Summary of key points: -

- Question 1: Will the “Trump Trade” unwind and how quickly will that happen?

- Question 2: The US turns inwards, what does it mean for the global economy?

- Question 3: Will the US Federal Reserve still cut interest rates to 3.50%?

The stunning victory by Donald Trump and the US Republican Party at last week’s election has already stimulated financial and investment market reaction, however there are a raft of unanswered questions remaining on how the change of political power in the US will impact the US economy, the global economy, US interest rates, currency markets and therefore, in turn, the New Zealand dollar exchange rate.

Question 1: Will the “Trump Trade” unwind and how quickly will that happen?

The currency and bond markets decided a month ago that there was a greater probability that Donald Trump would make a spectacular political comeback and return to power. Maybe these markets were just “following the money” on the betting platforms that favoured a Trump win. The bond market sold off (yields increased) as they factored in a greater supply of US Government Treasury Bonds being issued under a Trump regime, as his economic policies of tax rate cuts would lead to larger budget deficits that need to be debt funded. The US dollar followed the increase in bond yields, however the “Trump Trade” buying of the USD was also fuelled by the widely held view that Trump’s import tariff increases would lead to retaliatory measures by trading partners and a global trade war. The US dollar has always appreciated in the past on safe haven inflows on the uncertainty of disruptions and restrictions to free-flowing world trade.

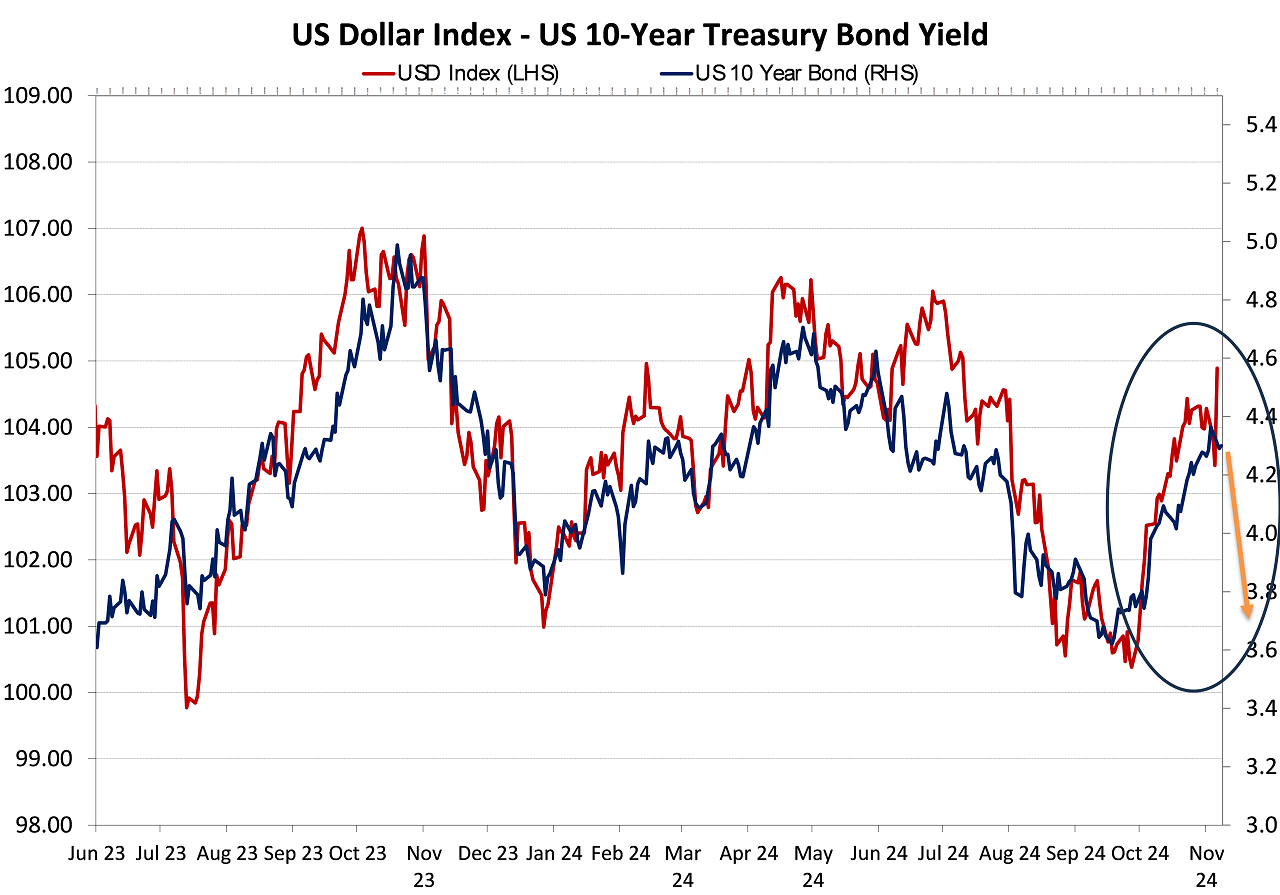

Since the election result was known five days ago, the US dollar has posted further marginal gains from the 104.00 area on the Dixy Index prior to the election day to the current level of 104.89. The Euro with a 58% weighting in the Dixy Index has suffered the most, deprecating from $1.0900 to $1.0700 against the USD over the last five days. The NZD/USD exchange rate was trading between 0.5950 and 0.6000 prior to election day and currently sits within that range at 0.5970 – so very little change. The Australian dollar, Japanese Yen and British Pound have all moved in a similar fashion to the NZ dollar, trading today against the USD at similar levels to just prior to the election.

US 10-year Treasury Bond yields were trading at 4.30% prior to the election, increased to a high of 4.48% on 7th November; however, have since drifted lower to return to a current 4.30% level.

The currency and bond market pricing action (except for the weaker Euro) tells us that the markets had fully priced in a Trump win beforehand (as this column projected last week) and no further buying of the USD or selling of US bonds has occurred since the event risk has become a known fact.

What is known with some certainty, is that the speculators who sold US bonds and bought the USD a month ago are now sitting on sizeable unrealised revaluation gains on their positions. Whilst the currency and bond market strategists, economists and fund managers all attempt to figure out what the numerous Trump policy changes mean for the US economy and therefore ultimately for US interest rates and the exchange rate, the market speculators will be pondering whether to “take their profits” or to sit as they are - long the USD and short US bonds.

The decision by the speculators for the former would seem far more likely given the short time period ahead until their 31 December financial year end. There is also something of a vacuum or hiatus period over the next two months until actual policy changes can be officially announced by the new President after his inauguration on 20th January 2025. The greater probability is that we see a wholesale unwinding of the October buying of the USD and the selling of bonds, as the speculators realise their trading profits into cash. At the end of the day, the projected size of the US Government budget deficit over coming years is the same today as it was in September and October.

The US Federal Reserve remain on their current path of another 0.25% cut to interest rates in December and four further 0.25% cuts in 2025, taking their Fed Funds rate to a terminal and neutral rate of 3.50%. With low US inflation over coming months and lower short-term interest rates it is difficult to see longer-dated bonds rising in yield. In other words, the bond speculator’s unrealised profits are not going to increase any further and could easily be eroded. Why would they not act now to unwind their positions?

Given all the above, the conclusion is that we will see a return of 10-year US Treasury bond yields to the 3.75% region over coming weeks as the bond speculators take their profits by buying bonds (forcing the yields lower). The USD Dixy Index religiously follows the bond yields, so the currency Trump Trade also unwinds before the end of the year. A USD Dixy Index back at 101.00, would see the NZD/USD exchange rate back at 0.6350.

Question 2: The US turns inwards, what does it mean for the global economy?

Well, it is hardly positive for global growth, however it remains to be seen to what degree the more extreme Trump economic policies are actually implemented. Lower tax rates for business is always positive for investment and growth, as was seen in Donald Trump’s first term of 2016 to 2020. The tax cuts require Congressional approval, and the Republicans do not as yet have confirmation that they also control the House of Representatives. Removing inhibiting regulations was very positive for the oil and gas industry in Trump’s first term. It is doubtful whether we will see that same growth burst this time as green energy programmes of the Biden Administration are canned.

The President alone can approve the tariff increases; however, they could be challenged in the legal courts and take longer to implement. Trump intends to bring in a blanket tariff of 20% on all goods imported into the US and a tariff of up to 60% for Chinese imported product. One ramification of the China tariff is that China could swamp other economies with product they divert from the US, resulting in lower inflation outside of the US. As was seen in Trump’s first term, import tariffs do not work to bring manufacturing jobs back to the US. US manufacturing companies import component parts from all over the world, they become uncompetitive on price if they are paying more for their inputs. US agricultural exporters will be worse off as China and the Europeans impose retaliatory tariffs on imported food from the US. It could be that Trump sees the threat of tariffs as his greatest leverage for concessions for US exports, negating the need to actually enforce higher tariffs.

US households are worse off as well, as tariffs on imported goods increases inflation and reduces spending.

US trade protectionism is bad news for European economic growth. The sell-off in the Euro since the election may be an early testimony to this expectation. Uncertainty over Trump’s stance in Ukraine and the Middle East also adds to the risk of greater instability in both regions, which would take a toll on European and global economic growth.

Last month, the IMF published a report that a major global trade war would hit the world economy by 7%, the size of the French and German economic combined. Let us hope that there are wiser heads to prevent this happening, however Trump thinks other countries have shafted the US economy in the past and he is out for retribution!

The Trump election victory is also bad news for the Asian economies. Arguably, China is better prepared than they were for Trump’s tariffs/trade war in 2016. China could well accelerate their economic stimulus measures to support domestic consumer confidence as a counterweight to the negative tariff impacts on their manufactured exports. Trump will have “China hawks” in his team, so the US/China relationship is in for a stormy few years. Adding to the complexity is that the Trump regime would be stupid to forget who funds their budget deficits, i.e. Chinese, Japanese and European investors!

How the fledgling recovery in the New Zealand economy is impacted by the policy changes in the US remains to be seen. There are two distinct negative forces for the Kiwi dollar in the period ahead: -

- Import tariffs and deportation of undocumented immigrant labour in the US increases prices for consumer goods and food. Higher than expected US inflation in 2025 causes the Fed to go slow on interest rate cuts. On the other side, interest rates are cut at a faster clip in New Zealand as inflation falls further on lower prices from Chinese imports.

- Global trade wars is always a negative for a trading nation like New Zealand and therefore the NZ dollar. Lower global growth is also a negative. We need to lobby the Trump administration that imposing tariffs on imported food is a dumb move and will make life tougher for US households. Whether we can get exceptions on the US tariffs remains to be seen.

Sovereign wealth managers and large family-office type investors in Asia may well be reluctant to allocate capital into a US economy that is about to turn its back on the world. In a roundabout sort of way that may mean more offshore investment flows coming into New Zealand as those Asian investors seek alternative destinations to the US.

Questions 3: Will the US Federal Reserve still cut interest rates to 3.50%?

If he could make it happen, President-elect Trump would like to instruct the Fed to cut interest rates to 2.00%! If Trump had his way the weaker US dollar from lower interest rates would also assist US exporters and reduce imports – two responses he would like to see.

However, as Fed Chair Jerome Powell reminded the world in his media conference last Thursday, it is not that simple. The Federal Reserve is strictly independent by law from any interference from the President. The question for the Fed into 2025 will be whether any further loosening in fiscal policy by the Trump regime requires them to hold monetary policy tighter than it would otherwise be?

The negative impact on US inflation from the tariff increases may be further away and more muted than what most currently expect. Consumer goods imports into the US have already ramped up before the election and will continue at higher levels over the next few months before the higher tariffs come in. Imported consumer goods into the US such as clothing, electronic equipment and communication devices have very low weightings in the US CPI Inflation Index. Housing, energy, transportation, medical and food, all domestic price components dominate the index. The 12 to 24-month delayed impact of lower rents and implied rents will continue to drive the US CPI lower over coming months.

There has been some speculation that massive deportation of undocumented immigrant workers in the US will mean the crops are not picked and food prices spiral higher on short supplies. The impact is severely exaggerated, as logistically it is difficult to expel one million illegal workers from the US in a year, let alone 10 million as Trump believes he will deport.

The greater probability is that the Fed remains on their current path with interest rate cuts as the threats of higher US inflation in 2025 does not transpire into reality. At some point not too far away, bond investors in the US are going to be forced to conclude that 2.00% real rates of return (bond market yields of 4.30% less annual inflation of 2.20%) is just too good to miss out on.

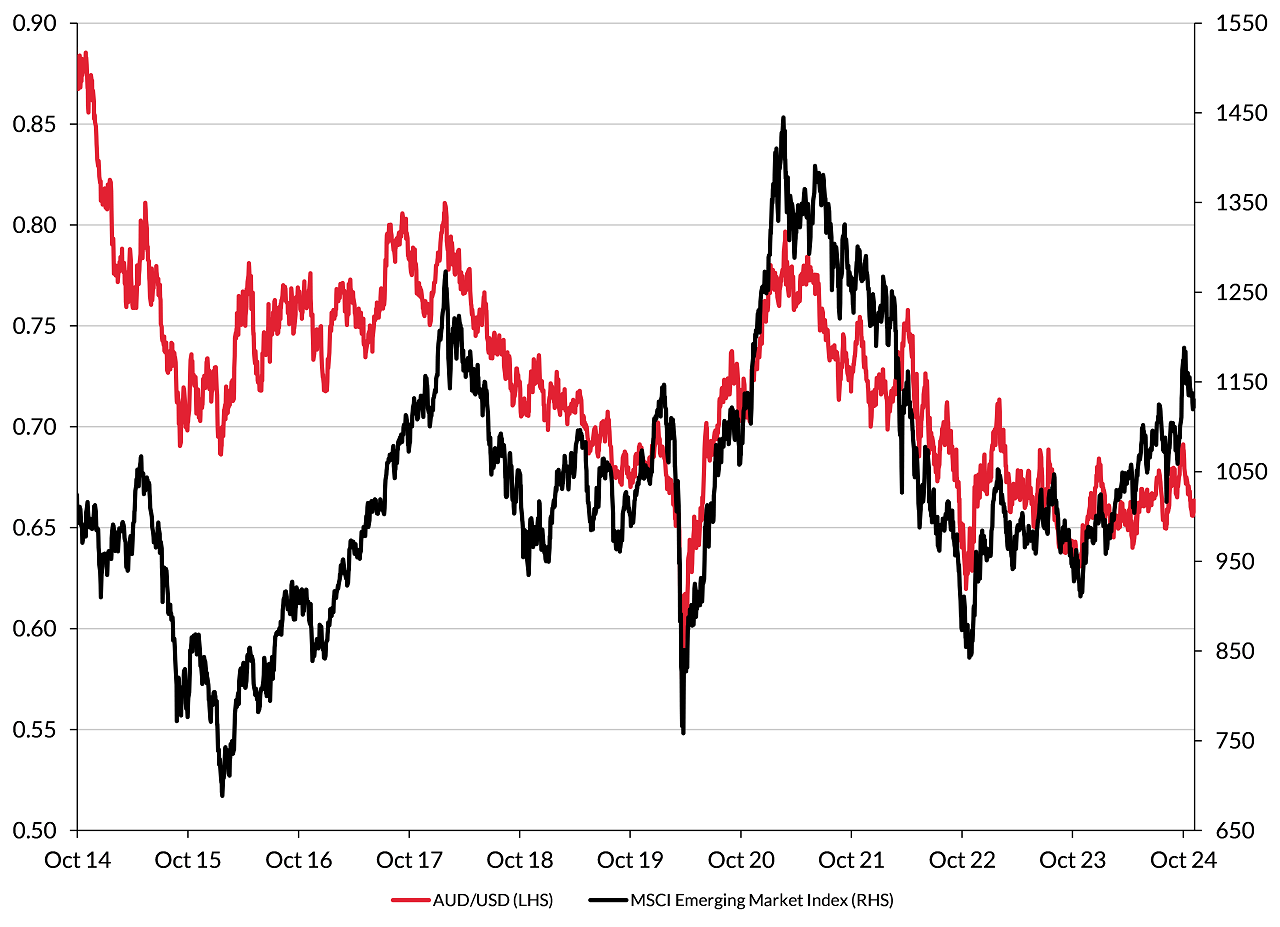

Lower US short-term interest rates is very good news for emerging market economies (China, Taiwan, India, South Korea, Brazil, South Africa, Indonesia etc.). Global investment funds are more likely to allocate increased investment assets to emerging market equity markets over the next 12 months. The AUD/USD exchange rate closely follows the MSCI Emerging Markets Index and already has some catching up to do.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.