By David Skilling*

Over the past few weeks, global eyes have been fixed on Washington DC and Mar-a-Lago for the latest statements from the Trump Administration: this past week it has been tariff threats to Canada and Mexico, the initial shots in the US/China trade wars, the Panama Canal, proposals for a US sovereign wealth fund, Gaza, and much more. Following and interpreting these developments has kept me busy: advising clients on what to take seriously – and what not to; what might be to come; and how to position.

My assessment remains that the second Trump term will be more disruptive and consequential than the first Trump term, as the US increasingly acts as a revisionist power. This will have material implications for firms, investors, and for governments: the effects on equity, rates, and currency markets as well as national economic outlooks are already evident.

But the world is more than the US. And global developments elsewhere over the past month are instructive for understanding the emerging world. This note provides a selection of 10 global developments that have struck me at the start of 2025 (in no particular order of importance).

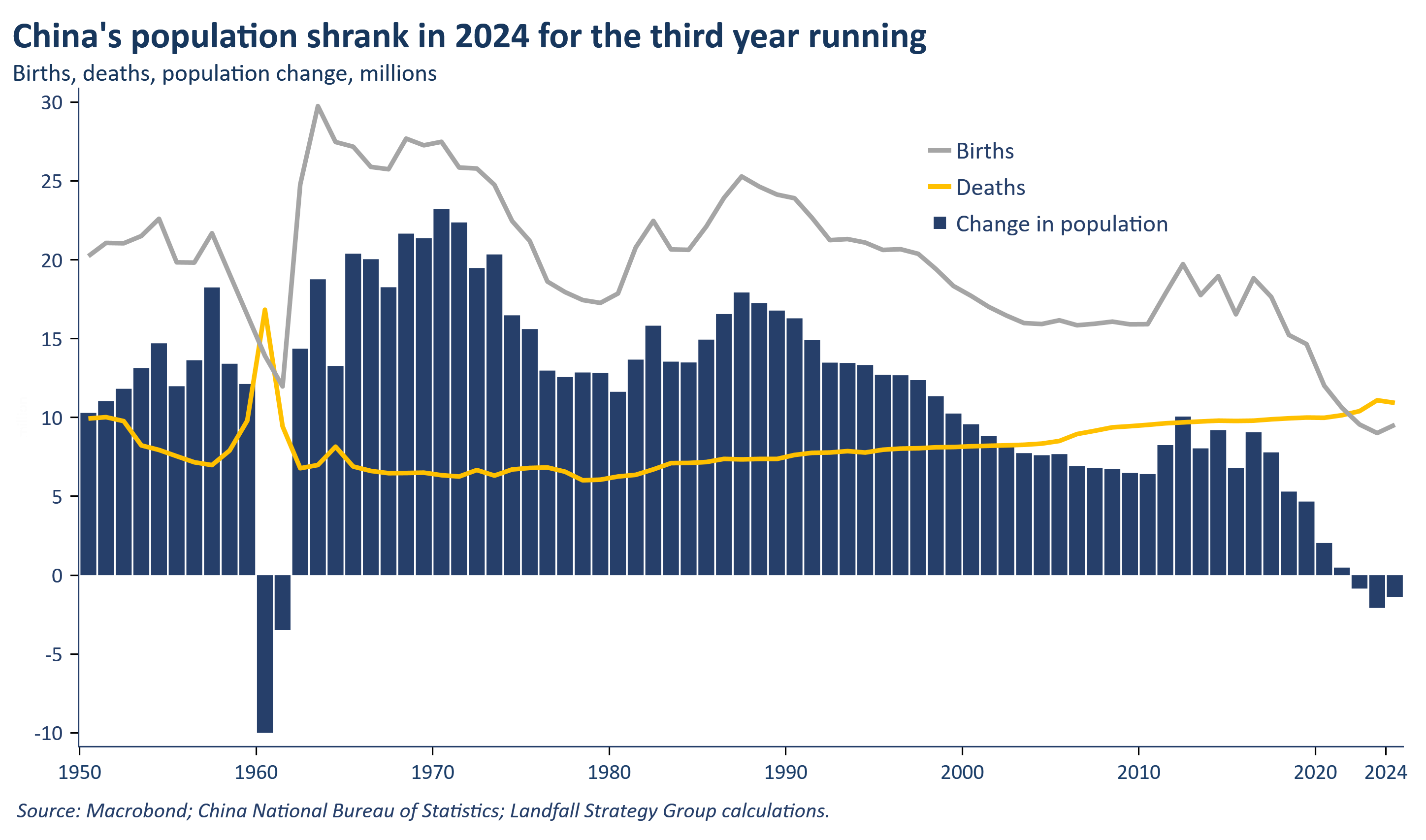

1. Shrinking China

China’s annual GDP growth for 2024 was reported in mid-January at 5.0%, happily also the government’s official growth target. But beyond questions regarding the plausibility of official data, there are material downside risks as ‘balance sheet recession’ dynamics deepen. And over longer time horizons, China’s rapidly weakening demographics will be an increasingly material drag on China’s headline GDP growth. In 2024, the Chinese population shrank for the third year in row. This dynamic will continue for the next several decades, impacting China’s GDP growth, China’s share of the global economy and its contribution to global growth, its economic model, and perhaps also its geopolitical posture.

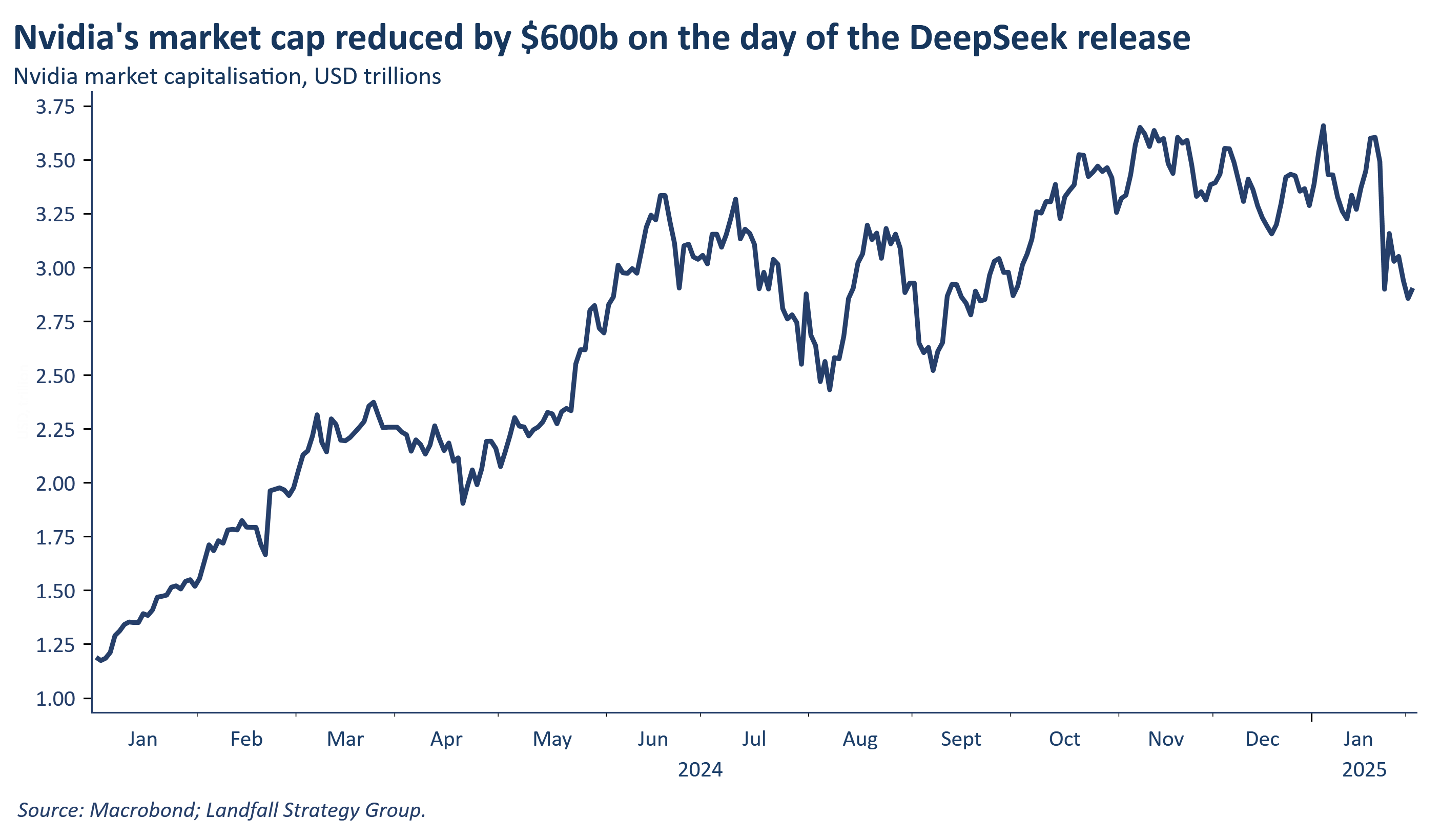

2. DeepSeek

Technology is a primary domain on which geopolitical competition is being conducted. But despite (some argue, because of) the restrictions imposed on Chinese access to advanced chips, an impressive Chinese AI model surprised markets and the AI ecosystem in January. This confirms the speed of progress in AI technology; it was bad for Nvidia shareholders (losing ~$600b in market cap in one day), but likely good for productivity around the world. AI is strategically important to the big powers as well as economically meaningful, so expect stepped-up AI investment (and restrictions) by the US and China to sustain/establish leadership. As in the 1960’s, geopolitical rivalry (such as around the Space Race) can spur more rapid innovation and productivity growth. Despite some promising smaller AI firms (such as Mistral), Europe lags in developing AI models.

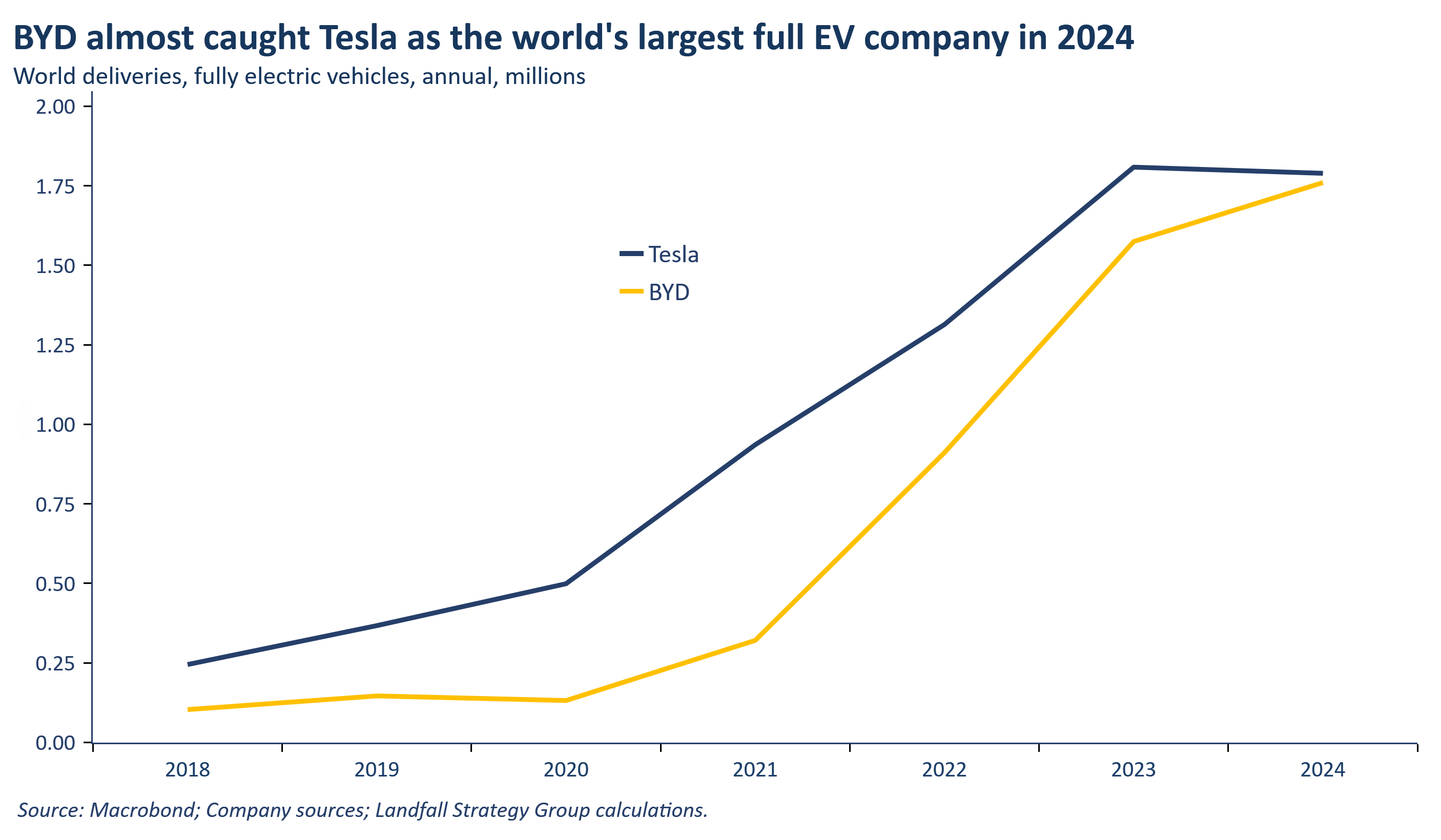

3. EVs

US (and European) firms are increasingly threatened by China in electric vehicles, another key technology. Tesla reported a 1% reduction in EV sales in 2024, even as overall global EV sales increased by ~25% - driven by China, now the world’s largest EV exporter. BYD sold 1.77m fully electric cars in 2024 (10% more than in 2023) just short of Tesla’s 1.79 million. And BYD sold 4.25 million electric cars in 2024, including plug-in hybrids. The intense competition, innovation, and subsidies in the Chinese EV market are creating a strong global competitive position. And this will continue despite tariffs now being imposed by the US and EU.

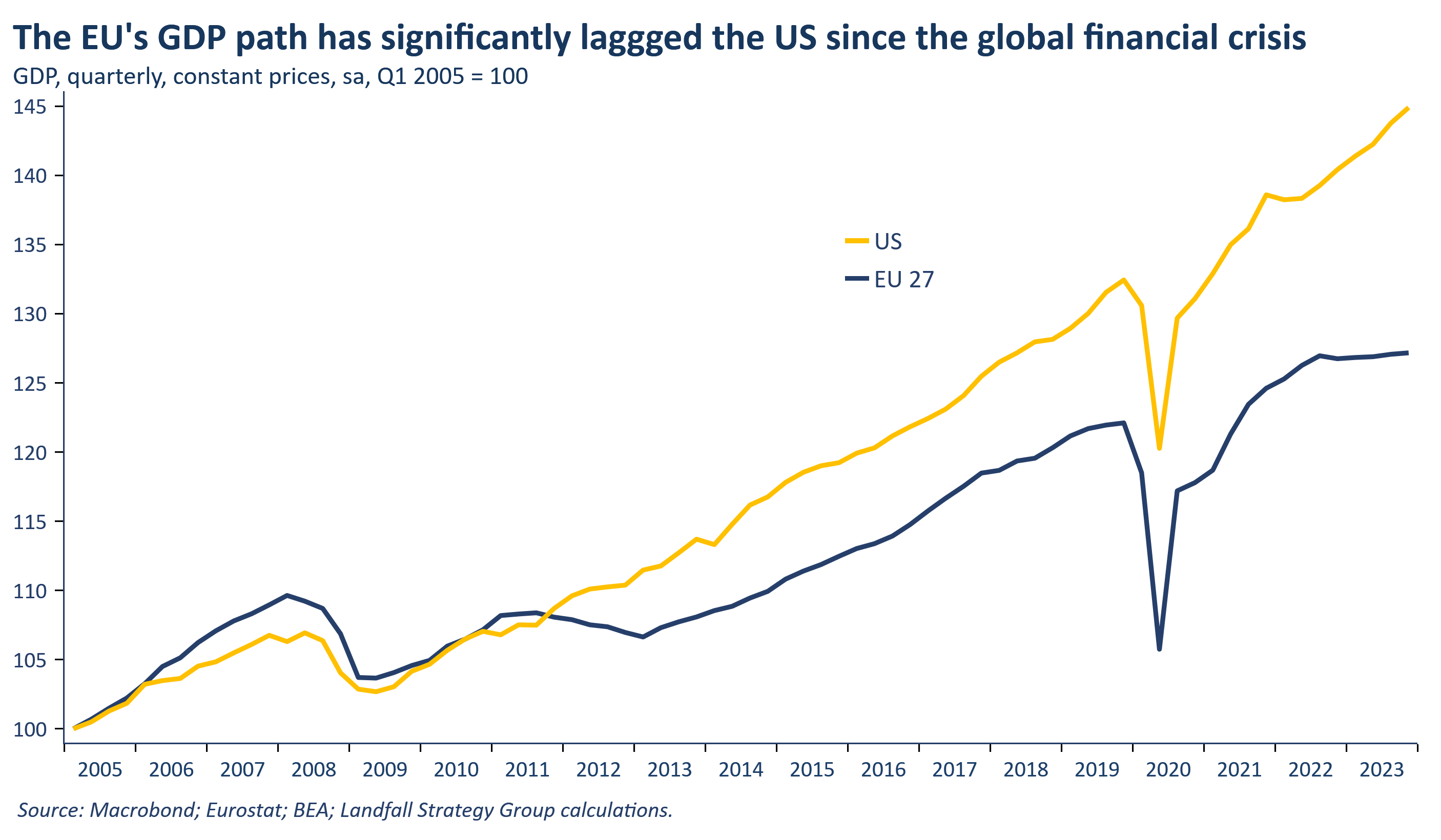

4. Europe stirs

Europe faces deep structural challenges, with sustained weak economic performance as well as strategic exposures in multiple directions (from Russia and China to the threats of US tariffs - and Greenland). The 5-year term for the new European Commission that is just kicking off will have a sharper focus on competitiveness. The ‘Competitiveness Compass’ released by Ursula von der Leyen last week contains initiatives from innovation and energy resilience to capital markets integration and reducing EU red tape. And discussions continue on raising EU defence spending to respond to a new strategic environment. The EU is slowly adjusting to a world that is distinctly unlike the world it was created in; it’s a useful start, but greater urgency is needed. As a reminder, eurozone GDP growth in Q4 was 0.0% qoq.

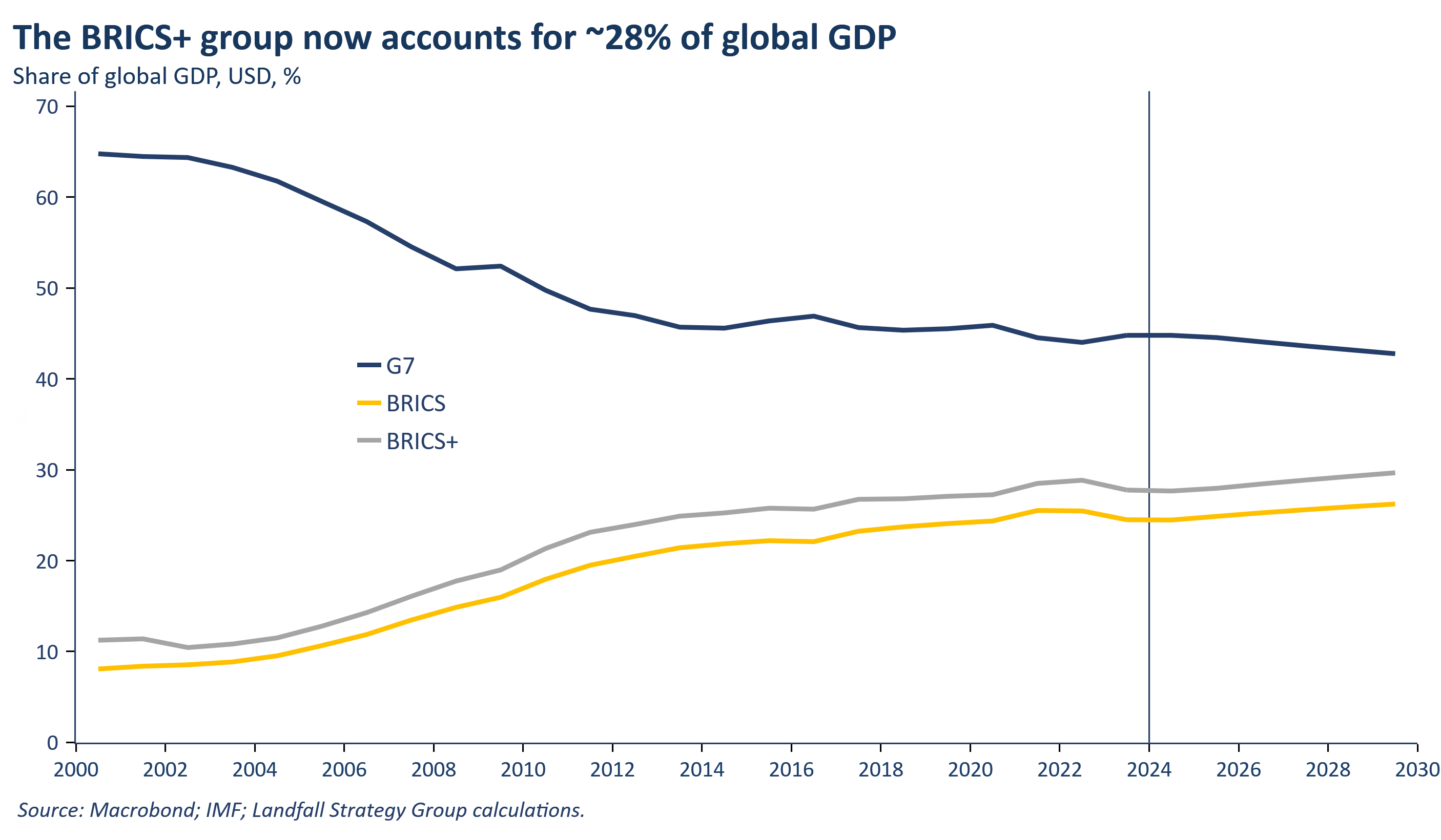

5. BRICS+

The BRICS group continues to expand. Indonesia joined as a full member in January, joining Egypt, Ethiopia, Iran, and the UAE as new members. There are also associate members such as Malaysia, Vietnam, Thailand, and Nigeria; and other counties have been invited, such as Saudi Arabia. The BRICS group is unlikely to be a strongly coherent entity (interests and preferences vary too much across the group); there is no meaningful chance of a BRICS currency, for example. But it reflects the desire among an increasing number of countries to develop additional options to reliance on the West. A global hedging and rebalancing is underway.

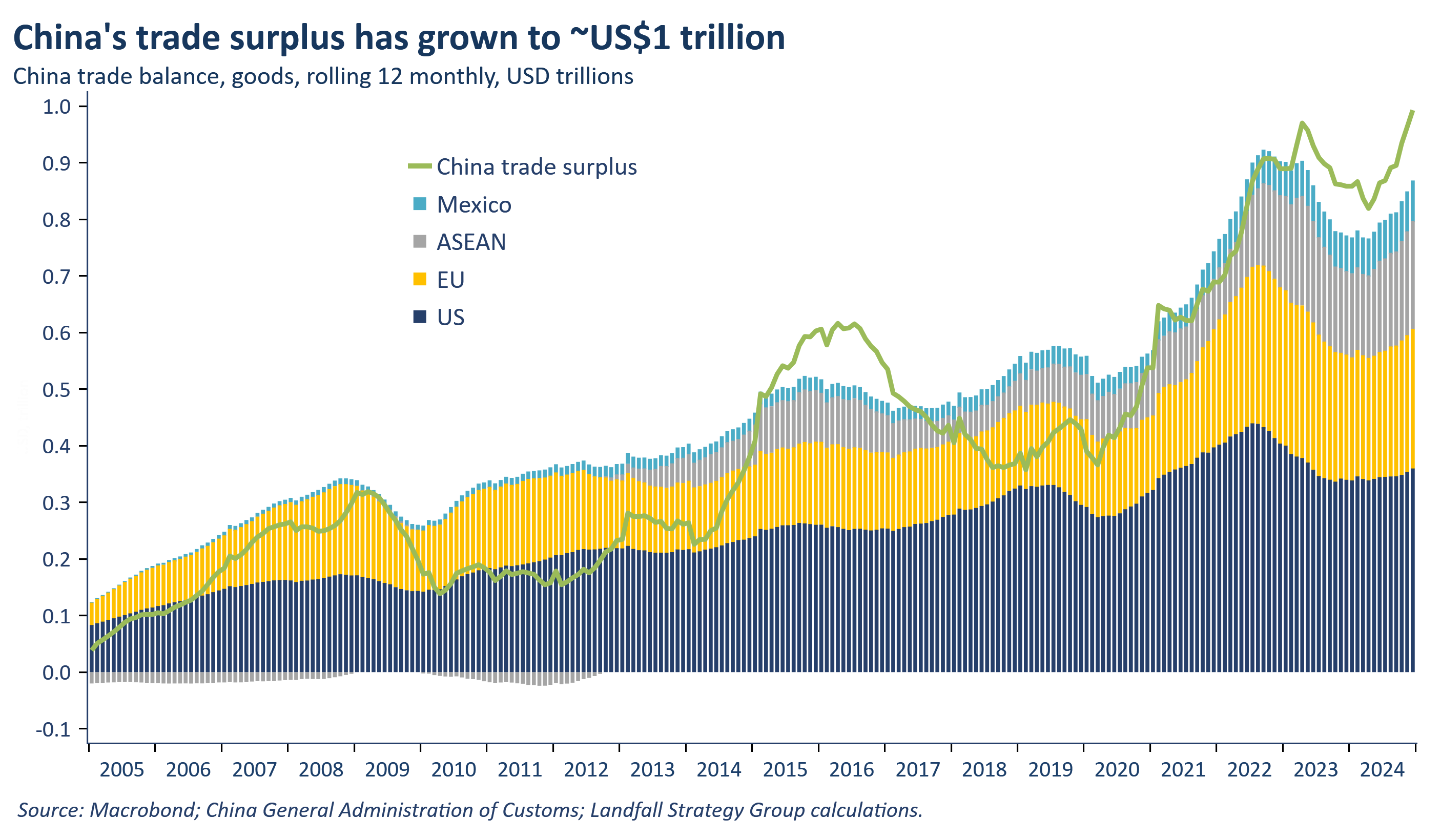

6. $1 trillion

One of the drivers holding up Chinese GDP growth has been its external balance. China’s merchandise trade balance for the year to December 2024 was just under US$1 trillion, a new record in absolute terms (and >5% of China’s GDP), supported by China’s aggressively mercantilist policies. This is creating stresses across the global trading system. Most obviously, the large trade surplus with the US ($360 billion) is leading to trade tensions and tariffs; and Europe is imposing tariffs against subsidised EV exports. Tensions are also rising elsewhere as China increases exports to countries in Asia, Latin America, Africa, and so on, leading to concerns about deindustrialisation in some of these economies. These pressures will become more acute as China redirects exports away from the US; even countries not directly subjected to US tariffs will be impacted by the indirect effects.

7. Washington Consensus

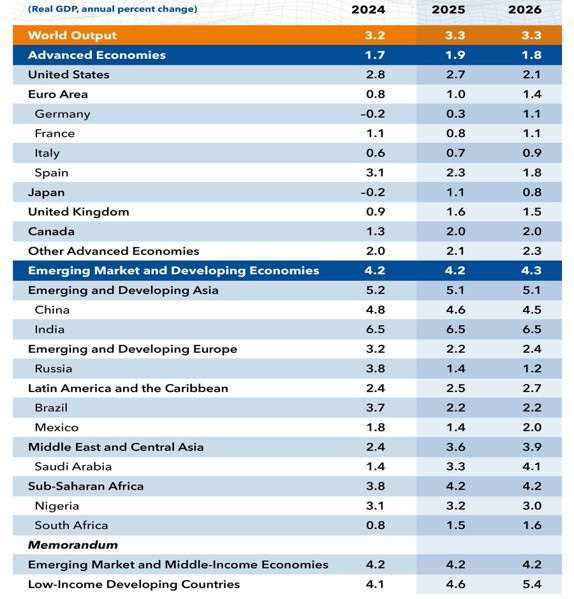

The IMF’s January World Economic Outlook confirmed the consensus view: ongoing US exceptionalism (GDP growth for 2025 was marked up to 2.7%), a weak Europe/UK outlook (eurozone growth marked down to 1.0%), and a slowing China (4.6% in 2025). There is much that is sensible about this consensus, but there are plausible scenarios in which this consensus is wrong: a US economy that under-shoots (tariffs, uncertainty that deters investment, and so on), a European economy that generates momentum on reduced household and government savings, and some supply side reform; and strengthening growth in China (stimulus, technology). The distribution of possible economic outcomes this year is very high.

8. Grey zone conflict

Geopolitical tensions continue to be evident around the world, and in expanding ways. One marker of this is the increasing incidence of grey zone conflict, which is short of direct conflict – and retains deniability. There have been several sabotage episodes in the Baltic Sea with undersea cables being cut by anchor dragging: Chinese/Russian ships are implicated in these, but it has been difficult to prove. These efforts are ongoing; and should be seen alongside Russian efforts to plant explosives in courier packages in Europe. War is extending beyond the battlefield. And undersea cables around Taiwan have also been sabotaged using similar methods, with suspicion falling on Chinese ships. This sort of episode is a likely way of squeezing Taiwan, short of invasion. Expect more of this grey zone conflict.

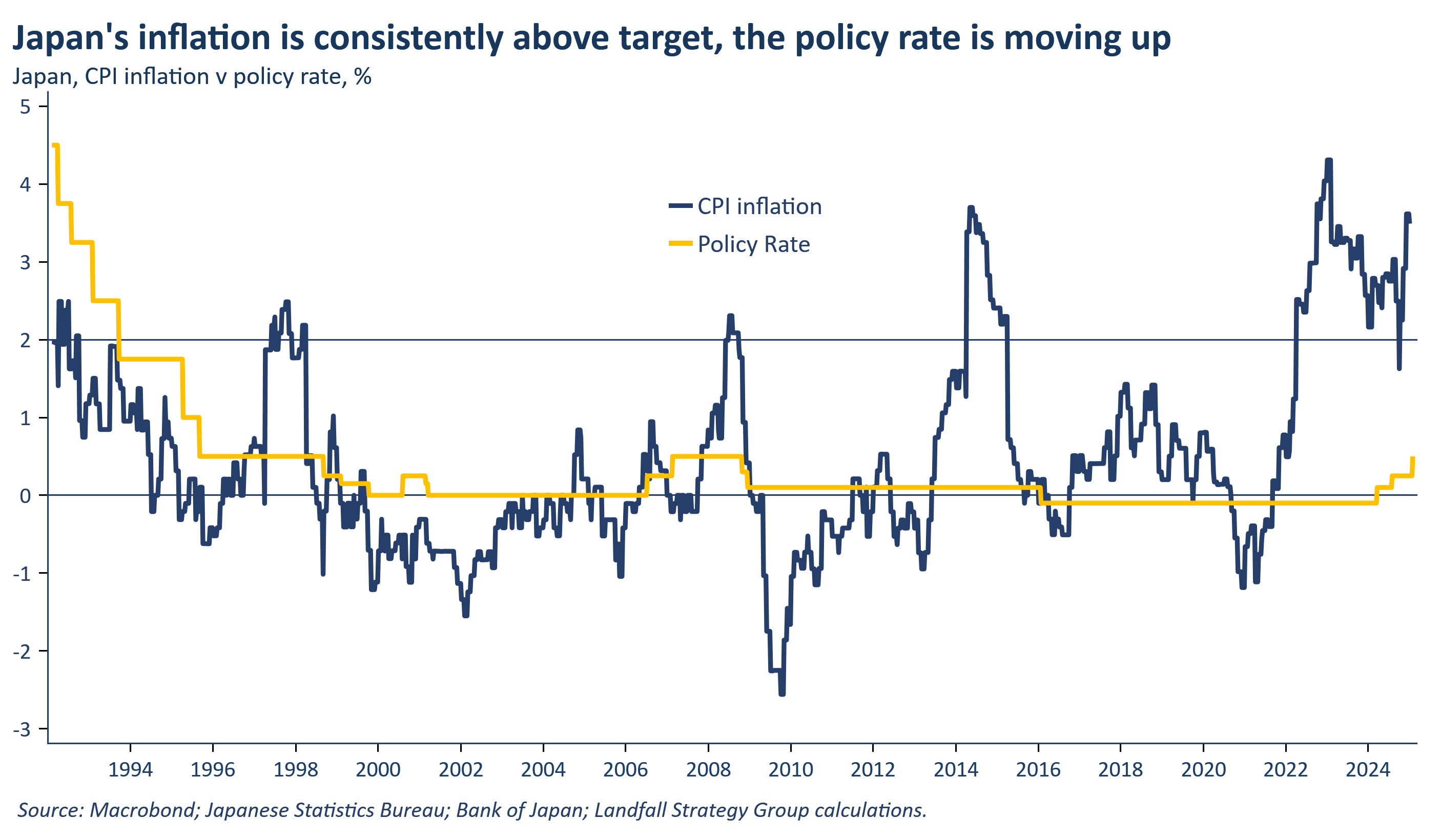

9. Japan normalises

Earlier this week, Bank of Japan Governor Ueda noted that Japan's economy was in a state of inflation not deflation. After decades of consistently low inflation (and periods of deflation), Japan’s CPI inflation is above 3% and wage growth is ~5%. And the BOJ forecast that core inflation will remain above 2%. This provides space to continue to raise policy rates, currently sitting at 0.5% after a January increase – the highest level since 2008. Given the amount of Japanese capital invested offshore, increasing rates (at the same time as rates in other advanced economies are reducing) could have tectonic impacts as capital moves back home: watch for the impact on the JPY/USD, currently siting at around three-decade lows, as well as global risk assets.

10. Golden times

Gold prices have repeatedly hit new highs over the past weeks, even as the prospect of multiple Fed rate cuts recedes, sitting well above its historical relationship with US real interest rates. The gold price has been supported by strong central bank demand: since Q3 2022, central bank quarterly purchases have been about double that of the decade previously on demand for diversification. And broader concerns about geopolitical risks and US policy behaviour are supportive of gold prices. There are many markers of economic and political risk out there, but the gold price is one of my preferred measures.

Thanks for reading small world. This week’s note is free for all to read. If you would like to receive insights on global economic & geopolitical dynamics in your inbox every week, do consider becoming a free or paid subscriber. Group & institutional subscriptions are also available: please contact me to discuss options (more information is available here).

*David Skilling ((@dskilling) is director at economic advisory firm Landfall Strategy Group. The original is here. You can subscribe to receive David Skilling’s notes by email here.

11 Comments

The demographic story in China is playing out as people have expected/projected. The lack of immigration will mean this population crash is going to continue apace.

The recent collapsing rates of fertility in India will likely have a more profound effect on the OECD because we are very reliant on immigration from India.

Immigration hurts locals, the market will adjust. Might take a little longer to order a pizza.

Immigration hurts locals

Not when we rely on some skilled immigrants such as GP's and surgeons, given so many of our own head abroad after study.

China has a problem with not enough jobs for the young. Which does not fit with the usual narrative of population decline.

The lack of youth Jobs is a problem in China, yet the larger and more pertinent problem is the 80 to 100million housing units that have been built - with no one around to occupy them.

This is sinking the Chinese economy, with Debts that cannot be refinanced or repaid.

NZs problem is smaller, with just many thousands of townhouses, without occupants.

Balance sheet recession.

I'd go with Grey Zone Conflict being the biggest potential disruptor. I wonder if every time a cable is taken out - whether Musk Starlink subs go up in the nation disrupted temporarily?

Could not agree more. And the cloak and dagger of days gone by has morphed into black operatives of scary sophistication and import. While the world has advanced enormously with electronic capability so to has the dependence on the same, and attendant vulnerability.

Needs more loose coupling between countries with data centres on shore……

And the perpetrators being called out. I am not sure why the West would buy things off countries that have proven to be doing this.

Agree Kate and I only feel this will get worse. It is all to simple to damage cables and electric connections.

I've been advised it will take 10 years to get new underseas cables to replace the current ones across the cook straight as the demand globally for these is very high.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.