Affordability is starting to improve significantly for aspiring first home buyers thanks to a combination of falling house prices and declining mortgage interest rates.

The Real Estate Institute of NZ's national lower quartile house price has declined slowly but steadily for the last four consecutive months, from $600,000 in March to to $570,000 in July and is now down by $100,000 from its November 2021 peak.

In Auckland, the country's most expensive and least affordable region for first home buyers, the lower quartile price has declined by $55,000 over the last four months, dropping from $815,000 in March to $760,000 in July.

Auckland's lower quartile price has now declined by $206,000 from its November 2021 peak of $966,000.

The lower quartile price is the price point at which 25% of sales are below and 75% are above, representing the lower priced end of the market, which is usually of most interest to first home buyers.

However first home buyers are currently receiving a double benefit, with mortgage interest rates also on the slide.

The average of the two year fixed rates offered by the main banks peaked in its current cycle in at 7.04% in November last year, and has since fallen steadily to 6.50% in July.

That combination of lower prices and lower mortgage interest rates brings several benefits to first home buyers:

- The amount they need to save for a deposit is reduced.

- The don't need to borrow as much.

- Their mortgage payments are reduced.

All of that means their chances of getting into a home of their own are considerably improved.

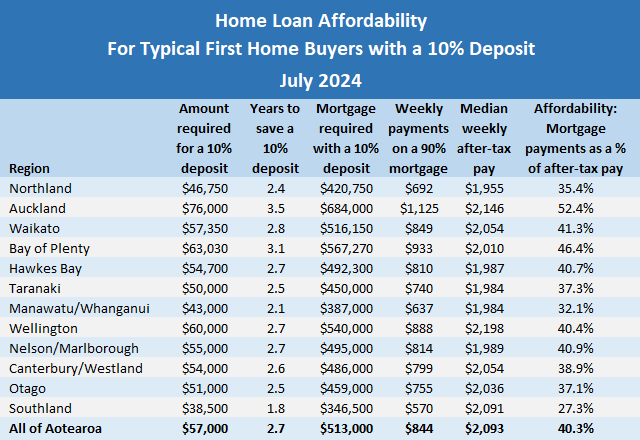

For someone looking to buy a home at July's national lower quartile price of $570,000, the amount they would need for a 10% deposit would have declined from $60,000 in March to $57,000 in July, a saving of $3000.

Compared to the price peak of November 2021, the amount needed for a 10% deposit would have declined by $10,000.

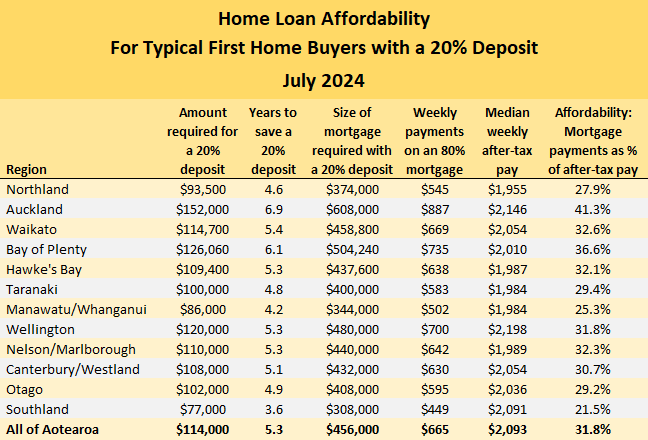

Of course you could double those figures for a 20% deposit.

The amount first home buyers will need to borrow is also less.

To buy a home at July's national lower quartile price with a 10% deposit would require a mortgage of $513,000, down from $540,000 in March and $603,000 at the November 2021 price peak.

But probably the most noticeable impact all of this is having is on mortgage payments.

For someone buying a home at July's lower quartile price with a 10% deposit and a mortgage at the average two year fixed rate of 6.5% and a 30 year term, the payments would be about $844 a week compared to $911 a week back in March, representing a saving of $67 a week.

If they purchased the same home with a 20% deposit the equivalent savings on the mortgage payments would be $54 a week.

So at the moment, the market is moving in first home buyers' favour.

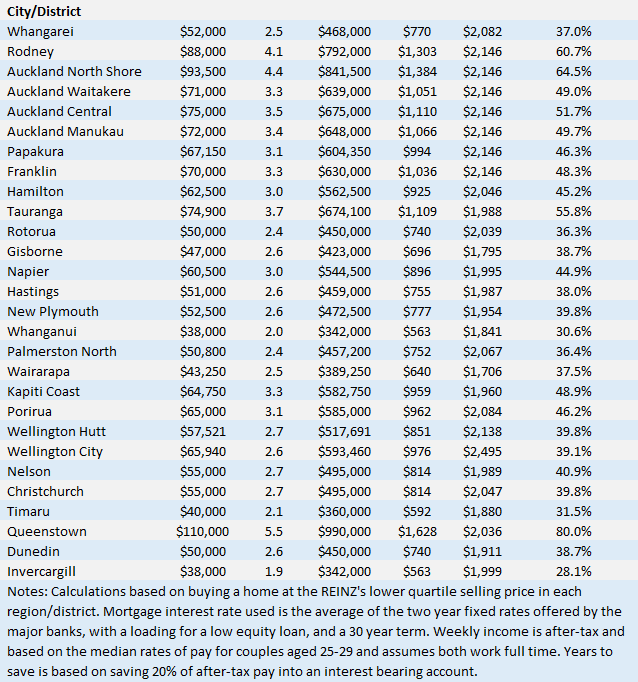

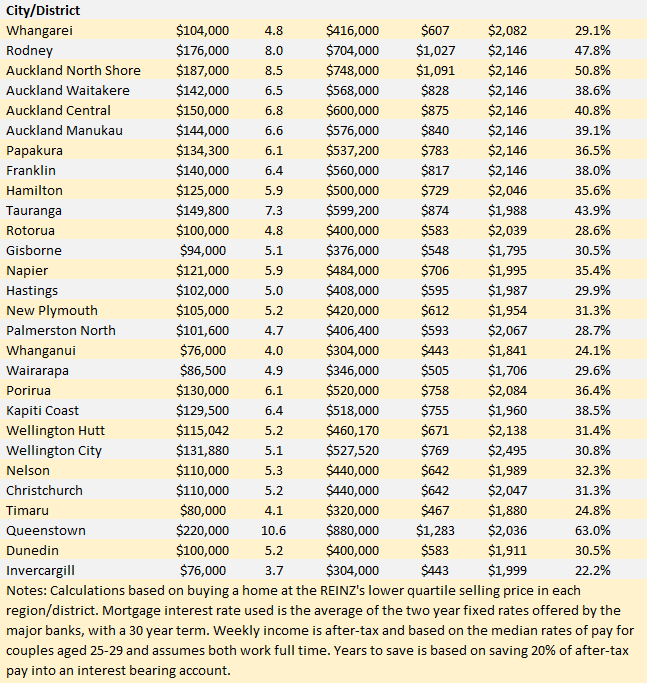

The tables below display the main measures of affordability in all of the main urban districts around the country, for typical first home buyers with either a 10% or 20% deposit.

- The comment stream on this article is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

80 Comments

GDM's "ahhh but 30 years ago you could buy a house for 1.5 x annual wages".

30 years ago was a lot different to today. Would you rather live 30 years ago or today?

I say today

30 years ago - All the councils were run by real people, not wannabe politicians! It was blissed then.

Oh.. no bloody leaky homes either!

Still plenty more Rimu etc to be used for everything. Breaks my heart to see people ripping out such immaculately made wooden kitchens these days in favour of some tasteless blank white or black euro-style thing that they'll get over in 2 years.

I actually love my kitchen to be built with ply-wood. We stayed in an AirBnB in Kanazawa with plywood kitchen.. beautifully made by Japanese tradies.

Pulled up 2 layers of flooring in our Kitchen recently (blue tiles laid over top of some patterned vinyl from the 60's) to expose the original Rimu. The rest of the house (except for an extension) has Rimu all through.

Why can't things in society get better without there being a converse & adverse impact elsewhere in something completely unrelated?

I.e. yay we have flat screen TV's and Uber Eats, but as a trade off house prices must be 10 - 15x the average annual salary.

What part of the various societal improvements suggests house prices must be where they are? As televisions became cheaper to make, mortgage rates had to fall???

It's the nature of economics. As the great Thomas Sowell says, "There are no solutions, there are only trade-offs".

The "societal improvements" you mention above are technology related. Technology is intrinsically deflationary, and there's nothing an economist hates more than deflation - so interest rates go down to keep the average inflation at an acceptable level. Hey presto, real assets inflate in dollar terms.

Just one example, but that's essentially what we've been doing for the best part of three decades.

Is technology actually deflationary? How much did people spend on computers and cell phones in the 1980's vs today?

Their price point might deflate, but from a consumer perspective if someone who has not owned a TV or gaming computer decides to buy one (because the price has "deflated" to where it makes sense for them to buy), is that not an added lifestyle expense therefore inflationary?

Technology may have had some benefits, but the impact it now has on our youth and our general level of sociability is arguably negative all round.

The "societal improvements" you mention above are technology related. Technology is intrinsically deflationary, and there's nothing an economist hates more than deflation - so interest rates go down to keep the average inflation at an acceptable level. Hey presto, real assets inflate in dollar terms.

You understand well young Jedi.

Consistent with Jeff Booth’s “The Price of Tomorrow: Why Deflation is the Key to an Abundant Future”

Exactly. Also to add to that, there have been lots of improvements in other ways that get capitalized into land prices. Better infrastructure, more amenities (many neighbourhood shops offer far better choices than the 1-2 dingy chinese takeaway/fish&chip joints of yesteryear), lower crime rates all get capitalised into property prices.

The technology you're referring to also gets capitalised into land prices. Ubereats doesn't help you if you live in the woops. But it does increase the value from being located in Ponsonby...

The technology you're referring to also gets capitalised into land prices.

Nonsense. Land prices are a function of money supply and credit creation. In fact, the the credit creation mechanism is the whole basis of the Ponzi.

Nothing to do with the deflationary benefits of technology.

Nothing at all....the whole system cannot function in a (truely) deflationary environment.....we simply move the inflation impact.

The ultimate trade off, we’ve traded cheap basics for cheap luxuries. The real question is how much cheaper can any of these luxuries really get? In real terms a brand new TV is about a tenth (a bit less than a tenth but being rough) the cost of one in the 80s, and that has freed up a lot of additional spending capacity for debt. If tvs are a tenth as cheap in 40 years time, will that have the same impact on our economy? Ie if GDP was an 8th the size it is today, what spare capacity would we have for the current size of private debt?

Living standards are meant to prove from generation to generation. Costs has fallen across most things in many other countries, e.g. a large part of the UK, costs of food, TV, housing, banking, travel have all come down across the board. The standard of living there is a heck of a lot better than it was 30+ years ago, it has actually increased, people just have more spare cash pump back into the economy and go on holiday, save into pension and so on. This idea of things having to balance out is a total myth, i.e. if you spend less on TVs and clothing then your spare money must be going more and more into housing - perhaps that's what some in NZ tell themselves to feel better about the current situation

I'd say that you were probably still in nappies then. 🙄 Bring back the 70's!

You can keep the 70's.

Choice of white or brown tiles.

Three TV channels.

Getting canned at school. (Regularly)

10pm and Sunday closing.

Compulsory to be drunk too drive.

Muldoon.

But also!

Flares

Disco

Pink Floyd

Hydro schemes

Motorways (surely they were cool when they were novel and new?)

CNG cars to go on the motorway (so long as it wasn't a carless day)

An active space race

The USSR showing you an alternate reality in which tiles are only grey and the state chooses that for you

Just because I wasn't born yet doesn't mean I can't be nostalgic about it all. In the 70s my mother bought a house in Brooklyn for $20k and paid the mortgage from her part time job while she was at uni if that helps?

I'm talking about NZ. The arse end of the world. USA and Europe were completely different.

1 TV channel

Yet multiple times better content in one channel than across the multiple channels today

What has any of that have to do with economics?...aside from the fact it is inaccurate

But Rookie, 30 years ago you would have been well on your way to building a retirement property portfolio. In this day and age you're just a rookie spruiker

Its easy to trade the left hand side of the history chart

yearightmate, I would have been a rookie 30 years ago also, that wouldn't change.

I don't dwell on what I don't have, or could have had, I worry about what I can do now and tomorrow, take a lesson from a rookie ;)

I'm quite happy with what I have.

Thirty years ago I was flatting and life was pretty good. It was easy to find a place to rent and it didn't take too much of my average wages. Tertiary education was free and 25-29 year old couples could afford to buy a house without needing flatmates and they could more easily afford to start a family. Buying a house earlier also means it's paid off quicker and people can save for retirement sooner. Gangsta's Paradise was just a catchy song, now it's a book about the rise of gangs, drugs and other social problems in NZ. Saying that though, any day is a good day to be alive.

Gestational Diabetes (GDM) is certainly a risk for any young couple planning a family and trying to purchase their first house......

The Rookie Spruiker can't even get the insults right.

not everyone feels they needed to insult people with differing opinions, I found mostly insecure people do.

And yet the first word of your comment was a botched insult ... insecure and incompetent?

What are you referring to?

30 years ago you could still smoke in pubs. You could have fun on the terraces at Eden park without getting locked up, taking risks was a personal problem, I had hair, fixing things yourself was the norm, bought 3brm house in onehunga for 123k, household income was 45k. Wife stopped working when we had kids. Not being nostalgic, well maybe a little bit, but life was a lot freer then.

And there was still no such thing as anti-social, social media. Everyone had a girlfriend, and no got murdered..

Yes, I'd go back 30 years ago any time. Cheaper houses, more peace in the world, better music, no Ai taking away human jobs, etc. Yes, technology improved but the quality of life (in the west) decreased on average I reckon. I'd rather have a better life than more technology/gadgets.

Yes, I'd go back 30 years ago any time. Cheaper houses, more peace in the world, better music, no Ai taking away human jobs, etc. Yes, technology improved but the quality of life (in the west) decreased on average I reckon. I'd rather have a better life than more technology/gadgets.

Great news!

Why do you keep up with the age 25-29 assumption when the average age of a FHB is now greater than 35?

Because if you can't assume 30 year mortgage terms then the narrative isn't as rosy 😉

Banks happily give 30yr mortgages to 40yos. They know most people will pay a mortgage down faster than the maximum term, particularly after a few more years of career progression and accompanying pay rises.

Stuff appears to be reporting another BNZ rate drop.

Edit:appears stuff is just several days behind.

What happens when the prices of all things are going up? Interest rates rise to temper price rises.

So what does interest rates doing the opposite, falling, reflect? Prices.... are falling. (See Market Interest comment above)

The lower rates go, the more the expectation is of Prices Falling. (NB: And the Riskier new lending is. We've just had a trial run over the last 2 years of what happens when lenders lend low. When % rates subsequently rise, those who are freshly indebted struggle with the higher repayments. And yet, here we are. Doing it all over gain)

It's the only game there is...think of a bouncing ball on a table - up and down, each time the rise is slightly less, eventually the ball will just roll, roll off the edge of the table (into negative rates) and bounce once again on the floor, but...again, eventually the ball just rolls, rolls on the floor and eventually stops. Game over.

You've obviously never owned one of those wonderful little rubber balls that manages to bounce twice as high as the height you dropped it from, defying most laws of physics. One bounce off the floor and it's skyward!

There is no ball that bounces higher than the height you dropped it from, basic physics. If there were it would eventually bounce out of the atmosphere.

I think you have your cause and effect a bit mixed up. The RB raises interest rates to (in theory) stop price rises. When things stop rising excessively they can lower rates.

Perhaps you better go tell stuff that tasty cheese hasn't hit $20/kg after all, since according to you prices are falling.

Politicians, bankers economist etc underestimate the potential to reverse the brain drain and have a happier more socially functioning society by gutting house prices.

I believe unaffordable housing and the financial stress flowing from it is doing more damage to NZ than any other factor.

And we spend billions on the symptoms... being crime, subsidies, hospitals, mental health, racial disharmony and so on.

Will they ever wake up?

The funny thing is that karma is coming for the boomers.

Why would a smart kid, just graduated... stay in nz vs Au/uk/USA vs where they have better opportunities, higher salaries, more to do, cheaper houses and better to raise a family etc. And those kids are in great demand.

So our boomers price the kids out by keeping house prices high. and then complain the public services and infrastructure is crap and their rates as pensioners are too high.. and soon they will have to be taxed on their wealth and super calculated based on wealth as all the taxpayers are gone and noone is left to run the place or pay taxes as needed to fund their super. Added to which will be the crime where the dump kids that remain are robbing them blind. Healthcare is getting awful and public transport sucks.

Karma. We and our kids are off as soon as their education is done. What's to stay for here? It's like a real sad country now with not much to be proud of

The older investors in nz don't get the need for balance. Money vs lifestyle etc.

So how does Karma work for those who don't pay their way in life OSE? Like reading and commenting on Interest and not contributing ?

I read and comment on Interest but I'm not "contributing".

I could cancel one of the monthly payments I make to half a dozen charities and put that towards a PressPatron account to appease the Karma Gods. Your thoughts?

If things are really that tight NZD, and I don't believe they are, I will pay for your monthly contribution to Interest. Just say the word. It's a triple win, Interest gets more $, you get to read ads free and a green tick and I get to help.

Thanks for your concern, things aren't really too tight at my end. Some of us don't mind the ads and find other things to spend the $10 each month on. It's a personal preference and priorities thing you know? But certainly not "bad karma" inducing either like throw away lines such as "what storm?".

It's great to hear that things aren't bad at your end. So why don't you contribute? Do you think David Chaston and his team's work are not with rewarding ?

Calm down Yves... you're taking the hall monitor role far too seriously.

I was seriously considering contributing until someone under the moniker "Yvil" came on here trying to shake everyone down at the door.

Painting us as ungrateful for the content and making us out as freeloaders.

Has David's team put you here to do this to try drum up contributions?

So you were considering contributing for the last 6 years and 11 months… but now that I press you, you suddenly changed your mind, is that right? Grow up and stop the BS.

No, David or his team have absolutely nothing to do with my call for helping Interest.

Nope, since I got my last pay cheque with an $80 per month tax cut I figured hell what's $10 per month out of that, it would've historically gone to the tax man.

Good content aside, why would I want to donate to a site that allows a pretentious fella like you to go around continuously berating people for not donating?

Do you have share in interest.co.nz, Yvil?

Why so uptight about paying subscription fee? It's option FFS, or they can adopt Newscorp model and make everyone pay if the contents are newsworthy!

My post are in reply to those that complain that things aren't fair, whilst not contributing, I think that is very hypocritical.

Hey Yvil,

you can pay my subs next year. I'll cancel now and let David and the team know you'll be picking up tab for me at renewal time.

Cheers.

My offer wasn't for you.

Take your pills

Contribute

My offer wasn't for you.

Oh dear, it looks like you just cost David a subscription. Never mind old chap.

They own about 3 houses each on average. No wonder they are out of touch with real public sentiment on this.

I have been saying this for a long time but often get labeled as "just being negative". Unfortunately there are some who couldn't care less how bad things get, as long as they are making money.

I've said it before and I will repeat, narcissism is the new pandemic and we don't have a vaccine yet!

The Scrooges... I think most investors must enjoy seeing the rest of society suffer.

I find the term dgm high amusing ... coming from those that spend their lives causing Misery for the many just to make some money in an easy way.

Do you mean yourself, taking advantage of David Chaston and his team's excellent work for free ?

Smudge: "I've said it before and I will repeat, narcissism is the new pandemic and we don't have a vaccine yet!"

The vaccine comes in the form of a green tick, it will make you feel a lot better not being a freeloader, and it will help Interest!

🙄

by HouseMouse | 27th Aug 24, 1:00pm

I will return to doing so (contributing) , Yvil.

Good on you HM.

Green ticks certainly aren't preventing meaningless waffle.

So rewarding people for their work is meaningless waffle in your opinion ?

"feel a lot better not being a freeloader".. now this is a bit rich for those trading properties! It's a zero sum game...

The interest paid on your saving is more than the increase in the deposit required due to house inflation. If not it should be.

This is really good news.... do we know if they buy new build or established. Gosh the 3 high and 3 deep is going crazy in Te Atatu South.

7% but could also be 10, 12 or even +15%

https://www.rnz.co.nz/news/business/526296/2025-the-year-house-price-ri…

BNZ’s view close to mine.

What's good for FHBs is actually even better for 'investors' after this government's changes, i.e. 100% interest deductibility and on existing houses.

I feel sorry for FHBs. They just can't catch a break.

But wanna be LLs better take care ....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.