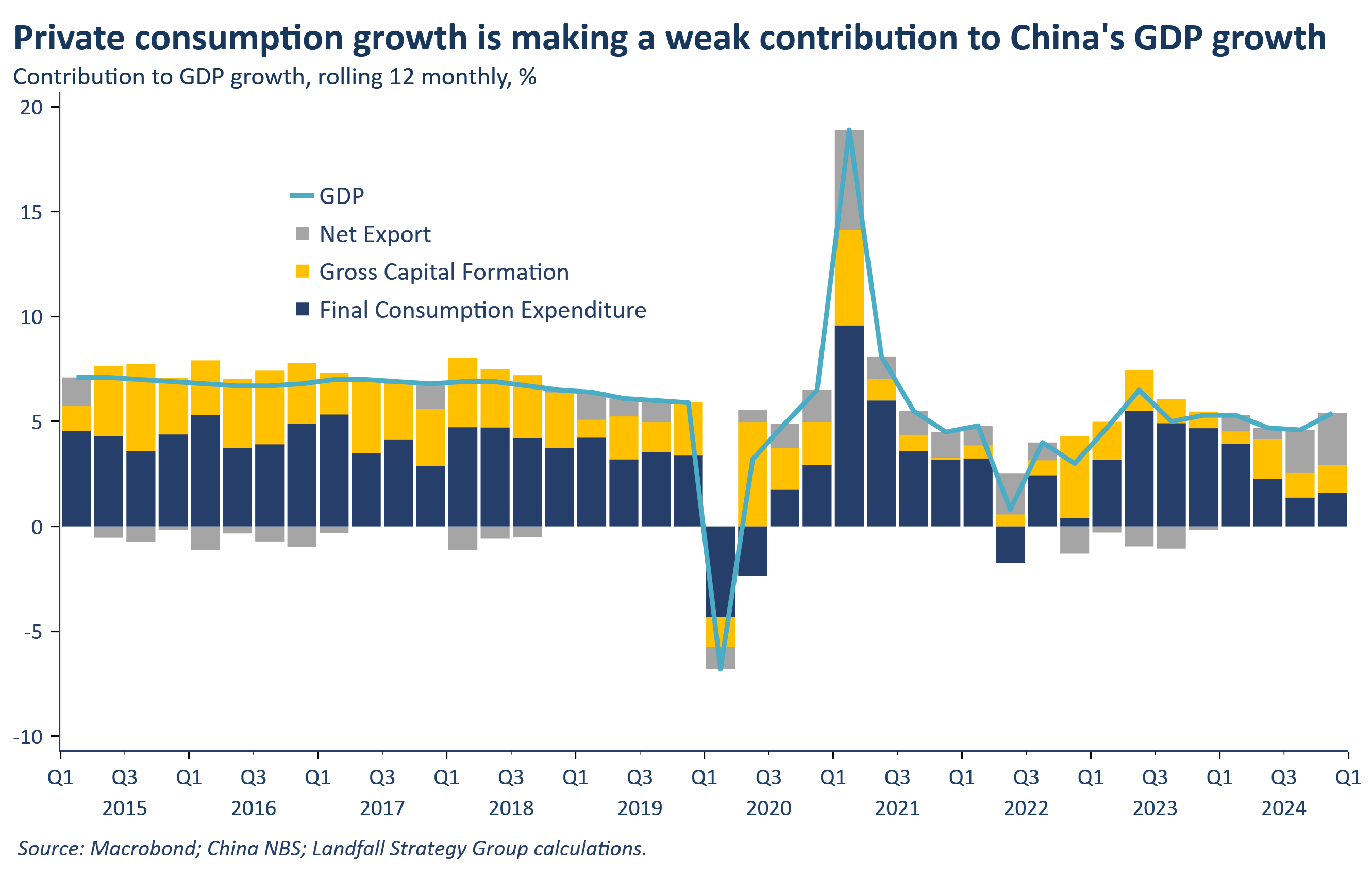

3. China consumption

I remain cautious about the Chinese economic outlook for several reasons. However, a couple of recent positive developments are worth noting. First, the impressive performance of the Chinese tech sector (EV firms, the AI ecosystem). Second, and perhaps more important, is the recently announced policy support for private consumption spending from the ‘Two Sessions’. The long-standing consensus view on China is that it needs to rotate its economic model away from export-oriented investment towards private consumption spending. But President Xi has been reluctant to do so. Indeed, previous policy announcements in the same direction have been made without much impact. But this time could be different given the changing global trade context: China needs new growth engines.

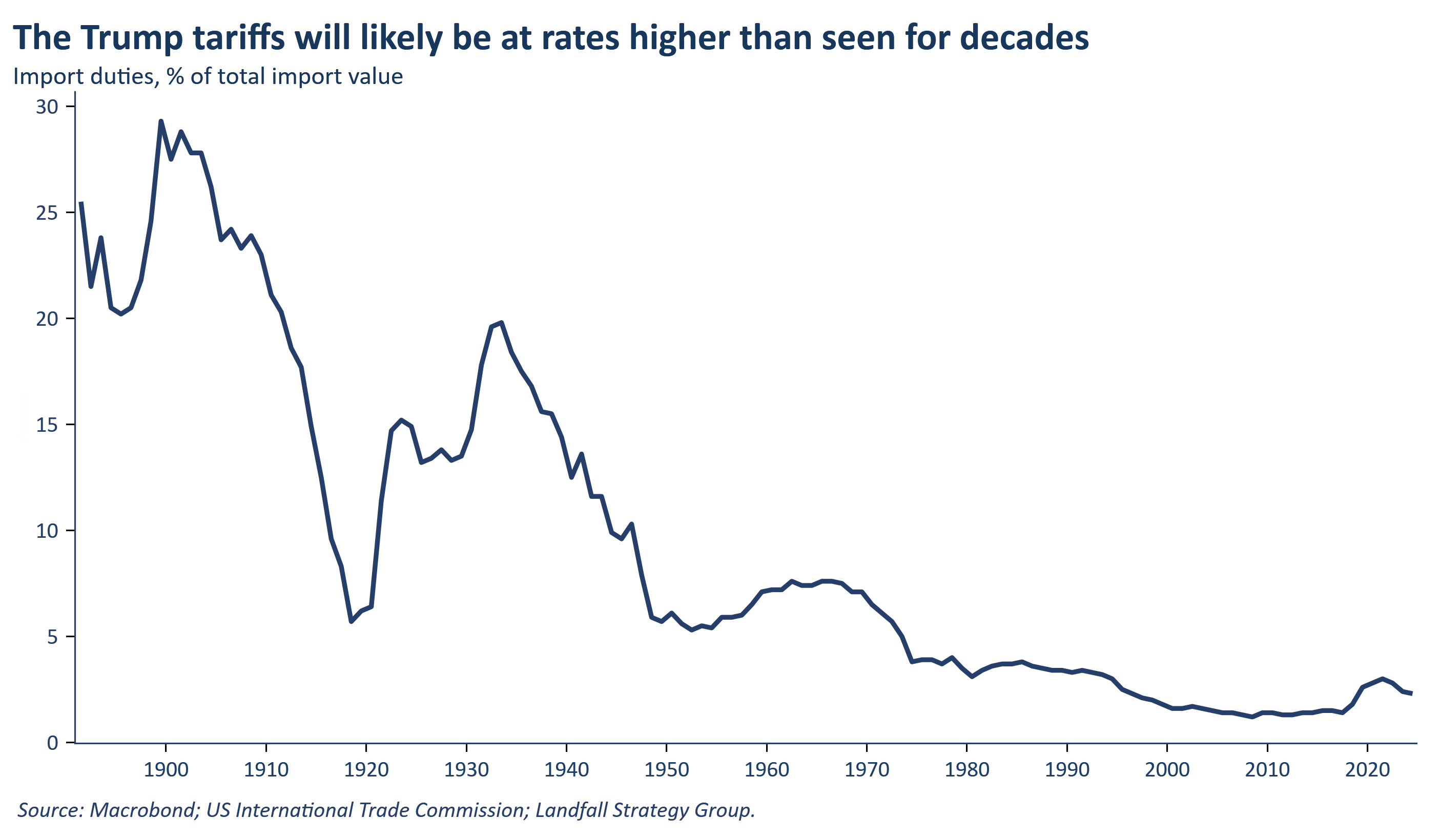

4. The return of tariffs

Wednesday (April 2) is billed as Liberation Day by President Trump, with sweeping ‘reciprocal’ tariffs promised; which come on top of measures just announced (e.g. 25% tariff on car imports). The coverage, tariff rates, and much else, remains deeply uncertain. But Mr Trump believes that tariffs are a magic weapon: to restructure the US economy, reduce the trade deficit, generate fiscal revenue, extract concessions, and much else. So we should expect material tariff rates to be applied on a comprehensive basis, with a focus on economies that run large bilateral trade surpluses with the US. We may be going back to US tariff rates not seen since the 1930s/1940s, which was not an auspicious precedent.

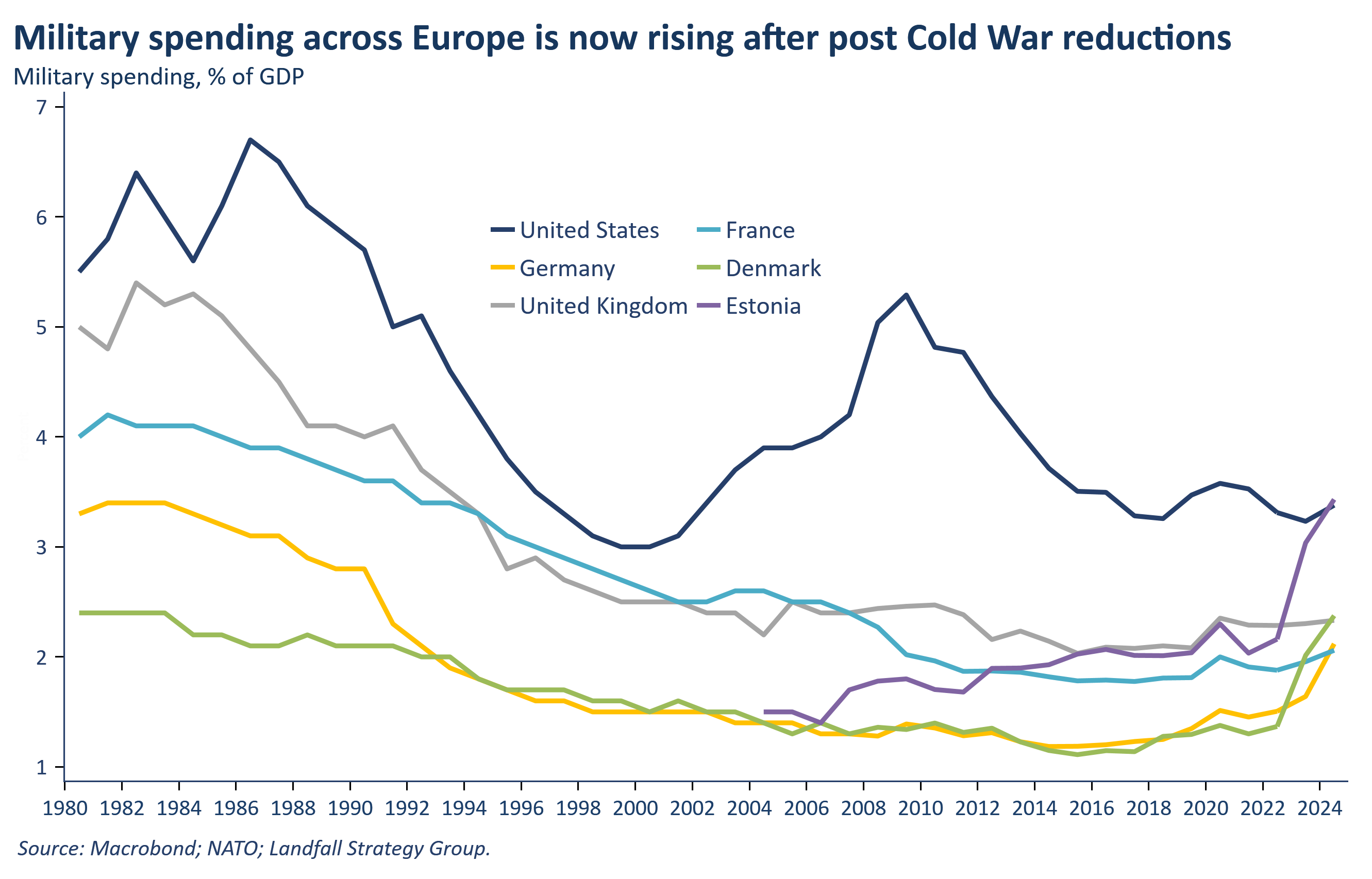

5. Farewell to the peace dividend

The post-Cold War peace dividend – which supported fiscal consolidation in the 1990s – is over, particularly in Europe. The weakening of the US security guarantee has accelerated efforts to increase military spending. The European Commission has proposed joint borrowing to fund €150 billion, and relaxed national borrowing limits to allow for €650 billion for defence spending. Germany is making aggressive plans for military spending; the UK has committed to a 3% of GDP target during the next Parliament (the Chancellor detailed some of the spending cuts that would be required on Wednesday); Sweden has just announced a 3.5% of GDP target by 2030, to be funded largely through borrowing; and Estonia has announced a 5% of GDP target. There will be variation depending on fiscal position and strategic exposure, but 3% of GDP will likely become the new floor for military spending over time. Hard fiscal choices lie ahead.

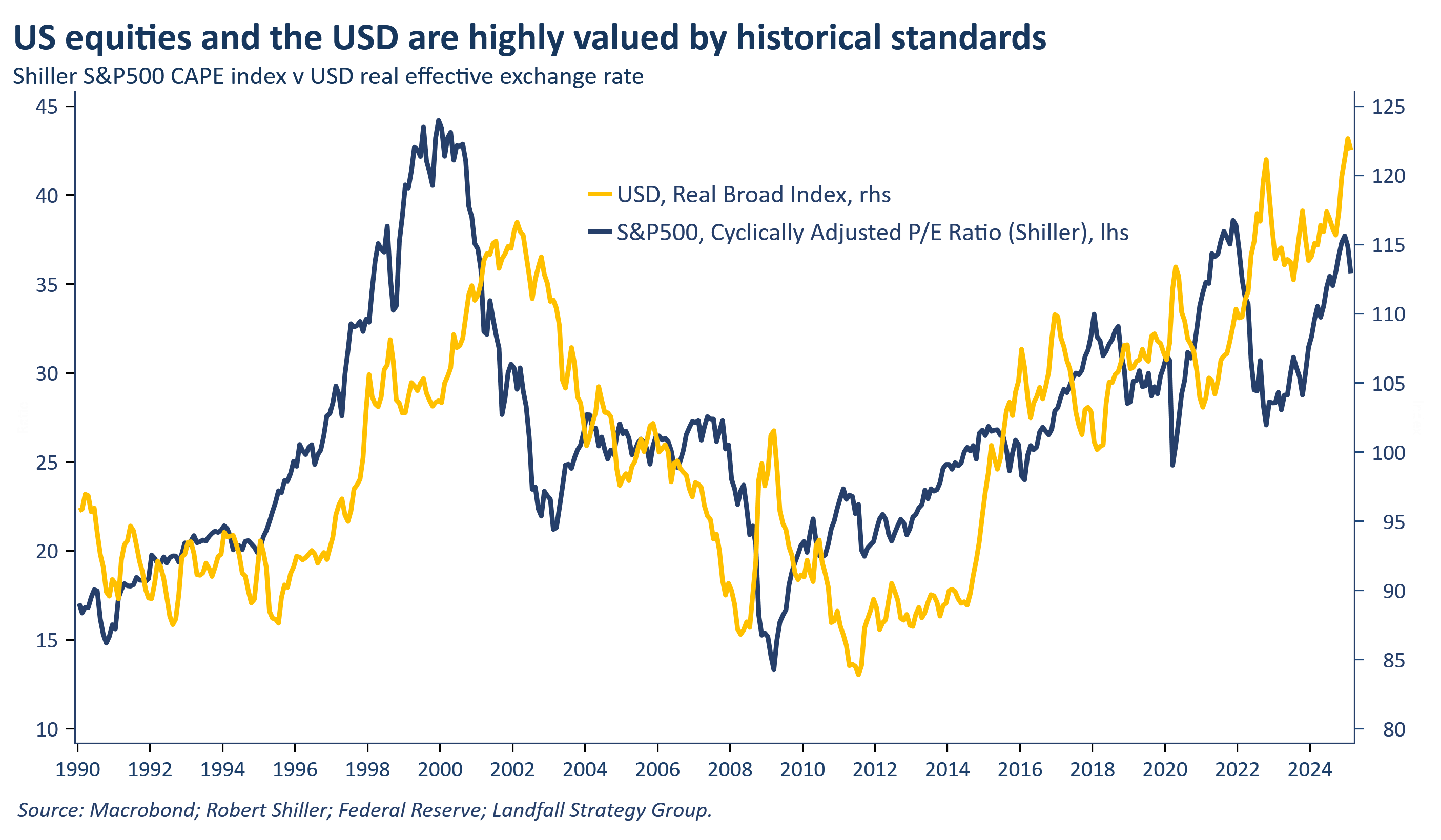

6. Watch out below

One of the striking features of the US economy as it confronts a series of risks is the highly elevated price of US assets. The Shiller CAPE measure is sitting at levels that have only been reached on a handful of occasions, despite a weak start to the year by US equity markets. And the USD effective exchange rate is also at historically very high levels. This is not a coincidence: the strong performance of US equities since the global financial crisis has led to a wall of foreign capital buying USD assets. The implication is that both the USD and US equities could come under significant pressure to the extent that foreign investors diversify US risk – and look for value elsewhere.

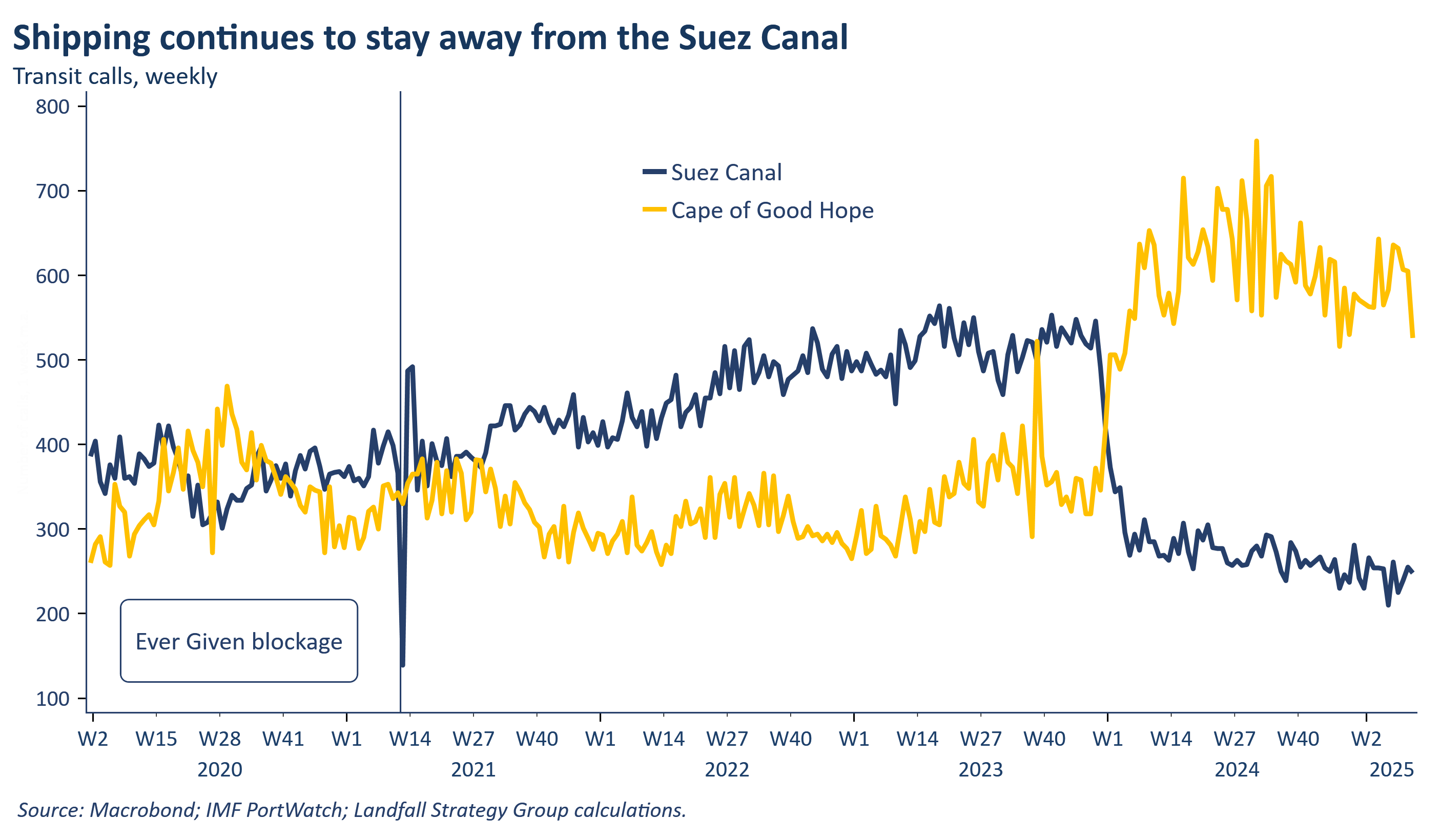

7. Suez Canal

Shipping movements through the Suez Canal remain heavily constrained because of the threat of Houthi missile attacks. But global supply chains have again demonstrated a high level of resilience and flexibility, finding new routes to market. Multiple measures of global supply chain costs and delays do not suggest material levels of stress. This is just as well because it seems unlikely that the Houthi attacks will stop soon, despite recent stepped-up bombing by the US.

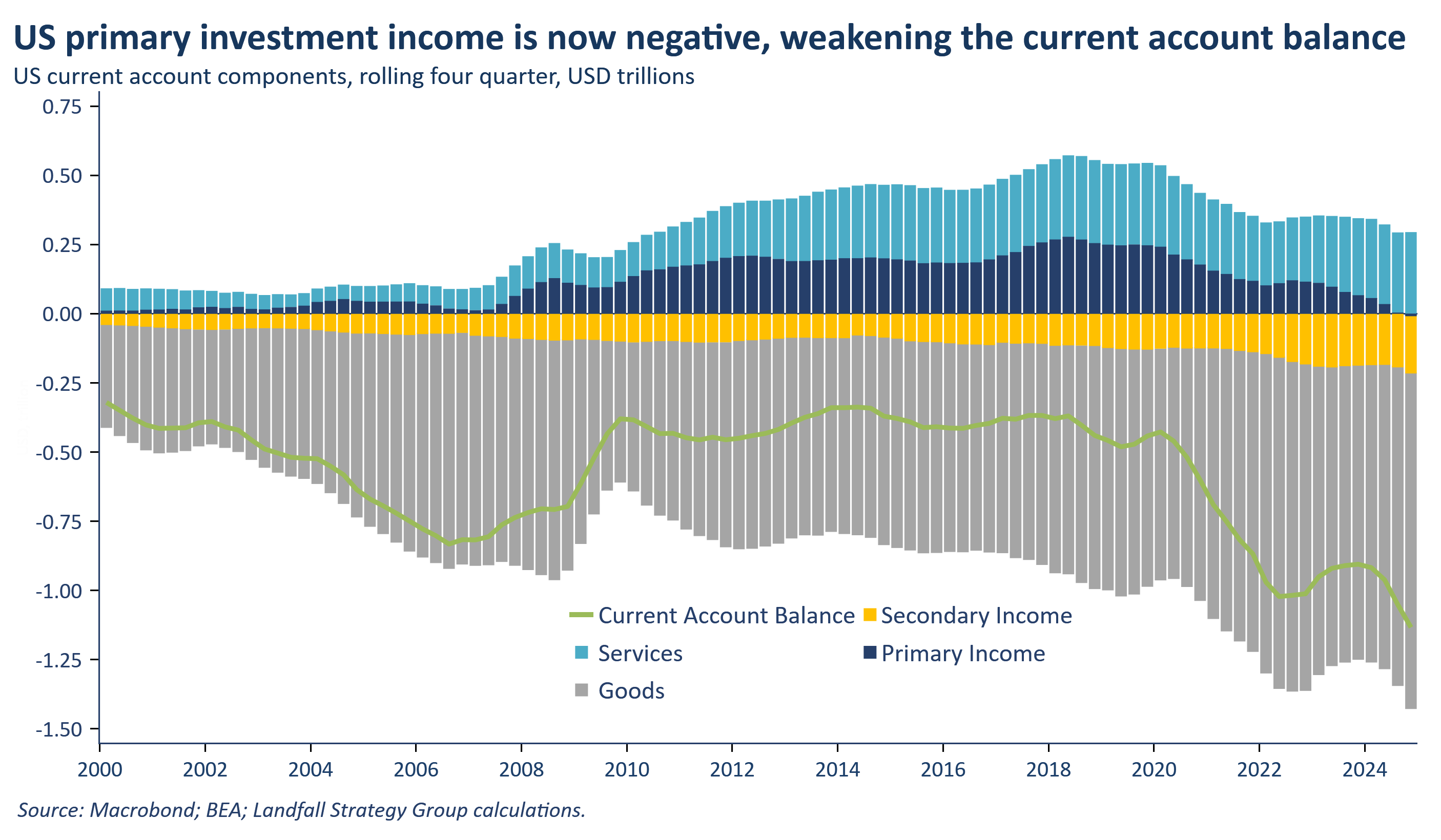

8. US primary income goes negative

Much to the annoyance of President Trump, the US has run a large, persistent goods trade deficit for decades. But its current account balance has been better because of a surplus in exports of services as well as a positive primary income balance – net investment income from international investments. However, this primary income balance has just turned negative for the first time since records started in 1960. This is partly due to reduced earnings on overseas investments; but the higher interest income flowing offshore from the US is also a key part. To the extent that interest rates stay high, expect sustained pressure on primary investment income – and on the US current account deficit. This is another source of potential USD weakness.

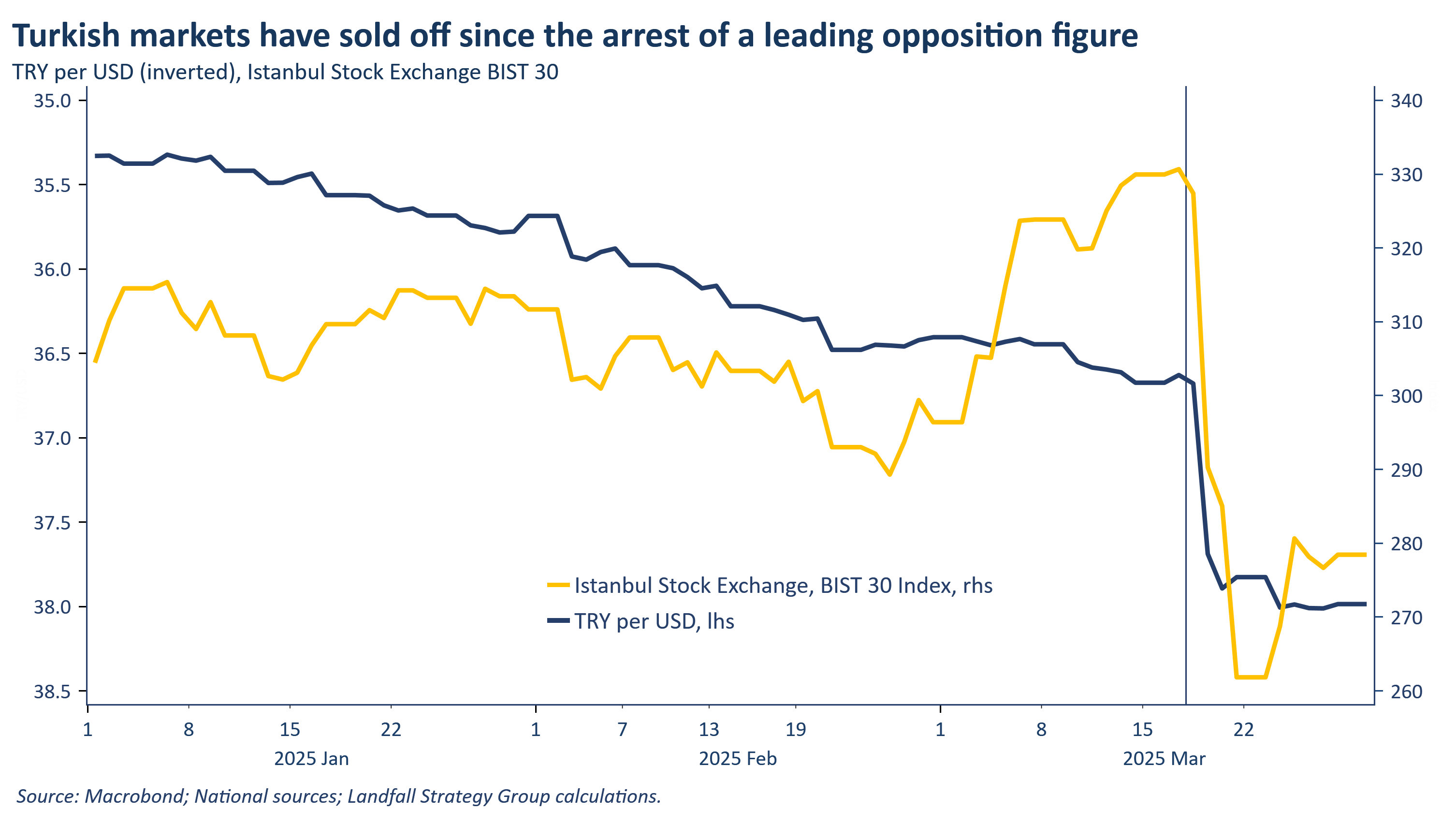

9. Turkey

Turkey’s markets have sold off heavily over the past couple of weeks after a leading opposition politician was arrested. The exchange rate is down ~4%, even after the central bank burned through an estimated $25 billion to support it, and the equity index is down by ~15%. President Erdogan likely judged that he could get away with this move - Europe needs Turkey for economic and security reasons, and the Trump Administration is unlikely to care about democratic backsliding. But the domestic political backlash bears watching. And as we saw with elections last year (Mexico, India) markets do not like unconstrained decision-making, particularly by someone with a poor history of economic policy decision-making. The impact of weakening political institutions on markets is something that has broader relevance at the moment.

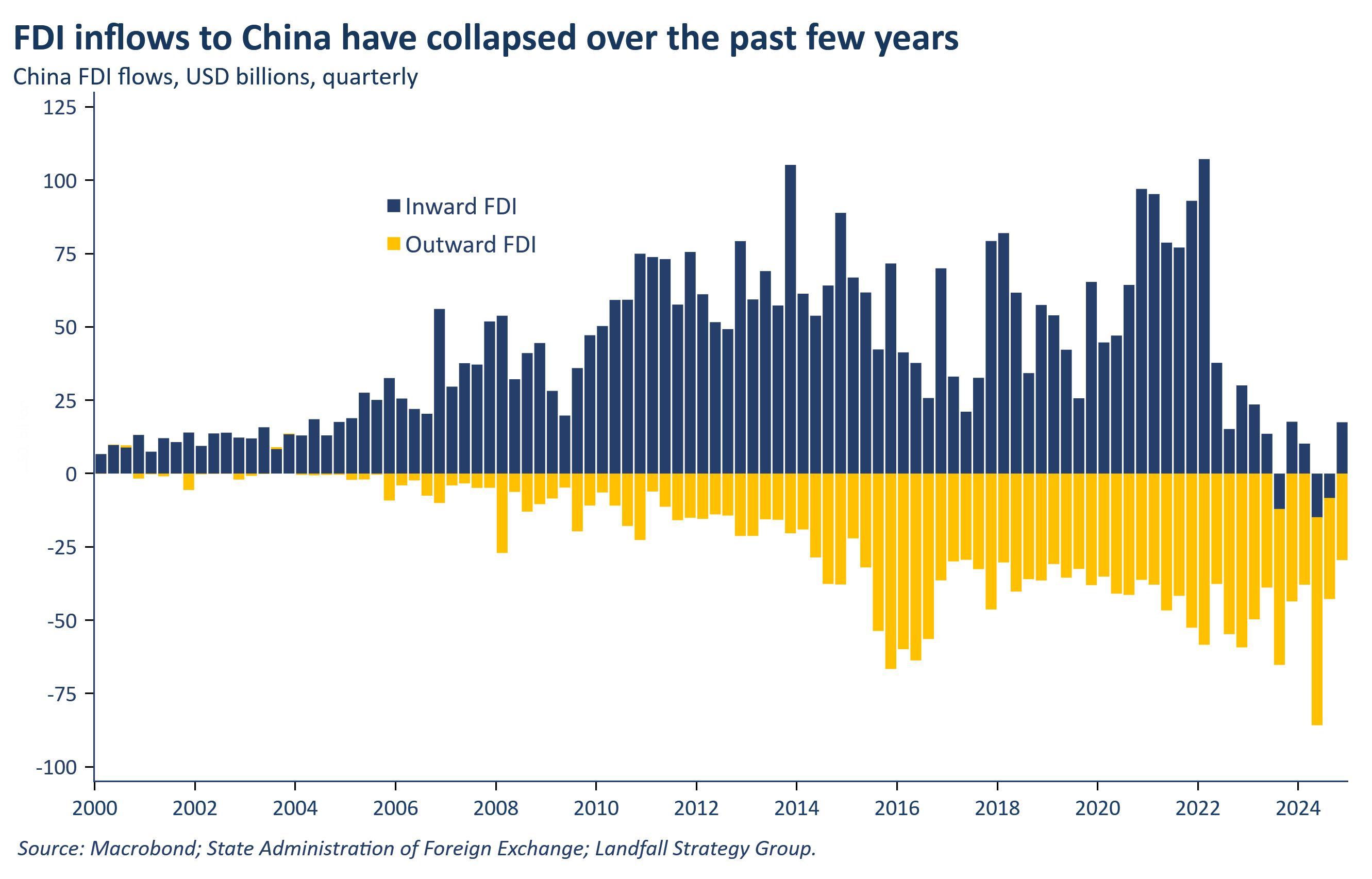

10. Inward investment into China

Q4 data shows that inward FDI into China remains heavily subdued. The slower growth profile of the Chinese economy, the politicised business environment, as well as deep geopolitical uncertainty make capital allocation into China a riskier proposition. But portfolio investors have been allocating capital into listed Chinese firms this year, particularly in the tech sector – shares are surging on impressive performance as well as because Chinese tech firms are back in political favour. China is no longer regarded as ‘uninvestable’ by many. The caveat is that changes in the political winds may change this profile again: the political risks of investing in China have not changed. In that context, note the Chinese antitrust review of CK Hutchison’s sale of its port holdings (including ports near the Panama Canal) - senior Chinese officials are unhappy with the Hong Kong company’s actions.

Thanks for reading small world. This week’s note is free for all to read. If you would like to receive insights on global economic & geopolitical dynamics in your inbox every week, do consider becoming a free or paid subscriber. Group & institutional subscriptions are also available: please contact me to discuss options (more information is available here).

*David Skilling ((@dskilling) is director at economic advisory firm Landfall Strategy Group. The original is here. You can subscribe to receive David Skilling’s notes by email here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.