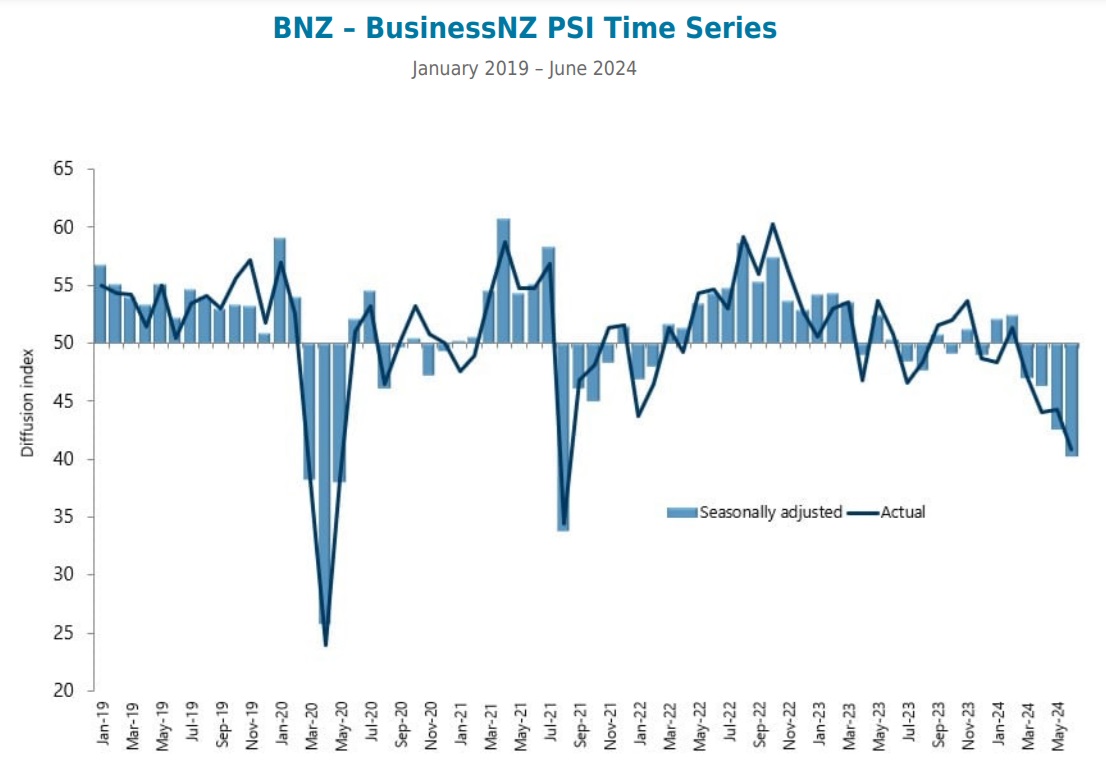

Activity in New Zealand's services sector - which accounts for about two-thirds of the country's GDP - has fallen sharply again in June, according to a long running survey.

The BNZ – BusinessNZ Performance of Services Index (PSI), which has been going since 2007, has for the second month in a row recorded the lowest level of activity for a non-Covid lockdown month since the survey began.

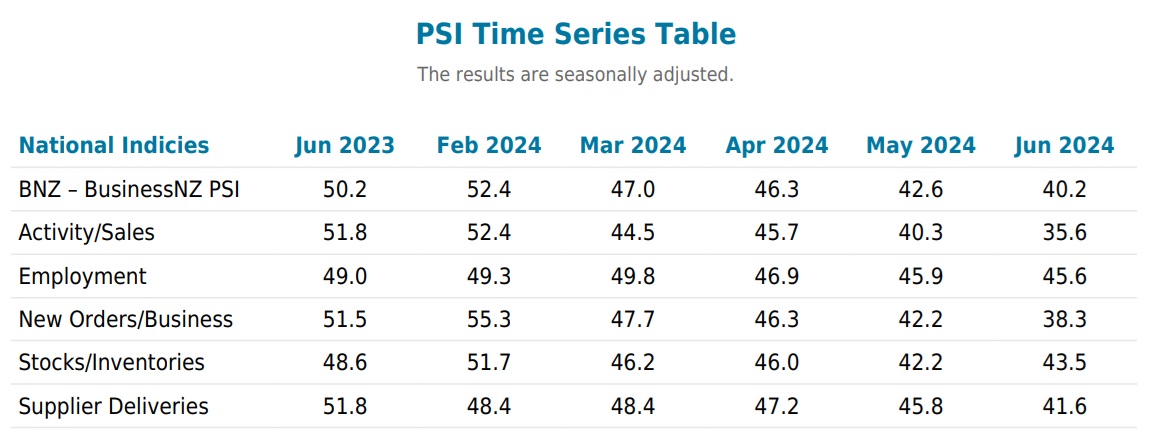

An index level below 50 shows a contracting services sector, above 50 shows it is expanding. The latest monthly result was 40.2 - down some 2.4 points from May. As recently as February 2024 the reading was 52.4.

This latest data comes amid a swathe of high frequency data that's pointing to the economy going backwards in a big hurry.

The Reserve Bank (RBNZ) belatedly acknowledged this last week when it said the range of declining data "may indicate that tight monetary policy is feeding through to domestic demand more strongly than expected". Financial markets have quickly moved to price in potential cuts to the Official Cash Rate, which is currently at 5.5%. The markets are now pricing in a 50-50 chance of a cut as soon as August, a full cut by October and TWO cuts by November.

Monday's continuing collapse of the PSI follows Friday's release of the June factory Performance of Manufacturing Index, which made for very grim reading, with this index now being below 50 for 16 consecutive quarters.

Commenting on Monday's PSI, BusinessNZ chief executive Kirk Hope said that "after a bad May result, the June figures simply got worse".

BNZ senior economist Doug Steel said the weakness in the PSI "appears to be accelerating".

In a separate Eco-Pulse note, BNZ chief economist Mike Jones said if there was a surprise in the RBNZ's "greenlighting of early rate cuts" last week it was only in the timing.

"We’ve long been of the view the economy is buckling, inflation is beaten, and rate cuts would ultimately be delivered much earlier than RBNZ projections. It was a matter of when not if. And it appears the deluge of extraordinarily weak economic data we’ve received over the past few weeks has prompted the change," Jones said.

Jones said from how the BNZ economists have been reading things, the RBNZ’s pivot "couldn’t come soon enough".

"There is a growing chorus of startlingly weak forward indicators that, at face value, warn of a crumbling in economic activity over the second and third quarters."

The BNZ economists had only just revised down their forecast of the second quarter GDP, picking a 0.2% contraction in the economy, but Jones said this was already looking "optimistic".

"Even in the few days since the RBNZ [Wednesday, July 10 OCR] decision we’ve seen further deterioration in the data flow," Jones said.

The June readings of the Performance of Manufacturing (PMI) and Performance of Services (PSI) indices fitted into the category of things pointing to crumbling economic activity.

"The prior month declines in these indices were of such a magnitude that we’d wondered if some sort of pause was in the offing this time around.

"It wasn’t to be. The additional, sizeable declines in the month of June put the PMI at the lowest level since the GFC (outside of lockdown months), and the PSI at the weakest level in the 17-year history of the series (again, outside of lockdown months)."

Jones said evidence of ailing labour demand is starting to mount.

"According to Stats NZ’s filled jobs measure, no jobs were added in May, on net. Labour turnover has slumped. And an 8% June fall in SEEK job ads in June confirmed the 18-month downtrend in job vacancies is accelerating rather than stabilising.

"Our projections for the unemployment rate to rise to 5½% by the start of next year have, to date, been largely built on expectations of stalled hiring against rising labour supply.

"The prospect of deeper employment cuts, as seem increasingly inevitable, means the rise in unemployment could occur faster than we’ve allowed for.

"The attendant impacts on job security, wage growth, spending intentions, and housing market activity have the potential to insert another layer of weakness into the economy over the second half of this year."

77 Comments

August must be in focus now. With the market thinking a cut in Nov is a done deal, Market will start pricing a decent chance of an August cut based on internal bank models and forecasting

I am starting to think they go 25 in August and keep going at that rate each decision. Fed will be close IMHO, you think its bad now, wait till the S&P 500 drops.

Agree. An August cut will be 90%+ priced in by the end of the week if 1/4ly CPI is <0.5%. Unfortunately, the RB woke up 3-6 months too late for the services sector.

On average, the approximately 300,000 NZ service businesses employ just over 3 people each. These are mostly small businesses and just under half of these companies are run by a self-employed owner operator.

How long will it take for this sector to recover? Of these 100,000+ owner operator businesses, how long will it take for them to recover, rebuild and start investing? IMO, at least 12-18 months+ best case scenario for a bounce back, and that is just for the lucky / well prepared who still have a business by the end of this cycle.

This sector contributes $100B+ to the GDP (30%+).

I am still amazed people are not dissecting the RB 22/05/2024 statement and holding the committee accountable for getting it so wrong.

I am also still sticking to my August cut, predicted over a year ago, which I did never change, even when "I was told I was dreaming, and worse, and there was no way in hell the RBNZ would cut in August 2024"

Congratulations?

Well, if they do start cutting in August, sure. It will be well deserved for calling it more than 12 months ahead of time, and compensation for having the courage to stick to my guns when data looked like it was unlikely, the RBNZ said not before mid 2025 and some were mocking me.

Lol, I predicted April on the basis that I thought the data was so obviously flashing 'warning, warning, custard turning'.

I'd rather Nov goes a big bang instead of August.

by then Feb most likely has started cutting rates, so NZD won't be affected too much when RBNZ drops rates.

I think Aug will be 0.25 and big bang in Nov after the fed drops. Aug 0.25 is all but priced into FX now so imports shouldn't get too much worse if it happens. I was thinking 0.5 before the end of the year but I think it will be 0.75 minimum. Watch the banks start shifting their advertised rates soon - especially long term ones.

I think August is too early for the RBNZ, as they will not want to appear out of control, panicky and so wrong with respect even to their recent forecasts (unless the CPI reading this Wed brings a significant surprise on the low side).

I think that August will be used by the RBNZ to significantly adjust their forecast, and October/November to execute a total of 50 bps cut.

It's not just services either - the high frequency data on filled jobs and earnings (weekly) is also showing primary and goods jobs tipping over the cliff. This was obviously going to happen of course. When you slam the brakes on bank lending and Govt spending, you don't get or deserve a smooth landing, you get a crash. Maybe people can understand now why I have been so boring and repetitive on this.

Sadly, we will now spend weeks debating whether RBNZ need to reduce borrowing costs in August or November, or by 25pts or 50pts. As if any of these 'fiddling with the OCR' choices will make any real difference.

It will be 12 - 18 months before the housing ponzi is firing on all cylinders again - not least because RBNZ will not be prepared to get too far ahead of the Fed. So, to prevent a catastrophic collapse, we need Govt to step up and act now to get the economy back on track.

Thankfully, we have a Govt that is well aware of all of the above, and more than comfortable with increasing public spending and intervening in the markets. Oh, no, wait...

They think they can still blame the previous govt, so all is well. All eyes on 2026, and been able to claim a big turnaround.

Except all the levers they are going to pull to "turn things around" won't work

A major infrastructure drive using private finance (aka commercial bank lending) will work for a couple of years until the private finance dudes start pulling the money back at a faster rate than they pump it in. But, they would need to be in negotiation now for any chance of jobs / growth impact in early 2026.

And what infrastructure projects are there on the shelf?...we have years of lead in time to even identify and design what and where any investment will be made....nevermind the capability to enact.

Another legacy of Gov abdicating its responsibilities and leaving it to the markets.

Not what I am seeing - plenty of public sector projects that are on the go or should be - just being done badly or slowly as seems to be the way here in NZ. In addition the rules are changing to allow more market driven development including for power generation and exploration so despite the NZRB being incompetent we will see change

"...months before the housing ponzi is firing on all cylinders again.."

And that in a nutshell is the problem. Even you, expect "The Ponzi" to kick in again. It's just a matter of when. And that's what everyone else thinks as well. So the only question becomes "How long do I leave it before I get in before everyone else does?" and when you've answered that question, so has everyone else.....and so, those months you speak of, become weeks or even days.

Cutting the OCR will be madness, unless fundamental changes to our lending rules have been put in place first.

And who sets the price for any transaction? The Buyer. Generally, "If you can't borrow, you can't buy"

For the avoidance of doubt, yes, kickstarting the housing ponzi is a stupid, stupid thing to do. I would question whether it is more stupid than a self-inflicted recession and a spiral of unemployment doom? I am genuinely torn.

It will need to be a balance. We need to take some alternate action to avoid a disaster.

CGT and reduced immigration and councils accepting max increases of say 4% in rates for 3 years ... in return for an ocr drop.

We have to stop the ponzi and wastefullness that are causing inflation.. and simultaneously remove some of the pain from businesses and individuals with mortgages.

If we even mention to drop the ocr we run a risk of a mad rush back to the ponzi and inflation. Let alone a continued exodus of young professional kiwis.

Gotta take some pain with our gain.

What 'wastefulness' is causing inflation?

There are lots of things I would do before dropping rates. Like offering a 10-year fixed-rate mortgage at 4% to anyone that wants to switch, or forgiving all student loans and MSD debts, or providing interest free loans for green tech. But, given that none of those things are going to happen...!

Fannie Mae and Freddy Mac!

Or Hone and Hine

JFoe while I think the Gov entering the secondary mortgage market would be the best thing that could happen to NZ longer term, the current crop of

*ankers would spit their cookies.

Thanks!

We could save the country billions of dollars per year by moving mortgages onto the Govt books (I'd add term deposits for good measure). This is how we did it when actually built enough houses and got stuff done.

What sort of discipline would apply to lending if it ended up with Govt?

its defined in the issue otherwise hone and hine will not buy off the primary issuer

its not hard... banks mange to do it

ok. So it would not be staffed by Kainga Housing's ex finance team?

Whatever you put in the services contract. Govt would not run the retail end, they would just provide the balance sheet and finance. Student loans is run a bit like that already.

Student loans - surely a model to avoid.

Council spending is the biggest culprit. NZTA. Govt and local govt are huge spenders.

Yes, but you appear to be assuming that Council or Govt spending automatically drives inflation? As if the economy is running at capacity?!?

When we have scarcity of resources, then surely it does?

We have over 300,000 people wanting work or more hours. We are not driving unemployment up because we are 'at capacity', we are driving it up so that people are desperate enough to take jobs that would go unfilled if workers had a tiny bit of choice. Would you take minimum wage working day shifts in retail a short bus ride away or working nights at a care home 30 minutes drive away ($10 petrol)?

The reason to raise the ocr is to remove financial restraints on hard working young homeowners. Who can spend more in retail. Ditto for small businesses.

To raise the OCR we need to make sure that all sources of local inflation are plugged so the right people have money to spend. Not so over leveraged businesses and investors can kick off again.

Else the exodus of young kiwis will continue. Our economy will continue to rely on cheap credit and buying and selling houses and will stumble more and more often and infrastructure and public services will fall apart.

The reason to raise the ocr is to remove financial restraints on hard working young homeowners. Who can spend more in retail. Ditto for small businesses.

OSE do you mean cut the OCR to remove financial restraints? I know a lot of hard working young homeowners who will be absolutely f*^ked if you kept raising rates 😳

The Reserve Bank only has an inflation mandate - the coalition ensured this as one of their first actions. They are doing a good job of getting inflation under control. The bigger problem is the lack of fiscal stimulation.

It is the government that should be getting out ahead of this. The too small tax cut has already been eaten up and it does not help those much who are losing their jobs. Supply-side stimulus is needed - infrastructure buildout, green loans, subsidies, a larger government workforce focused on positive cost-benefit projects, refocusing lending away from housing and into productive industries. The current coalition is doing the exact opposite of what the country needs.

While the RBNZ actions may be pushing us into recession, it is the government actions that will determine how deep and long it will be.

RBNZ are doing basically nothing to tame inflation. It is tracking down the same as everywhere else. We have been more aggressive than most with rates but this has prolonged inflation more than it is subdued it.

But, yes, the answer to our current slump is fiscal.

Definitely salary pressure is down, house prices are doen and unemployment is increasing as a result of the OCR shift. All 3 are outcomes that will drive domestic inflation down.

Without parallel specific targeted action to prevent investment in residential property .. dropping the ocr will surely lead to inflation.

Private sector wages are up about 8% this year - $10bn. Business cost of servicing debt has gone up by about the same amount. Now, which one is inflationary and deflationary again?

I get the feeling like the RBNZ thought the economy had already bottomed out and were going to bounce around here for a bit before things pick up again next year. It feels like this sudden drop over the last few weeks has caught them (and a lot of others) off-guard.

Given that businesses have been passing on the higher costs of interest there's a possibility that cutting i-rates will reduce inflation further and faster. (One of the reasons why November 2023 was the time to start easing. You know ... before consumers got 'comfortable' with the higher prices and the new normal.)

Exactly this. Prices are high because costs are high. We had a couple of quarters of price-gouging back in 2021 but since then prices have just reflected costs... and RBNZ responded by... increasing costs!!

Anyone who wants to debate this needs to tell me where businesses are getting the money from to pay the extra $9bn per year in interest costs they are paying compared to 2022.

To what degrees is bad news Self fulfilled, not exactly encouraging spending at the moment.

It's very tight out there for sure. Govt cuts to date have been minimal. There will be more public sector cuts next year, which, given the grim reality out there today, was/is probably the right call in hindsight.

Local govt remains a huge issue. No cost of living crisis for NZ council.

The tauranga election will be interesting. I suspect the candidates that talk loudest about cost cutting will win.

Anecdotal but the Ski fields in Queenstown are basically empty, which is surprising considering it's the school holidays. Haven't had to wait in a queue at all. This time last year was considerably busier.

Weekend or midweek ? I remember doing some mid week skiing and basically had the entire slope to myself and empty quad chairlift, literally just skied straight in and sat down. True about the school holidays however, it should be packed. How much is that day pass now ? must be horrendous.

I was up yesterday and Saturday, it wasn't busy last weekend either though. People I talked to on the lift had similar comments about how quiet it was.

The day pass is $165 but I actually think them ramping up the season pass prices might of actually put a lot of people off.

They can price what they want, but they have probably hurt themselves a bit by raising the season pass prices so rapidly to the point that people have actually decided to forgo it, some out of principle and others out of necessity.

Even the earlybird pricing is near $1000, a couple years ago it was closer to $600-700. I know heaps of locals who now either go ski touring or have just given up on skiing/boarding altogether.

The day pass is $165 but I actually think them ramping up the season pass prices might of actually put a lot of people off.

The season pass for Hakuba Valley (10+ resorts and Happo - site of Winter Olympics) in the Japan Alps can be as low as NZD1,200. Repeat buyer under $1,000.

$1600 NZD for an Ikon pass (with blackout dates too be fair) which gets you 51 different resorts.

$1600 NZD for an Ikon pass (with blackout dates too be fair) which gets you 51 different resorts.

That's a pretty good deal. Mind you, the terms of price to quality (snow, terrain, facilities), Hakuba wins hands down.

I was at Pure Turoa yesterday, they only have the Giant open due to lack of snow lower, and higher, but there where bugger all people about. It was an ok run for our first day of the year. I do not think many people got North Island season passes this year, due to the RAL collapse.

High winds and snow today will help, the rain will bring the fish up river tonight and I can fish tomorrow. I might go out later for a fish but it cold and pouring, vs a nice fire.

Queenstown has been very cold but we've had hardly any snow, concrete peak is living up to it's name.

Why do you always take up so much space in your comments IT? Do you collect pixels? The current Government hates any waste..you need to cut back please.

No wonder the countries in trouble, all you fellas fishing and skiing. Not that I can talk , at the hot pools, which seem busy.

The mountainbiking trails are also holding up well 😊

Oh , the cyclists having a go now , who's next , scooters???

Hoskings callers will have a fit.

No wonder the countries in trouble, all you fellas fishing and skiing.

Keep your eye on boat sales as a barometer of how bad it might be.

Aldi Australia couldn't shift all its ski gear this year. Mountains of the stuff.

Probably something to do with the season pass price staying the same, but the access halving.

The wheels on the bus are falling off.

Falling off.

Falling off.

.... now there are two of us trying to be 12 year olds....

Knock me over with a feather.

And yet, GDP Live has inflation tracking higher .....

If the RBNZ keeps the OCR up because insurance and rates have increased Luxon might have to rip up Orr's contract

Remember that Luxon does have two kids and will be well aware of how ridiculous our house prices are if they were to live in NZ.

I think you will find Luxon is using Bishop to test the waters on property price declines. I doubt that is Bishops own doing.

Remember that Luxon does have two kids and will be well aware of how ridiculous our house prices are if they were to live in NZ.

Suspect the bank of Mum and Dad comes into play in this case. Same with the Keys.

Maybe Luxon should concentrate on why rates, insurance, and in the near future, car registration, fixed electricity charges, are going up. Whoever is in charge of the RBNZ can't do much about non-tradable inflation. The quality of governmental policies determines that. Reducing the OCR before the FED does will tank the NZD and we will all notice it 14 days later at the pump.

Whilst I wouldn't rule out an upside surprise to inflation, the GDP live stats are hopelessly wrong a lot of the time. They think GDP was up 0.8% in the June quarter, how many of us expect that to turn out correct when the official days finally arrives?

After a decade of greed this was always going to be a messy unwind.Those not realising that were always going to burn. The really big questions is, how far back do assets drop to match returns, aka productive financial reality....?

..you would assume that to an extent they'll need to 'Follow The Fed' - any premature drop in interest rates will cause a significant drop in the NZ Dollar against our trading partners (accompanied by the still sticky non-tradables).

This will undo all the recent gains in reducing inflation.

All the money goes to mortgage, gas, food, insurance and savings for dark days

Yip, we structured our budget accordingly 3 years ago. Thought we would be were we are today at least 12 months earlier. And we are planning for things to look like this for at least 3 years and probably the decade and beyond.

Problems will really start once more and more choose to go without some of what you have listed (insurance and savings are the first to go). To be frank it's already a disaster and only a continuation of the ongoing decline in living standards for most of the population since the GFC.. I think me and my partner are oart of the lucky bunch in that we can do everything you have just listed. Still waiting for this government to do something other than blame everyone for what's happening. Thought they were the business party. Back on track? No, we need an alternative track.

I won't be expecting any meaningful help from this government. I like their tax cuts, but it's hardly some panacea given how far we have declined in recent years. $25/week will not cover my insurance, rates increases ect. Probably wouldn't cover the last few years increases in food alone. Furthermore, with the economic and employment outlook, good luck trying to get higher wages.

The RB is a pointless, obsolete entity from a bygone era like the VHS cassette, cancel it

Major export market has been declining for 2 years and National is cutting counter cyclical spending. And rates are up 4.5% in that period

And no one is buying houses

So recession will go on til next June at least and NZD is going to get hit

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.