Summary of key points: -

- Is the US dollar overcooked and overextended on its Trump Trade?

- Japanese Yen appreciating again on likely higher interest rates

- NZ Coalition Government one year in – bouquets and brickbats

Is the US dollar overcooked and overextended on its Trump Trade?

The one-way hurtle up the hill for the US dollar on the Trump election euphoria displayed distinct signs of spluttering and stalling last week. Over coming weeks, the probability or risk is that the previous juggernaut starts rolling backwards down the hill. Large-scale profit-taking on speculative long-USD Trump Trade positions was always likely in the month of December ahead of the 31 December financial year-end and Wall Street employee bonus calculations. The US dollar Dixy Index hit a high of 107.50 on 23 November. Over the last seven days it has reversed engines dramatically to fall to 105.83 as the USD selling on profit-taking commences.

The inevitable profit-taking on the USD Trump Trade has allowed the NZD/USD exchange rate to lift off its bottom of 0.5810 on 26 November and move up to 0.5920, despite the RBNZ cutting the OCR interest rate by 0.50% during the week.

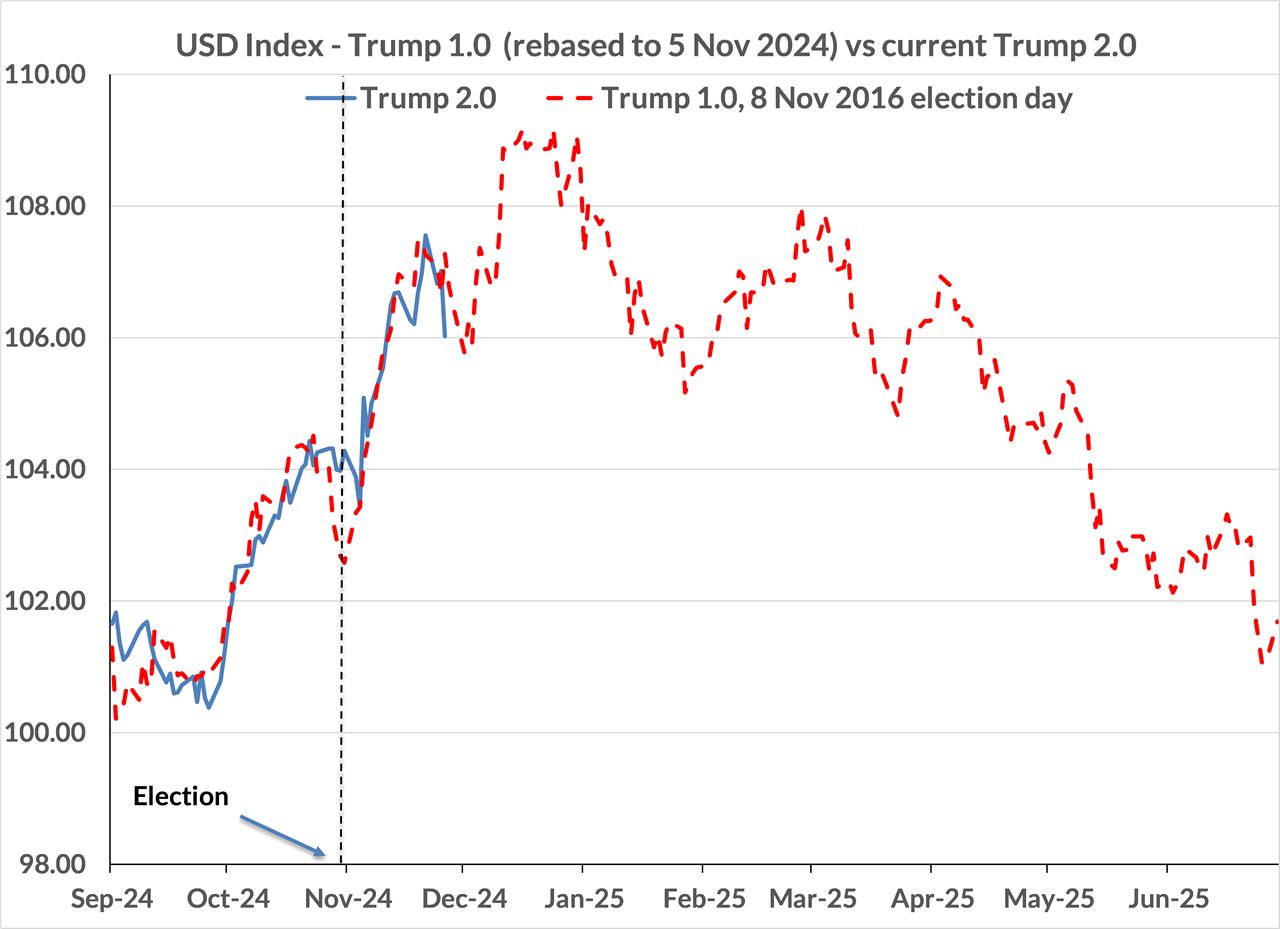

Whether the track of the US dollar before and after the US Presidential election remains on the same script that was witnessed in the late 2016/early 2017 period when Donald Trump was first elected President, remains to be seen. However, so far, the US dollar gains pre and post the election are scarily identical to the 2016/2017 period (refer chart below). Are financial market participants merely anticipating that history will exactly repeat and are today trading the US dollar accordingly?

In 2016/2017 (red dotted line on the chart), it took the US dollar six months to unwind, after peaking at 109.00, to return to its pre-election starting point of 100.00 on the USD Dixy Index.

It appears unlikely that the US dollar will have one last push higher to the 109.00 peak of 2016 this time around and for the following reasons the USD decline is more likely to be within two months, rather than six months: -

- For eight out of the last 10 years the US dollar has depreciated for seasonal and other reasons in the month of December.

- There is a massive incentive for hedge funds and investment banks to square-up their long-USD Trump Trade positions in December so as to crystallise cash gains and cement-in their bonuses.

- Despite all the rhetoric about the impact of Trump’s tariff increases forcing US inflation higher, the reality is that continuing reductions in the dominant housing/shelter component of the CPI index over coming months will more than outweigh any tariff increase.

- The Federal Reserve are highly likely to remain with their plan to cut interest rates by 0.25% at each upcoming meeting, the next being on 18th December.

- Over the last month, US equites gained 6.00%, whilst European stocks fell 3.20% and Chinese equites dropped 5.70% in value. The gap between the relative equities market performances forces investment fund managers to “rebalance” their portfolios so that the weightings of assets in various currencies remains at the mandated percentage limits. In other words, the fund managers need to sell US dollars and buy Euro’s and Yuan this week to rebalance their portfolios to the desired weightings.

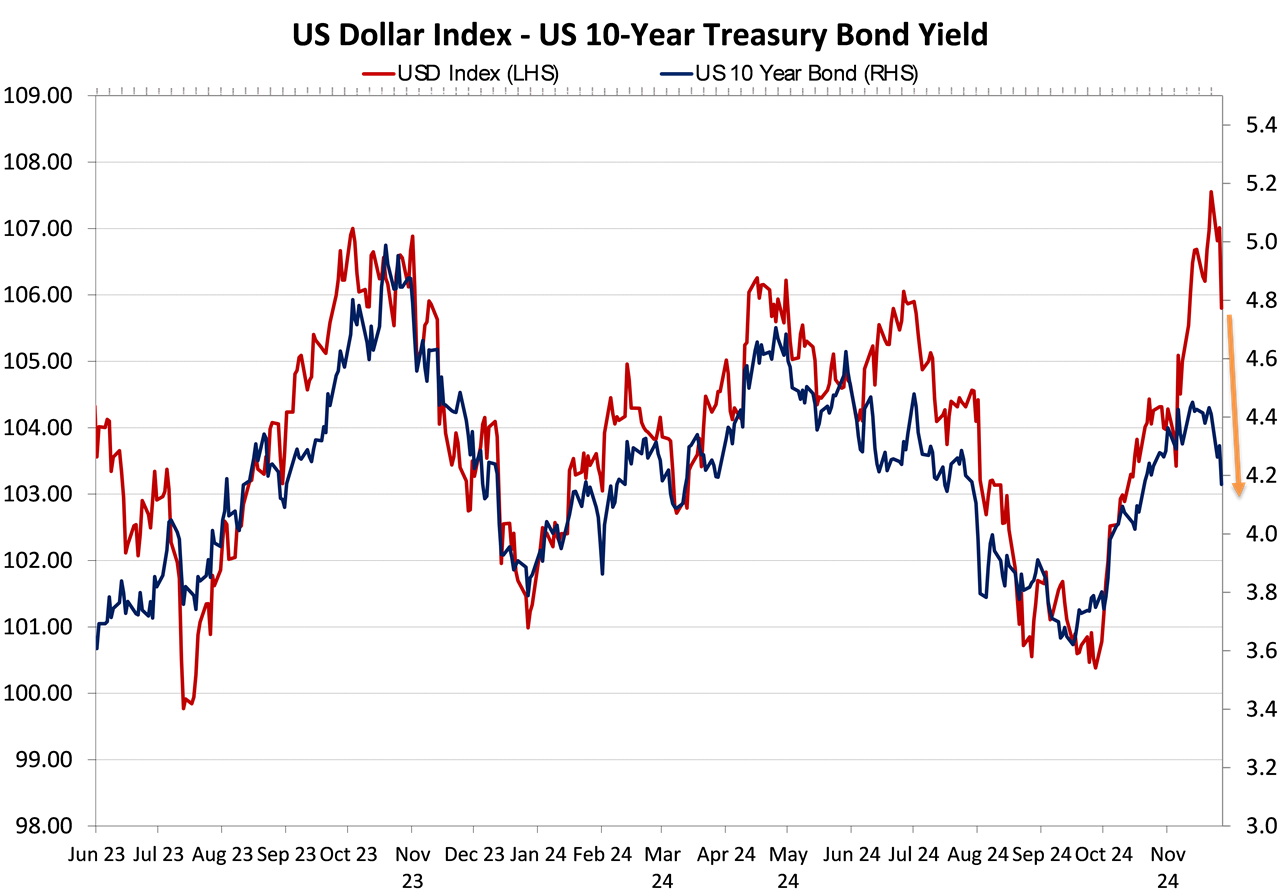

- The US dollar Dixy Index is closely correlated to the movements in the US 10-year Treasury Bond yield. Over this past week, the bond market has also commenced unwinding all the short-sold bond positions put on prior to the election in expectation of higher inflation and larger fiscal deficits under a Trump regime. The 10-year yield peaked at 4.50% on 14 November, it is now tumbled to 4.17% as the traders buy bonds to unwind. The USD Index has some catching up to do, however the environment is ripe for the USD to depreciate to 103.00 and below over coming weeks.

Foreign exchange markets often require a trigger or catalyst to reverse the market sentiment and direction. Looking ahead, this Friday’s US Non-Farm Payrolls employment figures for the month of November may well be that type of economic data trigger that ignites further US dollar selling. Prior consensus forecasts are for an increase in jobs over the month of 183,000 to 195,000. The Non-Farm Payrolls data series is notoriously volatile and prone to large subsequent revisions. Therefore, do not be surprised to see another very soft increase in jobs, as the earlier hurricanes disrupted operations and travel. A weak jobs number for November will reinforce the view that the Fed will still cut interest rates by 0.25% on 18th December.

Further depreciation of the US dollar to the 103.00 area before Christmas for all the reasons cited above would see the NZD/USD exchange rate make further gains to above 0.6100. Yet again, we are witnessing a Kiwi dollar sell-off to below 0.6000 as being as short-lived as all the previous spikes lower over recent years.

Many economic and currency forecasters are predicting that the Chinese will overtly depreciate their Yuan currency value by 10% to 15% next year to offset the impact of Trump’s tariff increases on Chinese imported product into the USA. Over recent weeks since the US election, the Chinese have been very restrained in responding to the tariff threats from Trump. They are prudently waiting to see the detail of the tariff adjustments. If US tariffs do slow down Chinese manufacturing exports, it seems likely that the Chinese authorities will switch their fiscal and monetary stimulus to the retail/consumer spending part of the economy to ensure they achieve the 5.00% growth target. Further good news for New Zealan’s protein exporters to China.

Japanese Yen appreciating again on likely higher interest rates

The Japanese yen appreciated to a six-week high against the US dollar last Friday after faster than expected inflation in Tokyo supported bets for a Bank of Japan interest rate hike this month. The Tokyo core CPI Index increased to a 2.20% annual rate, up from 1.80% the previous month. The Bank of Japan next meet on Thursday 19th December, the day before their inflation data for the month of November. The timing of their meeting before important inflation information is as ill-conceived as the RBNZ allowing the same silly scheduling of their meeting a few months back.

Japanese Prime Minister, Shigeru Ishiba has survived the recent general election and appears to have performed another “about-face” and now supports further interest rate increases to control inflation. It seems highly likely that the Bank of Japan will lift their interest rates by 0.25% and therefore further Japanese Yen gains have to be expected against a generally weakening US dollar over coming weeks.

The Yen has already reversed from 156.60 against the USD on 15 November to trade much stronger to 149.75 last Friday as the market positions for an interest rate hike a day after the Fed will be cutting rates on 18th December.

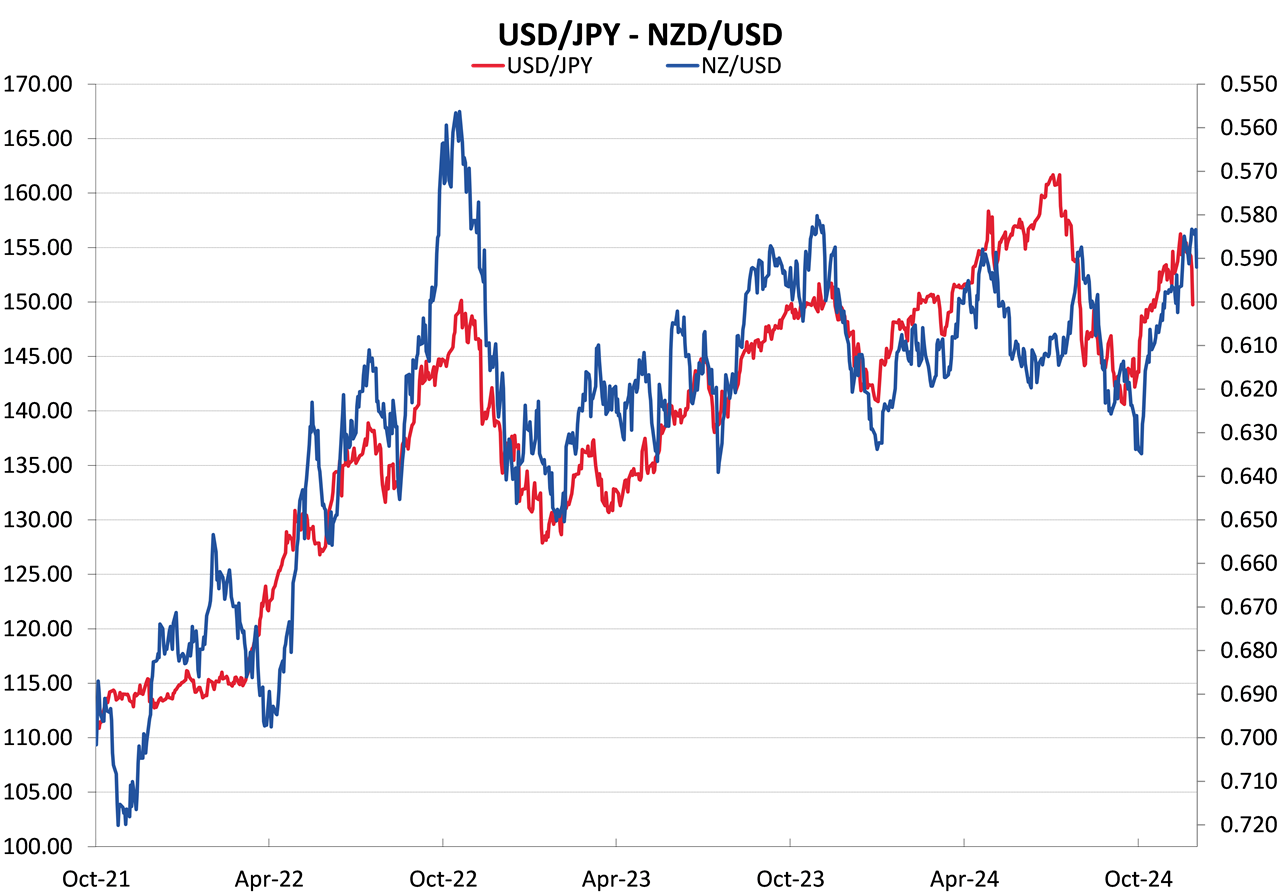

The NZD/USD rate closely tracks the USD/JPY movements, so interest rate changes in Japan is another good reason why the Kiwi dollar is headed back above 0.6000 before Christmas. The Yen appears headed back to 140.00 again, which would see the NZD/USD exchange rate above 0.6200.

NZ Coalition Government one year in – bouquets and brickbats

Our three-party coalition Government has talked a good game of transforming the New Zealand economy into something more vibrant, competitive and growing that lifts living standards for all. Over the past 12 months that they have been in power they have moved quickly and decisively on a number of fronts to achieve those stated objectives. Therefore, it is timely to take stock on what has been done and what still needs to be done: -

“Bouquets”

- Reducing red tape and speeding up processes in the construction industry.

- Cutting wasteful Government expenditure (fiscal deficits require this action).

- Contributed to lower inflation that allows lower interest rates earlier (albeit NZ got lucky with plummeting tradable inflation imported from offshore).

- Reversed the previous Labour Government’s restricting employment laws.

- Delivered income tax cuts to middle New Zealanders.

- Reduced crime and addressing problems in education and health.

- Excellent work by Trade Minister Todd McClay to reinvigorate overseas export market opportunities.

“Brickbats”

- Lots of talk and reorganisation to fast-track large infrastructure projects partnering with the private sector construction and financiers. However, little in the way of new Public-Private Partnership (‘PPP”) projects actually being announced and commenced.

- No policy initiatives to attract new foreign investment into New Zealand. Again, lots of chat on how we are welcoming the inwards investment, but where are the proactive policy incentives? New Zealand needs to aggressively promote and market itself to the world, it is not clear that this is happening.

- The tertiary education sector is missing the opportunity to bring back foreign students as Australia limits their numbers. The body that sells international education, Education New Zealand, still has a Board of domestic folk and not one international marketer!

- No initiatives to reduce the inefficiencies and burgeoning overheads of a bloated local government sector. Perhaps next year’s local government elections will change attitudes and direction.

- No real action to improve domestic competition in banking, air-travel, insurance, electricity and supermarkets.

- No price freezes implemented on Government department charges/fees to the public.

The good news for the Luxon-led Government is that booming export commodity prices will lift spending and investment in the economy next year and return New Zealand to a positive growth path.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

2 Comments

- Contributed to lower inflation that allows lower interest rates earlier (albeit NZ got lucky with plummeting tradable inflation imported from offshore).

It is 100% the latter. The government is still running at bigger than planned deficits. The midyear treasury update will confirm that. Also they allowed the commerce commision to approve a 43% increase of line charges by Transpower and the regional lines companies for the next 5 year. In my opinion there is absolute no contribution to a lower inflation from the current government!

What Roger Kerr states about the direction of the NZ/US dollar exchange rate is contrary to what is being said by some overseas economists, but he could well be correct! His views are always based on very comprehensive data that are often overlooked.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.