By Peter Dragicevich*

The wild gyrations in risk markets over the past week or so, such as Japanese and broader global stock markets, have generated bursts of volatility in the NZD. This isn’t unusual given the NZD’s standing as a growth-linked currency and its positive correlation to cyclical assets like commodities and equities.

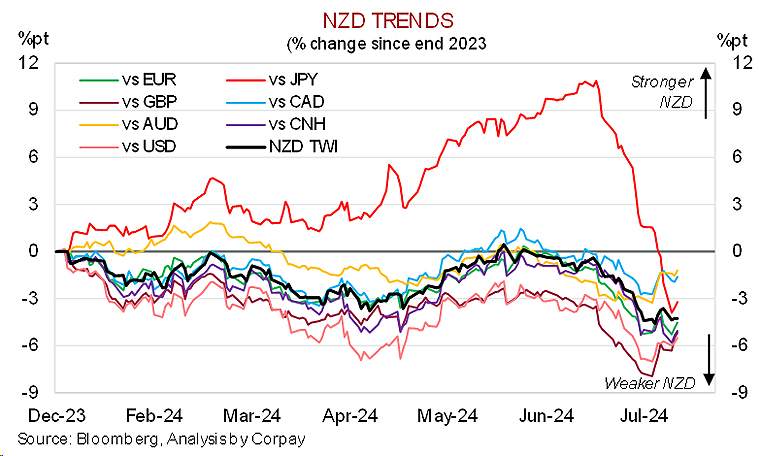

The NZD has recouped a bit of lost ground over the past few sessions, in line with a calming in concerns. But at ~$0.60 against the USD and ~$0.9175 versus the AUD it is still tracking below its respective one-year averages and remains within striking distance of its recently touched year-to-date lows.

Taking a step back from the day-to-day swings we think a couple of important domestic and offshore NZD headwinds are taking hold. From our perspective, these forces mean sustainable NZD upside should be constrained and that it is likely to remain a relative FX underperformer over coming quarters.

Firstly, we doubt the abrupt reversal in the JPY has run its course. Japanese economic signals, such as underlying wage and inflation impulses, suggest the Bank of Japan has further to move along its monetary policy normalisation path. After two hikes the BoJ’s policy rate is only at 0.25%. Importantly, this is negative on an inflation adjusted basis and below the equilibrium ‘neutral’ rate. We believe more tightening by the BoJ at the time many other major central banks (including the RBNZ, see below) are turning course and lowering interest rates will help the still undervalued yen’s revival extend. Additional downward pressure on NZD/JPY, particularly if outsized moves persist, could have negative flow through to other NZD pairs, as it has done since early-July. It shouldn’t be forgotten that FX is a relative price. NZD/JPY has picked itself up off the canvas over the past 24hrs, but it remains nearly 11% from its 8 July multi-decade peak. Over the same period other JPY-crosses like USD/JPY and EUR/JPY have ‘only’ fallen by ~8-9%.

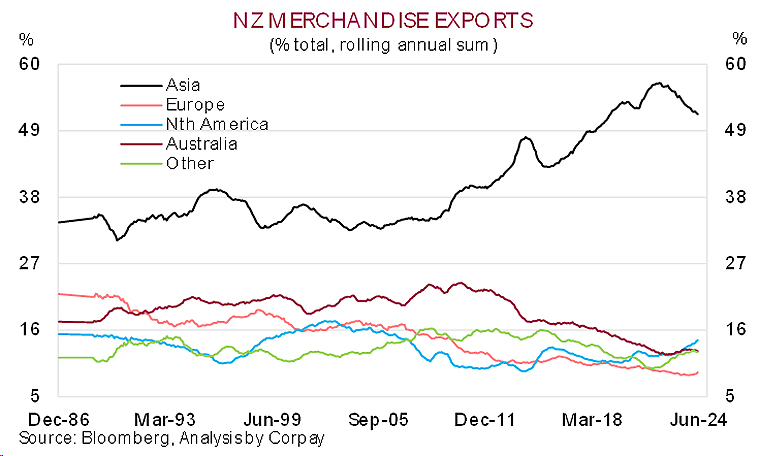

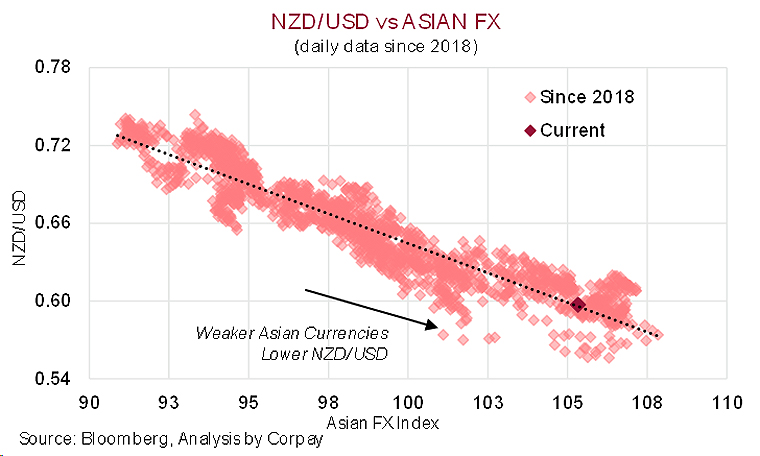

Secondly, we also feel regional Asian currencies are facing near-term challenges. Sluggish growth across Asia should continue as tight policy conditions, weak momentum in the major Western nations, and structural/overcapacity issues in China suppress industrial activity. This, combined with a potential ratcheting up in geopolitical risk premium as the 5 November US Presidential Election comes closer into view may stifle capital inflows and/or trigger capital flight. Former President Trump’s rather vocal enthusiasm for imposing substantial tariffs of ~10% on US imports and ~60% on goods from China could rattle nerves about the trajectory of Asia’s economy if the polling shows greater odds of his return to the White House. This is important for New Zealand given ~52% of its merchandise exports are sent to Asia directly. This jumps up to ~64% if Australia (which sends ~3/4’s of its exports to the region) are included in the numbers. The strong trade-ties between New Zealand and Asia help explain why the NZD’s fortunes have become increasingly tethered to trends in Asian currencies. As illustrated, depreciating (appreciating) Asian currencies typically translate to a weaker (stronger) NZD.

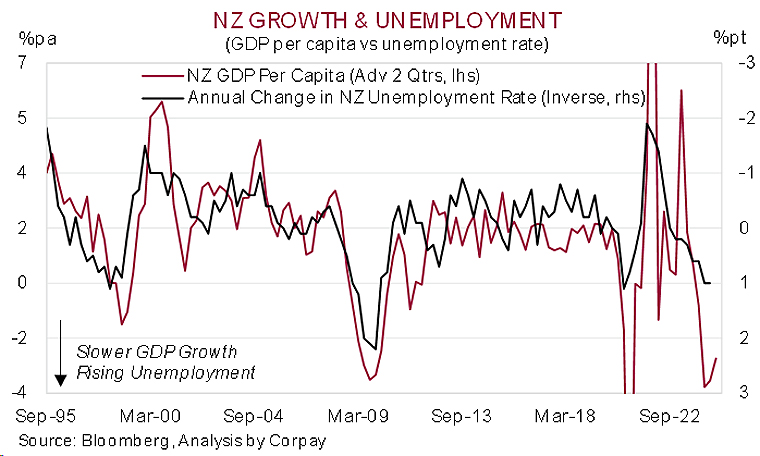

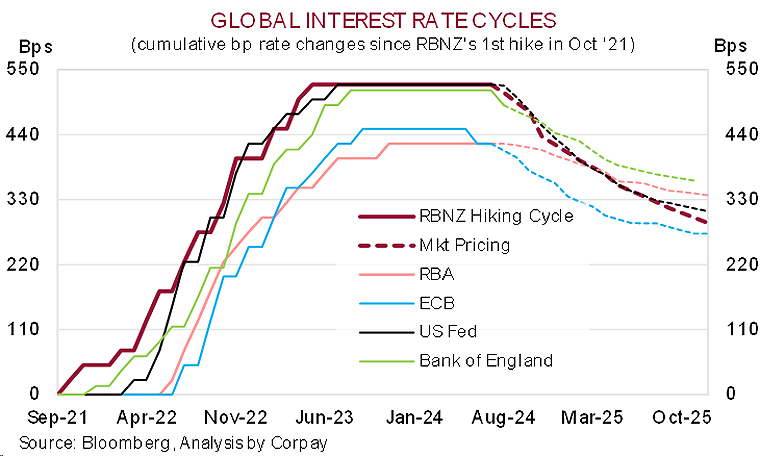

Thirdly, New Zealand’s domestic economic fortunes are floundering. The harsher macro climate due to the RBNZ’s aggressive tightening and quite ‘restrictive’ policy stance are clearly manifesting. On a per capita basis New Zealand GDP has now contracted for six straight quarters. Subpar business and consumer confidence, elevated mortgage costs, and amplifiers like high household debt levels and rising unemployment mean downside growth risks are in the ascendency. New Zealand’s unemployment rate has risen to 4.6%, ~1%pt above where it was a year ago. The labour market is a lagging indicator. The relationship with economic activity suggests further increases in New Zealand unemployment are probable. In our opinion, the ‘slack’ emerging across the New Zealand economy should help dampen inflation and means interest rate reductions by the RBNZ are a matter of time with an extended cutting cycle in the pipeline.

A swift turnaround from the RBNZ could be a multi-faceted pressure point for the NZD. A closer look finds New Zealand’s wide current account deficit position (now an above average ~6.8% of GDP) has been increasingly funded by foreign investors drawn in by attractive yields.

The loss of New Zealand’s superior ‘carry’ stemming from to a meaningful adjustment lower in interest rates aimed at warding off growth risks may expose the NZD to even more downside than what the crosscurrents outlined imply because of the possible drying up of capital inflows needed to fund the external imbalance.

Peter Dragicevich is Currency Strategist, APAC, at Corpay, based in Sydney, Australia. This is his Peter’s personal opinions and analysis and does not necessarily reflect the opinion of or endorsement by Corpay. This presentation is provided for general-information only. This presentation is not (and does not include) advice.

1 Comments

Really good analysis. Let's hope it will not be as bad as projected in this article.

The "sugar high" from the Labour government in NZ throwing loads of money around, and the RBNZ pitching in with quantitative easing, have finally come home to roost. However, I doubt there are a lot of Kiwis who will realise who is responsible. They may blame the current government, and opt for a Labour/Green government next time, with disastrous effects on employment and the businesses that employ people.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.