Summary of key points: -

- US dollar buying on a Trump victory has already happened

- Japanese political turmoil confuses interest rate and Yen currency outlook

US dollar buying on a Trump victory has already happened

The foreign exchange markets have already delivered their verdict on the outcome of the US Presidential Election on Tuesday 5th November. A good part of the US dollar buying over recent weeks appears to be speculative market participants positioning themselves in advance for a Donald Trump victory. The recent Trump improvement in the political opinion polls in the key seven swing/battleground states (for the electoral college votes) would have encouraged some of the US dollar buying.

The currency markets foresee a stronger US dollar value (initially anyway!) under a Trump Presidency for three reasons: -

- Lower tax rates being positive for economic growth (there is much economic debate as whether that would be the case).

- Increased tariffs on imported product into the US increases inflation and that will make it more difficult for the Fed to reduce interest rates over the next 12 months compared to their current plan i.e. USD positive.

- The draconian tariff increases will stimulate retaliatory tariffs and restrictions/sanctions from trading partners. The resultant trade-wars would lead to elevated economic uncertainty around the globe, an environment that has always produced a stronger US dollar in the past on safe-haven flows.

In placing their bets down early on a Trump victory, the FX markets also seem to be placing a lot of store on the predictive accuracy of the various betting sites that have opened books for the US Presidential Election outcome. It is no coincidence that the US dollar Dixy Index has appreciated 3.50% over this last month alongside the increase in the probability of Trump winning the election (from the betting websites). The US economic data released over the last month has also been more positive (jobs, retails sales and ISM services) and that in turn has pulled back the speed and extent of market pricing of interest rate cuts over coming months.

The two big determining factors as to whether the US dollar can continue to appreciate on its current upward trajectory over coming months, or alternatively, pull back down again and complete another up/down price action in the 100.00 and 106.00 trading range it has been in for the last 12 months, are as follows: -

- The outcome for the Presidential Election. A Harris victory or a “no-result on the night” would see immediate USD selling in the forex markets as all the long-USD bets for a Trump victory are unwound. A Trump victory may not see additional USD buying, instead the USD could also be sold under this scenario as all the USD buying has already taken place before the election date i.e. a classic “buy the rumour, sell the fact” situation.

- Upcoming US economic data releases this week (before the election) for September PCE inflation and October Non-Farm Payrolls employment statistics. Softer than expected outcomes for both (and subsequent revisions downwards in the jumbo +254,000 increase in jobs in September) would reverse the US dollar’s direction. US dollar selling related to these two economic data releases may prompt wider profit-taking by long-USD position holders ahead of the election result Tuesday week.

We are in for a turbulent two-week period in global financial and investment markets with the potential for market reactions to the aforementioned events to be quite different to expectations.

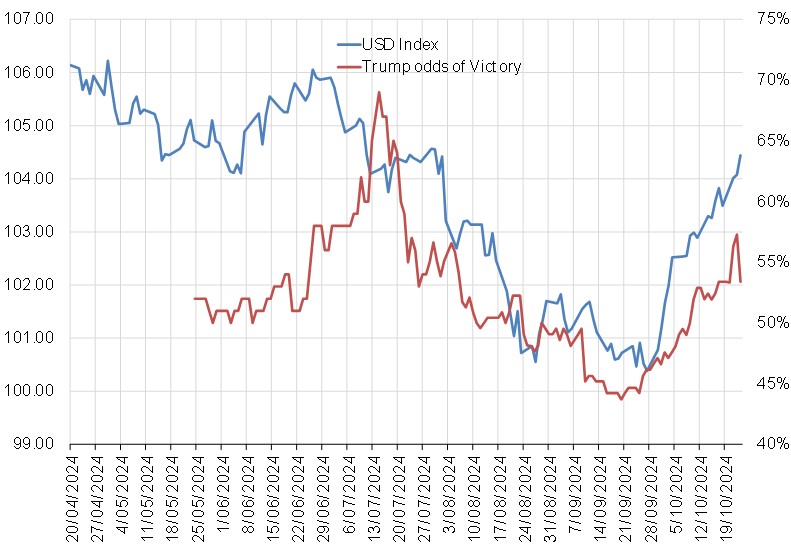

The chart below plots the USD Dixy Index (blue line) against the “Trump odds of victory” (red line) based on the weight of money placed on betting sites for the election. The political opinion polls suggest that the outcome is too close to call, however the FX markets are firmly backing a Trump victory – they may be disappointed!

Local NZD/USD foreign exchange risk managers should already be well-positioned for a stronger US dollar (lower NZD/USD rate) at this time, as the possibility of a Trump victory was one of those global geo-political risk events earlier foreshadowed in this column as a factor that would drop the Kiwi dollar back to 0.6000. USD importers were advised to have 100% hedging in place over the three-to-four-month period until 31 December 2024 to protect profits against the risk. As it has turned out, the risk event (stronger USD, lower Kiwi) has occurred before the actual election outcome is known.

Local USD exporters who are already heavily hedged have another opportunity to add to hedging percentages to bring down weighted-average hedged rates. Outside of economic and political developments in the US of A over the next 12 months, there are still foreign exchange forces related to the Yuan, Yen and Aussie dollar that will influence the NZD/USD exchange rate. The greater probability remains that all three of those currencies will appreciate on economic performance and interest rate differential reasons over the coming period.

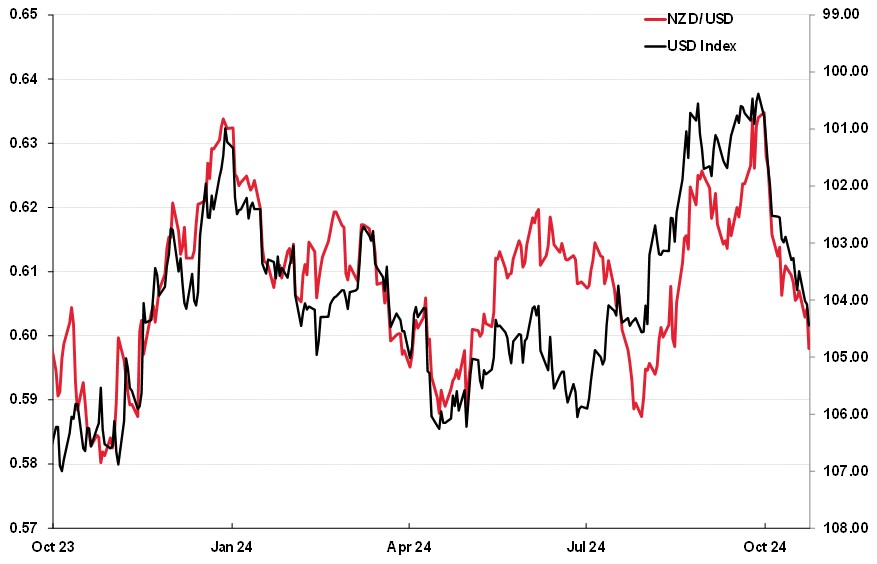

Over the last 12 months the US dollar has appreciated to the 105.00/106.00 region on three previous occasions and reversed back downwards each time (black line on the chart below, USD Dixy Index inverted on the right-hand axis). We are approaching the higher levels again, however, there has to be real questions on the conviction levels of the USD bulls to continue to buy the USD near to the top end of the established trading range.

The US Federal Reserve will not be that happy with the recent tightening of monetary conditions in the US economy (market two to 10-year bond yields up 0.50% over the last month), precisely at a time when they have just cut their Fed Funds rate by 0.50%. They might dismiss the higher market interest rates as volatility that you would expect ahead of a Presidential Election, however the higher market interest rates do make life tougher for US households (auto loans) and wipes out any benefit from the Fed’s commencement of a looser monetary policy cycle.

Nothing has changed with the US inflation picture, with the PCE numbers for September this Thursday night confirming a 2.10% annual headline rate of inflation. It seems the bond and FX markets need a reminder that one month’s Non-Farm Payrolls jobs increases (which is most likely wildly overstated) does not change the fact that US inflation has reached the Fed’s target of 2.00%, therefore interest rates can be returned to “neutral” (2.50% to 3.00%) as quickly as possible.

Japanese political turmoil confuses interest rate and Yen currency outlook

Japan is going to the polls at a General Election today (Sunday 27 October). The snap General Election was called by the new Prime Minister, Shigeru Ishiba in an attempt to secure a new mandate for the ruling LDP Party and him personally as the LDP leader and PM. It has all the hallmarks of backfiring and causing more political turmoil. All the political uncertainty is causing a lot of confusion at the Bank of Japan as they attempt to normalise monetary policy (i.e. increase interest rates to well above 0.00%) and control inflation. The new PM, Ishiba was expected to endorse interest rate increases when he came into power four weeks ago, however he did the opposite and instructed the officials to find other ways of containing inflation! That flip-flop caused the Japanese Yen to weaken from 140 to 152 against the USD over the last month. The NZD/USD rate is back below 0.6000 largely because the of the Yen’s abrupt depreciation.

There is a good chance that Shigeru Ishiba might become the shortest-serving Prime Minister in Japanese post-war history as he will struggle to find political partners to form a new Government.

If the Yen weakens any further on this political vacuum and uncertainty, the Bank of Japan are likely to intervene directly in the FX markets by buying Yen (as they have done so previously). The FX strategists at the Bank of Japan may well take the opportunity of some USD profit-taking (i.e. USD selling) ahead of the 5th of November US Presidential Election to move into the FX markets, buying Yen and selling the USD as they will have a greater chance of success in that environment of turning the Yen’s direction around.

Whatever the political outcomes in Japan, the Bank of Japan still has to increase their 0.25% interest rates to combat inflation (which is made worse by a weaker Yen exchange rate). The Bank of Japan next meets on Thursday 31 October, however any interest rate increase will have to wait until next month’s meeting.

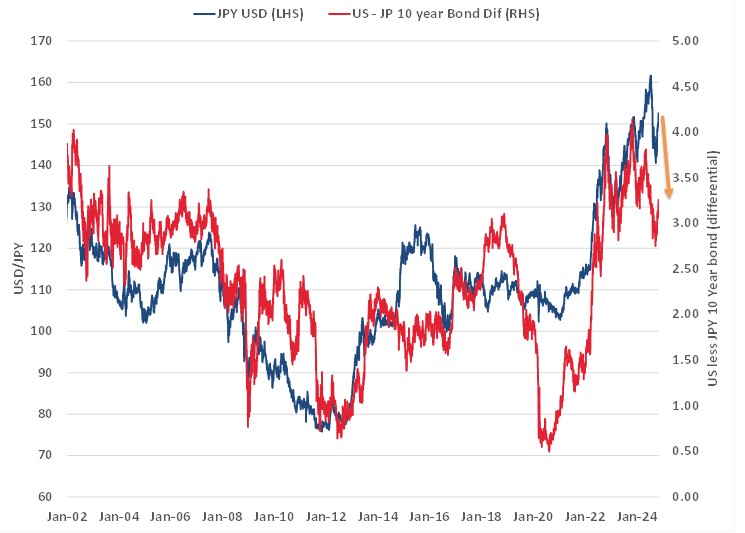

No matter what changes may occur with US and Japanese political leadership over coming days, the prospect of Japanese investment houses returning their funds to home base after a decade of investing outside of Japan for enhanced yield returns, is very real. Japanese 30-year Government Bond yields have increased to 2.20%. Why would they invest in US bonds in the 3.00% region?

The chart below of the interest rate gap between US and Japanese 10-year bond yields has proved to be a reasonably accurate predictor of USD/JPY exchange rate movements over the last 20 years. It still points to a much stronger Yen, despite the recent spike up in US 10-year Treasury Bond yields to 4.20%.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

8 Comments

Almost all the U.S. polls over sample with Democrat voters. The Wall Street Journal is one of the few that makes a more balanced assessment, and those polls consistently show Trump ahead. That said, there is evidence already that Democrat states are manipulating the voting process, and that could influence the outcome.

I was intrigued by the media and commentator reports of DJT having some sort of neurological event and subjecting a bemused audience to his mixtape for 40 minutes. I found the townhall on youtube and the reality was not like that at all. It's hardly news that the media is biased but the bad faith reporting was quite shocking. I am sure Trump is going to win convincingly.

Trump is old and weird. Jigging around to YMCA dates him plus. He is a convicted felon awaiting sentencing for fraud. And right now he is with the courtesy of Dolan doing a repeat of the 1939 rally at the same venue and they say history never repeats itself.

In respect to the US we are watching it lose out to China as the world power. It will happen it just will be messy.

I'm not saying he's not old or weird or vile or impressively ignorant. But he is very astute when it comes to reading people, crowds, and national moods. And at this town hall the audience was fawning over him. It actually reminded me of a Morrissey concert.

@ Elmoboy - You reckon the Democrats would be silly enough to risk Manipulating the voting process for a 2nd time in a row? Or you reckon this time around people will be watching for a crafty slide of hand trick?

Fascinating take.

It was said the Japanese election was the most boring election. All these predictions on and by some on the Republican win ignoring the yen $ trade.

Instead we see the ruling coalition has lost its majority. The fallout could be more interesting than what the Americans do.

I believe there are enough 'smart' people within the Trump environment who will realize that his policies will be inflationary. Trump will either manipulate Powell or replace him to lower the rates at the short end of the curve. Trump will decree pensionfunds, 401 k providers, insurers, private equity to buy longer term treasuries to bring the long end of the curve down.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.