It was always a question of 'when' - and that time appears to be upon us.

Latest month-end financial data from the Reserve Bank (RBNZ) indicates mortgage holders are beginning to migrate to longer term fixed rates again.

For the past year or so, house buyers and existing mortgage holders have been going shorter and shorter with their fixed terms - even to the point of floating rates starting to come back into focus.

This has been the natural and pragmatic reaction to the realisation that the RBNZ would be starting to reduce the Official Cash Rate - which it did duly begin to do in August of last year. So far the OCR has been dropped from 5.5% to 3.75%, with another 25-point cut universally expected in the next rate review on April 9.

But there was going to be a time when mortgage holders had to decide that rates might not get much lower, so, it would be time to fix for longer terms.

Mortgage holders usually favour either one or two-year fixed rates. However, the two-year rates in particular have been deserted in recent times, while some traditionally not-bothered-with options such as six-month terms have come to the fore.

The RBNZ compiles a wide and increasing variety of data series that captures mortgage figures. A recent addition has been the C71 series, which shows what new mortgages have been actually loaded up in the month and what the fixed terms are for those mortgages. The next set of those figures for February is not due out till next week. That will give us very specific detail around the new mortgages and who has taken what for what terms. But we can make some deductions about what's been happening based on the data that's already been just released.

And what we can say is that in February there was an interesting split between, on the one had a big move into floating rates, and on the other hand a big shift into two-year fixed terms.

It's difficult to try to get into people's minds and work out the thought processes, but it might appear that a fair few people have decided to 'float' in order to wait and see what the RBNZ comes up with in terms of further reductions in the OCR, while another fair few people have decided, okay two years will do me fine now.

It is significant that the banks have been really pushing the two-year rates since early this year, with, at time of writing, most of the big banks offering 4.99% for two years as their lowest 'special' rate.

The RBNZ's S33 data series shows all outstanding mortgages. There was a grand total of $372.154 billion worth of them as at the end of February. The data also shows the fixed v floating breakdown and also how long before a mortgage has to be repriced/reset.

So, it doesn't tell us per se what specific terms people are on with their mortgages, but we can make some educated deductions.

First up, and this is clear enough, the total amount on floating rose by some $4.256 billion in February to $51.398 billion. So, this is suggestive of $4 billion-worth of mortgage customers having a 'wait-and-see' looking for further OCR and mortgage rate reductions.

But, somewhat contrary to this, the amount of mortgage money due for a reset in two years (so, we can say this would be mostly people on two-year fixed rates) has increased by some $2.303 billion to $50.485 billion in February.

This is the first time the two-year figure has actually increased since May 2023. And $2.3 billion is a big move. It's not comparing apples with apples, but the amount of new mortgage commitments in February was a little over $5.8 billion. The total stock of mortgages outstanding rose by $1.784 billion from $370.970 billion to $372.154 billion during the month.

February has definitely been a moving month. The amount of mortgage money due a reset in a year has increased by $1.365 billion to $99.623 billion.

However, the amount due a reset in six or fewer months has plunged by $7.104 billion to $156.963 billion. If we look at the more than $4.2 billion increase in floating mortgages, the nearly $1.4 billon increase in the one-year tally and the $2.3 billion rise in the two-year, we can form a reasonable picture of where that $7.104 billion has gone.

The big mortgage migration in February has had a fair impact on the amounts of money now due for a reset. The great reset of 2025 is under way.

As of the end of January, as much as 56.9% of the total mortgage book was either on floating or due a reset within six months. At the end of February this was down to just under 56.0%.

And in terms of the 12 months, at the end of January 83.4% of the mortgage book was either floating or due a reset within 12 months, whereas at the end of February, this percentage was down to 82.8%.

So, while many folk are clearly grappling with the 'what to do and how long to do it for?' question, separate RBNZ data shows that significant numbers are still grappling with paying the interest bill.

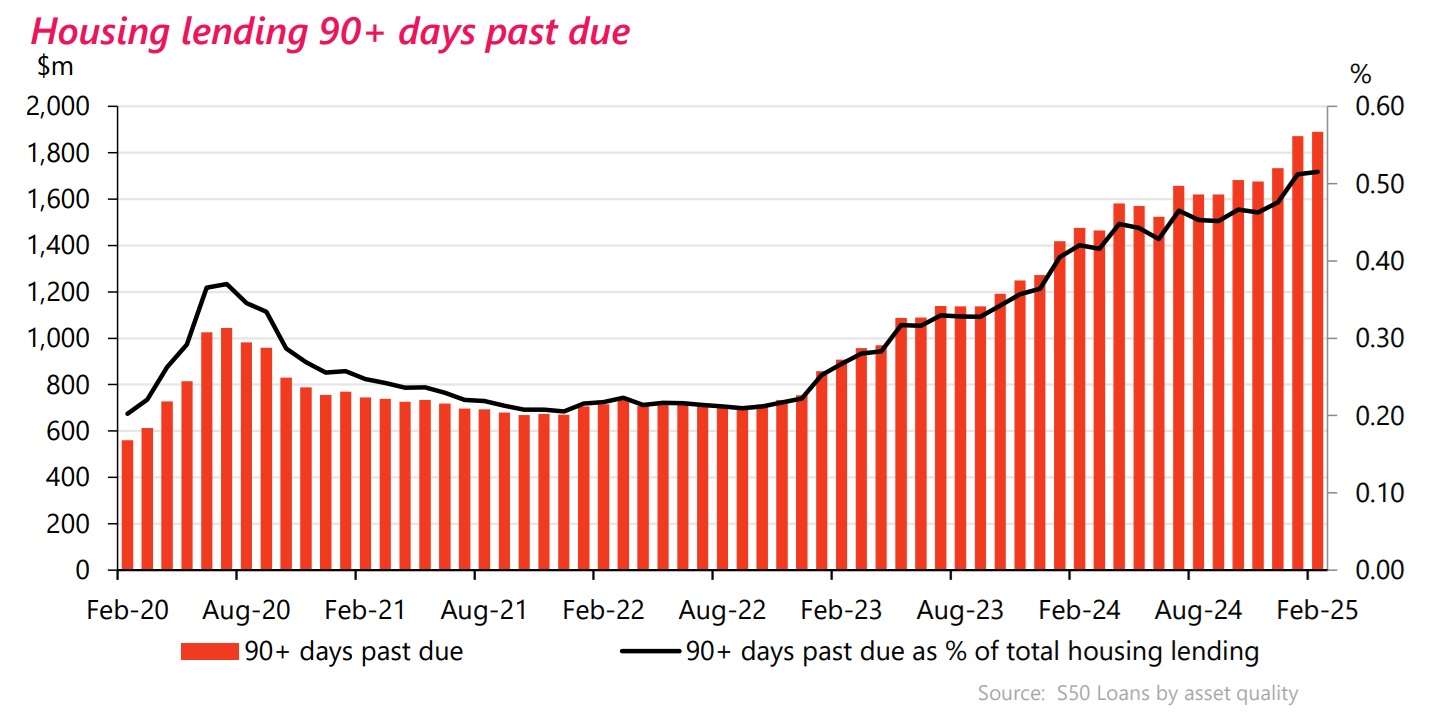

The RBNZ says that in February the total of non-performing housing loans increased $23 million to $2.351 billion and the figure is up $632 million (36.7%) in the past 12 months.

The amount of non-performing loans began to spike sharply as interest rates rose, but had appeared to plateau and even be falling in recent months. However, there was a large rise in January and that's been followed by another increase in February.

Non-performing loans currently make up 0.64% of the total of outstanding mortgages. That's the highest non-performing loan percentage since 2013, but still well off the 1.2% levels seen regularly during the 2009-11 post-global financial crisis period.

Breaking down the February non-performing figures, the amount of impaired loans rose to $462 million from $457 million, while the amount of loans 90 days past due but not impaired rose to $1.889 billion from $1.871 billion.

4 Comments

4.99% for 2 years is a good rate if you don't expect to make additional repayments during that time.

Agreed. Take out the stupidity of cheap printed cash thanks to the US over reaction during covid, and this is historically a fantastic rate.

Will it still look good if OCR reduces another 0.50% across the next RBNZ reviews...

Here is hoping , could do with a reprieve .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.