Followers of Statistics NZ's monthly electronic card transaction data will know that in the early months of this year spending by the Kiwi consumer has been grinding to a halt.

Figures have been dropping, despite prices having risen (which all things being equal should see sales figures rise), and despite the fact the NZ population surged by over 100,000 people in the past year. Again, all things equal, that's supposedly 100,000 extra wallets boosting the spending figures.

But it is the grand design. The Reserve Bank's shunting of the Official Cash Rate up from just 0.25% as of the start of October 2021 to 5.5% as of now was aimed at taking heat out of the economy so that runaway inflation could be brought to heel.

RBNZ Governor Adrian Orr even conceded that the central bank was engineering a recession. Well, job done. NZ was, as of the December quarter in recession. And we'll find out next week if this continued into the March quarter. If recent spending data is anything to go by, possibly. (I'll be having a closer look at the forthcoming GDP figures over the weekend.)

The country's largest bank has added some flavour and texture to the overall spending picture with the release of granular detail on card spending of ANZ customers during May.

The picture painted is one of serious cut backs occurring. Spending on home refurbishment has slumped. Discretionary spending and spending on durables are down. Spending on repair services is up. Make do and mend. Buy-now-pay-later (BNPL) spending is up.

ANZ points out that many data series are volatile month-to-month "at this very disaggregated level". The bank therefore presents the data in rolling 3-month average terms (3mma) to make trends clearer. The data is also seasonally adjusted where the diagnostics support this.

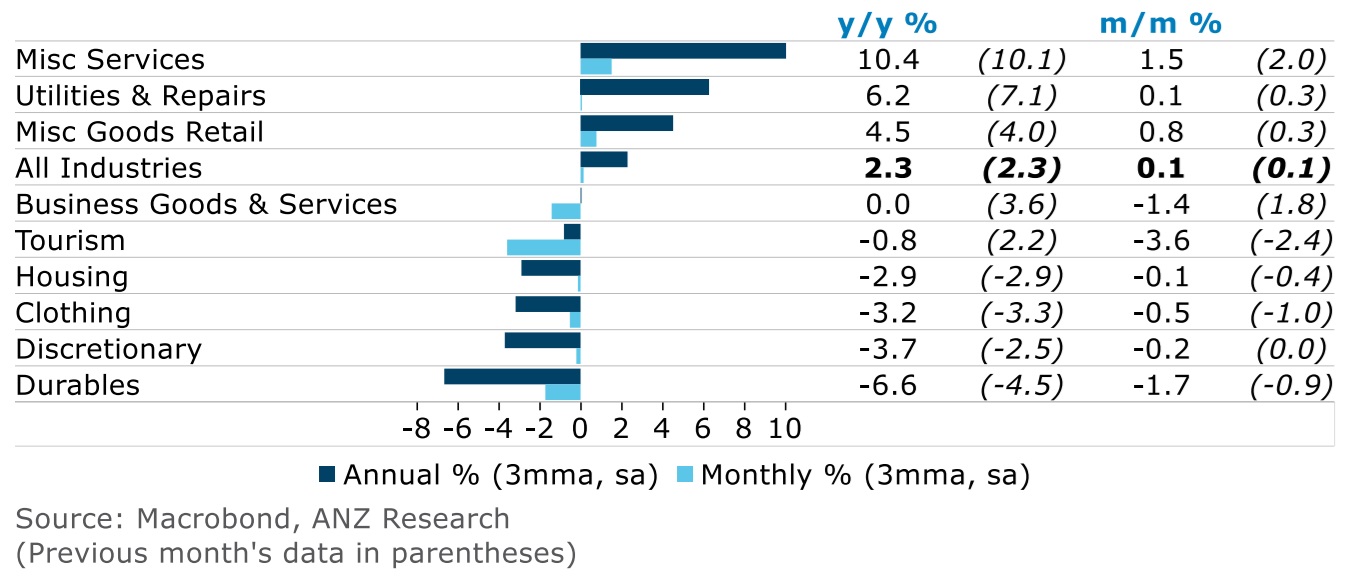

ANZ chief economist Sharon Zollner says annual growth in card spending was just 2.3% year-on-year in May, "despite inflation running at a considerably higher pace". (Annual inflation as measured by the Consumers Price Index - the CPI - was 4.0% as of the March quarter.)

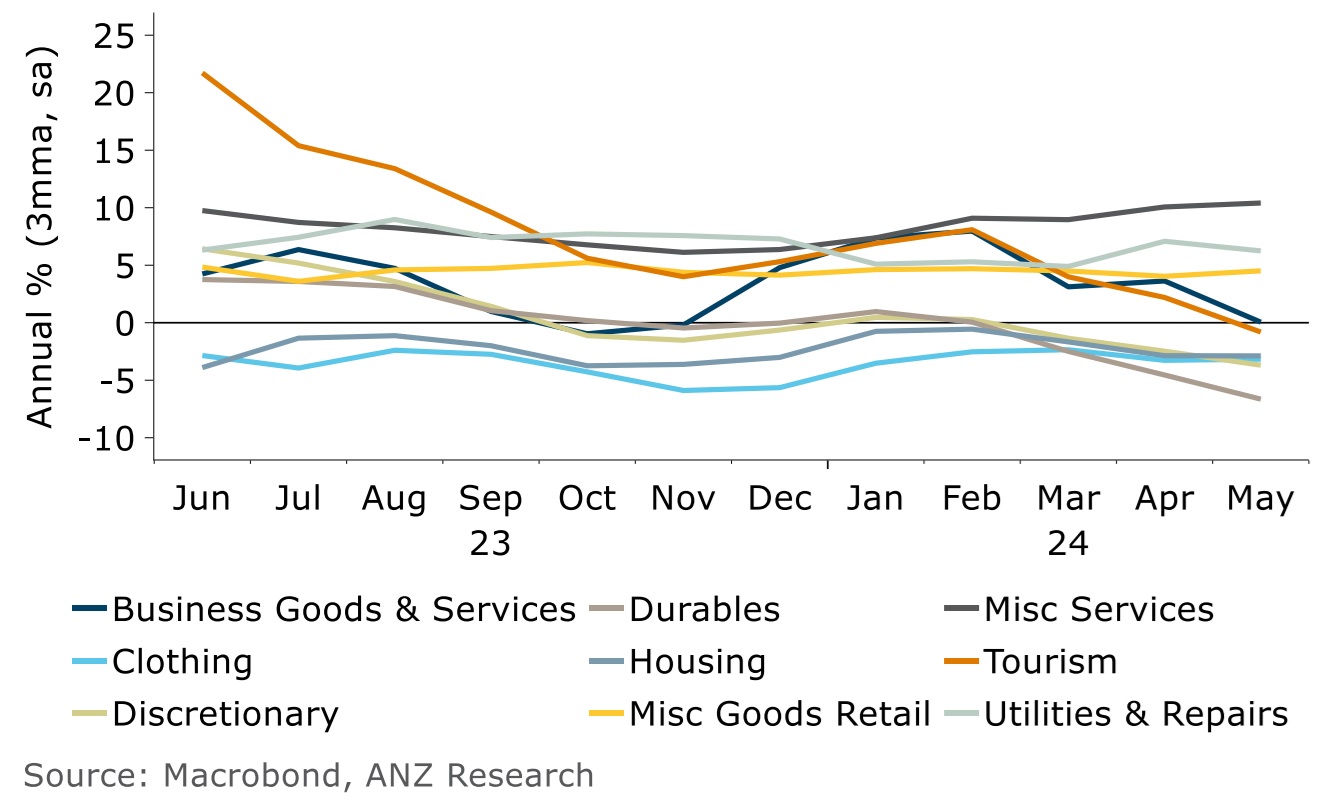

"Durables, discretionary spending categories and clothing continue to lag. The impetus from tourism-related spending has turned into a drag on growth. Miscellaneous services is one category gaining momentum, with strength here driven by finance services," Zollner says.

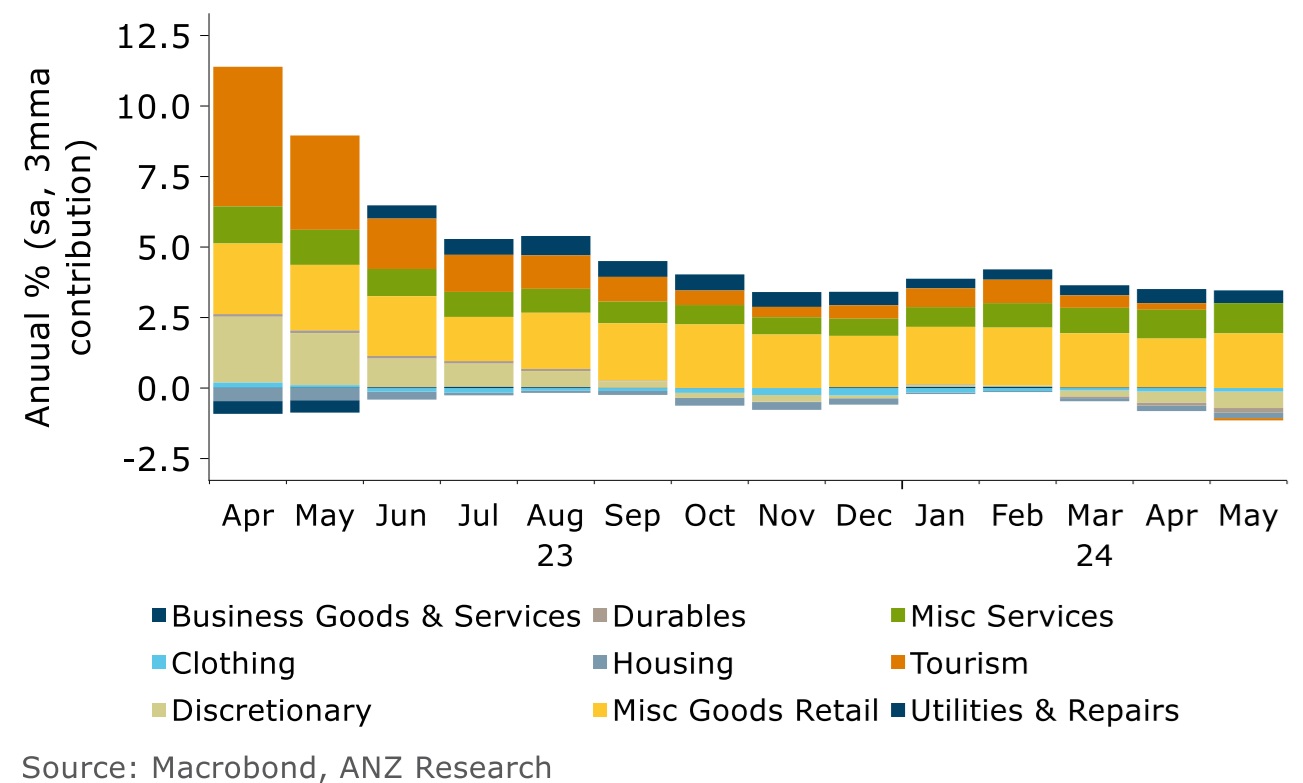

"Zooming in on the contributions of each category to total card spending growth in the past year [see graph below] shows growth being held up by just two categories: miscellaneous goods (which includes buy-now-pay-later payments) and miscellaneous services, which as noted, have been supported by finance services," Zollner says.

She adds that the strength in finance services "is not necessarily a strong indicator. Good advice is invaluable in tough times."

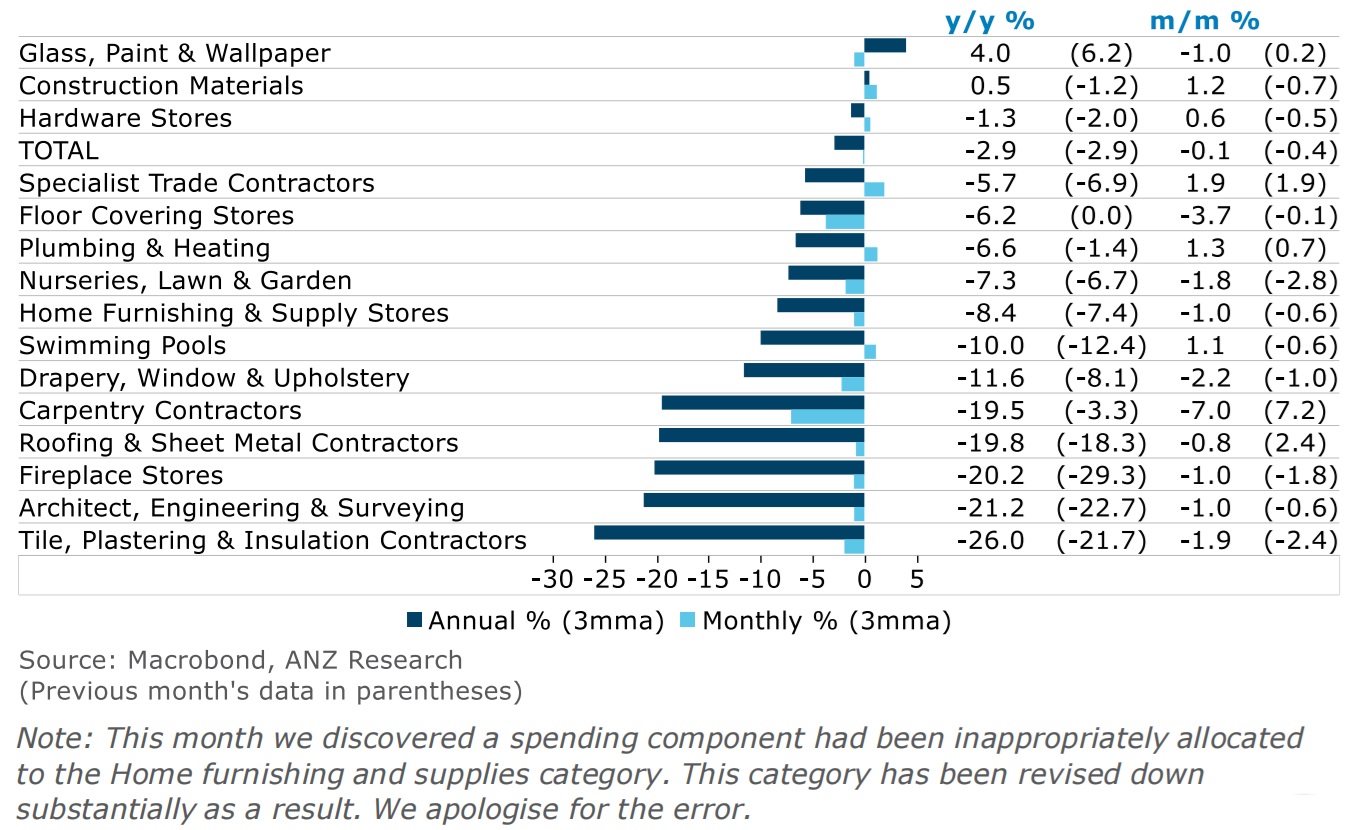

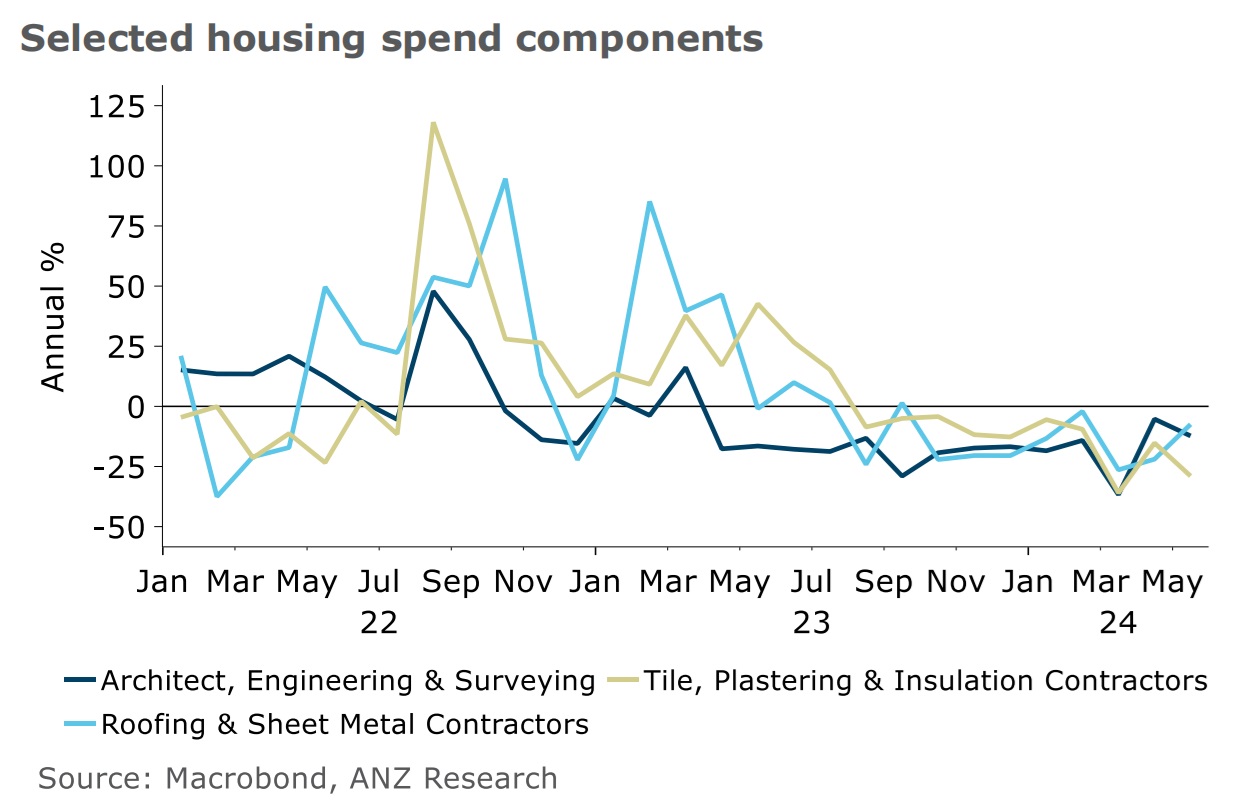

Looking at housing-related spending, Zollner says spending in this category is down nearly 3% year-on-year.

The only category in the housing group that is up more than negligibly year-on-year is 'glass, paint and wallpaper', "suggesting cheap spruce-ups may be standing in for expensive renovations".

Zollner notes that sharply weaker construction activity is evident in the bottom five categories, which are all down 20-25% year-on-year.

"Categories related to building are particularly weak at present."

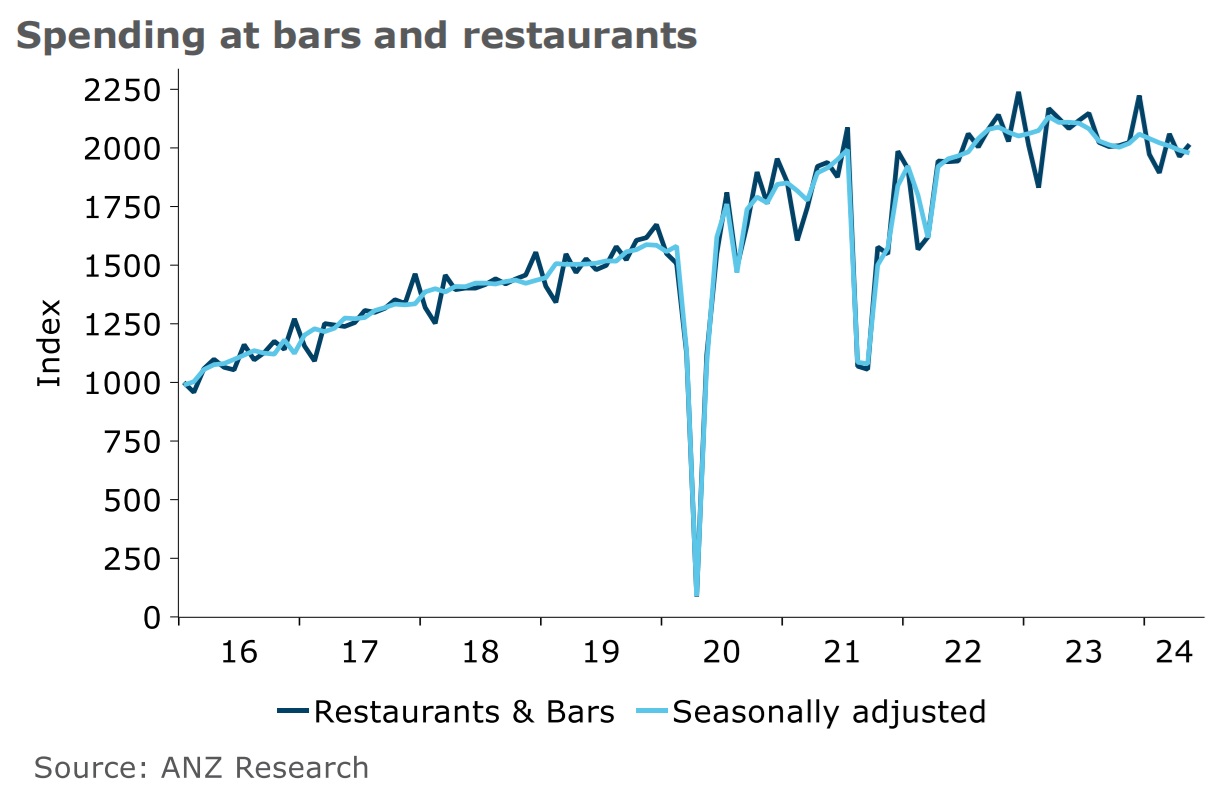

The flattening off and now outright decline in spending at restaurants and bars has been marked "as consumers increasingly watch their pennies", Zollner says.

Spending across a range of clothing store types remains very weak, while repairing existing clothing has been more popular.

Durables spending remains under pressure due to a soft housing market, high interest rates and a weakening labour market.

Boaties and motor home dealers may have benefited from the return of tourists, but now that the growth in tourist numbers is cooling, annual growth is following suit, Zollner says.

15 Comments

I went to a big box retailer down at the local 'Supa Center' the other day as my trusty coffee machine seems to be giving up the ghost (side note, anybody caught using the term 'Supa' instead of 'Super' when naming their shopping precinct will be sentenced to LWOP when I am running the country and Jfoe is minister of finance)

Mid afternoon on a Saturday, big sales on, and staff outnumbered customers five-to-one. You'd find more life on the surface of the moon than in that store.

Over on Cheapies (a very helpful site for finding good deals if you're not aware of it) there was a thread discussing the $1 reserve 'free selling' promotion on TradeMe. Numerous comments from in-trade sellers saying they won't use the $1 reserve option any more, because in the current economic climate people just aren't bidding like they were - even on the chance to get a bargain.

Looks like car sales are in the doldrums too.

I humbly submit myself for consideration in your cabinet for the role of Minister of Revenue.

I'd like to take the Ministry of Justice. I'd have that pesky crime problem solved in a jiffy.

It's not a minister of justice that's going to solve our crime problem.

Can I just get paid the housing allowance while living at home, sitting on the back benches, clipping the ticket and enjoying my vast holidays?

Who were the commentators on here saying the next OCR move will be a hike?

They were the older ones with money in term deposits.

This month around 25% of *total* NZ wages and salaries will be paid as interest on housing and business loans. The banks - most of whom have been big cheerleaders for 'higher for longer' - will take about 15% of that interest as profits. Indeed, the hawkiest of the hawks - ANZ - made record profits last quarter.

Given that we are collapsing demand and increasing unemployment harder and faster than just about every other country on earth, I am presuming that our inflation will moderate more quickly? Is that how it is supposed to work?

In other news...

- Average rents rose by an inflation-busting 6% last month

- Insurance premiums are going bananas

- Councils are queuing up to hike rates by double-digits

- The Government is banking on using the Emissions Trading Scheme to tackle emissions (and not a lot else), so petrol and diesel prices will be rising through 2025

- Global food prices are back on the move as climate change wreaks havoc

Just to clarify, on the "25% of *total* NZ wages and salaries" - you're meaning total gross wages and salaries right? (this is what I'm assuming).

Which means as a percentage of after tax wages and salaries, you'd probably be looking at a number between 30-35% (32.9% using an effective tax rate of 24% which is effectively the PAYE on a salary of $100k).

Yes, that's correct. Important to note that people in NZ have a lot of non-wage income (rents, entrepreneurial income / dividends etc). And, just under half of that interest is owner-occupier mortgages.

Yes. the most disinflation is in the discretionary spend categories. Plenty of inflation in the non-negotiable categories

I despair at RBNZ Orr, non tradable inflation - Interest/Insurance/Rates is not affected by OCR so higher for longer cannot fix theses items, perhaps Orr wants a depression.

Went out to dinner last Friday evening. Thai - nothing too expensive. Four tables in with the other 8 empty. Upon leaving we drove around a little bit of the central city on the way out of our [stupid] one way system. We were the only car actually moving on the road as we made this manoeuvre. More dead than quiet.

I went to a Viewnamese restaurant last week second time, pretty full good service, good food fair prices, leaving for the car park passed a Indian no one in,previous time one table occupied nice place wonder why - poor service, high price poor menu?? The writing is on the wall folks and its in English.

Even the wealthy are packing up & leaving offshore, so much for Nats claiming to fix the economy, instead they’re screwing it

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.