Set for launch in July, New Zealand's Depositor Compensation Scheme (DCS) means depositors at a failed deposit taker will be eligible for compensation of up to $100,000 per depositor, per deposit taker.

Interest.co.nz has previously detailed what will and won't be covered by the DCS. It is, however, important to note there'll also be a deposit product hierarchy policy that's currently being developed by the Reserve Bank (RBNZ).

The RBNZ notes in some cases, depositors may have total protected deposits with a failed deposit taker in excess of $100,000 held across multiple deposit products. In such circumstances under the Deposit Takers Act, the RBNZ has the discretion to; "apportion compensation across the protected deposits as it sees fit."

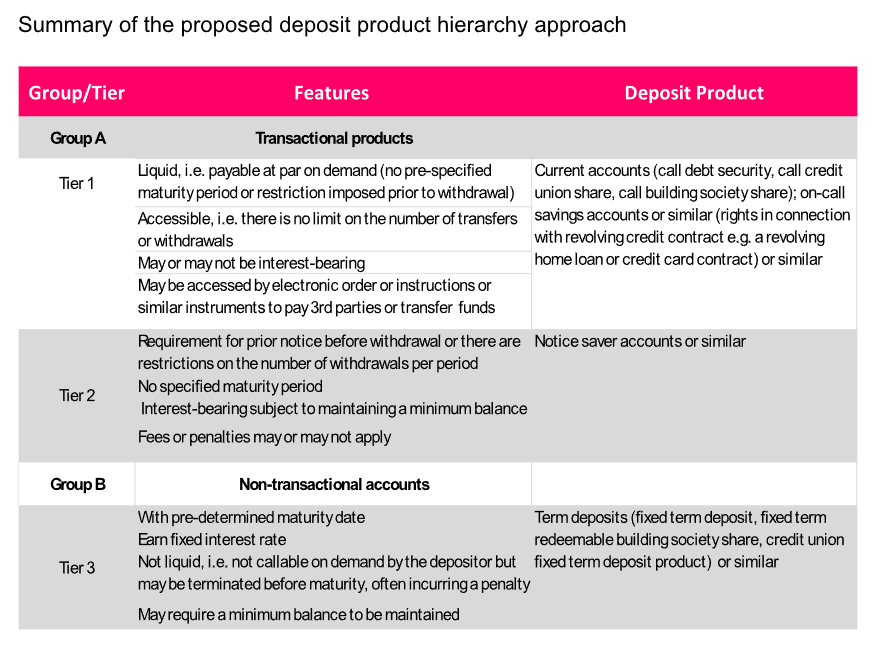

The RBNZ is proposing the introduction of a deposit product hierarchy policy. Through this, protected deposits would be grouped into tiers, or ranked in order of priority to enable the RBNZ to effectively allocate compensation across those protected deposits, it says.

"It is proposed that the product hierarchy will apply in liquidation, and payout, as well as in resolution, for example if Open Bank Resolution (OBR) is applied," the RBNZ says.

"The order in which compensation is apportioned across products also determines the order in which the RBNZ will subrogate an eligible depositor’s rights and remedies relating to particular products in cases where a liquidation and payout is undertaken."

So what is the proposed hierarchy?

Protected deposits would be placed in tiers, or ranks, based on liquidity and accessibility assessments.

"Liquidity refers to the feature of certain protected deposits of being funded at all times. This enables customers to have immediate access to their funds, sometimes on a daily basis. Inability to have access to liquid funds could potentially harm the depositor if they are unable to meet financial obligations or make purchases. Accessibility refers to whether there are restrictions or limits to the number of transfers or withdrawals that can be executed on the deposit account," the RBNZ says.

The table below summarises the RBNZ's proposals.

The RBNZ also provides an example of how the deposit product hierarchy could operate.

Depositor A has $75,000 in a current account and $50,000 in a term deposit with Bank B for a total sum of $125,000.

Bank B fails and depositor A is entitled to receive $100,000.

Using the deposit product hierarchy, depositor A is compensated

as follows:

♦ $75,000 from the current account (full compensation) and

♦ $25,000 of the term deposit (partial compensation).

This means that the current account is given priority over the term deposit.

Under the Deposit Takers Act protected deposits are comprised of the principal and any accrued interest as at a particular point in time. The RBNZ says it has the power to apportion the compensation between principal and interest, noting accrued interest is interest earned by the depositor but not yet paid out.

"We propose to prioritise the principal part of the deposit before accrued interest as this may involve less intervention or steps in the DCS calculation process, whether in liquidation or resolution, thus minimising execution risk. As such, accrued interest from all types of accounts would have a lower priority in the deposit hierarchy than Tier 3 deposit products," the RBNZ says.

The RBNZ has also floated alternative options to a deposit hierarchy policy. These include apportioning compensation on a pro rata basis across all protected deposit balances, and relying on reactive ad hoc arrangements. With the latter the RBNZ says it could issue an apportionment rule as it sees fit when a specified event notice is issued. This discretion could apply to a statutory or resolution manager when a deposit taker enters resolution.

The RBNZ says its preferred option is the deposit product hierarchy.

A spokeswoman says the RBNZ expects to publish a finalised product hierarchy policy document by June, which will serve as guidance for deposit takers.

*This article was first published in our email for paying subscribers first thing Tuesday morning. See here for more details and how to subscribe.

4 Comments

What is surprising is that with a little over 2 months to go they are still formulating policy?

Sounds so simple.

What about funds held on behalf, in say lawyers trust accounts, broker accounts, a family trust, real estate firms, a refund due, loans unrepayable and so on?

I expect they will either add some fine print to protect, or need insurance?

EQC payouts took forever, litigating this stuff will be a nightmare and lawyers dream in one.

It does seem sensible to have a defined order/process ahead of time for assessing what is prioritised to be paid when, rather than make it up on the fly mid-crisis (a failed deposit taker).

I have a fleet of term deposits. Once the scheme starts I will fold some into other institutions to keep the maximums below $100K.

Will have to be firm outfits with plain 100% eligibility for the scheme.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.