Summary of key points: -

- Impossible to predict the unpredictable RBNZ

- Euro and Japanese Yen movements do not suggest a lower Kiwi dollar

- Who to blame for the electricity price crisis

- Kiwi dollar undervalued on the “Big Mac” currency index

Impossible to predict the unpredictable RBNZ

The NZD/USD exchange rate has returned to 0.6000 after another short-term dip to below 0.5900. Whether the Kiwi dollar can continue to make gains higher against a weaker US dollar in global FX markets over coming weeks and months will largely hinge on what the Reserve Bank of New Zealand (“RBNZ”) say and do this Wednesday 14th August. Over the last 12 months the RBNZ have proven to be as inconsistent and unpredictable as a struggling All Blacks rugby team this season under a new coach.

If the RBNZ deliver a monetary policy statement this week in line with what they messaged back on 22 May, the Kiwi dollar will respond by moving higher, as interest rates will need to stay higher for longer to bring down the stubborn/sticky non-tradable inflation that the RBNZ highlighted as problematic. Should the RBNZ adopt the tone of the 10 July OCR review statement, wherein they completely ignored their May inflation worries, the Kiwi dollar is likely to depreciate as the RBNZ would be signalling much earlier reductions in inflation and interest rates.

The likely outcome is that RBNZ Governor Adrian Orr will keep the markets guessing for a while longer and deliver a statement not consistent with either of their messages in May or July. It would be a major surprise if Adrian fully endorsed the current interest rate market pricing of eight x 0.25% =2.00% of cuts over the next nine months. To endorse that market pricing, the RBNZ would have to forecast tradable inflation plummeting further to -2.00% to offset the +4.00% permeant non-tradable inflation track. Such a further dramatic reduction in tradable inflation is improbable. Oil prices have reduced; however, the NZ dollar currency value has weakened overall which pushes tradable inflation higher, not lower.

On the other side, Governor Orr will not totally renounce the aggressive interest rate market pricing. He is more likely to indicate that inflation is progressively moving lower in line with their forecasts, however a too rapid reduction in interest rates runs the risk of igniting inflation again (particularly in the NZD/USD exchange rates depreciates in response).

It is recognised that the economy has continued to weaken through June and July, however that does not automatically transfer through to lower inflation. As we have demonstrated previously, the high 5.40% domestic/non-tradable inflation is immune and impervious to GDP and interest rate levels. The non-competitive parts of the economy and public sector continue to increase their prices and the RBNZ can do nothing about that. Therefore, they need to drive tradable inflation to well below zero to lower the overall inflation rate to the 2.00% target. The economy needs a higher NZD/USD exchange rate to achieve that, so it would be totally irresponsible to deliver a statement next Wednesday that sends the NZ dollar lower!

It would be refreshing indeed if Governor Orr was as clear-cut and straight forward as the Reserve Bank of Australia (“RBA”) Governor, Michele Bullock in respect to messaging to the market and the wider economy. Last week, the RBA Governor was upfront and honest with unambiguous messages of: -

- Inflation will take longer to decrease to our 2.50% target than previously forecast.

- The interest rate markets have gotten ahead of themselves with pricing-in interest rate cuts this year.

- The RBA will not be cutting interest rates before February 2025.

The RBA delivered a “hawkish hold”, the RBNZ are likely to deliver a “dovish hold” this Wednesday. However, the two countries’ inflation rates (both with high domestic/non-tradable inflation levels) are very similar. The RBA are not that confident of their inflation rate reducing over coming months. The RBNZ should not have confidence about our inflation rate reducing dramatically either with electricity prices soaring and local government rates ramped higher as well.

Whether the RBNZ wait for the September quarter’s CPI inflation data in mid-October and therefore make the first cut at their 27 November meeting or they cut at the earlier 9 October meeting remains to be seen. Either way, the cuts to New Zealand interest rates will come after the US Federal Reserve’s first cut on 18 September. The US do not have a 5.40% domestic inflation problem that New Zealand has, therefore over the next six to nine months the Fed will be reducing their interest rates at a more rapid pace than we will be.

Outside of the risk of Adrian completely ignoring the domestic inflation problem, the conclusion is that the NZD/USD exchange rate will move upwards on a more favourable interest rate differential for the NZD against the USD.

A surprise 0.25% cut this Wednesday would totally destroy any credibility the RBNZ have remaining, as it would mean cutting interest rates 12 months earlier than what they stated on 22 May (less than three months ago). The future track of inflation just does not change that much in the space of three months.

Euro and Japanese Yen movements do not suggest a lower Kiwi dollar

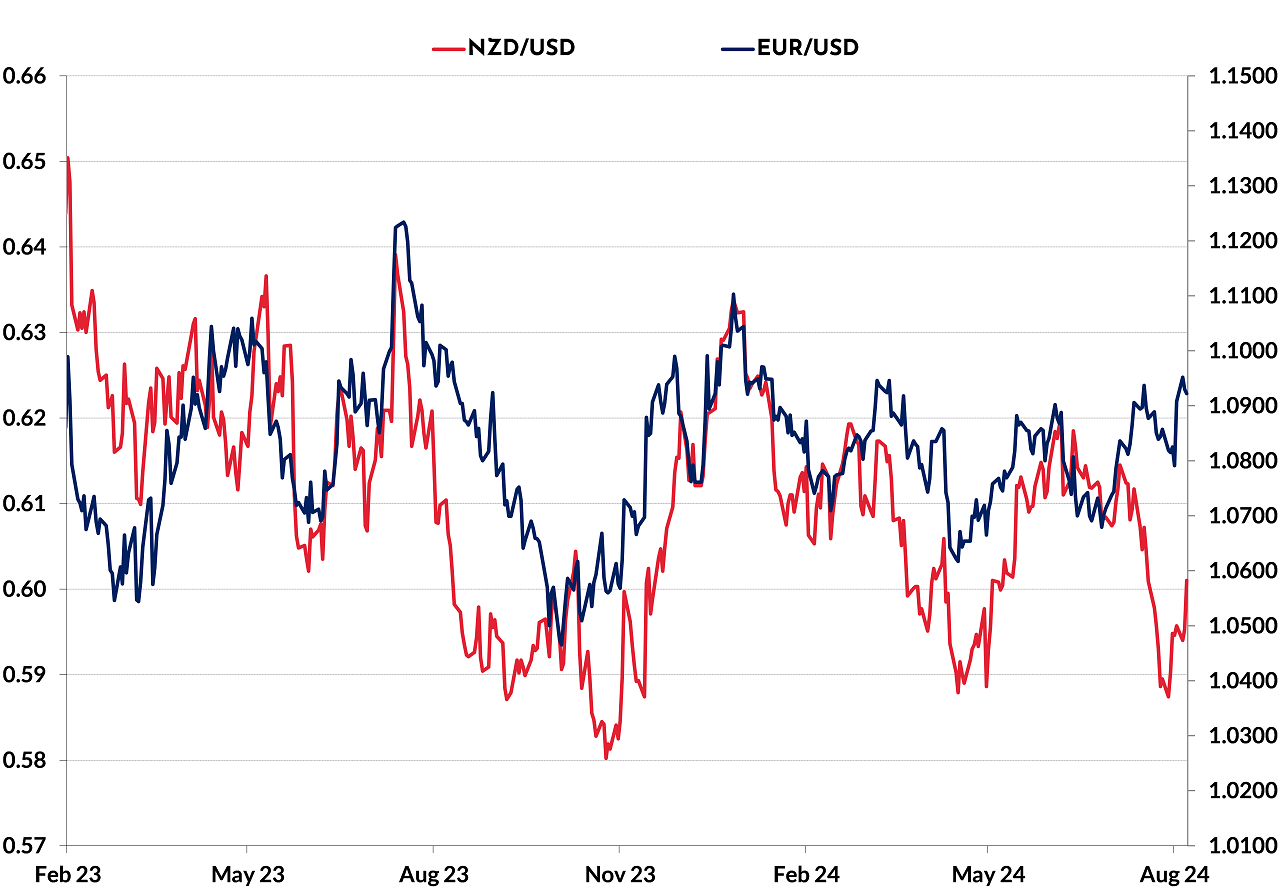

History tells us that the NZD/USD exchange rate is tightly correlated to EUR/USD movements, as what the US dollar does against all currencies remains the dominant determinant of NZD/USD direction. The chart below confirms that close correlation, however over recent weeks we have witnessed a significant divergence of the two rates. The NZ dollar was forced lower on the unwinding of Japanese Yen carry trades, independent and unrelated to a stable EUR/USD rate over that period. History also tells us that such divergence does not last for long. The NZD/USD exchange rate at the current 0.6000 level is arguably two cents undervalued and should be nearer 0.6200 based on the current EUR/USD level of $1.0920.

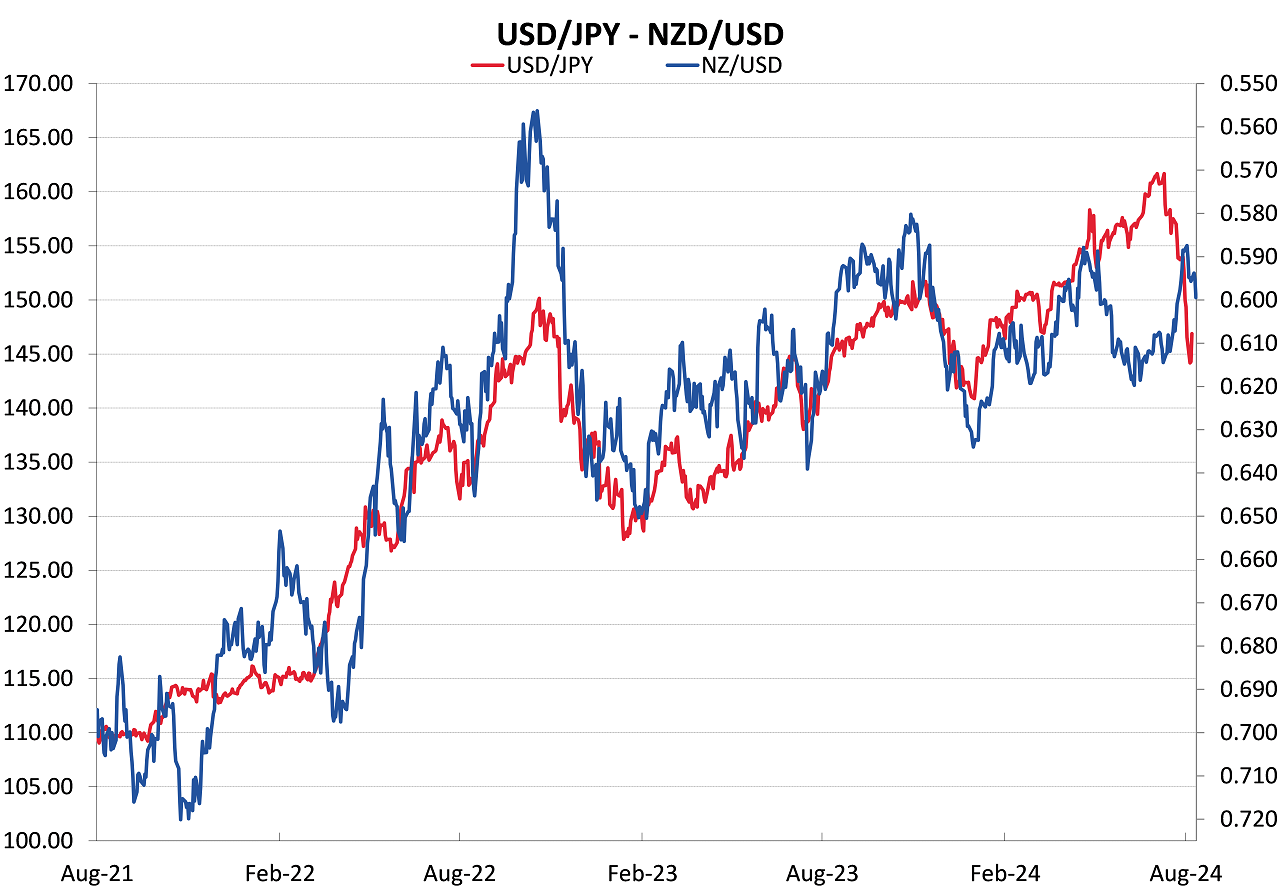

In our FX market report two weeks ago, we highlighted the connections between the Japanese Yen/USD exchange rate and other Asian currencies (including the NZD and AUD). The chart below depicts the Japanese Yen’s depreciation over the last three years against the USD (red line, left hand axis), the Yen weakening from 110 to 162 (now 145). The Kiwi dollar has not depreciated as much as the Yen in percentage terms; however, the directional relationship is close. The NZD/USD rate (blue line, inverted right hand axis) had weakened over recent weeks when the Yen strengthened on the unwinding of the carry-trades. However, over the medium term, the Kiwi does follow the Yen’s direction against the US dollar. It is estimated that the Yen carry-trades are now 75% unwound, so the intensity of Yen buying has somewhat abated.

Looking ahead, significantly lower US interest rates and higher Japanese interest rates suggests that the USD/JPY exchange rate still has a long way to go in its re-alignment i.e. continuing Yen strength to 130 (equivalent to 0.6500 NZD/USD) and 120 (equivalent to 0.6700 NZD/USD).

Who to blame for the electricity price crisis

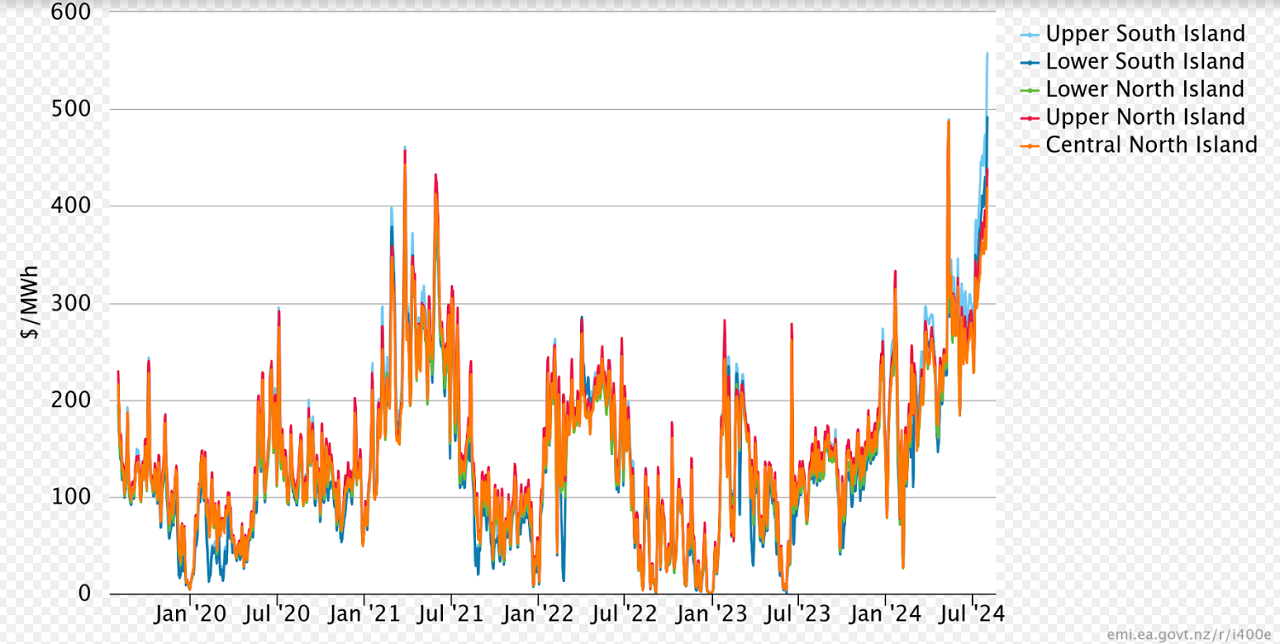

In typical Kiwi fashion, we like to point the finger and find someone to blame for things going wrong. The current electricity price crisis is a case in point. The “perfect storm” of a combination of factors of low hydro lake levels, low winds and higher winter demand has spiralled spot electricity prices higher. We cannot entirely blame climatic conditions, so we search for other scapegoats. The previous Ardern Labour Government has part culpability here as they stopped all new oil and gas exploration at a time when the existing offshore Taranaki gas fields were running out a lot faster than all forecasts. We now have a shortage of gas and are burning expensive imported Indonesian coal at the Huntly peaking generation plant. The Ardern Government also planned to build the massive Lake Onslow pumped hydro generation capacity, which stopped all other electricity generators from planning any new capacity. We fail help ourselves in this country!

Several pulp manufacturing facilities around the North Island are now threatening closure due to unaffordable electricity prices, they are all blaming the listed power generation companies for price gauging and profiteering. Pressure is mounting on the National Coalition Government to step in and intervene on electricity prices. The large industrial users are citing a failure of the electricity market and that someone should provide a subsidy to them so that they stay in business.

An examination of electricity spot market prices over recent years would suggest that the industrial users have had plenty of opportunity to buy forward fixed-price electricity contracts to hedge themselves against market price spikes, such as we are experiencing now. If they have not hedged their price risk under formalised risk management policies of minimum and maximum hedging limits over specified forward time periods, then they only have themselves to blame. Clearly, the overseas-owned pulp manufacturers have been playing the roulette wheel in the spot electricity market without prudent forward hedging protection. Managing electricity price risk is no different to hedging FX, interest rate and commodity price risk.

It is alarming that such large and sophisticated companies running pulp manufacturing plants in New Zealand adopt such high-risk business practices with one of their biggest operating costs.

NZ electricity spot prices (2020 to 204)

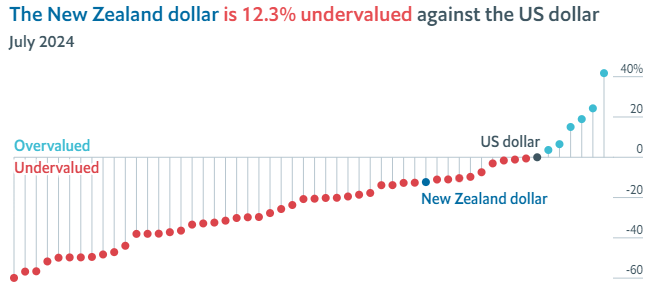

Kiwi dollar undervalued on the “Big Mac” currency index

It is not the perfect method to measure one currency value against another, however there are not many products that are essentially exactly the same in all counties of the world. The Economist magazines “Big Mac Index” has been published for many years now, the latest measure has the Kiwi dollar 12.30% undervalued against the US dollar. A Big Mac costs NZD8.40 in New Zealand and USD5.69 in the US, an implied exchange rate of 0.6750. The Swiss Franc is 42% overvalued.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

42 Comments

The Ardern/Hipkins government did NZ no favours by banning new gas and oil exploration. While the current government changed the rules, it is very unlikely that overseas investors will return to a market they perceive as politically unreliable. NZ will have to import more gas and oil.

This goes for much activity in NZ.

If the political setup trends towards sweeping changes/new costs every 6-9 years, you're not going to be as enthused about long term investment.

Or we could build a big battery to store energy when we have surpluses from low-carbon sources available? Or maybe even a few of them?

Wait? Wasn't the last government looking into that?

(Man alive I am sick of people re-gurging the gentailer's Kool Aid.)

OK Elmboy, let's say we allow exploration and find a bit of gas. We use it all up. And then what?

When you have a patient that is killing themselves by drinking too much do you try help them access alcohol more easily and more cheaply?

"A surprise 0.25% cut this Wednesday would totally destroy any credibility the RBNZ have remaining, as it would mean cutting interest rates 12 months earlier than what they stated on 22 May"

I'm reminded of someone here who recently posted a 0.25% cut this coming Wednesday was a guarantee in order to rescue the housing market they had earlier implied was already poised to take off on the back of recent bank initiated reductions.

Honestly, if some readers are confused by Spruiker mentality - I wouldn't blame them.

Easier to predict based on the person than what the decision should be. The decision should be to cut rates, that's pretty obvious its only the RBNZ standing in the way. If they don't officially cut rates, banks are doing it anyway so more cuts coming before September. The real question is why are we paying these people so much money when they are not really in control of anything ?

The real question is why are we paying these people so much money when they are not really in control of anything ?

https://www.treasury.govt.nz/information-and-services/commercial-portfo…

Enjoy.

Why would I need to read that ? Open your eyes to what is actually happening. We sold all the banks to the Australians mate and then I see they are even looking at selling Kiwibank. That pretty much summarises why we are where we are in two lines.

Why would I need to read that?

Because it's evident you've never read it before. Despite what you might think, the RBNZ serves it's purpose and as this article implies, has to be seen as credible. Sure the RBNZ might chose to cut rates this coming Wednesday however, to imply it's a 100% sure bet is certainly pushing it. edit

- to act as the central bank for New Zealand, including by:

- formulating (through the Monetary Policy Committee) and implementing monetary policy

- managing foreign reserves and dealing in foreign exchange

- issuing and managing bank notes and coins

- monitoring the needs of the public for banknotes and coins

- providing liquidity facilities to manage liquidity in the financial system and to protect or promote financial system stability

- providing settlement accounts

- operating or participating in payments and settlements systems

- liaising and cooperating with other central banks and relevant international institutions

- providing or facilitating the provision of information to the public that is relevant to the Bank’s objectives

The primary function of the RBNZ is evident ....the viability of the NZD as a currency...all else is secondary (or supportive) to that.

@RP

I think Zwifter was saying it's a 100% sure thing that the OCR won't drop on Wednesday, as it is Adrian Orr in charge

Good piece. I agree that credibility and pride could be key factors in not cutting, and they can use the ‘get out of jail card’ that inflation isn’t quite beaten to their satisfaction. A November cut will look less bad in terms of their credibility.

November would be less bad…but marginally less bad…either his jawboning was too aggressive or they completely f**ked up their analysis of everything…regardless, I would be shocked if he cuts before November.

I think it is possible the RB could drop .25 , reason behind this is there has been some improvement and the Fed rate sits 5.25-5.50 . Such a move by the RB would install some confidence that progress is being made. I wouldn't view such a move as being designed to save the housing market at all. Unlikely to see a series of rapid shifts or a return to super low rates rather slow and steady moves in line with what data shows itself . That said, if the data shows the need for upward adjustment this is possible somewhere along the way also. The belief that it will all be downhill on any pivot would be a dangerous assumption to make. My 10 cents

"Iran has decided to attack Israel"

https://www.reuters.com/world/middle-east/israeli-intelligence-believes…

What will the OCR be if tomorrow the whole of the Middle East looks like Gaza does today; oil fields and all?

And that, my friends, is what Adrian Orr is paid to anticipate - the unexpected and the unknown. 5.5% isn't a high level of interest rates in NZ historical terms. +20% is. It's not today's CPI he is worried about - but tomorrows.

Iran wont want Israeli and American forces invading their airspace . Some articles citing they are buying Russian air defense systems . More likely they will continue via proxy . Diplomats are working hard at resolving issues and creating a ceasefire... An attack by Iran would likely not be sustainable given the amount of firepower in the region.

Israeli and US forces won't go into Iran... the consequences would be horrific for either of them. An mid east war is bad for everyone.

Irans leaders may have to do something serious to save face this time...

Interesting times.

They will do a token retaliation wait until things have cooled down a bit and then launch an unexpected massive attack like the one that kicked this off in a few months/years time.

Is 5.5% a high level of interest rate when the debt level is 4 times as large as it was when the interest rate was 20%?

Well said. Knockers of our Reserve Bank Governor need to heeds your comments instead of their own Agenda

Yep, and nah...he acted earlier than many so for that he gets the kudos, but it was to fix his own f**k up so its only a smidge of kudos 😂

I think I read that the RBNZ's current neutral rate is 3.9% and their long term NIR is 2.5% (not sure exactly how current that is?), but look at the last three prints, even while acknowledging that the September quarter will definitely print higher than these three it is still bloody hard to imagine the headline number being over 3%...consider the rather depressed data coming out over the last couple of months, marry that up with the lag effect of any changes...jeez, an OCR 40% higher than neutral seems a wee bit too contractionary doesn't it?

I guess only time will tell if his actions lead to economic ☀️ or 🌧

@imhenry

You need to read the comments of the best commenters on this site, namely Chrisofnofame and Jfoe.

The Economist magazines “Big Mac Index” has been published for many years now, the latest measure has the Kiwi dollar 12.30% undervalued against the US dollar.

Which is similar between NZ and Japan - Big Mac approx 10-12% cheaper in Japan.

But this misses the point about how Japan actually controls prices. A Big Mac meal costs approx JPY807 (NZD9.15) in Japan. In NZ, the price is approx NZD15 (JPY1,320) - approx 40% higher.

Mr Orr and his board of DEI hires have a problem I think largely of their own making

1. Got to have a game plan

2. Stick to the game plan

3. If the facts change - change the game plan but make sure the participants i.e. us, know what the game plan and changes are. Currently its a bit of a mystery. And you dont have to wait until the game is over to change - usually that is to late

and all is dependent upon having the right skill set on board which can be difficult when big ego's are involved

It is estimated that the Yen carry-trades are now 75% unwound, so the intensity of Yen buying has somewhat abated.

According to JPM. We don't know if that claim is propaganda and what the reality is. Good chance that JPM doesn't know either.

Just because JPM says something, doesn't mean it is true.

One word to sum up Adrian Orr is “unpredictable”. Not what you want in a reserve bank Governor. Makes me reminisce about the days when the person in charge was nice and boring.

Much of Orr's unpredictability is a direct result of his incompetence.

You will never guess their plan if they don't really have one.

That is beautifully put 😂😂😂

I've been looking at some interesting charts of late: the 90 day bank bill futures are pricing us to drop below the Aussie cash rate next year to get to -15 basis points (rate differential) by the September contract (BBU5) Since 1999 when this rate differential is around -15 the AUDNZD has historically been closer to 1.2200 ( now at 1.1050) Something is mispriced.

The OCR isn’t going to fix council rates, insurance premiums and electricity prices in any way that is helpful.

But it has to keep the cost of everything else down.. to balance overall inflation.

Inflation is caused by a basket of multiple goods people need to buy. We can't ignore the cost of rises of some of those items.

We can actually. We make choices for things to cost more because it is ‘better’ for various reasons. We increase the price of petrol, cigarettes, alcohol etc. putting too much pressure on things like rates will have undesirable consequences (under investment or degraded services etc)

You could argue that it does, as it can impact the interest cost of existing debt on the council books, and hence factor into rates.

Council rates should not be included in the CPI number used for ocr setting. Auckland is having an increase in rates due to the scrapping of pay as you throw system. The headline will be rates increase but won’t take into account the scrapping of the bin tags.

Regardless if HorOrr drops the rate .25 or not the dovish commentary will drop our dollar so it wont really matter from a FX point of view.

The committee may well go rogue and vote to drop it. It'll be the most interesting meeting/announcement we have had in the last couple of years.

Yes. Rbnz don't have an easy way out tho..

Keeping it on hold with a slightly less hawkish statement might be their best option.

The longer they wait to do something the safer for them. Following the fed is probably the least risky move ..but then the fed might hold tight for a while.

Imagine having to weigh up all the 'might happens' affecting the local and global economies this year...

@bdogg

The non-RB members of the committee may go rogue, but the RB members are likely to stick together. Could get a 4-3 vote in favour of OCR remaining at 5.5 %

Kerr: "The [...] Government also planned to build the massive Lake Onslow pumped hydro generation capacity, which stopped all other electricity generators from planning any new capacity."

Sad.

Yet another person (who should know better?) echoing the misinformation from the Gentailers.

The Lake Onslow scheme was a battery.

It was never, nor could it ever, be considered new generation capacity. It would - in fact - have been a net electricity consumer!

Yes. That's right. You lose some energy pumping water higher so it contains potential energy thanks to gravity.

Where it would have proved it's value is ... right now!

It could have converted the potential energy (thanks to gravity) back into electricity ... So the Gentailers couldn't price gouge as they are doing right now.

Completely agree.

In reality, what has stopped investment in new capacity over the last decade is the risk that the Tiwai Pt smelter shuts down, which would reduce demand by 10-15%

Bingo!

I don't think he has been unpredictable at all. If you look at the monetary policy statements he has done almost exactly as forecast i.e. not cut rates from 5.5% until after inflation is under 3% (in some cases several quarters after this and in some cases signalling risk of further increase).

He may not have done as many think he should, but he has been very predictable.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.