So, have we gone forward? Or are we still stuck in reverse?

That's the big question ahead of the release on Thursday, June 20 of the Gross Domestic Product (GDP) figures for the March quarter.

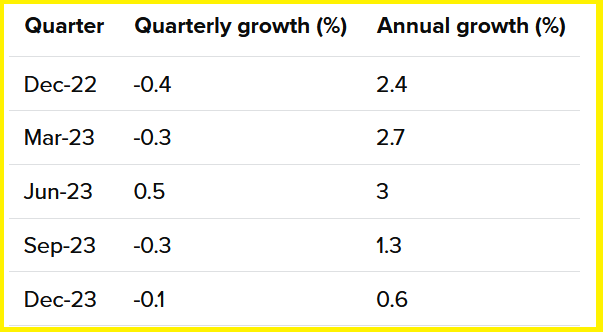

The background is that the economy contracted in both the September 2023 and December 2023 quarters - meaning New Zealand is 'technically' in recession, albeit the contraction in December was very slight, just -0.1%.

This has all come about through the efforts of the Reserve Bank (RBNZ) to get inflation back into its targeted 1% to 3% range by squeezing up interest rates, hiking the Official Cash Rate from 0.25% in October 2021 to 5.50% currently. Inflation IS falling. After hitting 7.3% in mid 2022 the annual inflation rate was down to 4.0% as of the March quarter.

As I've stressed before, in a real sense it doesn't make much difference if our economy is, to say, grow by 0.1% in a quarter, or contracts by the same amount. Either way it means the economy is as flat as a pancake.

However, there is a power in that 'R' word. And we are definitely now getting to the point where quarterly GDP figures with minus signs in front of them are starting to drag the morale of the country down. And that's bad, because it means wallets are locked away and the fact nobody's spending money actually makes things worse - the classic vicious circle.

So, we could probably do with a bit of a pick-me-up and a positive GDP figure for the March quarter, even if it's only JUST positive. Appearances can mean a lot.

To refresh memories, this is what the previous five quarters have brought us in terms of GDP:

So, that's not very cheerful reading is it? And if the above sequence is all starting to look to you as though it might be quite historically significant in terms of the sheer numbers of quarters with a minus sign in front of them, well, you would be right.

In the past 40 or so years there's been a couple of comparable periods. In the 2008-09 Global Financial Crisis (GFC) time we had FIVE consecutive quarters of negative growth - and some of them were a lot bigger (IE -0.9%) than anything seen in the current run.

Going back to the 1988-90 period we had a run of six out of nine quarters that were negative - and that included a -1.1%, and an unemployment rate that ultimately (in 1991) topped 11%. I remember that period well, and it was deadly.

While the recent run of GDP figures has been nothing like as depressing as the two above examples, and unemployment, for example, is currently just 4.3%, it's kind of gradually getting there, nevertheless. These are not happy times. Much depends on where we go from here.

All we don't need now is to start getting super downbeat and not spending at all. Gloom begats gloom.

And the worst thing about all this is our recent 'headline' GDP figures don't even really tell the 'real' story. Our economy is not growing at a time when our population IS growing, a lot. According to Statistics NZ estimates our population grew by about 130,000 - or 2.5% - in the year to March. That's huge. And it means a lot more bodies driving the economy...and yet, they are producing in net, actually less.

GDP per capita decline could be worse than during the GFC

Since the third quarter of 2022 our GDP per capita has declined by nearly 4%. To give some very meaningful comparison, during the GFC our per capita GDP fell by 4.2%. And regardless of whether the March quarter 2024 GDP outcome is a plus or a minus, we can be reasonably certain that GDP per capita will have fallen yet again in the quarter.

ANZ senior economist Miles Workman is suggesting the forthcoming figures on June 20 may well see the per capita GDP decline since the third quarter (Q3), 2022 hit 4.3% - IE MORE than during the GFC.

Okay, so enough of the gloomy talk for a minute. What are the prospects for that March quarter in terms of the 'headline' GDP figure?

Well, it really looks like it could go either way based on what economists at the big banks think.

The Reserve Bank (RBNZ) is forecasting a rise of 0.2%. ANZ economists are forecasting a 0.2% rise, while ASB economists are forecasting a 0.1% gain. Westpac economists, however, see a 0.2% fall, while BNZ economists see a 0.1% fall, as do Kiwibank economists.

We can get some clues as to what the GDP may have done in the quarter by looking at the already released March quarter results from some of the key sectoral contributors to GDP - 'partial indicators' as the economists like to call them.

The results have been pretty mixed.

Retail sales volumes rose 0.5% in the March quarter, breaking a run of eight consecutive falls. However, monthly data has continued to look weak and the March 2024 quarter figures were 2.4% down on those for the same quarter in 2023.

The volume of building work put in place during the March quarter slumped 4.0%, with residential building work falling 4.8% and non-residential work down 2.8%. The total volume of building work in the quarter was the lowest in the past two years.

The volume of total manufacturing sales fell 0.4%, following a 0.7% fall in the December 2023 quarter. After falling in the December quarter, wholesale trade sales lifted on a seasonally adjusted basis by 0.8% in the March quarter, but the figures were down on those for the same quarter in 2023.

So, all that leaves plenty of room for healthy debate as to whether come the unveiling of the latest figures on June 20 we will still officially be 'in recession' or will have pulled ourselves out - barely.

At this point then I will leave you in the good hands of some of our major bank economists and their views of where things may be going.

Westpac senior economist Michael Gordon, who is picking a 0.2% contraction for the March quarter, said he's expecting most sectors to do better (or less bad) than they did in the December quarter, "but with some pronounced weakness in a few areas driving the overall result".

"Manufacturing (outside of food, which is more tied into exports than domestic demand) has been in decline for the last two years straight, and the March 2024 quarter looks to have been particularly soft, with large declines in chemicals and machinery. Construction activity was also weaker, as the pipeline of work that was consented in past years has been run down. We also saw further weakness in wholesale trade, which is something of a bellwether for the wider economy given how many other sectors it touches upon," Gordon said.

Transport and hospitality to get a boost from the rebound in tourism

"On the positive side of the ledger, agriculture and food manufacturing benefited from a lift in milk production and the recovery from the devastation of Cyclone Gabrielle last year. We expect areas such as transport and hospitality to receive a boost from the ongoing rebound in tourism (in seasonally adjusted terms, overseas visitor numbers were weaker in the December quarter, but improved in the March quarter). And log harvesting rose strongly for the quarter – though that will almost certainly unwind next time, as we’re now seeing a glut of logs on Chinese wharves that have pushed prices down sharply."

ANZ senior economist Miles Workman, who is picking a 0.2% rise in GDP for the quarter, expects services industries (around two thirds of GDP) lifted 0.4% quarter-on-quarter (and making a 0.3% pt contribution to headline growth ). He thinks the goods-producing industries contracted 1.2 % q/q (making a -0.2% pt contribution to headline growth), while primary industries will have expanded 0.3% q/q (with its contribution to headline GDP coming in flat).

"Meanwhile, the net migration cycle has turned, the labour market is loosening, consumers and businesses are downbeat, the housing market is subdued, the terms of trade is well below its peak, and global demand is sub-par," Workman said.

"Slowing inflation and gradually falling fixed mortgage rates are providing some offset, but overall we’d characterise the numerous drivers of economic momentum as becoming more synchronised to the downside than they have been in recent years.

"In big-picture terms, while we may well see the occasional upside surprise in the GDP data over the near next year or so (given typical volatility), there doesn’t appear to be a lot of scope for a sharp and sustained recovery any time soon. While growth is expected to find a floor this year, it is expected to remain sub-par for a while yet. We think this backdrop is consistent with the RBNZ cutting the OCR sooner than signalled in the May MPS. We expect cuts from February 2025."

BNZ senior economist Doug Steel, who is picking a -0.1% figure, said the economy "still looks like it is bumping along the bottom and contracting on a per-capita basis".

"The indicators remain very noisy, so we wouldn’t rule out the possibility of a small positive in the quarter. But the main message remains of the economy struggling to grow. A quarterly outcome as we see it would result in annual growth steadying to flat, from -0.3% in Q4 last year. Anything near zero annual growth overall implies clear contraction on a per person basis."

'No more recession' headlines could be cold comfort

ASB senior economist Kim Mundy, picking a positive 0.1% figure, says the March quarter figure is therefore likely to result in many "no more recession" headlines.

"And while this is arguably a nicer read, it may prove cold comfort to those facing weak demand amid New Zealand’s cost of living crisis and heightened economic uncertainty.

"More importantly, a small rise in activity in the quarter isn’t being driven by any significant structural changes to NZ’s economic outlook. Long story short, we expect the economy to continue to oscillate between small rises and falls until there is a pronounced change in the economic outlook (i.e. monetary policy starts to ease).

"With the pricing side of the economy proving more resilient than the activity side at this point, those [RBNZ] rate cuts still look to be some way away. February 2025 is our best guess at this stage.

"The general weakness will continue to be more evident in the per capita GDP numbers as headline GDP continues to be flattered by high levels of population growth. We expect GDP per capita fell 0.4% in Q1, which would mark the sixth quarterly decline," Mundy said.

"In other words, each Kiwi’s slice of the economic pie shrunk again, even if the whole pie is a tad bigger."

Kiwibank economist Sabrina Delgado, who's picking a -0.1% figure, sees things as "all pretty sombre" but notes that "the weakness we see and feel is all by RBNZ design".

"The RBNZ needs to see subdued growth in their fight against the inflation beast. And subdued growth is what they’ll see," she said.

The 'heavy hand' of the Reserve Bank is hurting

"The RBNZ’s heavy hand continues to hurt households and businesses. Restrictive monetary policy is clearly working. So long as interest rates remain elevated, growth will remain subdued. And that is the outlook for majority of this year.

"Interestingly, though we’re living in a strange era where bad news is in a way good news. Because as the economy slows down inflationary pressures are squeezed out. And the sooner we see inflation back within the RBNZ’s 1-3% target, the sooner the RBNZ can deliver rate cuts. As interest rates are relaxed, confidence among households and businesses should build. And the economy should regain momentum. Fortunately, our forecasts see inflation falling below 3% by the September (third) quarter. We’ll see that data in mid-October, and hopefully receive confirmation of inflation back within the RBNZ’s band then. And from there rate cuts could come as early as November."

Delgado says high interest rates have weakened both domestic and global demand, "suffocating growth".

"We might be okay but we’re not fine. The simple message coming through is that households and businesses need to hang on ‘til 2025. The turning point is on the horizon. 2024 is not going to be a year of much growth. But it is the year of central bank rate cutting. Offshore we’re already starting to see a number of central banks cut rates. Most notably we saw the ECB cut rates for the first time since 2019. We don’t think the RBNZ will be too far behind."

Delgado expects to see growth pick up into 2025 as rate cuts are delivered.

Economic growth

Select chart tabs

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

85 Comments

Have the actions of the Reserve Bank really had any effect on inflation? Food prices have fallen due to better weather, imported inflation has fallen due to falling shipping rates (which are now reversing) and falling commodity prices. Fuel prices are falling which should bring transport costs down. None of this due the reserve bank. What the reserve bank has achieved is a huge fall in business confidence which has reduced productivity, investment and ambitions for growth - making it harder for the country to move out of the current economic situation.

Raising the ocr has reduced demand for products, reduced demand for salary increases and reduced house proces and hopefully soon rents.

As a result domestic prices for products are not rising as fast.

Inflation is dropping. There are other factors too but rbnz did what was needed and also had to align with other reserve banks. Albeit too late.

As far as i can see it has had a very positive impact on inflation.

What would have happened (and be happening) if they hadn't is too scary to consider.

A big aside is that if we manage to quell inflation. And finally make houses and rents affordable we may stop the net migration of our smartest kids and keep them here to grow our economy.

If this was all true, why was Nationals first priority to provide higher returns to landlords and cut taxes to put more money in people’s pockets. Young people are leaving due to lack of business confidence and lower wages. Higher rates force businesses to cut back on innovation and training and then young people leave. I think a rate cut would be the best move if we want to increase productivity and reduce the brain drain.

Cut the OCR and see the biggest (and only?) driver of our economy take off - house prices and the accompanying Debt that we are now totally reliant upon for economic liquidity. Then see what's left of our productive workers head to ...well, pretty much anywhere except New Zealand. (NB: Are we that much different to every other 'developed' economy? Not much. That's why the general philosophy of "Debt doesn't matter - it's only a figure on a spreadsheet" will likely see what you want to come to pass - interest rates will be cut - everywhere. Then, standback and marvel at the true meaning of Inflation driven interest rates - and down won't to be it)

Looking at the comments today seems people dont make the link between population growth and house/rental prices as a factor. Apparently its only interest rates that influence house and rent prices

Give another year or two of low consents for new homes brought on by low buyer demand and then watch the squeeze occur. If interest rates are lower by then it will possibly be a bigger mess.

I cite the case of Australia where you once lived, see whats happening there to firstly rents up 20 percent or more in some cases and house prices still Uppy. Aus house prices really didnt slow down much from the heights

The Waikato district experienced 21 percent avg house price growth on like for like basis from Oct 2020 to Oct 2023. Interest rates were rising exponentially from early 2022 so prices should have sunk over that timeframe. WDC had one of the strongest population growths and shrinking construction at the same time

Australia’s population growth has been insane. We won’t have much population growth at all in a year or so. There won’t be the economy and jobs to support it.

NZ population increased 820k over last 10 years and 450k for the 10 years before that.

And how does that relate to population growth over the next 2 years? It doesn’t. Population growth waxes and wanes, and I don’t think it’s likely there will be much population growth over the next two years. Do you?

Yes you are right Lord Master Housemouse. Everything is relative and causal, so lets not argue about something not provable whence you then get upset and meltdown if someone disagrees

Hows the rugby, blues vs chiefs super final, we could argue about what that score will be instead. High scoring game, close win by in form chiefs

So you didn’t answer my question and resort to semi-ad hominems.

You raised the issue yourself of low building consents coming soon, and high population growth. I put an entirely relevant point and question to you about population growth over the next couple of years.

Low levels of housing construction will mean diddly squat if population growth is also low

IMO We have rapid population growth spurts followed by assimilation. It starts with growth and we respond to the needs, not the other way around

The high population growth in 2019 and 2020 followed by two years of nothing, then 18 months so far of extra high growth will probably create enough demand from those immigrants for new housing once interest rates tumble and they have obtained residency and ability to buy a house.

You're known for childish outbursts but now playing victim

“….There won’t be the economy and jobs to support it….”

Most people move to New Zealand for the lifestyle rather than for job opportunities. Many have sources of income from overseas and might only work part-time here. This trend is likely to continue for the next 20 to 30 years. Once our population reaches 8 million, things might change a little.

Both of those things only influence price because of restrictive zoning. Everything else is a distraction. Destroy the RMA and the Building Act. Shut down the planning departments.

Did you hear wayne brown tonight talking candidly to John Cowan "real life". Dont listen if fragile

I agree. The low interest rate period that lasted over a last decade in NZ didn't magically raise productivity as some other commentators here suggest.

Im fact, NZ's real GDP per worker in 2022 was at the same level as recorded in 2011 despite there being 700K more filled jobs in 2022. The cheap debt-fuelled domestic consumption was simply filling the gap between average wages and worker productivity for all that long.

Here's some evidence that monetary easing reduces productivity but then increases it only when new market entrants increase competition across the board giving the incumbents a run for their money. Link

The commentators you refer too never expected low interest rates to affect productivity much at all.

Why? Because the bulk of the new money that was created flowed directly into non-productive assets like houses, cars and holidays. Very little was spent on productive assets.

How does a high OCR reduce demand for salary increases?

Obviously it doesn't.

Even if there was no inflation, raising the OCR actually increases the demand for salary increases as many salaried workers need more to pay their mortgages and other loans. Which, as we all know, can itself drive inflation higher.

The OCR is a crappy tool for controlling inflation. It is however a great tool for creating Recessions.

A high ocr reduces spend.. due to less equity in houses, less money due to higher mortgage payments etc.

If people spend less businesses make less, and govts get less tax. So both businesses and govt start to shed staff and take on fewer stff. People who do have jons are happy to have those jobs without a rise and more people are looking for work.

So.. Given more demand for less jobs... and far less jobs security (and people know it's easier for their employer to replace them... salaries don't rise like in a boom.

Waikatohome - fair point. But ask yourself, since the GFC, how has dropping the OCR to zero help to prevent deflation (eg 2008 - 2022 ish - or even longer from the 1990’s - 2020) in a period from when we were importing cheaps goods from Asia? All it did was allow excessive debt to be leveraged against our housing market (and create high aggregate demand for those goods/services to stop prices falling more). This is peak stupidity - pumping house prices because we were importing cheap goods from abroad that were giving us a low CPI number! That was never a sustainable economic model. It requires that you always import deflationary forces from abroad and the moment that stops, you find out that your local economy is the house that was built on sand - when the winds come it will fall.

Sorry IO, gotta pull you up and ask you to return to the real world ...

"But ask yourself, since the GFC, how has dropping the OCR to zero help to prevent deflation (eg 2008 - 2022 ish ...)"

1. The OCR was only near zero for 18 months during covid. All the rest of the time between 2008 and 2022 it was at a neutral setting or raised a bit to damp down early signs of inflation.

2. The OCR was never - not even once - lowered to prevent deflation.

Source: https://www.interest.co.nz/charts/interest-rates/ocr

With regards the explosion of debt and where it ended up ... I think we can conclude with considerable certainty that the Aussie banks outsmarted the RBNZ and ensured capital controls, that should have been in place when the RBNZ (as we know it now) was created in 1990, were never implemented.

2. Incorrect. Deflation was a significant concern in 2020.

https://www.interest.co.nz/business/108648/economists-see-longer-term-o…

it may pay to reread either the comment or the linked piece

Thank you.

Worth also noting the date that article was published ... Hardly 'a normal time' ... i.e. smack bang in the middle of covid with the bank economists doing their very best to shovel mortgages as fast as they could. Also - an excellent example a story being told by bank economists without a single non-bank economist being mentioned.

A bit too simplistic I think, the economy is much more than food and petrol. One thing is for certain, everyone will find it much harder to raise prices now than they would have 2 years ago.

"One thing is for certain, everyone will find it much harder to raise prices now than they would have 2 years ago."

Really? Has anyone told the insurance companies, banks, our local Councils. and most other businesses supplying 'essentials' including food and fuel?

This stuff is sad but predictable:

https://www.nzherald.co.nz/nz/reed-myers-liquidation-home-buyers-lose-1…

Be careful on what to trust. CAVEAT EMPTOR

Here are the marketing materials:

One heading in the section stated: “Is my deposit safe and where does it go?”

“Yes, your deposit is always safe, it is held in the Solicitors Trust Account, until it is time for settlement,” the answer states.

When the people put up these deposits, those deposits are used for things like to further the project, like you have to do resource consents and so on and so forth and, put deposits on the land, get finance, all that sort of stuff,” Constable said.

“And that’s what that money is actually applied towards.”

Typically deposits are held in trust accounts and used by developers to show to banks so the banks agree to grant them finances to pay for construction costs.

But Constable claimed Reed Myers customers knew their deposits would be spent on construction costs, and that by being entitled to discounts on homes yet to be built they’d got a good deal.

“These guys put up the deposit and got a benefit for that deposit, for putting up that deposit and allowing it to be used in construction,” he said.

“So it’s not as if they’ve given up the deposit and got nothing for it, they actually got a concessional rate.

Constable told the Herald some customer deposit money had been spent.

He is listed as sole director of The Raroa Project, the company set up for the Henderson development.

He is also sole director of Reedmyers Securities and Red Hills Road, the companies responsible for the Massey development.

'Restrictive monetary policy is clearly working' sing the commentariat chorus. What they mean is that higher rates are killing jobs, closing businesses, stopping houses being built, and dissuading businesses from investing in productivity.

But are higher rates bringing prices down? What evidence is there of that? I can't see any.

Food prices have dropped with global food prices with the 9 month lag that has been reliable for the last 20 years. We pay the import / export price plus markup.

Fuel, plastic and fertiliser costs have dropped with global prices - reducing the cost of some domestic things that rely on these inputs.

Wages have been catching up with the cost of living because they have to - and a key driver of that high cost of living has been higher interest costs!

The data is so clear that the only counter-argument worth entertaining is 'what about the counterfactual - inflation would have been even higher without rate increases'?

To answer that question I would simply point at the myriad of countries like us that have not seen the same level of rate hikes (or pass through to mortgage costs). Why is every country like us on almost exactly the same inflation path down? The answer is that monetarism is a guilty bystander - doing as much to push prices up as it does to push them down.

To answer that question I would simply point at the myriad of countries like us

Can you actually give an example of a country not like us Jfoe? One that can grow without the suppression of the cost of debt and debasement of the money supply by which only those closest to the monetary spigot can benefit?

The elephant in the room is the excessive housing debt relative to productivity that we (and AUS and CAN) have.

And this was caused by dropping rates too far for too long causing the economy to be reliant upon ever cheaper debt to function.

Ignoring this fact distorts your entire view on economics and means the economy is forever reliant on 2% interest rates to survive. Which in a variable world isn’t living in reality.

I agree with Jfoe that there would be smarter ways of doing things - but when you’ve been behaving stupid like we have the past 20-30 years (cheap debt pumping housing bubble) you don’t then get the right to act intelligently without facing the consequences of your past stupidity. We have to face those consequences before we can start implementing more intelligent ways of managing the economy.

And this was caused by dropping rates too far for too long causing the economy to be reliant upon ever cheaper debt to function.

Why do people think that OCR suppression is a recent Covid-related thing? Does nobody even remember Alan Greenspan? Not that long ago.

And that is less housing debt relative to GDP - but that means lower prices which a lot of people don’t want to accept as a viable solution (because it might hurt their net worth - even though it would be a positive move for the economy as a whole for the next 10-20+years)

Yes, the flourescent yellow elephant in the room!

The damage was done in the 1990 to 2010 period when household debt rocketed from 25% of GDP to around 95% of GDP. The net flow of bank credit into the economy during this period was around 11% of GDP per annum (noting that businesses also took on debt)! That flow of credit drove economic growth - or more accurately higher profits fed by that flow of credit money. This gave us great increases in measured productivity that the reckonomists thought were real, or, even worse, put down to the economic reforms of the 80s and early 90s!

Since 2010, household debt has stayed in the 90% to 95% of GDP range and the economy has relied on low interest rates for growth. Why? Because without low rates, interest payments drain too much disposable income from households and the economy stalls (hello 2023, 2024, 2025).

The answer here eventually has to be some kind of debt reset. But we'll struggle on into the deepening mud for a decade or two yet.

Great question. The countries most like us have all adopted the same economic model - run private debt as high as possible, Govt deficit spend enough to offset any current account deficit, inflate the price of property and financial assets to keep the flow of bank credit flowing into the economy and give people the illusion of saving for the future, set up tax and legal systems to ensure the top few per cent can gather up the surplus, extract value from the global south and our limited natural resources to keep the workers equipped with and pacified by tech, toys, and drugs.

Indeed...as has been noted the current decline matches and is set to exceed the declines of the 90s and GFC. If we take the 90s unemployment remained high for a decade.

The policies used then to (eventually) turn the economy are unlikely to succeed this time round though Im sure that they will be tried.

Well said, Jfoe.

Like I said above ...

The OCR is a crappy tool for controlling inflation. It is however a great tool for creating Recessions.

When are people going to realise this fundamental truth?

What’s the alternative?

Switzerland, Denmark - and a range of places where people having higher levels of disposable income doesn't drive prices up. How do they do it? They recognise that markets need managing and regulating. They use taxes to tackle wealth accumulation and inequality. They tax rent. They do what Keynesian countries did for decades before the Chicago school econ freaks took over.

And all those countries have well balanced tax systems working together with mature, sensible, prudent and wiser central banks.

Orr has said he needs a recession to reset pricing. Construction, food, a lot of things.

Remember all the “Go hard, go early” for covid, Orr may well have the same mantra think he still needs to cause damage for the reset to occur.

Orr is the fat lady and he hasn’t started singing.

I think calling Orr “the fat lady” is flattering. When he starts singing, we wont magically get our police, nurses, teachers etc. back from overseas. Our infrastructure problem won’t just fix itself. Our businesses who have suffered or gone bust, won’t be able to flick a switch and undo all the pain they have incurred.

Orr is central in making this problem as this appears to have been his objective, but it’s getting too late for him to control the fall out from it. He can’t immediately undo what he and his committee have inflicted on NZ. I wish he and his committee could look at the state of this country and what they have done! They could likely end up as an international economic case study for future generations, of exactly what you should not do during a crisis!

Would love to see a central banking committee who was in touch with what Main Street is feeling. Rather than having to watch him chuckling through his press conferences with an apparent lack of empathy for the hard working productive people and businesses who have suffered from his actions.

Orr has said he needs a recession to reset pricing. Construction, food, a lot of things.

Perhaps he's right. That the only realistic way forward is a reset of prices by crushing demand through increasing the cost of the debt. Creative destruction.

But what then? Once everything has collapsed, we go back to suppressing the price of money and start all over again on asset speculation as an economic basis for existence?

start all over again on asset speculation as an economic basis for existence?

Yes - that's the plan - but this time we will improve the recipe for success by selling financial and physical assets to offshore financiers so that they can extract rent from our housing ponzi.

Agreed J.C. good post.

Orr thinks that a recession will be a short cut instead of doing the hard laborious work to restructure the economy, improve supply chains (stop sanctioning key suppliers and participating in trade wars!) and increasing productivity. I bet that he's wrong.

Orr does not have the mandate or toolkit to do any of the things you mention. That is the Govt's role. How are they doing?

I think we can both agree that the last several terms of government have been generally appalling on these counts.

thanks for talking about GDP per capita as the real measure - but why is your headline about gross GDP? It just feeds the false narrative by the politicians that gross GDP is what matters.

thanks for talking about GDP per capita as the real measure - but why is your headline about gross GDP?

GDP per capita has only recently become more relevant as a signpost to the commentariat. Nobody seems to question why the mighty Anglosphere with its open gate strategy is barely doing better or even worse that the likes of Korea and Japan on this measure.

Gdp per capita changes arent even across the board. We have a bigger and bigger pool of hangers on going backwards. Others are meandering while a smaller group are producing more

Who is the small group producing more? What are they producing and how significant is that production to our overall economy?

I only know a small group of business-people but probably a few more across the motu

Gdp per capita changes arent even across the board.

Here's a great example of mainstream media (Aussie) picking up on GDP per capita.

SUNDAY - Why the Australian economy is in crisis mode 🇦🇺

https://omny.fm/shows/ben-fordham-full-show/sunday-why-the-australian-e…

He raises a good point.

But also misses the point that that those at the top continue to suck up the bulk of the profits from the growing aggregate GDP.

Time to start lowering the OCR slowly.

I think when the OCR gets lowered, it will come down quickly. The first drop will probably be 0.25% but as the RB realises how bad the NZ economy is, which is with many months delay, it will drop the OCR in larger cuts.

You are dreaming. The NZ dollar will drop even more causing inflation. It will be slow and sure.

A lower NZD is not necessarily bad, it helps the exporters, that's what we need for a NZ lead recovery.

Anyway, why don't we revisit our predictions in a year's time Ex Agent, and see who got it right ?

Unfortunately the lag between a lower dollar and rising employment/recompense is politically too protracted...and so the powers that be (attempt to) short circuit the process....so much for economic theory.

You cannot ignore reality....for long.

A lower NZD is not necessarily bad, it helps the exporters, that's what we need for a NZ lead recovery.

The collapse in JPYUSD has been a boon for Japanese companies, particularly the trading companies who own assets and commodities all over the world. And even their less obvious exporters like Asics. Japan also has innovation.

Betting on juicier receipts for milk powder and kiwifruit is not particularly ambitious and necessarily enough for a developed economy.

New Zealand export is only 24% of GDP. Imports are 30% of GDP. What will hurt us more when the NZD tanks? I think filling up your tank at gasstation! See:https://data.oecd.org/trade/trade-in-goods-and-services.htm.

Only a few at the top will notice the benefits of a lower NZD because of that low ratio.

All indicators indicate a deterioration over the medium term.. the higher for longer narrative is being played out by all central banks, looks like are fine with a total reset of their economies

Yes if you view the US 10 year bond yield, it’s clearly broken out of a 40 year downward trend (in my view this means that if you view the last 40 years of economic behaviour and results as your version of reality, then be careful that a new version of reality might now be starting - flat or rising rates for decades - if rates go to zero again it means WW3 has started or unemployment is 20% (ie depression) and it won’t be a better world than what we currently live in). We now live in a new world where we can no longer rely on cheaper debt to be the sole source of growth/wealth creation - we might actually have to produce something the world wants to consume/use (other than speculating on house price appreciation).

Spot on.. CB's have realized their experiments of flooding the market with cheap TOXIC debt has only helped the select few

Ha I think it is too soon to make that call. Just wait until the next black swan, then we will see

That right, they all sing from the same sheet...

"CB's have realized their experiments of flooding the market with cheap TOXIC debt has only helped the select few"

Agreed, but I come to a different conclusion to yours, I think that is precisely why they are likely to resume lower rates and QE.

If we want to create a world focused on science and technology we have to somehow hold onto our STEM graduates... at the moment we pay them poorly and our houses cost too much so they leave for a better life.

Maybe the correct thing to do here is to focus on sustainability... though this will never pay off the existing debt.

Out of a recession?

When all that is left is hope.

Out of a recession?

What are the chances?

Dumb and Dumber - One in a Million (youtube.com)

GDP per capital will definitely be negative, but there's worse to come for Q2, Q3 & Q4.

RBNZ lower interest rates to stupidly low levels, economy goes gangbusters and we get inflation. RBNZ raise interest rates to much higher levels and economy cools and inflation dissipates. Yeah maybe it’s a complete fluke, or maybe monetary policy does indeed work exactly as intended.

It's a very blunt tool... but there is no viable alternative ATM

Correlation doesn’t equal causation. They raised rates and inflation has fallen but inflation has fallen globally so it may have happened anyway. Another way to lower prices is to increase competition and for that we need more people running businesses. To run a business you generally need affordable borrowing.

Correct it is a correlation, but often it’s harder to get better evidence. Why change something that seems to be working?

We had very affordable borrowing right before the inflation started!

Ask mortgagee sellers and those made redundant if they think it is working. If you own property out right and have cash in the bank it’s working really well. Good for the boomers but not their kids and grand kids.

Raising rates now back towards historically normal levels isn’t the issue. The issue was allowing house prices to become to highly leveraged relative to productivity/incomes over the past 10 years.

- Even if the RBNZ didn’t control interest rates, they could fluctuate regardless.

- Banks do offer 5 year fixed rates, people susceptible to interest rate fluctuations should have taken those.

- Inflation can destroy an economy if it becomes baked in. Much worse than what we have right now

- I have a mortgage, it’s no fun for me either, but it’s better than runaway inflation

- The real issue is not the current interest rates, it’s the previous interest rates. The RBNZ cocked up, but to be fair no one expected the economy to be so resilient to lockdowns.

- I do feel sorry for those who have been shafted by both low interest rates and high house prices. I hope some lessons are learnt and vulnerable borrowers are forced to break their mortgage into chunks and fix them all with different terms so they get at least 5 years before they are fully exposed. Too much unnecessary regulation around borrowing but the obvious risk was ignored.

Whether it is -0.3% or +0.3% really makes no difference. The net effect is that we're going nowhere fast.

And with no end in sight!

Just as an aside - I expect Stats NZ to be under significant and considerable political pressure to be above zero.

'Just as an aside - I expect Stats NZ to be under significant and considerable political pressure to be above zero'

I fully agree with you. Imports, residential construction, consumer spending, are all below last years Q1 levels. They will need some very good cooks to get the number above zero.

Recession. Next stop is Stagflation.

Higher for Longer baby! 👶

Yep. I would say we are already in the stagflation window.

lol ... You'd both be wildly wrong.

“Wildly”, you sure? Remember that any inflation is still on top of all that went before and we have a ton of people with equity leaving the country which is suppressing the unemployment figures.

Are you waiting around for StatsNZ to report what is happening now?

I have a mortgage, and yes I've refixed on to new rates and we're certainly noticing it. We bought a cheaper first home, so roughly have $360k remaining on our mortgage, and even that is amounting to over $500 a week in interest alone. I don't want to see interest rates come down. I hope they stay at current levels permanently - I never want to see them come down so artificially low ever again. Look at the massive harm very cheap debt, and no regulations has delivered us. As soon as rates come down, we'll see prices shoot up again. I'm hoping through the DTIs actually remain in place. If it does curb lending significantly and people aren't able to borrow at levels similar to today's prices, we will see a big uproar about how it needs to go. Investor groups are already saying 7x DTI isn't enough.

Question regarding people in negative equity needing to refix - I saw an article about 2000 or so first home buyers now being in negative equity, will they not be able to access the special rate when they refix? Seems pretty miserable of the bank if that's the case.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.