I think this is what we could call 'starting the year with a bang'.

We are going straight into 2025 with the biggie - inflation.

The Consumer Price Index (CPI) inflation figures for the December quarter to be released by Stats NZ on Wednesday, January 22, will give us a very early indication of whether our current assumptions about the (lower) path interest rates will follow this year are correct or not.

The inflation figures will be the most important, though by no means only very significant influence, on the Reserve Bank's thinking ahead of its first review of the Official Cash Rate (OCR) for the year on February 19.

We've already had in the past week the influential and long-running NZIER Quarterly Survey of Business Opinion (QSBO) and the (I think) increasingly important monthly glimpse of inflation provided by the Selected Price Indexes, which contain about 45% of the ingredients in the CPI.

Then, to come, there's the inflation figures on January 22.

Then there's ANZ's monthly Business Outlook (ANZBO) Survey on January 30.

Then there's Stats NZ's suite of labour market figures - including the unemployment number - for the December quarter on February 5.

On February 13, there's the RBNZ's Survey of Expectations in which business leaders and forecasters give us their views of where inflation's going to be in a year, two years, five years and 10 years. And then there's another inflation sneak peak with a further Stats NZ Selected Price Indexes release on February 14.

So, that's heaps of useful stuff for the RBNZ to consider, and perhaps worry about, ahead of its February 19 decision.

Of course, I say the RBNZ's 'decision'. A really interesting point to consider about the forthcoming review is the extent to which the RBNZ has already pre-empted itself. A decision to all intents and purposes seems already to have been made.

Governor Adrian Orr commented after the last OCR decision on November 28, that the forecasts contained in the latest RBNZ Monetary Policy Statement (MPS) were "consistent" with another 50 point OCR cut in February.

In the veiled world of RBNZ-speak that's as close as you are ever going to get to hearing the central bank say in advance "yes, we will cut 50 points". I can't readily recall the RBNZ ever being as explicit before in its forward guidance ahead of an OCR decision.

All of which means that it would be reasonably awkward if some of many data releases outlined above before the February 19 OCR meeting have results that run counter to the logic of a 50-point cut.

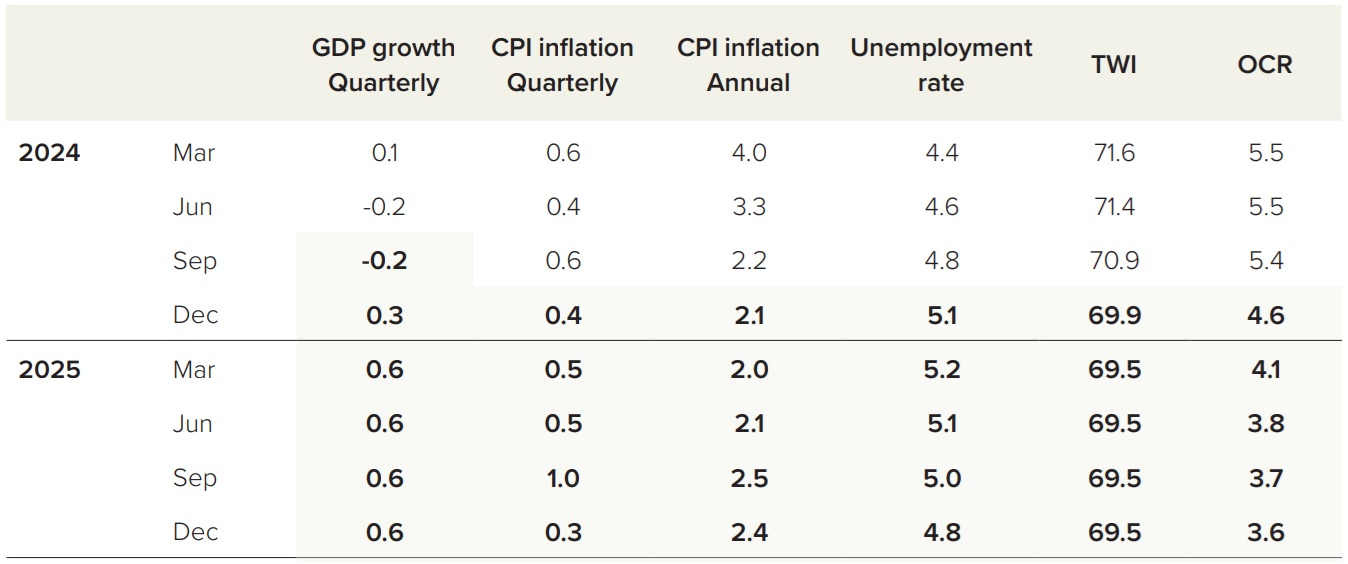

Here is an abridged version of those most recent RBNZ forecasts. Bold numbers on a shaded background indicate figures that are forecasts. The full version can be seen on page 49 of the MPS.

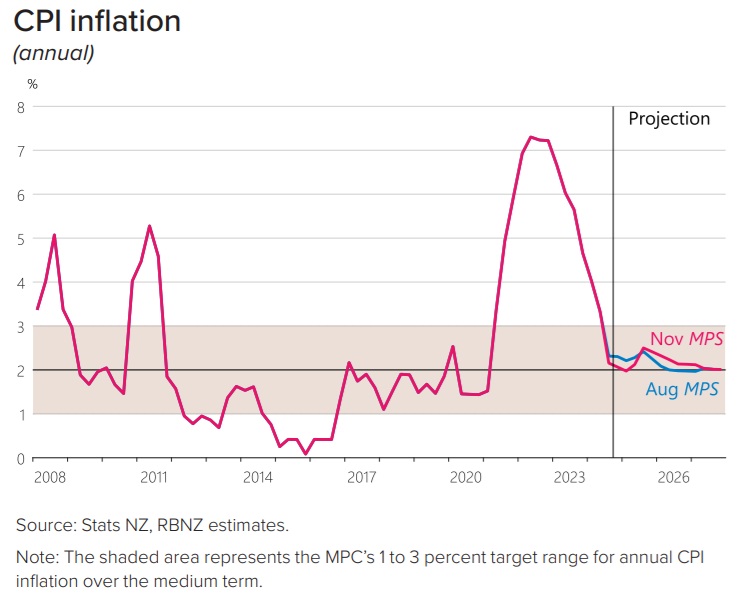

As you can see, the RBNZ is forecasting that the annual rate of inflation will have dropped to 2.1% as of December, down from 2.2% in September.

The RBNZ is charged with achieving inflation between 1% and 3% with an explicit target of 2.0%. There is therefore some possibility these latest figures to be released on January 22 will see the central bank hit its target bang in the middle.

It's all a far cry from June 2022 when the CPI hit 7.3%. Indeed, inflation was outside of the 1%-3% range from mid 2021 till September 2024. That's a long time.

So, having achieved the holy grail of low inflation once more, can it be maintained? Obviously, that's the key to seeing interest rates continuing to come down and staying down.

Both the NZIER QSBO and the Stats NZ Selected Price Indexes out in the past week appeared to suggest there'll be no nasty surprises in short term inflation. The RBNZ's pick that annual inflation will be 2.1% therefore seems reasonable enough. That means there's probably going to be no obstacle to the RBNZ going ahead with its planned 50-point cut on February 19, taking the OCR down to 3.75%.

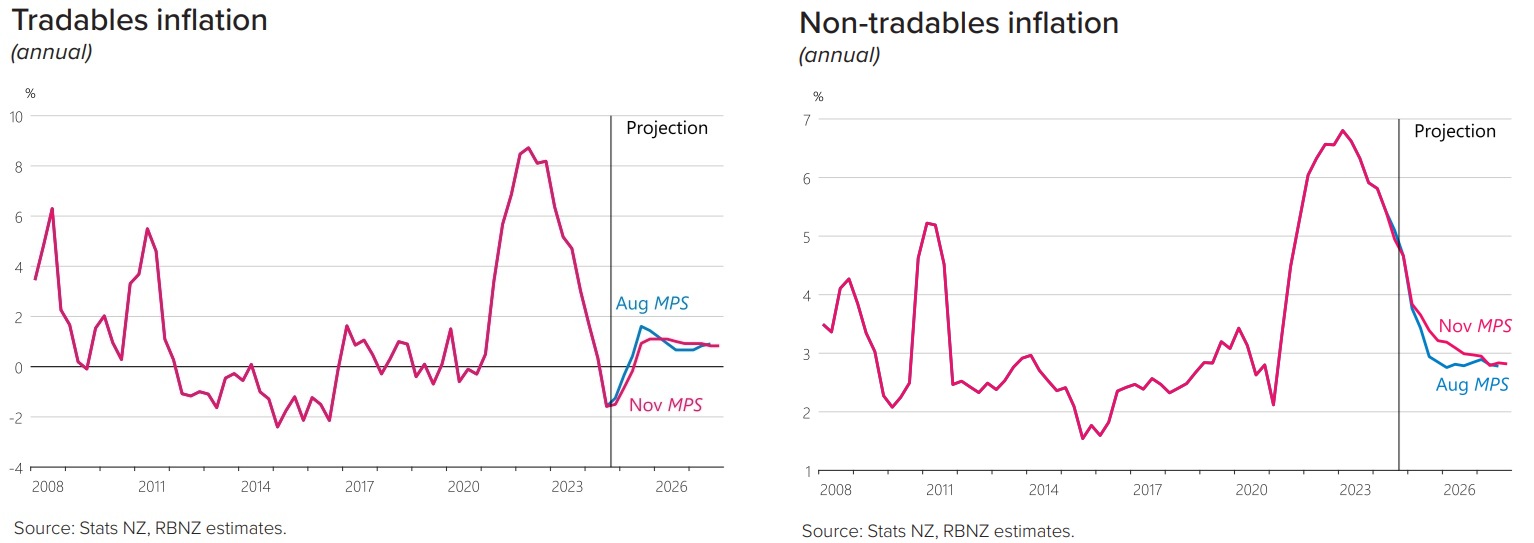

But we can always find something to be concerned about. The RBNZ's expecting domestically sourced, or 'non-tradables' inflation to remain relatively high. The main source of the sharp falls we've recently seen in overall inflation levels has been overseas, with things such as lower oil prices.

However, what comes down can go back up again. And oil prices are now very much on the rise. Compounding this is the fact our brave little kiwi dollar is getting killed by the American juggernaut currency while international bond yields, particularly those of longer durations, have been rising.

The RBNZ is forecasting that domestic, 'non-tradables' inflation will have been 4.7% as of December, down from 4.9% in September.

The RBNZ further forecasts than annual non-tradables inflation will be 3.7% by June and 3.2% by December this year. 'Tradables', overseas-sourced inflation, is forecast to have been at an annual rate of -1.5% as of December and is forecast to still be in the minuses, at -0.2% by June 2025, before going positive at +1.1% by December.

Clearly though, there is some risk to the inflation outlook if our domestic inflation does remain somewhat 'sticky' and more particularly if there are some shocks that start to come through from what's - let's face it - a very volatile global situation.

It appears that the forthcoming January 22 inflation figures will be satisfactory and that therefore the light will stay green for the projected 50 point OCR cut next month. Beyond that though is where it all gets a bit tricky.

The RBNZ's latest forecasts indicate an OCR of around 3.5% or a little lower by the end of this year. Taken at face value that forecast would suggest that after next month, when we can expect to see the OCR at 3.75%, most of the easing of interest rates will have been 'done'.

Various economists are suggesting rather more will need to be done with cuts to revive an economy that fell into a big hole in the middle of last year and is struggling to get out - notwithstanding the now rising business confidence we are seeing.

Inflation holds the key. Things appear to be looking okay for now - but there's plenty that could go wrong this year. If for any reason inflation begins to surprise on the upside in the next few months, interest rate reductions may stall. And that in turn could delay the hoped-for economic recovery.

51 Comments

I think we're going to see the last remnants of the rates/insurance hikes come through for the Q4 24 inflation. It's the numbers for the March quarter that will be interesting. We'll have less effect from non tradables and a still struggling economy.

I just received the annual comprehensive insurance premium for my car: 20% reduction + 16% increased agreed value (Tower)

They must have made a mistake !!

Must be all over the sector for cars, our two cars both came back with premiums slightly less than 90% of the previous year

The mistake may have been a year ago when the premium increased by nearly 30% (no claims or crimes)

"Last"? They've only just begun. Double digit rates rises coming in 2025 for most Councils. Same for insurance premiums.

Hmmm. Southern Cross premiums going up 22%.

They pretty much have to cut 0.5% after saying they would. But I suspect there will be some talk of future uncertainties etc.

Unless the CPI comes in much higher than anticipated that is, highly unlikely IMO.

What happens if the OCR falls and basically the banks don't move ? A 0.1% or 0.2% drop in interest rates is pretty much a waste of time. Have banks "Already priced it in" ? in any case.

They have. But if he doesn’t decrease the OCR they will price it out via higher rates.

If you think of something like the 2 year rate, it’s effectively priced at the markets guess of interest rates over that 2 year period, and that’s largely based on the current OCR and projected OCR.

It’s quite possible interest rates increase even if he does cut 0.5% as he may also change the tone and projections.

If the banks don't move their rates they can look forward to another year of refinancing and few new loans. More of the status quo in other words.

Thanks David. No mention of the the fall NZD and the effects that will have on inflation.

“Compounding this is the fact our brave little kiwi dollar is getting killed by the American juggernaut currency”

I'm waiting for all of Trumps tariffs to kick in. All signs point to inflation kicking off again. If the RBNZ drops 50bps in Feb to save face, they will be putting it up again in May.

They most certainly won’t be putting it up again in May

They will probably keep it at the same rate for the rest of the year after May, maybe outside chance of a small increase near end of year if inflation starts up again

The NACTF are relying on further falls and no increases. Methinks this was tacitly agreed when Luxy met Orr.

That's enough for you, JJ? Good to know.

Fluctuating oil prices or indeed the price of any commodities don't matter greatly. These things can indeed cause blips in the CPI rate but they are short lived given what's in the basket of goods being measured and the various weightings. Unless the total money supply increases we won't get inflation that sticks around, assuming nothing radical happens with velocity. (Without such an overall increase in the money supply, if one price rises then logically others must fall and it's just a question of timing/delays before that happens.)

Money is created mostly by the lending banks. The rbnz has little control over them other than via the OCR. Dropping the OCR does seem to be stemming at least the rate of decrease of the largest asset class bought with borrowed money in NZ, namely houses. So it also seems money supply constraints over the last couple of years have stabilised, as relatively greater amounts of money are created and lent to buy houses.

Will this continue and indeed gather pace? It depends on large part on the demand for loans - as supply isn't an issue given the banks are willing to make them to reasonable borrowers. I would say that demand, in turn, depends on sentiment and to a large degree employment.

Well said MV.

Personal note: I was inquiring about lending from 2x of the 4x banks I deal with, mid last year, about another property.

I was offered well over the amount we were seeking. Yet I was not keen to pull the trigger then, as our current property is good and as price falls looked more likely. I was 100% right, as falls occurred and many properties languished unsold for 3 to 12 months.

Now employment security/no pay rises is on my mind, as well a housing price falls look most likely going into 2025.

2025 will see more inflation and higher than expected borrowing rates. Assets that require borrowing will be a serious casualty and further price depression and in the emergency room needing a resuscitation.

Will the Nats rollout the terrible policy of allowing foreign buyers in? Maybe. Winnie will have to collapse the Govt, to put this issue to the people.

Trump 2025, will roil worldwide inflation, as he makes the rest of the world pay, to Make America Great Again. Such economic power/advantages/hegemony they have.

The 2x offering banks have been hounding us to take their money......I remain steadfast and "no thanks, not just now, still looking for the ideal property" and not keen on large Debts, as I get a little older.

Optionality and being in control of your life, with no effective Debt is liberating. Also not keen on lining the pockets of the old people herding farmers (Rymans, Metlife) and deluded vendors wanting moonbeams for lacking on maintenance homes and dirt.

Yes the lucky generation - the baby boomers - have had all the stars aligned right through their lifetime.

Low Home to Income Ratios when purchased in the 70s,

ability to have just one working and one bringing up the kids,

rapid house asset value increases in 70s and 80s (admitidly high interest rates in 80s),

Increased equity allowing purchase of rentals,

rapid house price increases from 2003 to 2019 to deflate away mortgages and launch into a well heeled retirement.

"Fluctuating oil prices or indeed the price of any commodities don't matter greatly."

No worries - JFoe will be along shortly to point out just how erroneous that view is ... (LOL)

My reference to oil prices was of course contextual - they don't matter greatly for the purposes of discussing inflation (for the reasons I gave). Obviously they matter per se.

Was you 'contextual' basis this bit?

"Unless the total money supply increases we won't get inflation that sticks around,..."

Because if it was, you need to look closely at how the money supply increases in times of inflation simply because people HAVE TO borrow to make ends meet.

If people borrow money, Chris, it's likely 'fountain pen' money created by a bank - so, adding to inflation.

Fluctuating is a vague term. A significant spike in oil prices over a couple of months, or a sustained increase over 3-6 months has been enough to trigger a sustained and broad increase in the price level (aka inflation) several times in the last 60 years. Energy-transport-food-wages-rent is the typical causal chain. Once you hit wages, you're not getting into reverse.

The money supply responds accordingly - see the expansion of revolving credit over 2023 in NZ for example.

"Once you hit wages, you're not getting into reverse".

If there isn't the money supply (or increased velocity) to pay for those increased wages, then yes you are, in my view

Three key flaws in that thinking (in my view):

- Consumers will reduce the scope of their consumption when times are hard - discretionary spending, and the businesses that rely on that spending, will fall, while businesses selling necessities (food, utilities, insurance, transport etc) will simply pass on increased costs to customers, and generally increase wages to ensure that they retain their workers. Look at wages vs household living costs over the last few years - near perfect alignment. So, prices for critical goods adjust to the new price level - and they can because consumers reduce spending on other stuff.

- Money supply responds to inflation. Chris made this point earlier, businesses extend their credit lines to get through the tough times. Sure, some will fail, but most will make it through using credit to bridge from price level 1 to price level 2. Businesses between 2021 and 2023 increased their revolving credit debt from $60bn to $70bn. Have a look at the data (isolate revolving credit by clicking on the key).

- How do central banks respond to inflation? By ensuring banks take money off mortgagors and businesses with debt, so that they can protect the wealth of bank shareholders and savers. How does that play out in the real world? Here you go. What do you see in the data? Households getting considerably richer! Now, how will they pay those higher prices? Oooh, it's a toughy.

Interesting response, thanks. In your first paragraph you are agreeing with me, as you describe some prices going up and so less money being spent on other things. That is one of the key points I made in my first post.

Your second paragraph gets the arrow of causation back to front - prices overall cannot logically all go up at once unless there is money there to pay for them. It doesn't rationally make sense the way you have described it. Next, businesses borrowing to bridge the gap they cannot afford to pay indicates the money supply is increasing - as most borrowed money is new money created by commercial banks (increasing the money supply). So, again you are agreeing with me, somewhat at odds with your other remarks in your second paragraph.

Your third paragraph is imprecise, as central banks respond to inflation by increasing the reference interest rate (unarguable) which decreases the demand for loans (just look at the vast stack of property on trade me) which limits the money supply (follows logically).

I think we're speaking past each other.

Your underlying assumption is that prices can't go up if there is 'not enough money' to pay those higher prices. This just isn't true in an advanced economy...

- People will stop buying some peripheral, discretionary things to pay the higher prices for important stuff, and wages will adjust to reflect higher cost of living. This enables a broad adjustment to the price level (aka inflation).

- Higher interest rates hurt a minority of households - the rest carry on.

- When times are tough credit keeps flowing and public debt kicks in (automatic stabilisers) - this provides the additional money required for the adjustment. During the peak high interest rates year of 2023, banks pumped in $15bn of credit in *net*. Govt weighed in with another $10bn.

All those years after the GFC we never had any real inflation, despite oil prices jumping around like a yo-yo. I don’t think it makes as much difference as many here believe.

The impact on CPI were just not significant enough to 'make news'. Here you go. Tell me what you see?

There was massive asset inflation. It's just that residential property isn't part of the basket of goods measured by the state as part of the number they are pleased to call the CPI.

And yet that asset inflation plays into everything - syphoning huge percentages of income away from most; increases in rents, deposits, the need for salary increases, as people see the kiwi dream slipping further and further out of reach.

The housing ponzi and its non-measured inflation has done huge damage to New Zealand.

The "official" inflation figure bears no resemblance to the household reality on the ground. Supermarket food prices still going up, double digit rates increases incoming, insurance premiums going up by more than "inflation", electricity prices going up double digits again, healthcare costs going up (mine are up 15% in January), petrol prices up, the list goes on.

Meanwhile, employers will be offering a measly 2% "inflation adjusted" pay rise to cover all of the above.

I thought supermarket inflation was very low? According to the stats, but also what I have noticed shopping over the past few weeks.

Rental inflation is zero.

Petrol prices have crept a bit higher but still well off the $3+ per litre they were a year or so ago, granted they might get back up there in the next 1-2 months.

Doubt we will see food premises increases prices any more - they won’t be able to.

Construction cost inflation close to zero I would say

Fair points on the ofter things.

potentially CPI might creep back up towards 3% in the 3rd quarter. Until then, 2-2.5%

I buy the exact same stuff every fortnight so I easily track the prices of everything, and they are definitely still going up. A bag of grated cheese went up by $1 which was a 12.5% increase. Bag of coffee beans the same. A box of cereal that used to be $6.99 is now $8.79 "on special". Produce is still expensive compared to normal summer prices (albeit they are cheaper than winter prices, which is probably what is making food prices look lower).

Buy a cheese grater and stop buying that Kopi Luwak Coffee

Not seeing those sorts of things at all. I am seeing sharper prices or flatness for most things. But I guess depends what you buy and where.

Away from anecdotes, the data released in December showed very low levels of inflation for food.

Does it depend which brands they include and the assumptions about buyers/consumers behaviours?

If the assumption is that the consumer will always buy the lowest cost substitute, does this influence the items included in their samples?

The data might not reflect reality, hence many saying they are still seeing inflation.

Higher Farmgate milk prices, that we celebrate, will definitely flow through to many food prices, which we won't celebrate.

It's all inflation though isn't it if it's just price increases and no improvement in the product or service.

Inflation begets inflation and we're so fixated on the delta we fail to see the bigger picture. And that is the destruction of monetary value. How do you get value for money if your money has no value?

We think millions and billions in asset values is wealth, when the reality is it simply reflects the destruction of value on a larger scale, and justifies the demand for more credit creation, and financial rent extraction. The only solution to restore value is deflation, not more speculative "asset" classes.

Inflation is dead & buried

Theres only 4 circumstances that create inflation, population growth, money growth, demand growth, supply shortages

All 4 circumstances are now dead & buried

Banks are needing to drop their rates & profiteering in order to stay alive

Do I assume correctly that exchange rates eg NZD devaluation vs USD come under your "money growth"?

Your joking right? China are printing - USA will shortly again - how do you think the FIAT ponzi will survive without money growth???

The future is simple! According to the RBNZ forecast the TWI was 69.9. The real current value is 66.8, about 4.3% lower than that forecast. The 0.5 pct reduction will bring the NZD even lower than 0.55 USD. Everybody will notice that at the pump and at the check out till at the supermarket.

The collapse in the Kiwi Peso is worrying but it does tend to take time to pass through inflation from currency moves to consumers pockets.

Meanwhile,despite having "defeated" inflation, National support has plummeted to 30%, and Luxon, realizing that something needs to change, has axed Chris Reti. What will Simeon Brown do differently? What will happen to the planned new Dunedin hospital and to the planned Waikato Medical School? Is $380 million too much to train future doctors for New Zealand, noting the massive shortages, brought to the attention of the Minister by both the union for junior doctors and the union for senior doctors?

Good call to move Simeon away from transport. He had some weird anti safety grudges and hopefully the new guy will back pedal on some of this.

Yeah but I'm not sure him taking his weird ideological grudges over to Health is the best idea either!

He comes across as a teenage boy who hasn't yet grown out of his overconfident Ayn Rand phase.

See they projected a TWI of 69.9 for Dec 24...its currently 66.8...and they are projecting it to remain around 69.5 throughout next year.

Is that a projection of convenience and will they ignore it, especially if it weakens?

Cut of .25 is all that is needed.

So, having achieved the holy grail of low inflation once more, can it be maintained? Obviously, that's the key to seeing interest rates continuing to come down and staying down.

If the holy grail has been achieved at the current rate, why does it need to come down further, unless you're trying to increase inflation?

Note that the OCR is already lower than forecast. The forecast also shows that inflation increases again as the OCR is reduced. Maybe a slower .25 reduction is all that is required, but the RBNZ have backed themselves into a corner again with promises, in attempts to improve their credibility.

that the global structure of interest rates will be higher going forward than it was pre-pandemic

This from todays Westpac Group article published here. How does this align with your desire/belief of interest rates continuing to come down and stay down?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.