Summary of key points:

- Trump back-tracks on tariffs - for the meantime…

- Tariffs, commodities and the Aussie dollar

- Investment and competition will solve New Zealand’s productivity problem

Trump back-tracks on tariffs - for the meantime…

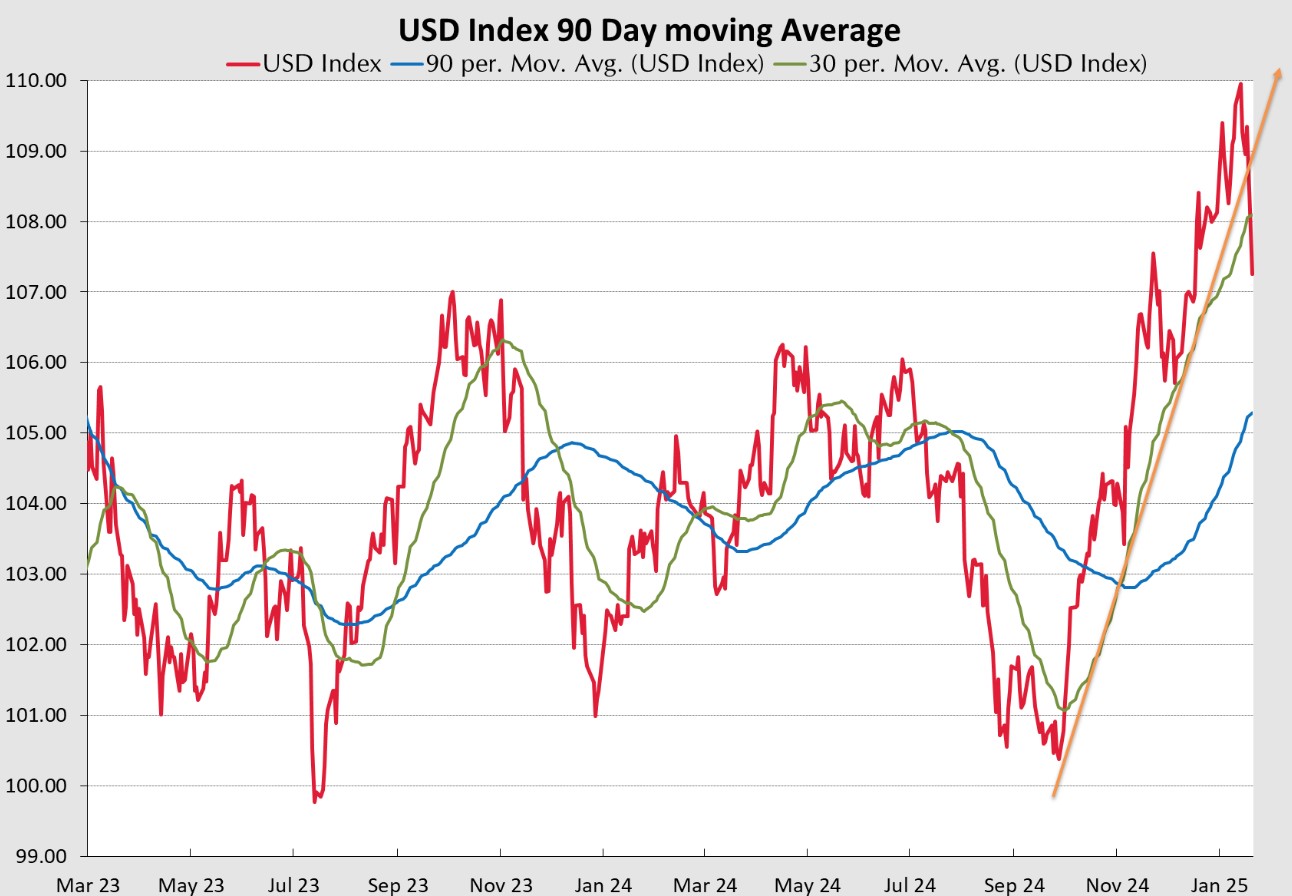

The US dollar had its worst week in almost 18 months last week, depreciating from 108.60 on the DXY Index to 107.25 (refer to the chart below). President Trump’s speech at the World Trade Forum in Davos adding to the US dollar selling as he mused that he would prefer not to impose import tariffs on China if they would negotiate to meet some of his other demands. It does appear that Trump’s ultimate motivation with the tariff threats to China, as well as Canada and Mexico, is to stop the flow of drugs across the border to address the horrific opioid problem in the US. Time will tell if regulations and laws can stop the drug trade. There were many commentators who offered the view before the US election that the whole Trump tariff policy was merely a negotiating tactic to achieve other objectives. No matter which way you may interpret the recent events with Trump not actually imposing 60% tariffs on Chinese imports on “day one”, however seemingly back-tracking on his promise, the risk of a nasty global trade war in 2025 has receded.

The US dollar buying under the euphoria of the “Trump Trades” since October 2024 has certainly run out of steam, and we are now seeing some serious USD selling on profit-taking. As a result, the Kiwi dollar has been able to claw itself off the bottom at 0.5540 and trade higher to above 0.5700.

While the Trump rhetoric on tariffs may have changed over recent weeks, we really have to wait for the various reports from the America First Trade Policy groups that are due on 1 April 2025. Following the reports due on that date, changes to the tariff policies could be announced, likely taking effect 30-to 60-days later. The conclusion at this point, is that the tariff threat and the potential retaliatory tariffs from China and the Europeans, have not turned out as bad as most expected. Therefore, the feared negatives for the global economy are reducing and that is why the US dollar is now losing its value as the risk reduces.

While the tariff question will still be a dominant influence over the US dollar direction over coming months, how US economic data prints relative to prior forecasts will be just as important.

We still expect another U-turn by the US Federal Reserve on interest rates in March when they realise that their fears of rising inflation in 2025 are unfounded.

Do not expect an interest rate cut by the Fed at this week’s meeting on 31 January, however the actual inflation evidence should be in front of them by the 20 March meeting that the annual inflation rate is tracking to 2.00% this year, not 3.00% as they worried about back in December. An example of the current strength of the US economy not being as robust as forecasters have been predicting, was the December S&P Global Services PMI Index coming in at a weaker 52.8 compared to prior forecasts of a stronger 56.6. The outcome of the PCE Inflation figures for December, due this Friday night 31 January, may also be another case of softer than expected data. The consensus forecasts are for a 0.30% increase for the month, whereas a lower 0.10% or 0.20% would seem likely on the evidence of the earlier weaker CPI inflation measure for December. Further US dollar selling is likely before and after the inflation numbers as the previous expectation of only two 0.25% interest rate cuts from the Fed this year is adjusted higher.

The US dollar gains since October have been spectacular from 100.50 on the Index to almost 110.00 two weeks ago. That upward momentum has now been lost and at 107.25 the Dixy Index is already trading below the 30-day moving average level. Soft US inflation and jobs data over the next two weeks could well see the USD Index drop to below the 90-day moving average point of 105.25. That would signal the end of the USD bull run and add to a new downward trend.

The prospect of the USD Index depreciating back to the 105.00 area would allow the NZD/USD exchange rate to lift to 0.5950, confirming that another spike lower in the Kiwi dollar to 0.5500 has been as short-lived as all the previous occasions.

Tariffs, commodities and the Aussie dollar

The commodity markets were hopeful that President Trump’s trade policies against China would not be as aggressive as first feared, and it looks like it is turning out that way. As a consequence, commodity prices have not declined as many would have anticipated ahead of a potentially bad global trade war. Copper prices are today well above the lows of the last six months and iron ore prices at US$101 a tonne have held well above the lows of US$92 a tonne of last October. Whether these commodity prices can make further gains depends on Chinese demand. Recent Chinese economic data (industrial production) has been stronger than forecast, indicating that we finally have some improvement in the Chinese economy. Coupled with the AUD/USD exchange rate being at a very low point in its cycle at 0.6300, the resultant AUD prices and profits to the Australian mining sector are major positives for the Australian economy and government.

Australian CPI inflation data for the December quarter being released this Wednesday 29th January should come out at the forecast 0.50% increase, reducing the headline annual inflation rate from 2.80% to 2.20%. However, the Reserve Bank of Australia (“RBA”) make their interest rate decisions based on the “Trimmed-Mean” calculation of annual inflation (removes volatile extreme high and low components), which is much higher at a 3.50% annual rate and will only decrease to 3.40% after the December data. It is hard to see the RBA having sufficient evidence to cut interest rates at their 18th February meeting, particularly as the labour market has remained much stronger than what they anticipated.

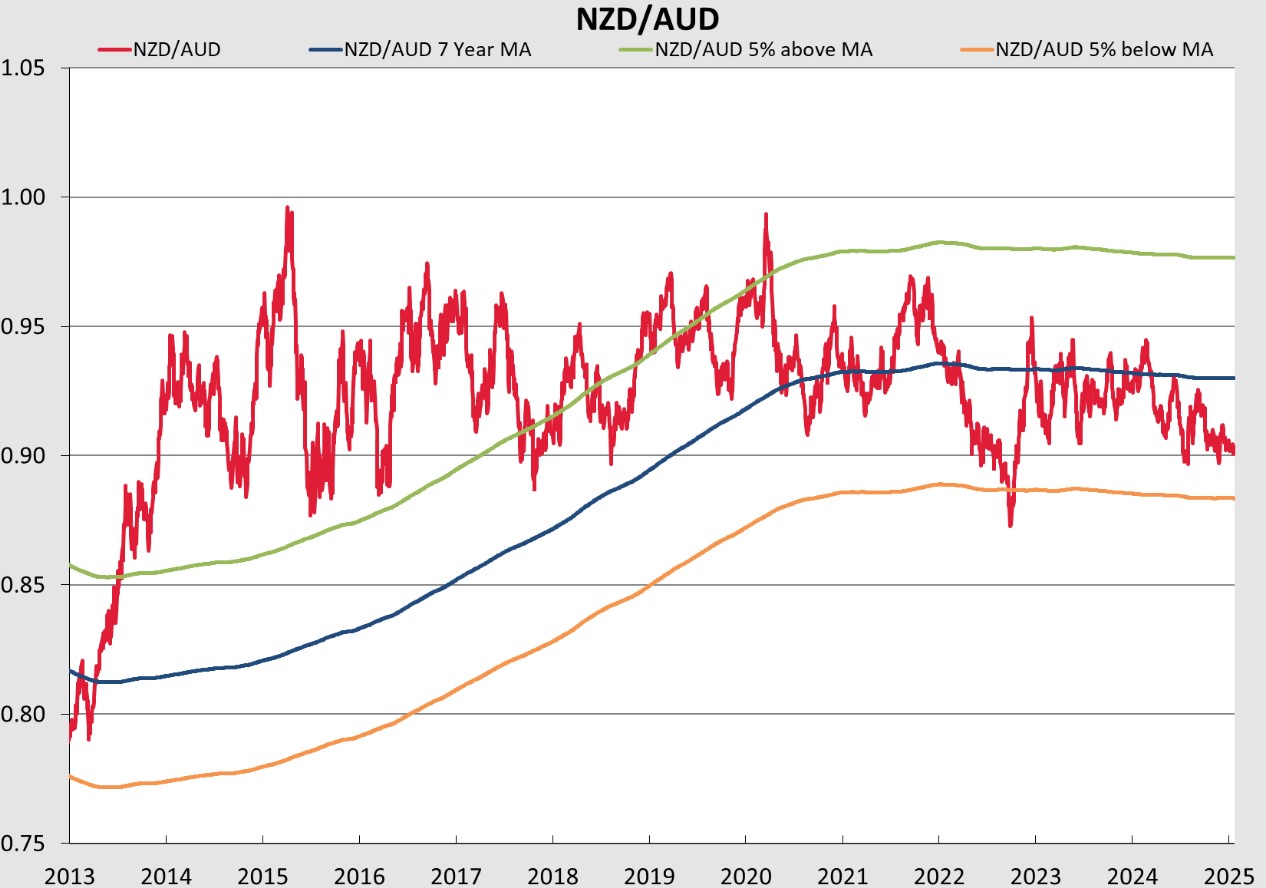

The potential scenario of the RBA not cutting their OCR interest rate on 18th February, however the RBNZ delivering on their promised 0.50% interest rate cut the next day at their 19th February meeting, points to further downward pressure on the NZD/AUD cross-rate from its current 0.9040 level. Historically, dips below 0.9000 in the NZD/AUD rate have also been very short-lived. Therefore, local AUD exporters are recommended to be loading up on longer-term currency hedges in the 0.8900’s. Looking further into 2025, the relativity between NZ and Australian monetary policy settings changes again with the likely scenario of the RBA cutting interest rates in the second half of the year, however the RBNZ will have finished cutting in February or March. Under this scenario, the NZD/AUD lifts back up gain to near its long-term average of 0.9300.

Investment and competition will solve New Zealand’s productivity problem

Prime Minister, Christopher Luxon delivered a very upbeat “State of the Nation” speech last week, focusing on stronger economic growth pulling up households, businesses and his Government into improved financial positions in 2025.

The economic policy initiatives of better welcoming foreign investment and the quality of Government spend on scientific research are however only a small part of the bolder economic reforms that are required if we are to emulate the economic success stories of Ireland, Denmark, Singapore and Israel.

What was missing from the PM’s economic analysis is what New Zealand has to do to improve is woeful productivity record. Hordes of economists are very good at decrying the poor NZ productivity record; however, they very rarely proffer the specific economic policy solutions that will improve matters.

There are two good reasons why our productivity levels remain below those of peers: -

- The absence of “economies of scale” in NZ manufacturing, food/fibre processing and distribution. Our small size and challenging geography just work against the most efficient deployment of capital, which results in sub-optimal output.

- Our retail sector, which does not produce much at all in an economic sense, employs far too many people, which drags down our productivity numbers.

There are two things that will improve New Zealand’s productivity capability and performance – investment and competition. The investment does not just have to be foreign sourced as the PM suggests, however the NZ Super Fund and KiwiSaver schemes could allocate higher weightings to local investment opportunities if the risk/reward metrics stack up. With the NZD/USD exchange rate at cyclical lows below 0.6000, why wouldn’t these fund managers allocate higher weightings to local assets from foreign investment assets at this time? The investment monies are available to solve our productivity problem, it only needs the scale and returns to be sufficiently attractive.

The competition solution is somewhat harder. Innovative ideas are required as to how we go about improving true competition in our less competitive industry sectors such as banks, energy, domestic air travel, supermarkets and building supplies. Luxon’s Coalition government has the challenge to come up with policy prescriptions based on what has worked elsewhere to engender more competition into the New Zealand economy. The RBNZ should be acutely focused on competition in the economy to keep inflation low, however, very strangely, they seem to avoid the subject.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

4 Comments

RBNZ is more concerned about supposed climate change than productivity or competition. The numbers employed at RBNZ have increased dramatically to focus on woke subjects rather than the economy.

Another culture wars narrative sucker. You know this type of messaging is put out there by PR companies who are paid to distract you from the real issues.

Meanwhile Trump has introduced emergency tariffs, sanction cancellation of visa etc because the Colombians insisted he met their reequirement of who was being deported.

And I don't blame them. Why should any nation accept a whole lot of people with no knowledge of who they are.

So not such a good article. Yes I understand you are examining the impacts but come on, Greenland and the 2023 Biden continental shelf claim of the Bering sea and as well Trump's threat to Denmark and Greenland. The oil and mining ambitions of US companies. These American moves do not come out of nowhere!

What is next. Tariffs on the Danes? Because of America's mining ambitions? Trump is the noise out loud but Biden has been positioning on Greenland and like prior Presidents positioning Amerrica and Greenland ignoring the Americans signed in 1916, recognition of Denmarks sovereignity of Greenland.

I think Roger Kerr's analysis of our productivity issue is pretty shallow. Having outlined 2 and I think, perfectly valid reasons why we struggle with productivity, he first suggests that the Super fund and Kiwisaver funds could invest more 'where the risk/reward metrics standup'. Ok, but he had just explained why our lack of economies of scale across the economy makes these metrics largely unattainable. There will be opportunities but not on the scale needed.

he admits that the lack of competition across many sectors of the economy will be hard to crack and I think, probably impossible-see reason 1.

I think there would be merit in raising our R&D spending, in both public and private sectors, but sadly, I see little reason to believe that we will 'solve' our very long-standing and deep-seated productivity issues. If any government of recent times was going to make a dent in the problem, it must surely have been John Key's 9 years in office, but he did nothing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.