Summary of key points: -

- Fed interest rate forecast “Dot-Plotters” lose the plot!

- Outlook for the New Zealand and US economies in 2025

Fed interest rate forecast “Dot-Plotters” lose the plot!

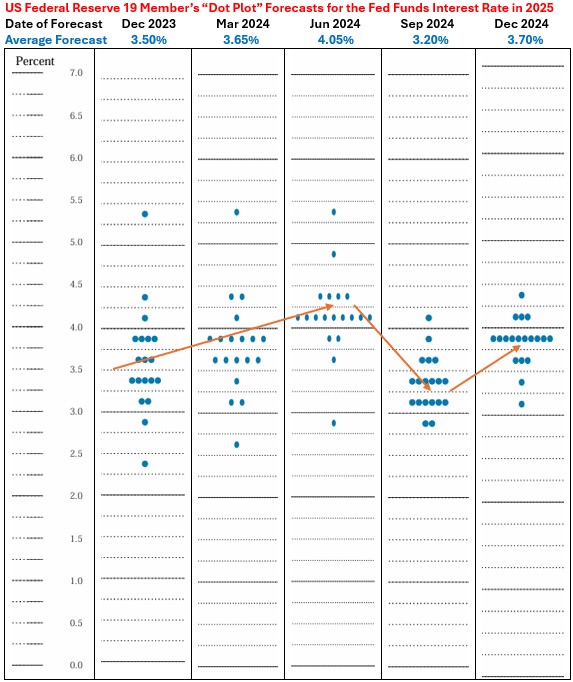

The US Federal Reserve famously “pivoted” on their monetary policy settings and interest rate forecasts in December 2023, signalling four times 0.25% cuts to the Fed Funds interest rate in 2024. The December 2023 “dot-plot” of the 19 Fed member’s individual forecasts for the interest rates over the 2025 year came in an at an average of 3.50% (refer chart below). By June 2024, stronger than expected inflation and jobs data in early 2024 progressively lifted the dot-plot forecasts to 4.05%.

However, by September 2024 the Fed members had dramatically revised their interest rate forecasts to a much lower 3.20% average for 2025. Softer inflation and jobs data through the middle months of 2024 were behind the sudden change in view and outlook. It now appears the nineteen Fed members have been roundly spooked by the Trump regime threat of increased tariffs on imports into the US, forcing another about turn last month in their dot-plot interest rate forecasts. The Fed again pivoted on their monetary policy stance by reducing the previous indicated four times 0.25% cuts to the Fed Funds interest rate in 2025 to only two 0.25% cuts. The previous forecast 3.20% average rate for 2025 has now increased to 3.70%.

The constant flip-flopping in their outlook instils absolutely no confidence whatsoever that the actual Fed Funds interest rate for 2025 will be anywhere near the latest 3.70% forecast, when we look back on the year in 12 months’ time. All we can conclude is that the Fed members have no conviction on a medium-term view and merely knee-jerk to the latest month’s inflation and jobs data as it is released. The historical track-record of their forecasts is one of volatility and inaccuracy. Therefore, one would expect that the financial markets would hold a fair amount of scepticism about the December pivot of fewer interest rate cuts in 2025. However, that is not how the markets have reacted over the last month. Long-term 10-year US Treasury Bond yields have continued to increase to 4.60% and the US dollar has further appreciated to a high of 109.25 last week. The NZD/USD exchange rate being pushed to a 28-month low of 0.5590 last week as a consequence of the continuing USD strength.

The ever-changing Fed interest rate forecasts and monetary policy signaling has not allowed any room for the expected “profit-taking” on the “Trump Trades” of short-sold bonds and long-USD speculative positions before the end of December 2024.

It does pay to look back on the events of recent months as it frames the forward-looking view of how exchange rates may move from current levels over coming months. The official Fed inflation forecasts for 2025 were increased at the 18 December 2024 Fed statement. Continuing moderate GDP growth, tariffs and sticky services sector inflation appears to be behind the Fed’s December change in heart compared to their September view that inflation would move to below their 2.00% annual rate target.

Our view is that there is greater than 50/50 probability that by March/April 2025 the Fed will again be changing their 2025 interest rate forecasts to lower levels as economic evidence evolves that inflation and jobs are softer than both Fed and market expectations. Already we have seen the November 2024 PCE monthly inflation increase come in at a low 0.10%, below prior consensus forecasts. This coming Friday’s Non-Farm Payrolls employment data for December may well prove to be another piece of evidence that the US economy is not a robust as the Fed and markets currently believe. A monthly employment increase closer to 150,000 than 200,000 may well be a catalyst to reverse the bond yields and the USD currency index lower.

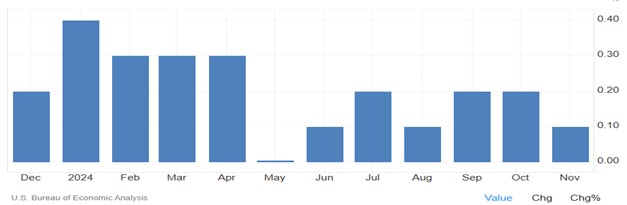

US companies always increase their selling prices once per year at the start of the year. In early 2024 those price adjustments resulted in monthly PCE inflation increases of 0.30%/0.40% (refer bar-chart below). The question is whether US retailers currently hold the same pricing power to repeat those monthly 0.30%/0.40% PCE increases over coming months. We suspect not; therefore, the annual PCE inflation rate will decline, which is not what the Fed and the markets expect to occur.

US PCE Inflation – 2024 Monthly Increases

Fed and market forecasts for US inflation that do not see any further decreases to below 2.00% in the annual rate (instead they see inflation rising to nearer 3.00% over the 2025 year) do not seem to consider the continuing falls in housing and rent components that make up 35% of the CPI and PCE Indices. In addition, the weightings in the inflation measures of imported/tariffed products from China such as toys, clothes, furniture and electronic goods are all very small weightings in the inflation indices. On the demand side, consumer credit costs have not really declined for auto and personal loans, so it is difficult to fathom from which particular part of the economy the upwards pressure on inflation will come from. However, food prices will certainly increase if Trump deports all the immigrant workers who harvest the crops!

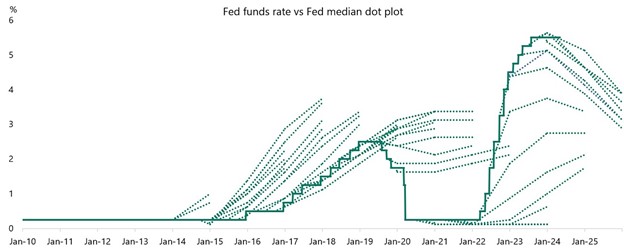

To round-out the commentary on the unreliability of the Fed member’s “dot-plot” interest rate forecasting record, the chart below from Apollo confirms the poor forecasting performance: -

The conclusion from the above analysis is that the US bond and FX markets are likely to react in a surprise fashion to upcoming US inflation and jobs data that does not fit their narrative of increasing inflation and robust jobs/GDP growth in 2025. The expected softer data will cause the unwinding of bond and USD currency positions in January/February, which we originally expected to happen in December. Under this scenario, from the current NZD/USD rate of 0.5615, the Kiwi dollar would be able to make some recovery higher.

Outlook for the New Zealand and US economies in 2025

Two media articles in the Royal New Zealand Herald struck a chord over this last week.

Article 1: “NZ’s top economists pick the big three issues for New Zealand in 2025”

Business Editor at large, Liam Dann canvassed the views of the normal suspects on what will be the major issues for the economy this year: -

Jarrod Kerr of Kiwibank: The unemployment rate will rise to somewhere between 5.20% and 5.50%.

Brad Olsen of Infometrics: Higher interest rates in 2024 will continue to limit household spending.

Sharon Zollner of ANZ: The unemployment rate has risen less quickly than what the RBNZ thought.

Kelly Eckhold of Westpac: Businesses are talking more positive for 2025, however will they put their money where their mouth is?

Stephen Toplis of BNZ: Despite a weak labour market, he lamented that skills shortages still hampers economic expansion to build the infrastructure and service the health system.

Christina Leung of NZIER: Trump’s tariffs pose downside risks to global trade and global growth.

Nick Tuffley of ASB: The lower NZ dollar will provide some offset to Trump’s trade policies.

Cameron Bagrie (Independent): Non-tradeable inflation is still elevated, and fiscal policy still needs to be tightened up.

Oliver Hartwich of the NZ Initiative: Government spending as a percentage of GDP has had a structural shift higher since the Covid pandemic. If you want to keep inflation down, you need to address this.

What was surprising about the article was that there was absolutely no discussion about the principal drivers of the NZ economy - the agriculture and export sectors (apart from Kelly Eckhold briefly mentioning that the terms of trade had significantly improved). Our view is that the material increase in export commodity prices is the dominant issue and development for the economy in 2025 and will propel GDP growth higher – it always does. The majority of the economists are disconcertingly “inwardly looking” and not addressing the important aspects of competitiveness, productivity, business investment and smart marketing of our exports. The lower NZ dollar value is not necessarily a positive either, tradeable inflation will increase with higher import costs.

Article 2: “Donald Trump’s “Maganomics” will damage growth, economists tell FT polls”

According to a recent Financial Times poll of economists “Trump’s vision to reshape the world’s largest economy through protectionist policies that put “America First” will damage growth”. The survey of 220 economists in the US, UK and Europe certainly contrasts against equity market investors’ current bullishness over the President-elect’s plans.

The surveyed economists view is that Trump’s isolationist policies may boost economic growth in the short-term, however they will hurt US economic performance in the medium term. It should be remembered that Trump has yet to lay out a comprehensive economic plan, leaving analysts to base their outlook on pledges and threats made on the campaign trail.

One UK economist summarised the situation as “The Trump administration will be an ‘unpredictability machine’ which will dissuade business and households from taking long-term decisions with ease. This will inevitably have an economic cost.”

The financial markets will now await the detail on the execution and implementation of Trump’s economic policies after his 20th January Presidential inauguration. Market reaction and associated volatility has to be expected and will be represented through the currency markets.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

14 Comments

Excellent article! Thank you.

I don't think anyone knows where the market is heading. The advice to my partner is lock in a 2 year fixed mortgage at 5.49% at the beginning of February.

I've got about $500k due on 27th Jan

Am trying to decide between refixing at 6mth or 1yr, didn't really consider 2yr.

2 year fixed rate is currently the best rate from the ANZ. $500K is a lot so its a bigger gamble.

Welly-FHB , you'd be well advised to ignore the Grifter and seek advice from anyone other than the Grifter. Maybe even someone that understands your financial position and goals? The Grifter's track record on here can be described as "a broken clock is right twice a day". Take care.

"The advice to my partner is lock in a 2 year fixed mortgage at ..."

Just quietly, Zwifter, from what I have read from you, you are in no way qualified to offer financial advice to ANYONE.

Nor are you qualified to engage on a public forum - with ANYONE ELSE - with what THEY should do.

That's hilarious, I advised her to go 5 year fixed at about 3.19% at the time and she went 3 years instead. I didn't get where I am today, basically retired at 48 by being an idiot, but you do you.

What would you do Chris, if you had $500k to refix in the next month or two?

Crickets....

Roger - good article however a focus on the flip-flop nature of the FED is a little harsh given to be fair they have been faced with plenty of challenges and changes of policies throughout the periods you have commented on. If you take a step back and look at their longer term forecasts of the US Fed Funds rate you will note that they have been steadily increasing (when calculated using all individual forecasts and working the average of those) from March 2022 ~2.43% to Dec 2024 ~3.11%. I think this is the real story that people should focus on.

Consumer demand is core of GDP not exports

Market rates in USA are rising by mirror image of Fed cuts because market knows debt means more risk and Trump means more risk. Rates will hence remain higher for longer regardless what a Powell does

I thought at first glance that final dot plot was someone's satirical scribble on paper. There really is some variety in there!

I find that the fact almost every commentator is calling USD higher in 2025 interesting given the fact that it is already significantly higher. And as you mention a lower NZD is a significant stimulant for NZ Inc. As is the transmission of any policy lever it takes longer than markets want it too. Predicting currency moves is a random exercise but I’m not as bearish as consensus for 2025 in our currency vs. USD. I am still curious as to why we are elevated to the AUD when the longer term (post OCR 1999) average is way lower and our economies and hence cash rate differentials are suggesting otherwise.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.