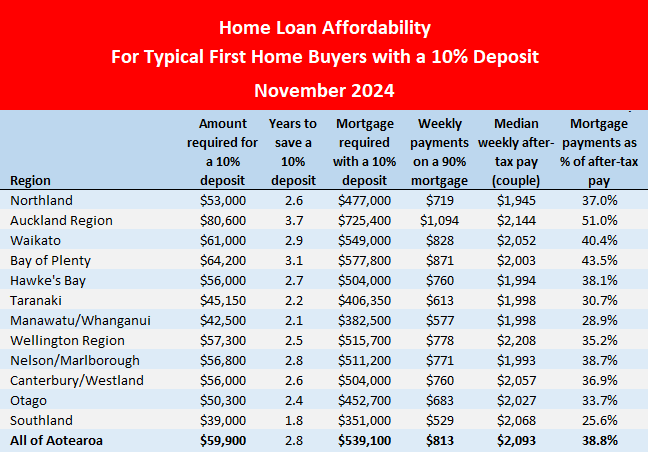

Small declines in both house prices and mortgage interest rates during November made home ownership the most affordable it has been for first home buyers since October 2021.

According to the Real Estate Institute of New Zealand, the national median selling price declined from $607,500 in October to $599,000 in November.

That puts it just below where it was in November last year, $600,000, but still well below its November 2021 peak of $670,000.

At the same time the average of the two year fixed mortgage rates has continued to decline, down to 5.63% in November from 5.68% in October and 7.04% in November last year.

The average two year fixed rate is now at its lowest point since September 2022.

Slow but steady increases in income are also helping.

Interest.co.nz estimates the median take home pay for working couples aged 25-29 has been increasing by about $3 a month since the beginning of the year.

While none of the above would have made a significant impact on housing affordability levels on their own, when taken together they have made home ownership the most affordable it has been for typical first home buyers since October 2021.

Unfortunately an improvement in affordability is not the same as being affordable.

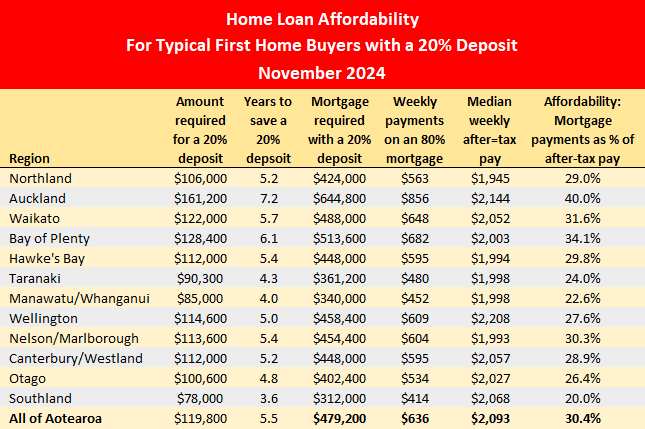

On average, first home buyers would still need to find more than $100,000 for a 20% deposit on a home at the national lower quartile selling price, and in Auckland they would need $161,200.

If they went for a low equity mortgage with a 10% deposit, the repayments would likely be so high they would push home ownership out of reach for typical first home buyers in higher priced regions such as Auckland and the Bay of Plenty.

So although affordability has improved for first home buyers, major challenges remain.

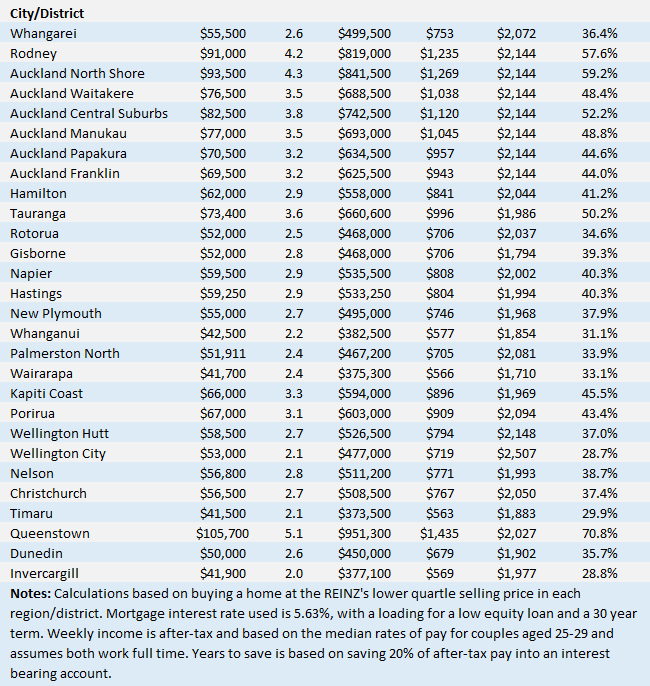

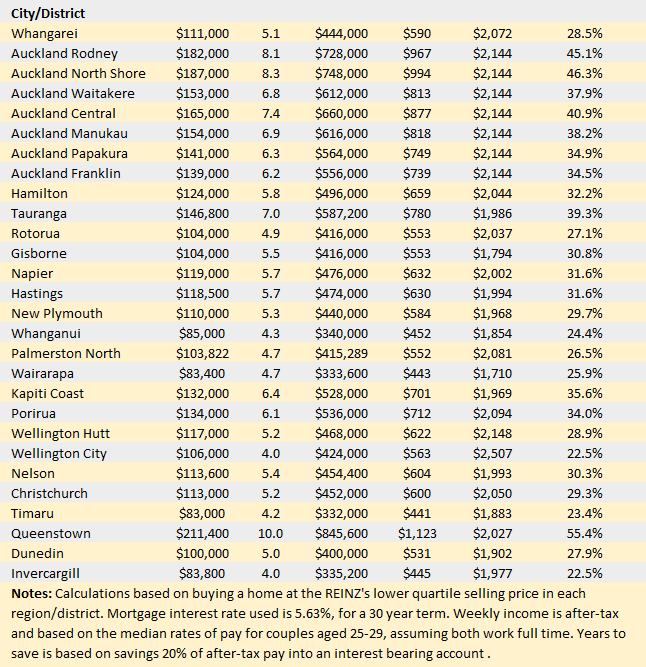

The tables below show the main affordability measures for typical first home buyers with either a 10% or 20% deposit, in all major urban areas of Aotearoa.

The comment stream on this story is now closed.

74 Comments

So if one of the couple loses their job, they cannot even afford the mortgage payments?

Two people working on the typical NZ wage has been the requirement to pay a mortgage for the last 25 years, nothing has changed. If you want to buy a place on your own you need flatmates. Very few people are on the sort of money you can do it all on one income.

"Very few people are on the sort of money you can do it all on one income."

Isnt the point of greater concern that fewer and fewer can do it on two full time incomes (and government assistance)?

So no kids then....

True, we can import all the people we could ever need from other countries. Kiwis, please stop breeding.

It’s just reality. Unless we had an excess of houses (which is unlikely unless we get population decline), then people will pay whatever they can afford to buy one. The way they afford it is by working as many hours as physically possible. If you don’t do that, someone else will.

It took me a while to realise this, but there is no fix other than population decline, and that has its own problems.

There will be an excess of houses the moment the immigration ponzi is shut down.

The native population of NZ is declining, rapidly.

Wait till Trump is inaugurated January 20 (only under a month away) .......then the Fed have got a great excuse to do whatever they like and either:

A. Take interest rates down further than markets think, markets borrow again like drunken sailors, pushing stocks etc into the stratosphere, then create inflation like no one has ever seen it - then the banksters can snap up assets that nearly all folks won't be able to afford ...

B. Lift interest rates and strangle the economy into a recession ....and either leave there or keep raising them until the point of a depression - then the banksters can snap up assets that nearly all folks won't be able to afford ...

Notice a theme above ?

Then no matter what happens, if it all turns to custard, they can all blame Trump !!!

He will be used as the scapegoat in all cases, in how this economy plays out in 2025

Ummm. Are you an AI generated contributor or just a deluded wanker?

Charming comment ... your cognitive dissonance is clearly showing through...tell me what an inverted yield curve is then we may have a conversation ...by the way are you a bankster ?

Rhumline are you all up to date on your flu shots?

Believe it or not, Elizabeth Warren first became a celebrity long before winning a US Senate seat, while a Professor at University, with a video presentation called "The Coming Collapse of the Middle Class". She discussed the various categories of household spending and said that housing was the big outlier one that had significant inflation in recent decades. She said that one of the implications of this was that the kind of misfortune that does come along for many people in a normal lifetime, will tip a lot more people into bankruptcy. Not just a job loss, but sickness or injury of either breadwinner; or of one of their children or a dependent parent; birth of a child with a disability; a natural disaster; being the victim of a crime; an increase in interest rates (the lower they are, the more likely this is).

I actually quoted this in an opinion piece the Sunday Star Times published ten years ago, which I will now post as a new comment.

Just like when interest rates were the lowest they ever were people bitching and saying "don't fix for 5 years, there going negative"

Now its the best time to buy in years and interest rates dropping and people still bitching...

The people that do do and the people the whine get no where..

Merry Ho Ho :)

Mad isn't it.

“They act as if a low rate is a panacea and comes with no downside. That is clearly nonsense. It’s created the biggest evil in our society and that is inequality.”

- Legendary investor Jeremy Grantham on how the sheeple and Ponzi promoters think and the actual reality - low interest rates working with non-GDP qualifying credit creation to drive up asset prices

But it need not with the right policies and in fact the drop in interest rates has not seen the, normally, corresponding rise in house prices.

It is possible to have both more affordable house prices in real terms, and lower interest rates.

It is possible to have both more affordable house prices in real terms, and lower interest rates.

You mean like Japan and China? For sure this is possible. But you also have to face the consequences. I'm not sure Aotearoans are mentally, emotionally, and financially equipped to go what Japan has faced and what China is dealing with.

No, I mean like Texas and many other jurisdictions.

In Texas, mortgage rates are currently competitive and generally lower than the national average. As of December 2024, the average rate for a 30-year fixed mortgage in Texas is approximately 6.41%, compared to a national average of 6.83%. So not much lower and somewhat similar to Aotearoa.

The inflation rate in Texas is reported to be approx 3.1% yoy year-over-year, based on the Consumer Price Index (CPI) data - the national average inflation rate for the same period is slightly lower at 2.7%.

As of November 2024, home prices in Texas increased by approx 2.4% compared to the previous year. However, between 2019 and 2023, median home prices in Texas surged by about 40%, with some areas experiencing even sharper increases. For ex, the Brownsville-Harlingen area saw a whopping 73% increase.

So why did you stop there?

Why didn't you mention the median income multiple?

Median house price to income in Texas is approx 4.7x in 2024.

Does this somehow debunk Jeremy Grantham's suggestion that the ruling elite is a one-trick pony manipulating the price of money?

The original point made was lowering interest rates would result in capital asset increases.

My point, as the Texas evidence shows is that you can have both low interest rates and house prices relative to income - if you have the right land use policy settings.

And maybe also if you have, like Texas does:

- huge areas of flat land (na for Auckland)

- big population and economies of scale (na for Auckland)

- very cheap labour (na for Auckland)

Huge fossil fuel subsidies that externalise the costs of sprawl.

California has the same subsidies, but twice the house price.

Both California and Australia have large areas of flat land and yet they have high house prices.

Also if you have been to Texas then you would know that it has plenty of hills and flat land with poor building conditions.

California has both a larger population and just as easy access to cheap labour as Texas does, yet housing is twice the price of Texas.

And prior to 1994, we used to have the same low median multiple as Texas.

The price of housing in NZ is almost entirely due to poor land use policy decisions.

And prior to 1994, we used to have the same low median multiple as Texas.

The price of housing in NZ is almost entirely due to poor land use policy decisions.

So would your reckon suggest that if Aotearoa and the Anglosphere had optimal land use policies, the issuance of cheap credit creation would flow for productive purposes at the same rate it has for the Ponzi?

No doubt sub-optimal land use policies distort markets. But those markets can only be distorted when lending for mortgages is one of the primary vehicles for juicing the money supply.

People in Texas have mortgages, but the mortgages don't 'juice' the housing market.

That is because the land use policies allow supply to meet demand in real time, so there is no ability to speculate the market via non value added costs.

If you want to make money in the Texas property market you have to add value-added inputs.

The housing market becomes more stable and thus less risky, capital returns are lower, thus operating yield needs to be higher as a % (but are still lower in real $ terms than NZ because of the lower price). Banks require greater deposits to reflect real skin in the game by purchasers but again this is still less in real terms than NZ.

Everyone is better of - and the speculators follow the speculative market like start ups, hoping to invest in the next Apple etc.

People in Texas have mortgages, but the mortgages don't 'juice' the housing market.

One of the primary drivers of the Texas housing boom in 2021 during was the historic low mortgage rates that emerged in response to the pandemic. The Federal Reserve lowered interest rates to stimulate the economy, making borrowing cheaper for homebuyers. This encouraged many people to purchase homes, leading to increased demand in the housing market.

If the Fed admits this, surely you must.

https://www.dallasfed.org/research/swe/2022/swe2202/swe2202f

No, it’s 100% due to land use policy

sarc

The article lists 6 reasons that accumulated after a disaster(the pandemic) but you put it down to only one as the reason.

And shock horror, they rise to the catastrophic median multiple of 4.7 (and now on the way back down).

NZ best efforts in non disaster times in the last decade plus has been nearly double that.

The article also misses the 7th and main reason in that people's activity was heavy restricted during the pandemic and thus supply was limited even when the capacity was available.

Low interest rates do make more people want to buy houses as it now becomes more affordable, but there is very little to no correlation in truly free markets in making house prices to rise.

In restriction land use places like NZ any saving (relative to the previous high prices) with low interest rates is only captured briefly by the first in but after one build cycle this feeds back into the supply shortage it created and now make the housing unaffordable again for new purchasers going forward even at the new lower interest rates.

In a truly free market, ie with less restrictive land use policies like Texas, whatever extra demand interest rates may cause they just build the supply to match, (exception of a pandemic aside)

In NZ lowering of interest rates allows the 'juicing' of speculative non value added gains, in places like Texas(a pandemic disaster aside) they don't.

And it was worse in real terms in the likes of California and that is why Texas had a huge internal emigration especially from the likes of NZ like very unaffordable California.

Ummmmmm minimum wage in California is double that of Texas

And San Francisco and LA have far less flat land in their immediate hinterland than Houston does

And the Californian wage is still not enough to compensate for the higher cost of housing.

California lost more people than it gained in the last 12 months the first time in its history.

And most of the outflow of people and jobs is going to Texas.

At the end of the day, workers in Texas have more disposable income, which is alot easier to do when you are only paying 3 to4 x median multiple for housing.

Houston was build on marshland.

With the right land use policies, any negative on the land, is a cost against the land, ie it can be bought cheaper.

The evidence for the difference has been shown to be almost exclusively due to land use policy.

Can you please provide some evidence? Academic, peer reviewed.

What? You can't do your own 30 minute Google search?

The Academic peer review trope is for those that refuse to look at the past and current evidence.

But here is some Christmas reading for you in order of ease/summary of readability.

1. Demographia 2024 housing affordability report.

2. Order without Design. Alain Bertaud.

3. NZ Productivity Commissions report into Housing.

4. Urban Valuation in NZ. R J Jefferies.

5. Anything by Alan W Evans

6. Wealth of Nations. Adam Smith

They all cite sources.

The first two are completely rabib ‘small government’ ideologues that garner little respect beyond their own very small circle of ideologues.

I am pretty well read on this stuff, and once gave the ideology more credit than it’s due. I won’t deny that Texas’s land use policies have helped deliver more affordable housing. The benefits are there to see. However, negative externalities and costs of those policies are never acknowledged by the ideologues. Very jaundiced.

I also think it’s incredibly naive to think that the benefits of the Texas system could be replicated here, even if it were possible to exactly mimic their system. There are so many differences (geographical, environmental, cultural, economic, political) that are critical beyond the actual land use policies themselves.

But I won’t waste any more energy at this point. It’s a futile conversation!

The Demographia report is quoted by the world bank, and by both National and Labour.

And having developed both in Texas and NZ and having studied this for nearly thirty years including doing comparisons with NZ subdivision budgets I can easily show that if allowed to be done the way they used to be done on NZ, and with the Texas method then it is easily do able, if policy allowed.

We used to have a median multiple if 3, exactly as Texas did and is still close to. It's not their system, it's the universal supply equalling demand system that we use to do as well.

Of course many people don't want this to happen, you as one of many, as the biggest externalities they fear is the loss if equity or the potential for speculative non value added capital gain.

This present Govt. policies are on the right track to help reverse a dysfunctional land use system which has seen capital diverted into non value added growth.

And then we wonder why our GDP is so poor.

And your counter to provide affordable housing is what?

This is just a garbage pep talk to throw useful idiots into the ponzi so their leveraged investment is protected.

Imagine this attitude with trading or building a business.

You’re faced with a critical decision that could make or break you financially for the rest of your life, odds are no better than the spin of a roulette wheel and your approach is….

tHosE thAT Do, Do! Aaaannd, it’s gone.

How about those that calculate, win?

You're definitely a 'doer' as you have several million in debt which means you must have a lot of assets and equity to cover it. Business and investment properties?

by Murph777 | 7th Oct 24, 1:53pm

So glad I fixed for 5 years at 2.99%.

Several M all rolling off Mar 2026.

Was pure greed that stopped people from fixing at the lowest rates ever....

Same but not the same. I'm not forgetting that cost of living is still way up with shrinkflation, and cheapflation, where the cheapest goods and services have been hit the hardest by inflation, are still biting hard.

Auckland house sales 2003: 72,000

2018: 37000

2023: 32000

Would be great to have a trend line.

Cannot see how first home buyer affordability has improved at all today since 2021 given... The OCR rate today is much higher , Rents, Insurance and rates are much higher, Wages are likely flatter and the job market wounded, Food /fuel prices are out the door, ... the idea of a 25 year mortgage is somewhat historical Marxist thinking , more likely the new average term being 30 years...its all smoke and mirrors and firing the fog cannon wont work this time ....I doubt if even a very low OCR will spark a frenzy. 2025 will see more stock added to the unsold pile .

Affordable. More Affordable. Perhaps unaffordable and less unaffordable are more appropriate words. The cost of the housing/banking/council sector is likely completely unaffordable for the nation as a whole. That is why we are in recession and may progress to a depression. How can you have a viable economy with this huge over burden?

Who read / remembers this: How much do investors drive house prices?

I emailed David for a copy of his thesis which I promptly received. (Subject to a NDA so I can't share the detail here.)

It concludes (using my words) that investors in the Auckland market are inclined to over-price houses largely due to an over-estimation of capital gains (e.g. "doubles every ten years') and an under-estimation of costs/risks, with the over-estimation of capital gains becoming self-reinforcing in the terms of the overall market ... which results in overall house price escalation.

It's a thoroughly interesting read. And agrees with similar'ish studies I've read done for other places overseas.

CN, HM et al, if you want a copy, email David.

One wonders if a CGT - even a low one - would force 'investors' to look far more closely at the assumptions they've made about their future capital gains.

On a side note - and JFoe will hate this as he's not a fan of behavioral economics - David's paper mentions a concept called 'bounded rationality' in investment decisions. (Bounded rationality is a human decision-making process in which we attempt to satisfice, rather than optimize. In other words, we seek a decision that will be good enough, rather than the best possible decision.)

Or put another way, we only attempt to beat TD interest rates and no other options enter our decision making process. Thus, we don't look for other investment options that would maximise our returns. (I teasingly call this as property 'investors' as being 'none too bright'.)

Would real economists do this? (Most of the ones I know don't - except as a minor part of a balanced portfolio'.)

But this 'economist' does. It's the only investment option he ever talks about.

Wow, that 'economist' is a genius. Doing exactly what multiple American-run seminars were telling people to do in Auckland, circa 2002 (and it wasn't new then - but pay your ticket and you'll have NZ's tax law that makes property speculation oops I mean investment explained to you). And voila by 2006 Auckland was recognized internationally as in a property bubble, and then a generation of Aucklanders started using their capital gains to spread the malaise further afield.

At the time I thought it was unethical - enslaving fellow humans to pay your money-rent by denying them opportunity to do otherwise, but history shows I am a tiny minority on that one.

All that, is endogenous to urban land supply conditions being changed by Councils. It is like smoking; it would have been best not to start. Then year after year, things get worse and worse and we completely forgot what kicked it off; we just blame the endogenous phenomenon of speculators being attracted to a market rigged perfectly for Ponzi. Hugh Pavletich was right early on. This site never seems to improve in the focus of its comments on where the problem started, and where it starts everywhere, representing a slam-dunk causation.

Land use policy .. tax policy .. it's not necessarily either-or is it though?

We should probably add in banks being allowed to create credit out of thin air as well (would State Advances allow leveraged purchase of investment properties - I'm not old enough to know)?

I'm probably a bit simple, but I think it boils down to the age-old sin of greed.

Yeah, human nature. It's "just the way things are, that I can sell this land for x,000,000 dollars".

But monopoly economic rent in land and housing was a problem back when money was gold. Karl Marx and Henry George both had "solutions" for it, and they didn't involve stabilizing money supply, because it didn't need stabilizing back in their day. Virtually no economists disagreed with their analysis of the problem; it was just that their solutions were untenable according to the morals of the time, except in some countries where the Marxist revolution happened. Sadly, the problem was resolving itself, as Alfred Marshall argued that it would; by superior transport systems making the supply of resources superabundant compared to when all transport for supply of necessities involved draft animals. The same thing happened in housing when affordable automobility became a thing - Henry Ford knew what he was doing, he was probably more significant in his time than Elon Musk is today. It is central planners today drawing lines on maps about where housing is allowed, that have sabotaged the beneficial resolution of monopoly rent in housing by automobiles.

It should get even better next year as interest rates drop more and house prices continue to ease back. Too much on the market and still pouring on. So many people leaving NZ including well qualified professionals and tradies looking for higher incomes, lower costs of living, cheaper housing and better politicians. Luxon is less inspiring than Jacinda and she achieved very little as PM.

It will simply be jaw dropping if this side is as poor.....

I can see civil unrest occurring.

Things were bad enough back in 2014. Sad that we are still faffing around painting smiley faces on a horrific situation, because things aren't quite as bad now as they had got to 3 years ago. They are still much worse than 2014, and 2014 was unacceptably worse than 2009, and 2009 was unacceptably worse than 2003.

House price multiples really do matter

September 7, 2014 | Sunday Star Times (New Zealand)

Page: D017 | Section: NEWS

By Phil Hayward

THE NZ Property Investors Federation claims that median multiple ratios are too simplistic for assessing housing affordability. A chart published in August 17's Sunday Star-Times - "Tracking Mortgage Affordability" - includes interest rates so that a large mortgage at a low interest rate appears just as affordable as a small mortgage at a high interest rate, such as was the case in 1985.

But older generations who remind us how tough they had it in their day need to apply a bit of maths and scepticism, and start sticking up for the young folk.

Because the interest rate generally correlates with inflation and hence nominal income growth, it hardly matters what the inflation rate and interest rate is. It can literally be stated as a kind of general rule:

House price multiple 3: total share of 25 years income required to pay off a house: 10 per cent

House price multiple 6: total share of 25 years income required to pay off a house: 30 per cent

House price multiple 8: total share of 25 years income required to pay off a house: 40 per cent

Using the NZ Property Investors Federation's own example: in the case of prevailing mortgage interest rates of 18 per cent, incomes are likely to be rising at least 12 per cent per annum. By the end of the 25 years, the total cost of paying off the house, will have been 9.8 per cent of the total income.

In reality, either the buyers will have paid the mortgage off much more quickly because, by year nine, their annual income will be more than the remaining principal, or, as happened in NZ, inflation will have fallen, and so will interest rates. Either way, the outcome is very happy. If you do the maths for any scenario, the total proportion of 25 years of household income will be stuck at below 10 per cent.

But the 2014 house purchaser with the mortgage interest level of 6.3 per cent is likely to only enjoy income growth of 3 per cent per annum, so that by the end of the 25 years, their total cost of paying off the house will have been 36 per cent of their total income. Again, there is very little variation in this under any scenario where interest rates and income growth both move in tandem; but it gets worse - with interest rates at 6.3 per cent versus 18 per cent, the chances of an interest rate increase that is immediately catastrophic for the household are very real.

In fact, households are left far more vulnerable to financial reversal of any kind during a much longer period; sickness or injury of either breadwinner; or of one of their children; a child with a disability; loss of employment; a natural disaster; being the victim of a crime; an increase in interest rates - a whole host of scenarios that tend to affect a certain proportion of the population during their lifetimes - will tip a much higher proportion of households into bankruptcy during that lifetime.

Professor - now US Senator - Elizabeth Warren calls this "the coming collapse of the middle class".

But there is cause to complain about the median multiple as an affordability measure. When urban land costs inflate, while the median multiple house price may rise to "only" 7+ (from 3 as recently as the 1990s), the house price distribution is changed considerably, the bottom of the market being eliminated.

Eventually, increasing numbers of Kiwis will go into retirement as lifelong renters with no home of their own free of encumbrances and ongoing charges.

Phil,

Great article. Thank you for sharing for those of us who have not seen it.

"THE NZ Property Investors Federation claims that median multiple ratios are too simplistic for assessing housing affordability."

Remember, the NZ Property Investors Federation is a lobby group for their members - non owner occupier owners of real estate.

They have their own vested financial self interests and will lobby to protect those vested financial self interests.

The housing affordability issue is going global.

https://www.wsj.com/economy/housing/housing-affordability-crisis-europe…

Thanks, I agree. There is more to the story. Within weeks, that article had vanished off the online page it was on, and even off Pressreader. Editor Rob Stock, who had been interested and graciously ran the article, simply didn't reply to my emails asking what had become of it. I really should have taken it further at the time, put it up on some alternative media site with a question "why was this vaporized by the SST"?

I recently did engage the help of a research assistant at a public library to see if it could be found. There actually is some kind of backdoor website for NZ media articles that still holds a copy of this. But no-one will ever find it via Google. Even searching that backdoor site itself doesn't bring it up; you have to know the date of the paper and the page it was on, literally. This is the first time I have put it back out in public.

I had a run of pieces published in the NBR too at about the same time and then they went cold too. Form your own conclusions.

It's a great article, Phil. And this comment explains why I've only just read it.

re ... "Form your own conclusions." No need too. I know how much MSM's "real estate news" is funded and supplied by RE interests.

"I had a run of pieces published in the NBR too at about the same time and then they went cold too. "

Don't know what you're allowed to repost regarding these articles, but I would be interested in reading them.

Either on your own social media profile or in the comments section here.

Elizabeth Warren calls this "the coming collapse of the middle class"

A controversial figure to say the least. On the surface, Warren seemed to be fighting the good fight in the jihad against Wall Street. In recent years, while maintaining her critical stance, Warren has also engaged with Wall Street figures who support her regulatory agenda, indicating a nuanced approach. Her influence within the Biden administration, through appointments of allies in key financial roles, reflects a strategic shift towards integrating progressive policies into mainstream governance.

So while she appears to be on the side of the great unwashed, many are skeptical. For Warren, centralized power and control are the basis for which she presents her case. Even if that means siding with the likes of Jamie Dimon and putting puppets in place like Gary Gensler at the SEC.

As an aside, those who rally against climate change while using private jets for their own convenience. It looks like hypocrisy. Bernie Sanders is similar.

Ah, I certainly agree there. Bear in mind this was published in 2014 when she was still more highly regarded, especially for that particular insightful commentary. Even then I was a bit suspicious of her being a Democrat but that particular analysis was a great piece of work. She actually admitted that free markets had made most common consumer goods more value for money even as housing was going the opposite way. You are quite right that she is unrecognizable now as the kind of politician who would support anything effective being done about this problem. Probably even back in 2014 she would not have admitted that the problem in housing is regulatory distortions to the market for land for housing.

Her policies back in 2014 - when she was a minor firebrand - would have lost most the Dem's billionaires backers. There was never any chance of her carrying these policies to the highest levels. Her only chance at the highest level was to do as Bernie Sanders has done and raise money across the entire USA through lots - and it is a lot - of small donations from ordinary people who are sick of the USA being engineered for the very rich.

Just as an aside - I see it as a mathematical impossibility for the US middle class not to be gutted with their current settings. It simply becomes as question of how much longer it will take.

Her policies back in 2014 - when she was a minor firebrand....

You might want to do some research on who Liz Warren is. Warren was chair of the Congressional Oversight Panel, established to oversee the implementation of the Emergency Economic Stabilization Act (EESA) and responsible for monitoring the use of funds allocated through Troubled Asset Relief Program (TARP), aimed at stabilizing the financial system in the GFC. She was the key person driving the establishment of the Consumer Financial Protection Bureau (CFPB) in 2010.

Warren has been influential in US politics and the Dems since that time. And she doesn't rely on corporate lobbying / funding to run her campaigns. She's similar to Bernie Sanders

Spare me the pomposity, J.C. I know exactly who she is. My 2014 assessment stands. She was just one among 50+ at similar levels and below perhaps another 50.

"As an aside, those who rally against climate change while using private jets for their own convenience. It looks like hypocrisy. Bernie Sanders is similar. "

I always chuckle when I read such thoughts.

Tell me - Would it be more energy / time / $$$ efficient to have all the people who wish to hear or talk to them visit them in a static location?

Or maybe you're suggesting they should use ordinary airline services which would result in fewer engagements but at far larger venues meaning many more people would need to travel larger distances to get to these mega-events?

A relatively simple spreadsheet can answer these sorts of question ... It is such a shame so many use primitive heuristics to answer what isn't a very complex equation and make fools of themselves in the process.

Tell me - Would it be more energy / time / $$$ efficient to have all the people who wish to hear or talk to them visit them in a static location?

More energy would be spent for the masses to move to Liz Warren. Regardless, the hypocrisy claim still stands. What makes her any more important than anyone else? Is leading by example demonstrating the appropriate behavior not her modus operandi?

Remember, Warren regularly rallies against the wealthy and said she is 'tired of freeloading billionaires' and accused a Trump official using taxpayer's money to fly on private jets

If she were so committed to her cause, she could soapbox and present from her own office and / or home and reach larger audiences than by flying in a plane to a rally. The technology exists.

Check out this corruption, laid bare, within the National party. Its no wonder land prices are so high with this sort of cronyism going on:

https://www.reddit.com/r/auckland/comments/1hgonlb/cronyism_at_its_fine…

I don't understand why this isn't front page news, why any major news outlet isn't covering it. Arena did almost all the work for them.

Yes I have mentioned this several times before. Certainly cronyism, bordering corruption.

Thanks for sharing. Arena is impressive. And she knows her stuff, or at least properly does her homework, unlike most politicians. I say this as someone who knows a lot about land development.

I've noticed media reports lately of Chris Luxon selling more than one of his properties. When property prices come down, whether or not the Bishop reforms are the cause, the usual suspects will probably blame Luxon for "insider trading" when all he is actually signaling is that he believes the reforms will work, which are well and truly public knowledge and if anyone doesn't believe they will happen and doesn't believe that they will work, they have only themselves to blame.

With respect, Phil, take care with 'recency bias'. The reforms, and probably the major ones, began way before this government's term. (Here's a good example.)

With regards Luxon's actions, I suspect he's read my posts (humor), or many from others like mine, that conclude NZ house prices are likely to flatline in real terms for a decade or more as the numerous 'supply restrictions' imposed by local governments have been removed, or lessened. We have central government to thank for this. And by central government, I include many of the so-often-despised bureaucrats that survive for longer than any government does.

The recency bias is plain to see in most present councils inability to process central Govts. Land use intent.

It is hard to determine whether this is due to councils legally not being able to comply ie they are caught having to operate between old and new legislation that maybe contradictory, or they have a certain contrary ideological bias so they are deliberately resisting using whatever means possible.

Whatever the reasons, councils are not expediting development at the speed the legislation would appear to offer and is needed for supply to meet demand.

Or there are other reasons?

"Or there are other reasons?"

A lack of ability to provide infrastructure may be the greatest barrier....and no method to improve that fact. We are still essentially operating a system that was developed to serve 3 million and not terribly well at that, and on top of that theres been 30 years of maintenance neglect.

Blobbles,

Fantastic share. Auckland Council rate payers are being left out in the dark on this.

So Auckland Council pays millions more for the land and one company benefits.

Also, unlike a plan change where development contributions can be negotiated as part of the process (80k per dwelling in Drury) so that council can recover infrastructure costs, that will potentially be much harder on this one since it is a process not run by council

Exactly and that company is partly run by former National party members and big donors to the National party this time around.

Fascinating how if you are poor, National want to absolutely ream you "cos there isn't enough money coming in, due to recession", but if you are a rich land owner already "Here's a huge trough of public money, dig in!".

Absolute shocker, but NZ is "one of the least corrupt countries on earth", don't you know it.

I don't understand why this isn't front page news, why any major news outlet isn't covering it. Arena did almost all the work for them.

Not surprised to see Stephen Joyce involved in this grift. Would have thought that with the Waikato University sham (which will achieve nothing), he might have cleaned up his act.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.