Summary of key points: -

- Market pricing at odds with softer US inflation data

- How the Yen and the Yuan drive NZD direction

- Inflation challenges for the RBA and RBNZ

Market pricing at odds with softer US inflation data

The data released on the US economy over this past week has generally printed on the softer side, reminding the markets that the stronger economy and higher inflation they have been pricing into the US dollar, in particular, is by no means certain to actually occur.

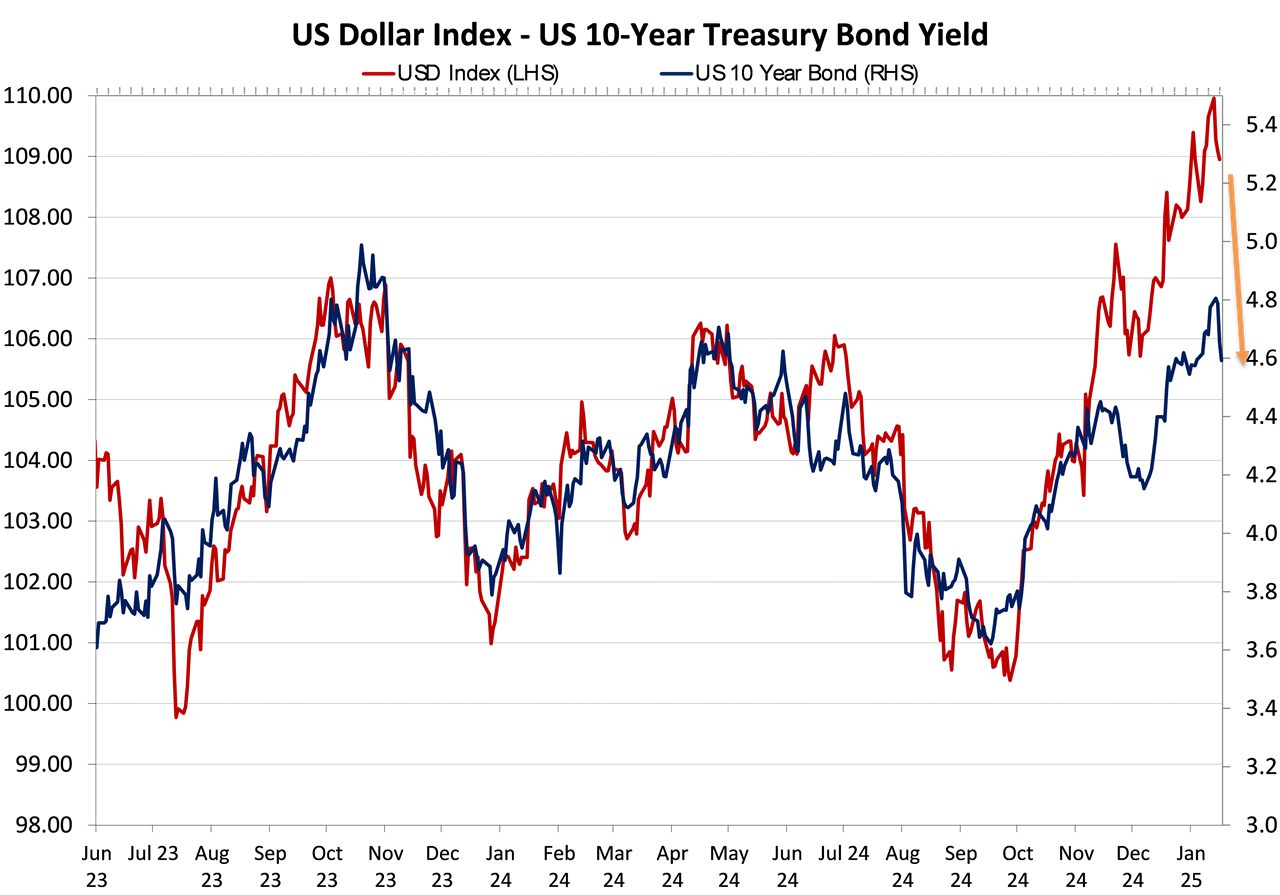

Interestingly, the US 10-year Treasury Bond market did react to the weaker than expected inflation results with market yields pulling back from the highs of 4.80% a week ago to 4.62% by Friday 17 January. Typically, the US dollar Dixy Index follows the bond yields in direction (refer to the chart below), however the USD has remained elevated at 109.20 ahead of Donald Trump’s inauguration as President on Tuesday (NZT). The current divergence between the two indices is unusual and it appears inevitable that the US dollar will also move back down, it just needs a catalyst to prompt the USD selling.

The currency speculators sitting on “long-USD” positions have been unwilling to sell the USD at this point as they await the President Trump “big bang” announcement on promised tariff increases on imports into the US. There is possibly the first stand-off between Trump and his economic policy team already brewing as Trump favours immediate 60% tariff increases on Chinese products and a 10% increase on the rest of the world. Treasury Secretary, Scott Bessent favours implementing tariff increases progressively over time (2% to 5% increases per month has been reported) so as to not push inflation up. The forex markets are anticipating a tariff policy announcement from Trump immediately after this week’s inauguration. They may be disappointed on that expectation; in which case the US dollar has the potential to correct back to the 105.00 level as it catches up to the lower bond yields.

The weaker than forecast US economic data released last week that pushed the bond yields lower is summarised as follows:-

- Producer’s Price Index (“PPI”) – wholesale prices increased 0.20% in December, below the 0.30% forecast. Core PPI prices were 0.00% against a +0.20% prior forecast.

- CPI Inflation – Whilst the headline inflation increase for December was bang on the forecast of +0.40%, the core CPI measure (excluding food and energy) came in at +0.20%, less than the +0.30% prior forecast. The shelter index (cost of housing/rents), accounting for over 67% of the annual increase, rose 4.60% over the year, marking the smallest annual gain since January 2022. The shelter component has a dominant 35% weighting in the Core Index and due to the extreme lagged nature of the data, will continue to decrease over coming months.

- Retail Sales - The December increase of 0.40% was the lowest in four months and below consensus forecasts of +0.50%.

Looking ahead, the next “market moving” pieces of data will be US GDP growth for the December 2024 quarter (+2.70% pa forecast) on 30 January and PCE inflation for December on 31 January, where a 0.30% increase is forecast. Given the continuing decreases in shelter/rents in the CPI measure of inflation, it would not be surprising to see the PCE measure print below the +0.30% forecast pushing bond yields and the USD lower.

The Federal Reserve next meet on 29 January, so they will not have the PCE inflation data available. The interest rate market is currently pricing for no cut on 29 January and only a 50/50 probability for a cut at the following 19 March meeting.

The long USD speculative positioning on the Trump Trades has become extremely crowded and has lasted for longer than we anticipated. The latest US economic trends suggest an unwinding (i.e. selling USD), however the possibility of a “big bang” tariff policy announcement from Trump is keeping the USD bulls satisfied for the moment.

How the Yen and the Yuan drive NZD direction

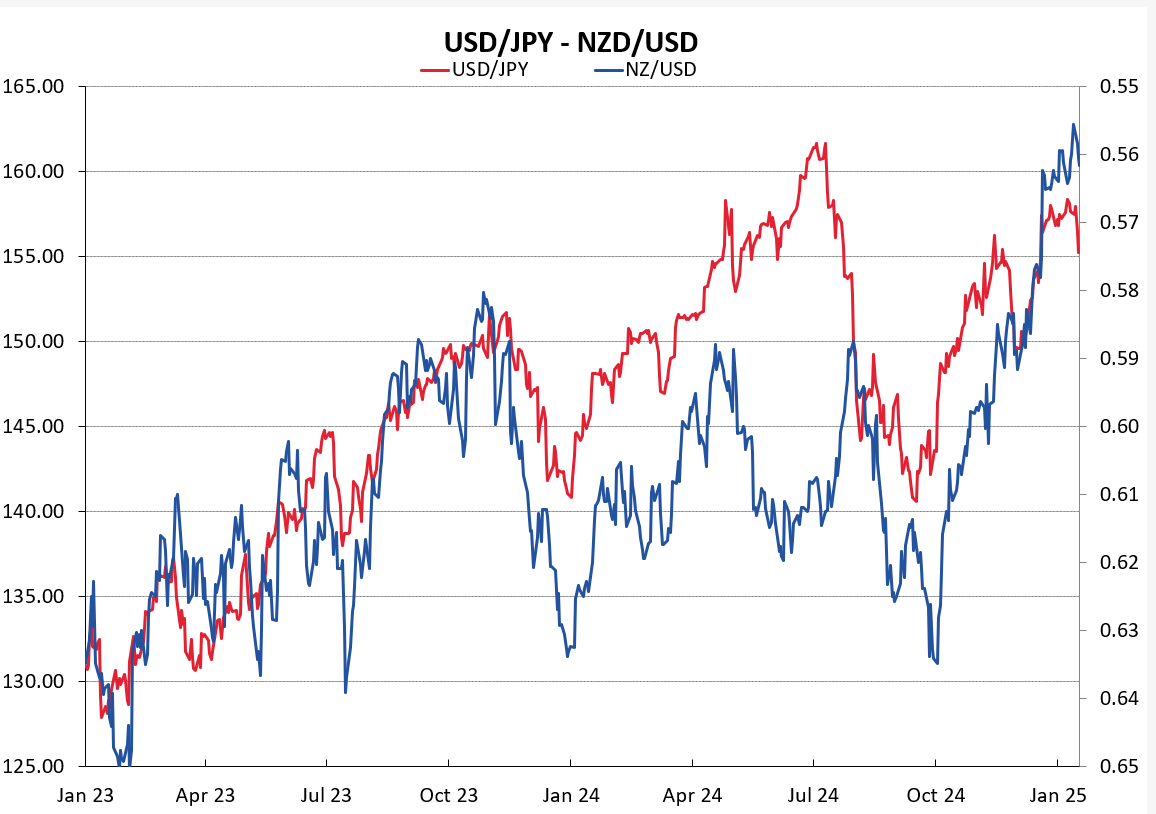

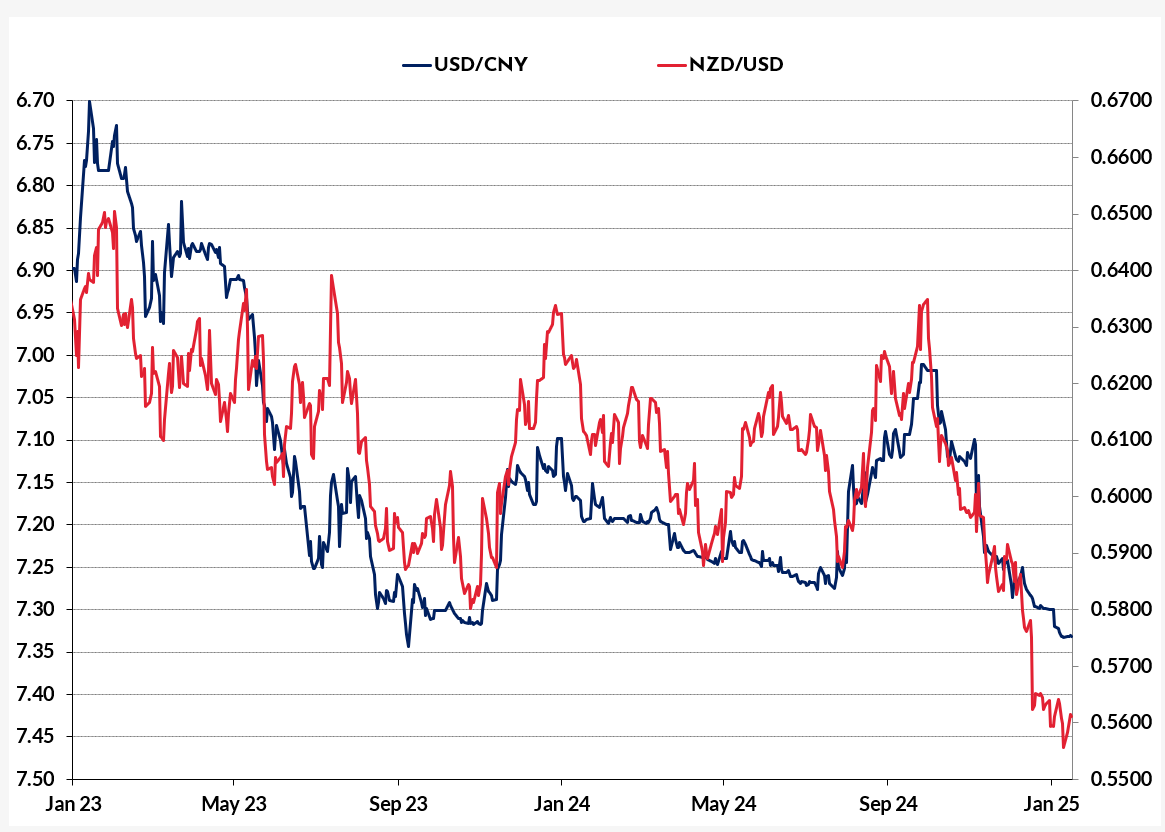

The Japanese Yen is the largest free-traded currency in the Asian/Pacific region and the NZD and AUD have to be regarded as Asian currencies, therefore there is a reasonably close correlation between JPY and NZD movements against the USD (refer chart below).

The Bank of Japan did not increase their interest rates in December; however, it is looking very likely that they will hike rates at their next meeting on 24 January. Over this past week, the Japanese Yen has bucked the trend of other currencies remaining weak against the Trump Trade USD, the JPY strengthening from 158.40 to a low of 155.30 (currently 156.30). Bank of Japan Governor Kazuo Ueda has hinted at a likely interest rate increase as wages and inflation continue to increase in Japan. The Japanese have been hesitant to increase their interest rates as they fear another global equity market crash, they sparked last July/August when they first lifted their rates. Inflation figures for December are released on the same day as the Bank of Japan meeting. The annual inflation rate is forecast to increase from 2.90% to 3.00%. Outside of USD movements from any Trump announcements on tariffs, the Japanese Yen appears destined to make further gains to 150.00 and below against the USD. The Yen also benefits from safe-haven inflows as a result of potential trade wars disrupting global growth.

The People’s Bank of China (“PBoC”) has so far been successful in defending the Yuan at the 7.3500 level against the USD. There have been record capital outflows from China over the last 12 months as foreign investors pulled their money out on China’s faltering economic performance and weak equity markets. Chinese corporations have also had a strong appetite to invest offshore. The Chinese authorities will need to implement more effective monetary and fiscal policy stimulus packages this year to entice households to spend rather than save, if they want to slow the exit of capital and stabilise the Yuan.

Chinese December economic numbers were all stronger than forecast last Friday with annual GDP growth +5.40% (forecast 5.00%), Industrial Production +6.20% (forecast 5.50%) and Retail Sales +3.70% (forecast +3.20%). The Yuan strengthened to 7.3230 as a consequence.

Inflation challenges for the RBA and RBNZ

The debate rages on in Australia between economic forecasting groups as to whether the Reserve Bank of Australia (“RBA”) should cut their interest rates in February or May. There continues to be enormous political pressure on the RBA to make the first cut in February as that would lower mortgage interest rates well before the May general election and lift the Albanese’s Labour Government chances of reelection. The economic trends point to a later cut as being more prudent. The increase in the number of new jobs each month in Australia continues to run well above RBA forecasts, so whilst the labour market is hotter than expectations, the case for rate cuts is not a strong one. State Governments in Australia are under pressure to concede to large public sector wages increase demands. Rail workers in Sydney after a 32% pay rise over four years are taking industrial action, New South Wales hospital specialists are going for a 25% pay increase and Melbourne policy officers want 24% over four years. The RBA is hoping the cash-strapped state governments will not bow to the aggressive public sector union demands. These issues will be central themes in the upcoming election campaign.

Ahead of the 18 February RBA meeting, the CPI Inflation outcome for the December quarter on 29 January will be crucial for their decision making. The annual headline inflation rate is forecast to reduce from 2.80% to 2.20% pa; however, the RBA prefer the “trimmed mean” CPI measure (excludes the volatile and outlying largest increases and decreases) which is forecast to come in at +3.40% pa – well above their target of 2.50%. The headline CPI inflation increase of 2.20% is artificially reduced by 0.40% due to the Government’s electricity subsidy to households. A decision not to cut interest rates on 18 February would be positive for the Australian dollar (outside of USD influences).

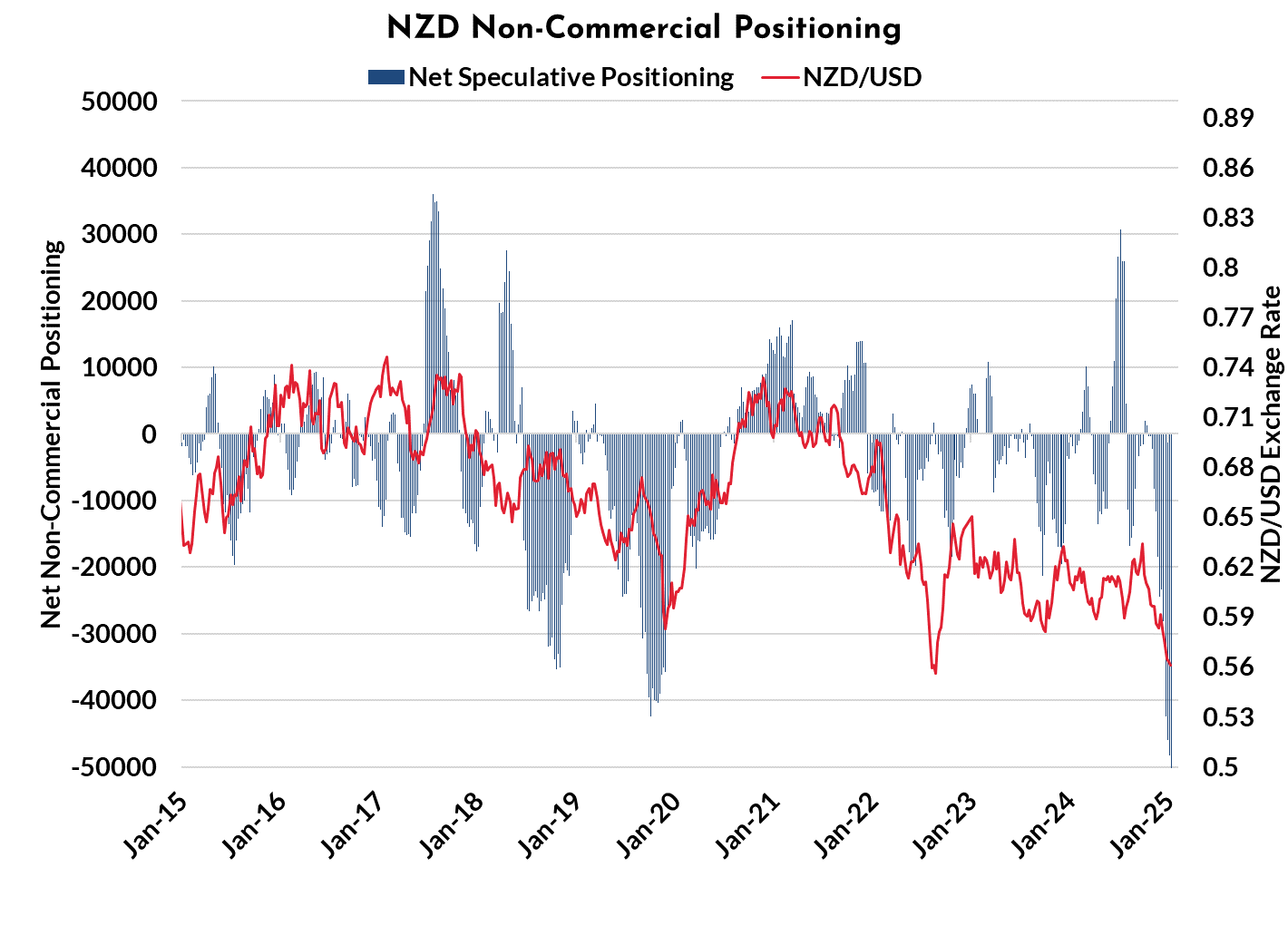

In New Zealand, the case for the RBNZ making a 0.50% cut at their meeting on 19 February is weakening with a lower Kiwi dollar contributing to higher food and fuel prices. CPI inflation data this Wednesday 22 January is likely to be at the forecasts of a 0.50% quarterly increase, producing a stable 2.20% annual rate. The FX speculators have increased ‘short-sold” NZD positions over recent weeks to record high levels (refer chart below). The extreme short-sold positions never last too long, leaving the potential open for a rapid Kiwi dollar recovery as they are closed-out.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.