Summary of key points: -

- Weak US economic data changes odds on interest rate cuts

- Unwinding of Japanese Yen carry-trades having a wide market impact

- Tricky decision for the Reserve Bank of Australia this week

Weak US economic data changes odds on interest rate cuts

Over the last seven days the US dollar currency value has weakened across the board, the USD Dixy Index plummeting 1.5% from 104.60 to 103.00 at the close of trading on Friday 2nd August.

The full extent of the USD depreciation has not (yet) been reflected in the NZD/USD exchange rate, the Kiwi dollar lifting just 80 points from 0.5880 to 0.5960 over the week. The unexpected weakness in the Australian dollar at this time has certainly been holding the Kiwi dollar back from making more meaningful gains against the USD. The Aussie dollar has struggled to recover above 0.6500 against the USD after its three-cent upper-cut from 0.6800, due to the unwinding of Japanese Yen carry-trades against the AUD the previous week.

In addition, there has also been some very large currency options positions in the NZD/AUD cross-rate that have been forced to reverse, sending the NZD/AUD cross-rate soaring from below 0.9000 five days ago to 0.9150 at Friday 2nd November. The NZD/AUD option trades were originally set to gain from the NZ dollar depreciating against the Australian dollar as NZ interest rates are supposedly cut well ahead in time of Australian interest rates. However, when the selling of the AUD against the USD last week was greater than NZD selling, it started to propel the NZD/AUD cross-rate upwards. Effectively the option trades expecting a lower NZD against the AUD were “stopped-out”, resulting in the cross-rate climbing to 0.9150. Local exporters selling in AUD who had FX orders placed in the market to enter hedges from 0.91000 down to 0.9000 have been well rewarded for their strategy.

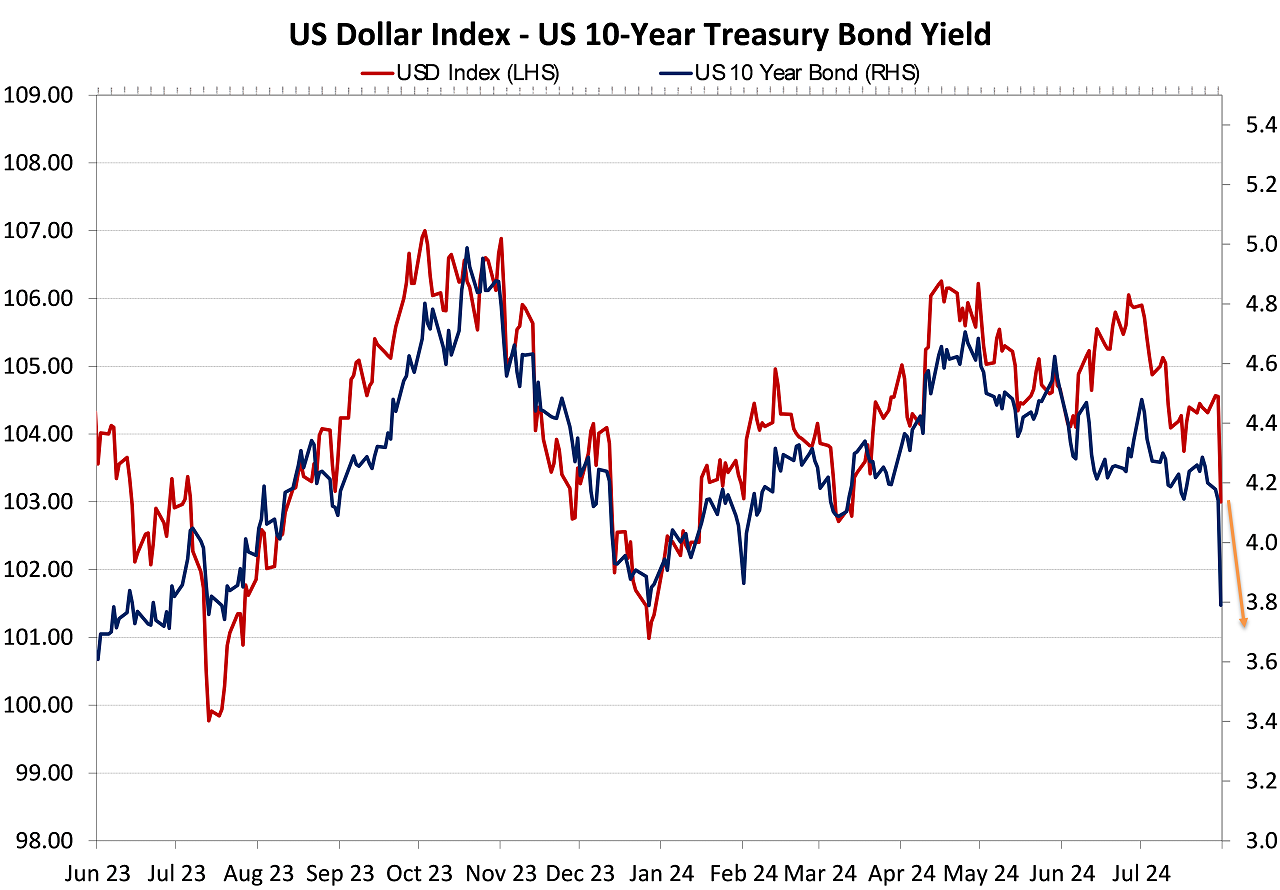

In last week’s FX report we included a chart of the USD Dixy Index closely tracking the US 10-year Treasury Bond yields lower. Added on to the chart were two gold arrows of the expected further reductions in the bond yields from 4.25% and the USD Index from above 104 at the time. We did not necessarily expect the US bond yields to plummet to the 3.80% target indicated by the gold arrow within a period of seven days! However, that is precisely what has happened. The expected implied confirmation from the US Federal Reserve at their meeting last Thursday morning that they are set to cut interest rates in mid-September caused the initial push down in bond yields. The much weaker than expected Non-Farm Payrolls jobs report on Friday night sending the 10-year bond yields lower still to 3.80%. Greater confidence from both the Fed and the bond market that US inflation is headed to 2.00% and there is no risk of its rising back up again has driven these major market changes. At 3.80%, the US 10-year bond yields have returned to the level they reached in December 2023 when the Fed first pivoted on monetary policy.

Back in December 2023, the USD Index was sold off to 101.00 on the lower 3.80% bond yields and the NZD/USD exchange rate soared to a 0.6300 high. As the updated chart below depicts, the US dollar still has a lot of catching up to do to match the decrease in bond yields. However, the correlation is reasonably reliable, therefore expect further general USD depreciation over coming weeks from the current 103.00 level to 101.00 (indicated by the gold arrow). In December 2023, the USD Index (red line) hit a low of 101.00, only to recover higher on the “bump” upwards in US inflation and jobs over the first three months of 2024. On US dollar depreciation alone, the Kiwi dollar should be trading well above 0.6000 at this time. However, the Aussie dollar has held it back, as has “heroic” forward pricing on massive interest rate cuts in New Zealand over coming months.

The US short-term interest rate markets are now pricing-in a 70% probability that the Fed will be forced to make their first interest rate cut on 18 September a 0.50% reduction, instead of the earlier anticipated 0.25% cut. The US unemployment rate increasing to 4.30% will be prompting the pricing, as the Fed have always stated that a more rapid softening in the labour market would be a reason why they would cut earlier and by more than the standard 0.25%.

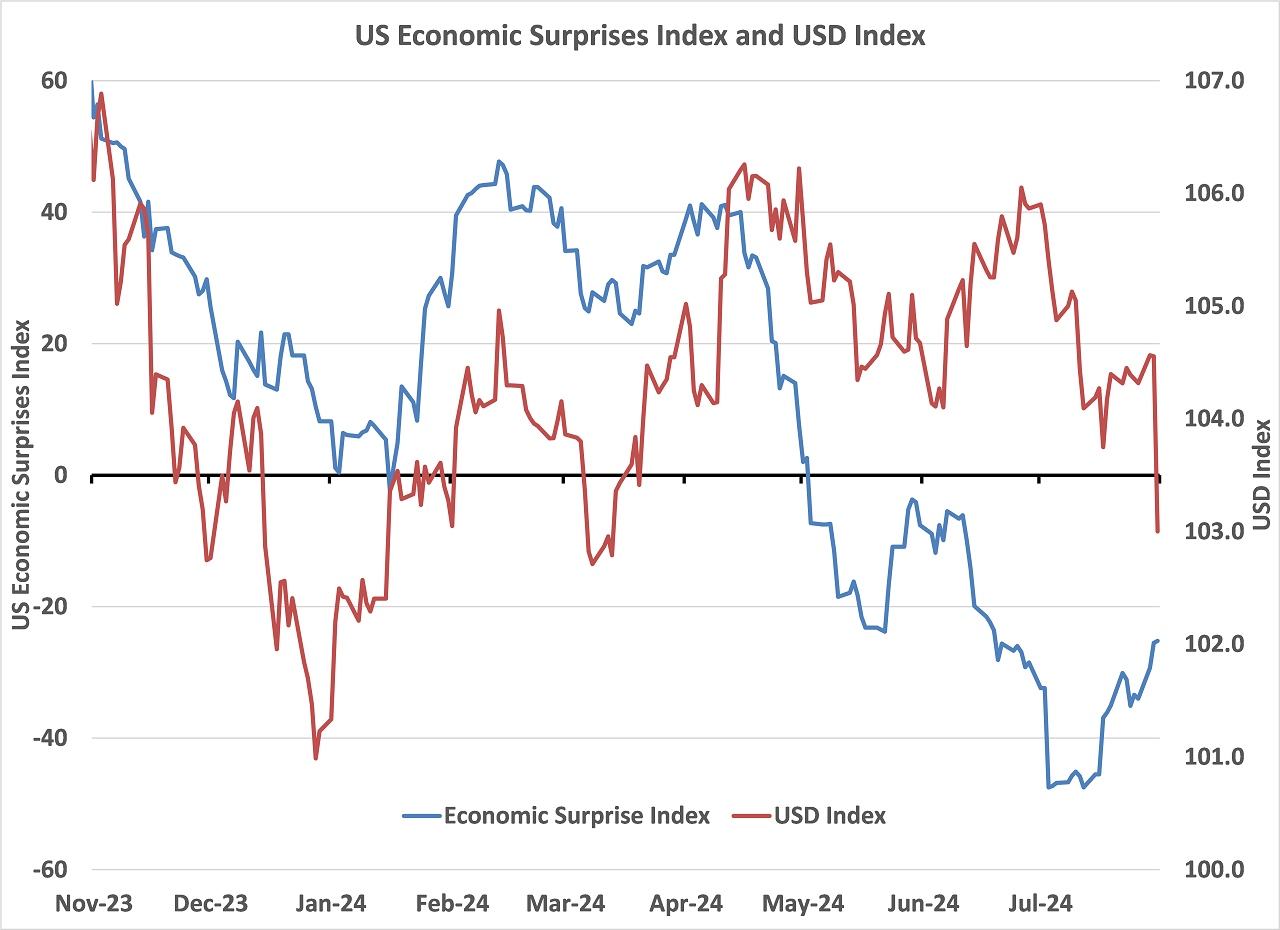

US economic data has been weaker than expected across the board over recent weeks, the long lags it takes for restrictive/tight monetary policy to impact at the household and “Main Street” level is now being observed. Another reason why the US dollar has much further to decline over coming months is confirmed in the chart below that plots “economic surprises” i.e. the blue line below zero on the chart when all measures of the economy come out weaker than prior consensus forecasts.

Unwinding of Japanese Yen carry-trades having a wide market impact

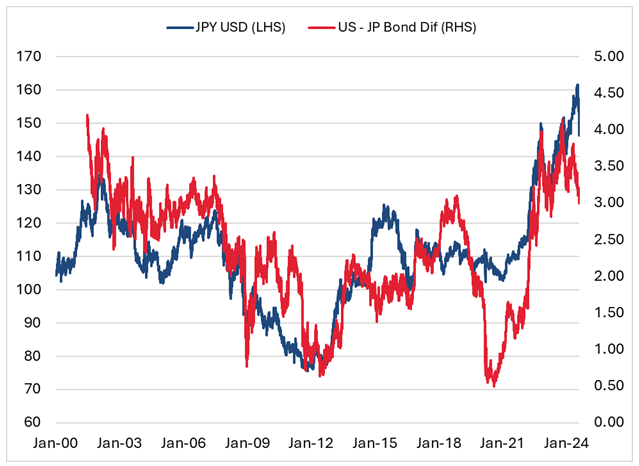

The Bank of Japan increasing their official interest rates by 0.15% from 0.10% to 0.25% last week added to the already spectacular appreciation of the Japanese Yen. The Yen has now appreciated 9.50% from 162.00 against the USD on 10th July to 146.50 on 2nd August. With the interest rate differential between US 10-year bond yields and Japanese 10-year bond yields closing up dramatically from above 4.00% to less than 3.00% over recent weeks, the tracking USD/JPY exchange rate seems destined to go a lot lower yet towards 130.00 (refer chart below).

The original entry by currency investors/traders into the Japanese Yen carry-trade and now the rapid exit from those trades, has wider implications for global markets than just the foreign exchange market. Renowned economists in the US are reporting that “the strong relationship between the structure of monetary policy in China and Japan and US asset prices will come as a huge shock for most US investors”. In other words, part of the reason for the sell-off in US equities over the last few weeks is related to the Yen currency reversing and the Japanese increasing their interest rates when everyone else is seeking to cut. Japanese investment houses are bringing funds home as the interest rate advantage of being invested in the US is not as attractive as it once was. US hedge fund investors are being forced to sell US shares to raise cash to repay their Yen debt on the carry-trades. As an example of “following the money”, Warren Buffets Berkshire Hathaway was buying into Japanese trading houses several months ago when the Yen was weak, Buffett is now selling out of 50% of his over-valued Apple shares in the US. Berkshire Hataway has a US$277 billion cash war chest, whenever they decide to deploy that into investments around the world rather than in the US, is not a good sign for the US dollar value.

Unfortunately, for risk sensitive currencies such as the NZD and AUD, falling US equity markets do not allow these currencies to make the gains they normally would in an overall weaker US dollar environment. Having said that, a continuation of Japanese Yen appreciation to 130 against the USD would likely see the NZD/USD and AUD/USD exchange rates follow to some extent and lift a good few cents.

Tricky decision for the Reserve Bank of Australia this week

It tells you something about financial market psychology when annual inflation in Australia remains stubbornly high at 3.80%, however the Aussie dollar depreciates rather appreciates on the fact that Australian interest rates are set to remain stable when the rest of the world is cutting rates. Why the AUD was sold off on the June quarter inflation report is answered by the likelihood that the short-term FX market was “long AUD” going into the economic data release in expectation of a quarterly increase above 1.00%, and when that did not eventuate the AUD’s were sold back to market. The markets latched on to the RBA Trimmed Mean CPI measure coming in at an 3.90% annual rate, fractionally below the 4.00% of prior forecasts. The conclusion from the markets was that the RBA will not be lifting their interest rates at their meeting this Tuesday and that has kept the AUD/USD exchange rate close to 0.6500.

The wording of the RBA statement and the approach of Governor Michele Bullock in the subsequent media conference will determine how hawkish (or not) this monetary policy decision will be. Inflation at 3.80% remains a very long way above their target rate of 2.50%, therefore the RBA should not be signalling any message that interest rates are about to be lowered. A more hawkish than expected message from the RBA on Tuesday should send the AUD/USD exchange rate higher. It is unlikely that the RBA are in a position to provide any hint to the markets that inflation is totally under control, and they will soon be lowering interest rates. Australia’s annual inflation rate over the last six months has increased from 3.60% to 3.80% and there are no signs that the ever-increasing prices for rents, electricity, insurance premiums and building construction costs are about to suddenly turn the other way.

The local FX and interest rate markets are likely to be disappointed if they are expecting Ms Bullock to signal interest rate cuts before the end of this year. Early 2025 seems the earliest likely timing for cuts as the RBA will need to see clear trends of inflation decreasing, currently they are not seeing that. Similar to New Zealand, Australian services inflation remains stubbornly high. Unlike New Zealand, their goods (or tradable) inflation is not rapidly decreasing.

Tuesday’s RBA statement should signal a turn-around in the Aussie dollar fortunes and kick-start an AUD/USD recovery back to 0.6800 and higher.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.